Aerospace Wiring Harness Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Aircraft Type (Commercial Aircraft, Military Aircraft, Business & General Aviation Aircraft, Unmanned Aerial Vehicles (UAVs), Advanced Air Mobility (AAM) / eVTOL Aircraft), by Component (Wires & Cables, Connectors, Terminals, Clamps, Others), by Material (Copper, Aluminum, Fiber Optics), by Application (Avionics, Flight Control Systems, Power Distribution Systems, Lighting Systems, Data Transmission Systems, Cabin Systems), by End User (Original Equipment Manufacturers (OEMs), Maintenance, Repair and Overhaul)

| Status : Published | Published On : Mar, 2026 | Report Code : VRAD12048 | Industry : Aerospace and Defense | Available Format :

|

Page : 195 |

Aerospace Wiring Harness Market Overview

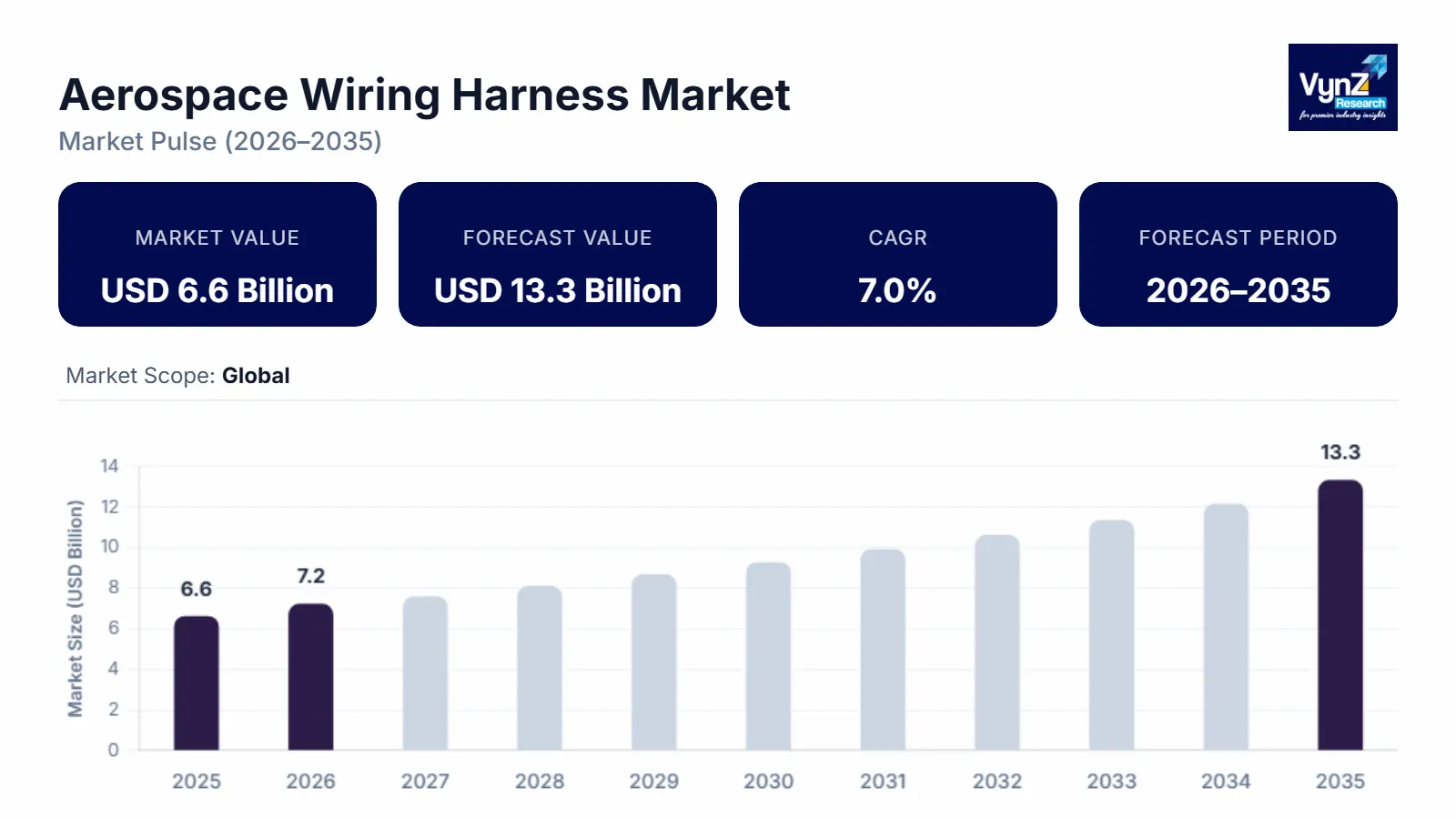

The aerospace wiring harness market which was valued at approximately USD 6.6 billion in 2025 and is estimated to reach around USD 7.2 billion in 2026, is projected to reach close to USD 13.3 billion by 2035, expanding at a CAGR of about 7.0% during the forecast period from 2026 to 2035.

The market is primarily driven by the increasing production of commercial and military aircraft worldwide, as modern aircraft rely heavily on complex electrical systems for avionics, communication, navigation, and in-flight entertainment. The adoption of more electric architecture (MEA) aircrafts is rapidly expanding the need to have advanced types of wiring harness systems capable of supporting higher power distribution and data transfer. Also, due to the development of the international air passenger traffic, the airlines are growing, which directly stimulates the increase in the aircraft wiring infrastructure. The ever-growing technological developments in the avionics, sensors, and on-board electronics are also making the wiring harnesses assemblies in the aircraft even more complex and bulky. Increased demand in the wiring systems that offer reliability and composite weight is another issue that is boosted by the growth of defense modernization systems and the acquisition of the next-generation fighter jets, drones, and surveillance aircraft.

In addition, the growing attention to aircraft weight savings and fuel efficiency is pushing the manufacturers to produce high-performance lightweight wiring harness products. The increased use of electric and hybrid-electric propulsion systems in the aviation industry is also increasing the demand of special high-voltage wiring systems. Increasing focus on the retrofitting and maintenance, repair and overhaul (MRO) activities in aircraft is also generating steady demand of replacement wiring harness components in aging aircraft fleets.

Aerospace Wiring Harness Market Dynamics

Market Trends

The increasing adoption of more electric aircraft (MEA) architecture is a major trend shaping the aerospace wiring harness market. MEA systems replace traditional hydraulic, pneumatic, and mechanical components with electrically powered systems to improve efficiency, reliability, and aircraft performance. As aircraft manufacturers integrate electrically driven subsystems such as flight control systems, environmental control systems, and landing gear operations, the demand for advanced wiring harnesses capable of handling higher power loads and complex data transmission increases. This transition significantly expands the amount of electrical wiring required within modern aircraft. The Government of the United Kingdom has committed £113 million in funding to accelerate the development of emission-free electric aircraft and electrified aviation technologies. This funding supports research into electric propulsion, energy storage, and advanced electrical systems that form the foundation of MEA architecture. Additionally, MEA architecture helps reduce overall aircraft weight and improves fuel efficiency, making it highly attractive for both commercial and military aviation sectors. The growing development of next-generation aircraft platforms and electric propulsion technologies further accelerates the need for high-performance wiring harness systems.

Growth Drivers

The increasing global aircraft production and fleet expansion is a major driver of the aerospace wiring harness market. Growing air passenger traffic and rising demand for air cargo services are encouraging airlines to expand and modernize their fleets with new aircraft. Commercial aircraft manufacturers like The Boeing Company and Airbus SE are opening factories at an accelerated rate to cope with the high demand of commercial aircraft in the international market. Every plane is fitted with massive wiring harnesses to accommodate avionics, power distribution, communication, communication, lighting and in-flight entertainment. With the increasing sophistication of the electronic systems incorporated into the new aircraft models, the wiring harnesses are becoming increasingly complicated and larger in size. The Government of Quebec partnered with Airbus to accelerate production of the A220 commercial aircraft, committing approximately $300 million as part of a joint investment plan to expand manufacturing capacity. Airbus also invested about $900 million, enabling increased production rates of the aircraft. Additionally, Asian-Pacific and the Middle East aviation markets are emerging, which is also adding to the new aircraft orders and fleet growth. New electrical architecture is also sought after due to the replacement of old aircraft with modern and fuel-efficient models.

Market Restraints / Challenges

The high manufacturing and installation costs of aerospace wiring harness systems represent a significant challenge for the market. Aerospace wiring harnesses must meet strict aviation safety and performance standards, which require the use of specialized materials, high-precision manufacturing processes, and rigorous quality testing. Such harness systems are very much airplane (model)-specific, which makes them more expensive to engineer and develop. Besides this, wiring harnesses installation in aircraft bodies is a labor-intensive job as it needs qualified technicians to make sure, they are properly routed, insulated and cushioned against vibration, heat, and electromagnetic interference. The production costs are further aggravated by the requirement of lightweight but resilient materials like high-grade aluminum, copper alloys, and high-level insulation compounds. The certification and adherence to global aviation standards are also associated with the increase of overall costs and development schedules. In addition, changing design in the production of the aircraft may cause extra installation and testing costs.

Market Opportunities

The growing development of electric and hybrid-electric aircraft is creating significant opportunities for the aerospace wiring harness market. As the aviation industry focuses on reducing carbon emissions and improving energy efficiency, aircraft manufacturers are increasingly investing in electric propulsion technologies. Electric and hybrid-electric airplanes are dependent on advanced electrical architectures and high-voltage wiring-harness systems are needed to deliver power to the propulsion system, the battery, and other electrical propulsion systems. Such designs of aircraft are normally associated with more elaborate wiring networks than the traditional aircraft, which puts a strain on the use of special wiring harness solutions. The U.S. Department of Energy’s Advanced Research Projects Agency–Energy (ARPA-E) allocated $33 million in funding to support research projects focused on developing hybrid-electric aviation technologies. Moreover, the creation of electric regional aircraft, urban air mobility vehicles and eVTOL platforms are further growing the demand of lightweight and high-capacity wiring systems. Technology developers and aerospace companies are busy developing next-generation prototypical electric aircrafts that will need novel electrical integration.

Global Aerospace Wiring Harness Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 6.6 Billion |

|

Revenue Forecast in 2035 |

USD 13.3 Billion |

|

Growth Rate |

7.0% |

|

Segments Covered in the Report |

Aircraft Type, Component, Material, Application, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia-Pacific, Rest of the World |

|

Key Companies |

TE Connectivity Ltd., GKN Aerospace Services Limited, Amphenol Corporation, Yazaki Corporation, Glenair, Inc., kSARIA Corporation, Latecoere S.A., Carlisle Interconnect Technologies, Amphenol Aerospace, HarcoSemco LLC, Interconnect Wiring L.L.P., Japan Aviation Electronics Industry, Ltd. |

|

Customization |

Available upon request |

Aerospace Wiring Harness Market Segmentation

By Aircraft Type

Commercial aircraft is the largest category with a market share of about 45% in 2025, since the production volume of passenger aircraft is high and there is a constant growth in airline fleets around the world. Aircrafts use wiring harnesses, which are large due to the use of avionics, cabin systems, lighting, communication, and entertainment in the aircraft. The demand of advanced electrical infrastructure is greatly influenced by increasing air passenger traffic and investments that airline companies have made in modern aircraft models. Large aircraft manufacturers are ordering in large quantities to fill backlog on orders, and this directly adds to wiring harnesses.

Unmanned Aerial Vehicles (UAVs) is the fastest-growing category with a CAGR of 7.2% during the forecast period, owing to the high rate of drone applications in the defense, surveillance, logistics, and inspection processes. UAVs are based on wiring harness systems that are small and lightweight to make flight control systems, sensors, navigation systems and communication equipment. The rising military expenditures in high-tech drones and the increasing number of UAVs used during commercial operations are boosting the growth of the market. There is also growing complexity in wiring of drones due to technological advancement in autonomous flight and miniaturized electronics.

By Component

Wires & Cables is the largest category with a market share of about 50% in 2025, as they form the fundamental structure of aerospace wiring harness systems. These components are responsible for transmitting electrical power, signals, and data throughout aircraft systems. Aircraft contain thousands of meters of wires and cables that support avionics, navigation systems, lighting, communication equipment, and cabin electronics. Increasing integration of electronic subsystems in modern aircraft is further expanding the volume of wiring required. High-performance insulation materials and shielding technologies are also being adopted to ensure reliability under extreme operating conditions.

Connectors is the fastest-growing category with a CAGR of 7.5% during the forecast period, due to the increasing complexity of aircraft electrical systems and the need for reliable electrical connections. Connectors ensure secure transmission of power and signals between different aircraft subsystems and electronic modules. The growing adoption of advanced avionics, sensors, and digital communication networks is increasing the number of connectors required in aircraft wiring architectures. Additionally, manufacturers are developing lightweight and high-performance connectors that can withstand vibration, temperature variations, and harsh aerospace environments.

By Material

Copper is the largest category with a market share of about 75% in 2025, because of its better conductivity of electricity, durability and reliability of the electrical system of aerospace. Copper is an extensively utilized wiring across aircraft due to its ability to deliver effective power relay and high corrosion and mechanical resistance. It is especially relevant in avionics system, power delivery networks and communication circuits where regular electrical operation is necessary. Copper has still been used by aerospace related manufacturers because it has been tested to be stable in operation even under severe environmental conditions.

Fiber Optics is the fastest-growing category with a CAGR of 7.7% during the forecast period, due to the rising demand on high-speed data transmission and lightweight wiring systems in aircrafts. Fiber optic cables have high speed capacity and can pass large amounts of data a long distance with minimal electromagnetic radiations as opposed to use of copper wire. These features render them very appropriate in sophisticated avionics systems, in-flight entertainment and in-flight communications networks.

By Application

Avionics is the largest category with a market share of about 30% in 2025, as avionics systems require extensive electrical connectivity to support navigation, communication, monitoring, and flight management operations. These systems rely on complex wiring harness networks to ensure reliable data exchange between sensors, cockpit instruments, and control units. Modern aircraft incorporate increasingly sophisticated avionics technologies to enhance safety, operational efficiency, and automation. The growing adoption of digital flight control systems and integrated cockpit displays is further increasing wiring complexity. Additionally, avionics upgrades and retrofitting projects are driving demand for advanced wiring harness solutions.

Data Transmission Systems is the fastest-growing category during the forecast period, driven by the increasing use of digital communication networks and connected aircraft technologies. Modern aircraft generate large volumes of operational and passenger data that must be transmitted quickly and reliably between onboard systems. High-speed data transmission is required for applications such as real-time aircraft monitoring, advanced navigation systems, and in-flight connectivity services. The growing adoption of fiber optic networks and advanced digital avionics platforms is further increasing demand for specialized wiring systems.

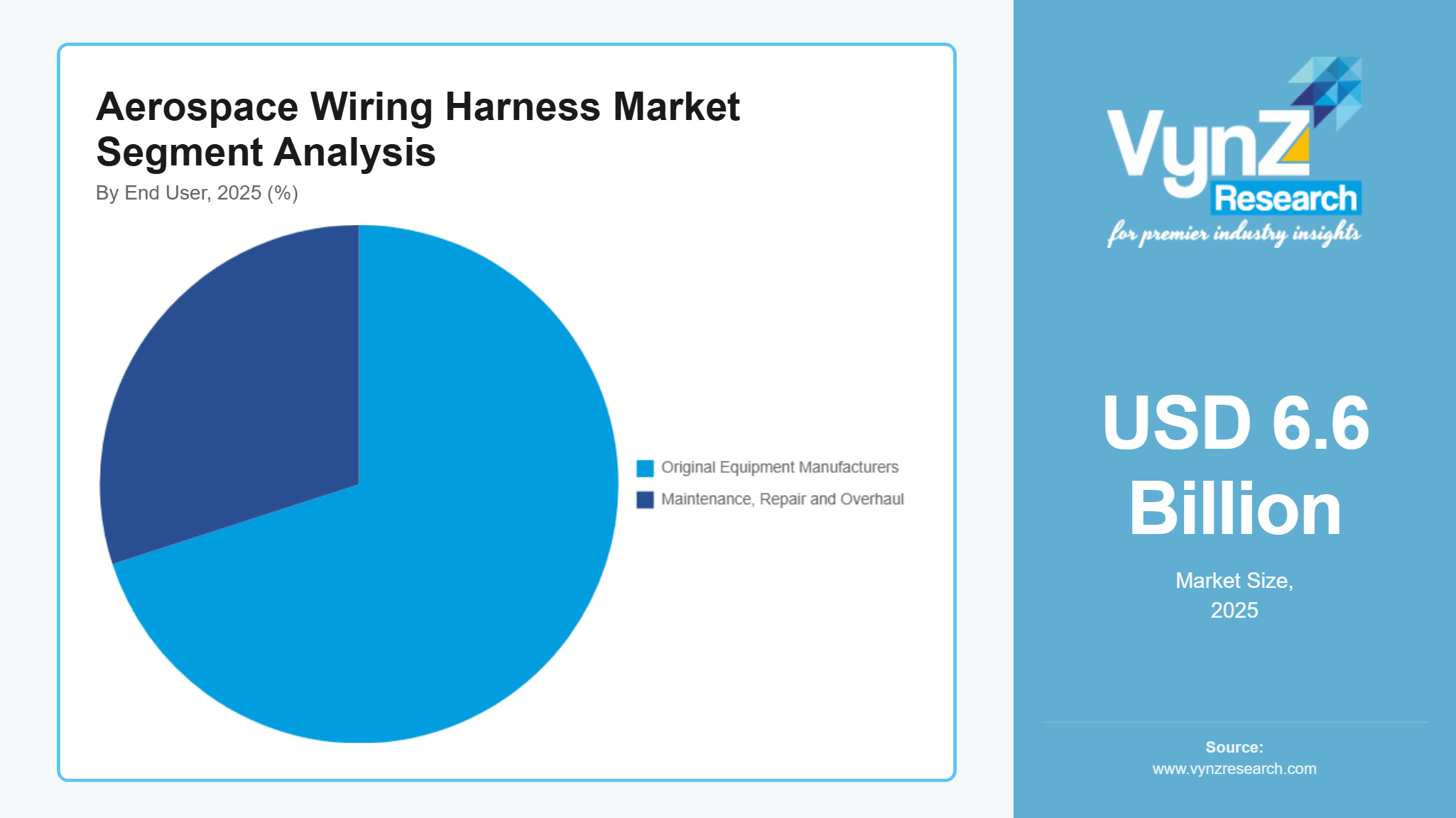

By End User

Original Equipment Manufacturers (OEMs) is the largest category with a market share of around 70% in 2025, because of the high demand of wiring harness installations when the new aircraft are being manufactured. The assembly of aircraft needs the widespread incorporation of the electrical systems, so OEMs are the major users of wiring harnesses solutions. The growth of aircraft manufacturing in the world, and huge order books are putting pressure on the manufacturers of these harness wiring needs. Wiring systems are also demanded by aircraft manufacturers that are specifically designed around a particular aircraft platform.

Maintenance, Repair, and Overhaul (MRO) is the fastest-growing category during the forecast period, due to increasing number of aircrafts in the world and replacement of old electrical systems and maintenance. Wiring harnesses may deteriorate over time because of vibration, exposure to temperatures or operational stress and need to be inspected and replaced periodically. Airlines and defense operators are working on maintenance programs to make sure their aircrafts are safe and efficient in their operation. The growing old of many aircraft fleet in most parts is also contributing to the increased demand wiring system maintenance.

Regional Insights

North America

North America is the largest regional market for the aerospace wiring harness market, supported by the presence of major aircraft manufacturers, strong defense spending, and advanced aerospace manufacturing capabilities. The United States leads the region with extensive aircraft production, large defense aviation programs, and continuous technological innovation in avionics and aircraft electrical systems. The Boeing Company and Lockheed Martin Corporation are major aerospace companies that have a huge input to the need of sophisticated wiring harness system in the region. Aerospace component and electrical system supply chain is also well-established in the region. Market growth is further being supported by the increasing investments in the next-generation aircraft, space exploration programs, and modernization of the military. National Aeronautics and Space Administration (NASA) launched the Electric Powertrain Flight Demonstration (EPFD) project, awarding about $253 million to companies such as GE Aerospace and MagniX to develop hybrid-electric propulsion systems. In addition, the Advanced Research Projects Agency–Energy (ARPA-E) announced up to $55 million in funding to support electric aviation technologies such as electric motors and lightweight powertrains. The Federal Aviation Administration (FAA) is also modernizing U.S. aviation infrastructure through the NextGen program, which has already invested over $14 billion to upgrade air traffic systems.

Asia-Pacific

Asia-Pacific is the fastest-growing region in the aerospace wiring harness market, driven by rapid expansion of the aviation industry, increasing aircraft procurement, and growing domestic aerospace manufacturing capabilities. Countries such as China, India, Japan, and South Korea are investing heavily in aviation infrastructure, aircraft production, and defense modernization programs. Rising air passenger traffic in the region is encouraging airlines to expand their fleets, which increases demand for aircraft electrical systems and wiring harness assemblies. The Government of India is investing heavily in domestic aircraft manufacturing through the Regional Transport Aircraft (RTA) program, aimed at developing a locally produced 80–100 seat passenger aircraft. The government is expected to allocate around ₹12,511 crore (about $1.36 billion) to establish a special-purpose vehicle responsible for aircraft development, certification, and production infrastructure. China’s domestic aircraft development initiatives and India’s expanding defense aviation programs are also supporting regional market growth. Additionally, the emergence of regional aerospace manufacturers and growing partnerships with global aerospace companies are strengthening supply chain capabilities. Continuous investments in advanced aviation technologies and aircraft manufacturing facilities are expected to accelerate the demand for aerospace wiring harness systems across Asia-Pacific.

Europe

Europe maintains a strong presence in the aerospace wiring harness market due to its advanced aerospace industry and strong focus on aircraft innovation and sustainability. Countries such as Germany, France, and the United Kingdom host major aerospace manufacturing hubs and component suppliers. Airbus SE, the leading manufacturer of aircraft, is important in the growth of demand in wiring harness system by manufacturing commercial flights and the next generation aircraft technology. Electric and hybrid-electric aircraft development is also going on in the region as a way of minimizing aviation emissions. Also, the advanced aerospace supply chain and deep cooperation between research institutions and industry participants in Europe facilitate the constant innovation. The United Kingdom government announced a £250 million ($340 million) investment to support research and development in sustainable aviation technologies. The funding supports projects led by aerospace companies and universities focusing on zero-emission aircraft, hydrogen propulsion, lightweight aircraft structures, and advanced manufacturing technologies. The governmental investment in aviation research and sustainable aviation programs also leads to growth of the market in the region.

Rest of the World

The rest of the world, including Latin America, the Middle East, and Africa, is experiencing steady growth in the aerospace wiring harness market as aviation infrastructure and defense capabilities expand. UAE and Saudi Arabia are some of the nations in the Middle East that are investing heavily in developing airline fleet and aviation infrastructures to facilitate the growing passenger traffic. Latin American states like Brazil are consolidating their aerospace production base and defense aviation. The African aerospace industry is slowly growing as more investments are made in airport construction and the growth of the airlines in the region. Increasing defense acquisition initiatives and the level of interest in unmanned aerial systems is also adding to aircraft electrical system demand. The Government of Saudi Arabia is investing over $100 billion in its aviation sector under the Vision 2030 strategy to transform the country into a global aviation hub. The plan includes airport expansion, airline development, and aviation infrastructure modernization, with major projects such as the $30 billion King Salman International Airport in Riyadh. These investments are expected to increase aircraft operations and fleet expansion, which will drive demand for advanced avionics systems and aerospace wiring harness components used in modern aircraft. Even though the manufacturing base in these areas are still maturing in the aerospace, further aviation investments and modernization programs should help facilitate slow market growth.

Competitive Landscape / Company Insights

The aerospace wiring harness market is moderately consolidated, characterized by the presence of global aerospace component manufacturers and specialized electrical system providers that focus on high-reliability aviation connectivity solutions. Major companies such as Safran S.A. and Collins Aerospace maintain strong market positions through their extensive aerospace product portfolios, integrated avionics systems, and long-standing partnerships with leading aircraft manufacturers. These companies provide entire electrical interconnection systems, wiring harness assemblies, connectors and high-performance cables that are engineered to be resistant to extreme aerospace operating conditions. Their international production capacity and long-term supply contracts with aircraft manufacturers help them to have considerable competitive advantages.

Other interconnect and component manufacturers like TE Connectivity Ltd. and Amphenol Corporation are focused on specialized interconnect and component products that compete by offering some of the highest-level solutions including connectors, terminals, and lightweight wiring solutions, which are compatible with the current electrical architecture of an aircraft. Such businesses are very concerned with the area of innovation, creation of high-speed data transmission network, fiber optic interconnections, and ruggedized connectors that serve next generation avionics and digital plane platform.

Mini Profiles

TE Connectivity Ltd. develops high-performance connectivity and sensor solutions for aerospace electrical systems, including advanced connectors, terminals, and wiring harness components designed to operate in extreme aviation environments.

GKN Aerospace Services Limited is a major aerospace supplier providing advanced electrical wiring interconnection systems (EWIS), aerostructures, and engine components for commercial, defense, and space aircraft programs worldwide.

Amphenol Corporation manufactures a wide range of aerospace interconnect products including connectors, cables, and wiring harness systems used in avionics, communication systems, and aircraft power distribution networks.

Yazaki Corporation produces advanced wiring harness systems and electrical components used in aerospace and automotive applications, focusing on high-reliability electrical connectivity and lightweight harness technologies.

Glenair, Inc. specializes in high-reliability connectors, fiber optic interconnect systems, and advanced wiring harness solutions designed for demanding aerospace, defense, and space environments.

Key Players

- TE Connectivity Ltd.

- GKN Aerospace Services Limited

- Amphenol Corporation

- Yazaki Corporation

- Glenair, Inc.

- kSARIA Corporation

- Latecoere S.A.

- Carlisle Interconnect Technologies

- Amphenol Aerospace

- HarcoSemco LLC

- Interconnect Wiring L.L.P.

- Japan Aviation Electronics Industry, Ltd.

Recent Developments

In January 2026, TE Connectivity Ltd. announced the expansion of its aerospace interconnect manufacturing facility in Europe to support rising demand for high-reliability connectors and wiring systems used in next-generation commercial and defense aircraft.

In December 2025, Amphenol Corporation introduced a new lightweight high-speed aerospace connector platform designed to support advanced avionics networks and high-bandwidth aircraft data transmission systems.

In October 2025, GKN Aerospace Services Limited announced a collaboration with major aircraft manufacturers to develop advanced electrical wiring interconnection systems for more electric aircraft architectures and future hybrid-electric aviation platforms.

In August 2025, Latecoere S.A. secured a long-term contract to supply electrical wiring interconnection systems for next-generation commercial aircraft programs, strengthening its position in aircraft electrical architecture integration.

In June 2025, Carlisle Interconnect Technologies launched a new range of high-temperature aerospace cables and wiring harness solutions designed to support high-power electrical systems and advanced avionics in modern aircraft platforms.

Global Aerospace Wiring Harness Market Coverage

Aircraft Type Insight and Forecast 2026 - 2035

- Commercial Aircraft

- Military Aircraft

- Business & General Aviation Aircraft

- Unmanned Aerial Vehicles (UAVs)

- Advanced Air Mobility (AAM) / eVTOL Aircraft

Component Insight and Forecast 2026 - 2035

- Wires & Cables

- Connectors

- Terminals

- Clamps

- Others

Material Insight and Forecast 2026 - 2035

- Copper

- Aluminum

- Fiber Optics

Application Insight and Forecast 2026 - 2035

- Avionics

- Flight Control Systems

- Power Distribution Systems

- Lighting Systems

- Data Transmission Systems

- Cabin Systems

End User Insight and Forecast 2026 - 2035

- Original Equipment Manufacturers (OEMs)

- Maintenance

- Repair and Overhaul

Global Aerospace Wiring Harness Market by Region

- North America

- By Aircraft Type

- By Component

- By Material

- By Application

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Aircraft Type

- By Component

- By Material

- By Application

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Aircraft Type

- By Component

- By Material

- By Application

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Aircraft Type

- By Component

- By Material

- By Application

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Aerospace Wiring Harness Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Aircraft Type

1.2.2. By

Component

1.2.3. By

Material

1.2.4. By

Application

1.2.5. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Aircraft Type

5.1.1. Commercial Aircraft

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Military Aircraft

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Business & General Aviation Aircraft

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Unmanned Aerial Vehicles (UAVs)

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Advanced Air Mobility (AAM) / eVTOL Aircraft

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.2. By Component

5.2.1. Wires & Cables

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Connectors

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Terminals

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Clamps

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. Others

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.3. By Material

5.3.1. Copper

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Aluminum

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Fiber Optics

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.4. By Application

5.4.1. Avionics

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Flight Control Systems

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Power Distribution Systems

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Lighting Systems

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Data Transmission Systems

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

5.4.6. Cabin Systems

5.4.6.1. Market Definition

5.4.6.2. Market Estimation and Forecast to 2035

5.5. By End User

5.5.1. Original Equipment Manufacturers (OEMs)

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Maintenance

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Repair and Overhaul

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Aircraft Type

6.2. By

Component

6.3. By

Material

6.4. By

Application

6.5. By

End User

6.5.1.

U.S. Market Estimate and Forecast

6.5.2.

Canada Market Estimate and Forecast

6.5.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Aircraft Type

7.2. By

Component

7.3. By

Material

7.4. By

Application

7.5. By

End User

7.5.1.

Germany Market Estimate and Forecast

7.5.2.

France Market Estimate and Forecast

7.5.3.

U.K. Market Estimate and Forecast

7.5.4.

Italy Market Estimate and Forecast

7.5.5.

Spain Market Estimate and Forecast

7.5.6.

Russia Market Estimate and Forecast

7.5.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Aircraft Type

8.2. By

Component

8.3. By

Material

8.4. By

Application

8.5. By

End User

8.5.1.

China Market Estimate and Forecast

8.5.2.

Japan Market Estimate and Forecast

8.5.3.

India Market Estimate and Forecast

8.5.4.

South Korea Market Estimate and Forecast

8.5.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Aircraft Type

9.2. By

Component

9.3. By

Material

9.4. By

Application

9.5. By

End User

9.5.1.

Brazil Market Estimate and Forecast

9.5.2.

Saudi Arabia Market Estimate and Forecast

9.5.3.

South Africa Market Estimate and Forecast

9.5.4.

U.A.E. Market Estimate and Forecast

9.5.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

TE Connectivity Ltd.

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

GKN Aerospace Services Limited

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Amphenol Corporation

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Yazaki Corporation

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Glenair, Inc.

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

kSARIA Corporation

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Latecoere S.A.

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Carlisle Interconnect Technologies

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Amphenol Aerospace

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

HarcoSemco LLC

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

Interconnect Wiring L.L.P.

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

10.12.

Japan Aviation Electronics Industry, Ltd.

10.12.1.

Snapshot

10.12.2.

Overview

10.12.3.

Offerings

10.12.4.

Financial

Insight

10.12.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Aerospace Wiring Harness Market