China Light Electric Vehicle Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Vehicle Type (Electric Scooters, Electric Bicycles, Electric Motorcycles, Low Speed Electric Vehicles), by Battery Type (Lithium-Ion Batteries, Lead Acid Batteries), by Price Range (Economy, Mid-Range, Premium), by End Use (Personal Mobility, Commercial Logistics, Shared Mobility, Industrial Applications)

| Status : Published | Published On : May, 2026 | Report Code : VRAT9675 | Industry : Automotive & Transportation | Available Format :

|

Page : 112 |

China Light Electric Vehicle Market Overview

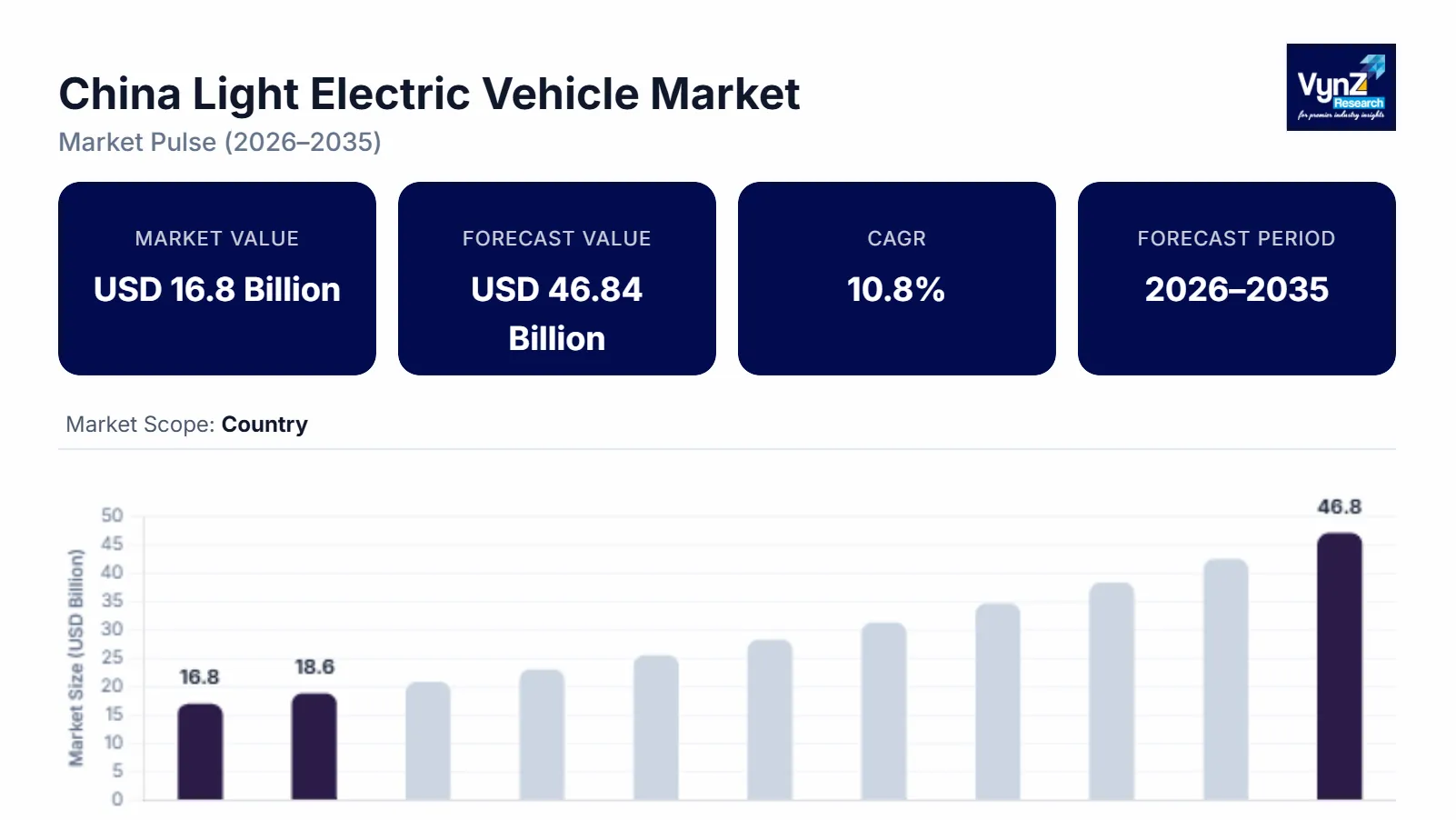

The China Light Electric Vehicle market which was valued at approximately USD 16.8 billion in 2025 and is estimated to rise further up to almost USD 18.6 billion by 2026, is projected to reach around USD 46.84 billion in 2035, expanding at a CAGR of about 10.8% during the forecast period from 2026 to 2035.

Market growth is fueled by increasing urban mobility needs, electric mobility subsidies that are more or less supportive and also by the battery manufacturing capacity that keeps expanding along with the growing adoption of smart, connected mobility solutions. The demand is rising for low-cost urban transport and there are ongoing investments in charging infrastructure and clean transport policies. They receive backing from the Government of China, the Ministry of Industry and Information Technology and the China Association of Automobile Manufacturers which keeps the market expansion rolling across big areas such as Guangdong, Jiangsu and Zhejiang.

China Light Electric Vehicle Market Dynamics

Market Trends

The industry is seeing shifts around battery technology adoption, light weight vehicle integration and how people actually prefer moving around in cities. A big change is the growing adoption of lithium-ion battery powered compact electric scooters and low-speed mobility vehicles. This promotes better energy use, less pollution and cheaper transportation options. Policy direction put out by the Government of China together with the Ministry of Industry and Information Technology has encouraged intelligent, energy efficient electric mobility systems across the entire urban transportation network. There is also an emerging push toward smart connectivity and digital fleet management solutions, which is being driven by fast digitalization and the expansion of intelligent transport infrastructure.

Growth Drivers

The market keeps growing due to steady government support for electric mobility, which helps produce consistent demand for urban commutes and short distance logistics work. Investments in charging infrastructure, battery manufacturing facilities and smart transportation projects are pushing the market further. Green transport and carbon reduction related government initiatives are helping domestic production and consumer acceptance, especially in major manufacturing provinces. Growing worries about fuel prices going up and consumer reflex for budget friendly trips are pushing adoption. For the urban crowd and also for commercial delivery the main focus is operational efficiency along with lower maintenance fees which pushes compact electric scooters, electric bicycles, and lighter city mobility vehicles.

Market Restraints / Challenges

Even with the positive outlook, the market still has issues that can slow expansion. Battery raw material price swings and supply chain dependence are both real factors that limit profitability and market penetration especially for cost sensitive manufacturers or smaller regional suppliers. Since lithium, nickel and imported semiconductor components are involved, procurement uncertainty cause trade disruptions pushing commodity prices up. Another hurdle is regulatory standardization and battery safety compliance which create operational friction. When companies rely on outside battery technologies and when product certification requirements keep evolving, it causes cost pressure, late launches, and scaling problems.

Market Opportunities

The market offers opportunities in urban last mile mobility and intelligent fleet transportation services, especially as urbanization rises, e-commerce keeps expanding and people ask for more sustainable transportation options. Firms that offer affordable, lightweight, connected mobility solutions are in a good position to meet demand from delivery companies, commuting users and shared mobility operators across big metropolitan regions. Clean mobility plans backed by government are also supporting expansion inside smart urban transport ecosystems. There is also a pretty strong opening around battery swap infrastructure and linked electric mobility platforms. With growing investments in digital enabled transportation services, companies enjoy higher margin models and long-term business partnerships.

China Light Electric Vehicle Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 16.8 Billion |

|

Revenue Forecast in 2035 |

USD 46.84 Billion |

|

Growth Rate |

10.8% |

|

Segments Covered in the Report |

Vehicle Type, Battery Type, Price Range, End Use |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

Guangdong, Jiangsu, Zhejiang, Rest of China |

|

Key Companies |

AIMA Technology Group Co. Ltd., Yadea Technology Group, Xiaomi Inc., Jiangsu Xinri E-Vehicle Co., Ltd. (SUNRA), Zhejiang Luyuan Electric Vehicle Co. Ltd |

|

Customization |

Available upon request |

China Light Electric Vehicle Market Segmentation

By Vehicle Type

In 2025 electric scooters took the lead, making up around 38% of total industry revenue, mainly due to lower ownership costs and more people choosing them for short distance trips. Government backed urban mobility ideas and limits placed on fuel powered two wheelers in big Chinese cities have pushed the segment forward. For the forecast period, the segment should keep a near steady pace, roughly 10.4% growth, largely because manufacturers keep putting money into battery efficiency and charging accessibility.

Electric bicycles are projected to hit the highest growth rate of about 11.7% over the forecast period because ecofriendly mobility is becoming more appealing for consumers and penetration is rising in tier 2 and tier 3 cities. There is also expansion in e-commerce delivery operations and local transportation policies pushing the demand.

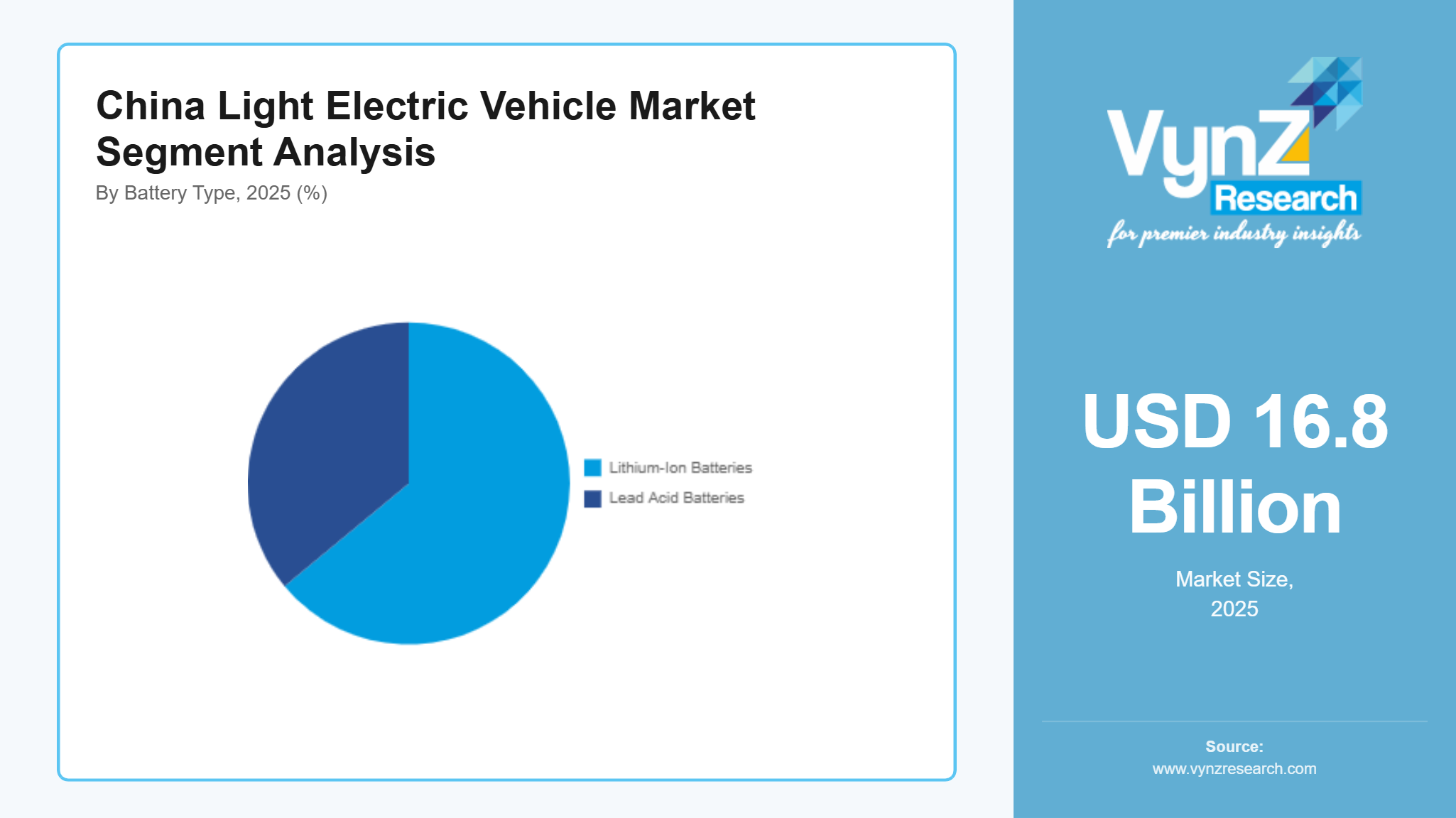

By Battery Type

Lithium-ion batteries were the bigger share in 2025, around 64% of the market, since both manufacturers and consumers keep caring about longer battery life, quicker charging, and higher energy density. Production capacity got a real boost due to strong investments in domestic lithium processing facilities and battery manufacturing infrastructure with support from industrial development authorities in China. The lithium-ion segment is expected to grow about 11.2% CAGR, as integration keeps increasing in premium and connected mobility solutions.

Lead acid batteries will grow at 7.8% CAGR due to lower upfront costs and long-standing supply networks. Adoption of battery swapping systems and intelligent energy management platforms is pushing more companies and users toward advanced technologies, both in commercial and personal mobility.

By Price Range

The economy group lead by volume, representing about 46% of total unit demand in 2025 due to affordability, widespread urban use and heavy participation among students, delivery workers and middle-income consumers. Manufacturers also keep focusing on cost efficient product development and localized production strategies to stay competitive in the mass market segment. The economy category is forecast to grow at nearly 9.6% during the forecast period.

Premium vehicles are expected to grow faster, around 12.4%, driven by rising disposable income, more demand for smart connected vehicles and consumer interest in better safety and battery performance features. Mid-range vehicles continue to gain momentum with urban buyers as it is affordable enough but still offers advanced mobility features.

By End Use

Personal mobility took the lead in 2025, grabbing the biggest revenue portion, around 52% of the whole market as more people are living in cities, traffic congestion is getting worse and lots of commuters are leaning toward economical transportation alternatives. Government backed clean mobility programs lend real support and the charging network for electric vehicles keeps expanding which makes adoption easier in major urban centers like Shanghai, Shenzhen and Beijing. It should keep moving up steadily, roughly 10.1% each year across the forecast window.

Commercial logistics is also picking up and it’s projected to grow at nearly 12.1% CAGR due to fast e-commerce expansion, more food delivery services and an ongoing rise in last mile transportation needs. Fleet operators are also shifting toward lightweight electric vehicles, mainly to lower operating expenses and stay aligned with urban emission reduction policies. Shared mobility and industrial applications are growing at a steadier pace, supported by digital fleet management integration, battery swapping infrastructure and increased investment in smart city transportation systems.

Regional Insights

Guangdong

Guangdong accounted for approximately 32% of the market in 2025, representing nearly USD 4.7 billion in market revenue, driven by strong manufacturing capacity, extensive battery production infrastructure and rising urban transportation demand. Strong demand from Shenzhen, Guangzhou and Dongguan continues to support market growth, particularly across electric scooters and commercial delivery vehicles. The presence of large-scale electric mobility manufacturers and battery suppliers has further strengthened regional production capabilities.

Jiangsu

Jiangsu accounted for approximately 18% of the market in 2025, reaching nearly USD 3.0 billion in value due to expanding industrial activity, rapid urbanization and supportive clean transportation policies. Increasing adoption across urban commuting and shared mobility services is driving consistent demand for lightweight electric vehicles. Major cities including Suzhou, Nanjing and Wuxi continue to witness rising penetration of electric bicycles and low speed mobility vehicles supported by growing middle income consumer populations and improving urban transport infrastructure.

Zhejiang

Growth in Zhejiang contributed approximately 23% of the market in 2025, accounting for nearly USD 3.5 billion in market revenue, supported by rising urban mobility demand, expansion of intelligent manufacturing facilities and increasing consumer awareness regarding low emission transportation alternatives. Cities such as Hangzhou and Ningbo continue to witness increasing deployment of electric scooters and connected lightweight mobility platforms due to rapid digital infrastructure expansion and growing smart city initiatives. Zhejiang is anticipated to register growth of approximately 11.1% during the forecast period.

Rest of China

The rest of China segment accounted for approximately 27% of the market in 2025, representing nearly USD 4.5 billion in market value, supported by increasing urbanization, expanding regional transportation infrastructure and rising adoption of affordable electric mobility solutions across emerging provinces. Growing demand from provinces including Shandong, Henan, Sichuan, Hubei,and Anhui continues to support market expansion, particularly across personal mobility and commercial delivery applications. Improving local manufacturing capabilities and increasing battery supply chain investments are further strengthening regional growth potential.

Competitive Landscape / Company Insights

The market is moderately competitive with the presence of established domestic manufacturers and emerging regional companies focusing on battery innovation, smart mobility integration and production expansion. Companies are increasingly investing in research and development, intelligent vehicle technologies and battery efficiency improvements to strengthen their market position. Supportive industrial policies introduced by the Government of China and the Ministry of Industry and Information Technology are further encouraging local manufacturing and electric mobility innovation. Strategic partnerships, export expansion and connected mobility solutions continue to shape the competitive landscape across the industry.

Mini Profiles

AIMA Technology Group Co. Ltd. focuses on electric scooters, electric bicycles, and urban mobility solutions, supported by strong domestic distribution networks, extensive dealership presence, and cost-efficient manufacturing operations across China.

Changzhou Yufeng Vehicle Co. Ltd. operates in mass market electric mobility segments, emphasizing affordable transportation solutions, product durability, and expanding regional distribution capabilities across urban and semi urban markets.

Jiangsu East Yonsland Vehicle Manufacturing Co. Ltd leverages local manufacturing infrastructure, scalable production capabilities, and expanding logistics partnerships to strengthen market presence within lightweight electric transportation applications.

Xiaomi Inc. focuses on connected electric mobility products and smart transportation technologies, supported by strong digital ecosystem integration, consumer brand recognition, and advanced technology development capabilities.

Yadea Technology Group emphasizes premium electric two wheelers and intelligent mobility platforms, supported by extensive export operations, advanced battery technologies, and strong manufacturing efficiency across global markets.

Key Players

- AIMA Technology Group Co. Ltd.

- Changzhou Yufeng Vehicle Co. Ltd.

- Jiangsu East

- Yonsland

- Vehicle Manufacturing Co. Ltd

- Jiangsu

- Kingbon

- Vehicle Co. Ltd

- Jiangsu

- Xinri

- E-Vehicle Co., Ltd. (SUNRA)

- Xiaomi Inc.

- Yadea

- Technology Group

- Zhejiang

- Luyuan

- Electric Vehicle Co. Ltd

- Zhejiang Taotao Vehicles Co. Ltd.

- Zuboo

- Technology Co. Ltd.

Recent Developments

In March 2025, Jiangsu Xinri E-Vehicle Co., Ltd. (SUNRA) expanded its intelligent electric scooter portfolio with upgraded lithium battery models targeting urban commuting applications. The company also strengthened dealer partnerships across eastern China to improve distribution efficiency and regional market penetration.

In June 2025, Xiaomi Inc. expanded its electric vehicle manufacturing footprint through a new land acquisition in Beijing to support future EV production capacity. The company further accelerated investments in intelligent mobility technologies and automated manufacturing systems.

In November 2025, Yadea Technology Group introduced the new Yadea Velax electric motorcycle and a full scenario charging ecosystem during EICMA 2025. The launch highlighted the company’s focus on high-performance charging technologies and global electric mobility expansion strategies.

In April 2025, Zhejiang Luyuan Electric Vehicle Co. Ltd increased investments in advanced battery safety technologies and lightweight vehicle production capabilities for domestic urban mobility markets. The company also expanded its retail presence across multiple tier 2 cities to strengthen consumer accessibility.

In February 2026, Jiangsu Kingbon Vehicle Co. Ltd strengthened its commercial electric mobility portfolio through the introduction of upgraded low speed electric transport solutions for logistics applications. The company additionally focused on expanding regional manufacturing capacity to support increasing domestic demand for affordable electric transportation.

China Light Electric Vehicle Market Coverage

Vehicle Type Insight and Forecast 2026 - 2035

- Electric Scooters

- Electric Bicycles

- Electric Motorcycles

- Low Speed Electric Vehicles

Battery Type Insight and Forecast 2026 - 2035

- Lithium-Ion Batteries

- Lead Acid Batteries

Price Range Insight and Forecast 2026 - 2035

- Economy

- Mid-Range

- Premium

End Use Insight and Forecast 2026 - 2035

- Personal Mobility

- Commercial Logistics

- Shared Mobility

- Industrial Applications

China Light Electric Vehicle Market by Region

- Guangdong

- By Vehicle Type

- By Battery Type

- By Price Range

- By End Use

- Jiangsu

- By Vehicle Type

- By Battery Type

- By Price Range

- By End Use

- Zhejiang

- By Vehicle Type

- By Battery Type

- By Price Range

- By End Use

- Rest of China

- By Vehicle Type

- By Battery Type

- By Price Range

- By End Use

Table of Contents for China Light Electric Vehicle Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Vehicle Type

1.2.2. By

Battery Type

1.2.3. By

Price Range

1.2.4. By

End Use

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. China Market Estimate and Forecast

4.1. China Market Overview

4.2. China Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Vehicle Type

5.1.1. Electric Scooters

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Electric Bicycles

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Electric Motorcycles

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Low Speed Electric Vehicles

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.2. By Battery Type

5.2.1. Lithium-Ion Batteries

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Lead Acid Batteries

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Price Range

5.3.1. Economy

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Mid-Range

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Premium

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.4. By End Use

5.4.1. Personal Mobility

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Commercial Logistics

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Shared Mobility

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Industrial Applications

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

6. Guangdong Market Estimate and Forecast

6.1. By

Vehicle Type

6.2. By

Battery Type

6.3. By

Price Range

6.4. By

End Use

7. Jiangsu Market Estimate and Forecast

7.1. By

Vehicle Type

7.2. By

Battery Type

7.3. By

Price Range

7.4. By

End Use

8. Zhejiang Market Estimate and Forecast

8.1. By

Vehicle Type

8.2. By

Battery Type

8.3. By

Price Range

8.4. By

End Use

9. Rest of China Market Estimate and Forecast

9.1. By

Vehicle Type

9.2. By

Battery Type

9.3. By

Price Range

9.4. By

End Use

10. Company Profiles

10.1.

AIMA Technology Group Co. Ltd.

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Changzhou Yufeng Vehicle Co. Ltd.

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Jiangsu East

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Yonsland

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Vehicle Manufacturing Co. Ltd

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Jiangsu

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Kingbon

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Vehicle Co. Ltd

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Jiangsu

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Xinri

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

E-Vehicle Co., Ltd. (SUNRA)

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

10.12.

Xiaomi Inc.

10.12.1.

Snapshot

10.12.2.

Overview

10.12.3.

Offerings

10.12.4.

Financial

Insight

10.12.5.

Recent

Developments

10.13.

Yadea

10.13.1.

Snapshot

10.13.2.

Overview

10.13.3.

Offerings

10.13.4.

Financial

Insight

10.13.5.

Recent

Developments

10.14.

Technology Group

10.14.1.

Snapshot

10.14.2.

Overview

10.14.3.

Offerings

10.14.4.

Financial

Insight

10.14.5.

Recent

Developments

10.15.

Zhejiang

10.15.1.

Snapshot

10.15.2.

Overview

10.15.3.

Offerings

10.15.4.

Financial

Insight

10.15.5.

Recent

Developments

10.16.

Luyuan

10.16.1.

Snapshot

10.16.2.

Overview

10.16.3.

Offerings

10.16.4.

Financial

Insight

10.16.5.

Recent

Developments

10.17.

Electric Vehicle Co. Ltd

10.17.1.

Snapshot

10.17.2.

Overview

10.17.3.

Offerings

10.17.4.

Financial

Insight

10.17.5.

Recent

Developments

10.18.

Zhejiang Taotao Vehicles Co. Ltd.

10.18.1.

Snapshot

10.18.2.

Overview

10.18.3.

Offerings

10.18.4.

Financial

Insight

10.18.5.

Recent

Developments

10.19.

Zuboo

10.19.1.

Snapshot

10.19.2.

Overview

10.19.3.

Offerings

10.19.4.

Financial

Insight

10.19.5.

Recent

Developments

10.20.

Technology Co. Ltd.

10.20.1.

Snapshot

10.20.2.

Overview

10.20.3.

Offerings

10.20.4.

Financial

Insight

10.20.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

China Light Electric Vehicle Market