U.S. TIC Market for Aerospace & Aviation Industry Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Service Type (Testing, Inspection, Certification), by Sourcing Type (In house, Outsourced), by End Use (Aerospace manufacturing, Commercial aviation, Defense aviation)

| Status : Published | Published On : Apr, 2026 | Report Code : VRAD12049 | Industry : Aerospace and Defense | Available Format :

|

Page : 129 |

U.S. TIC Market for Aerospace & Aviation Industry Overview

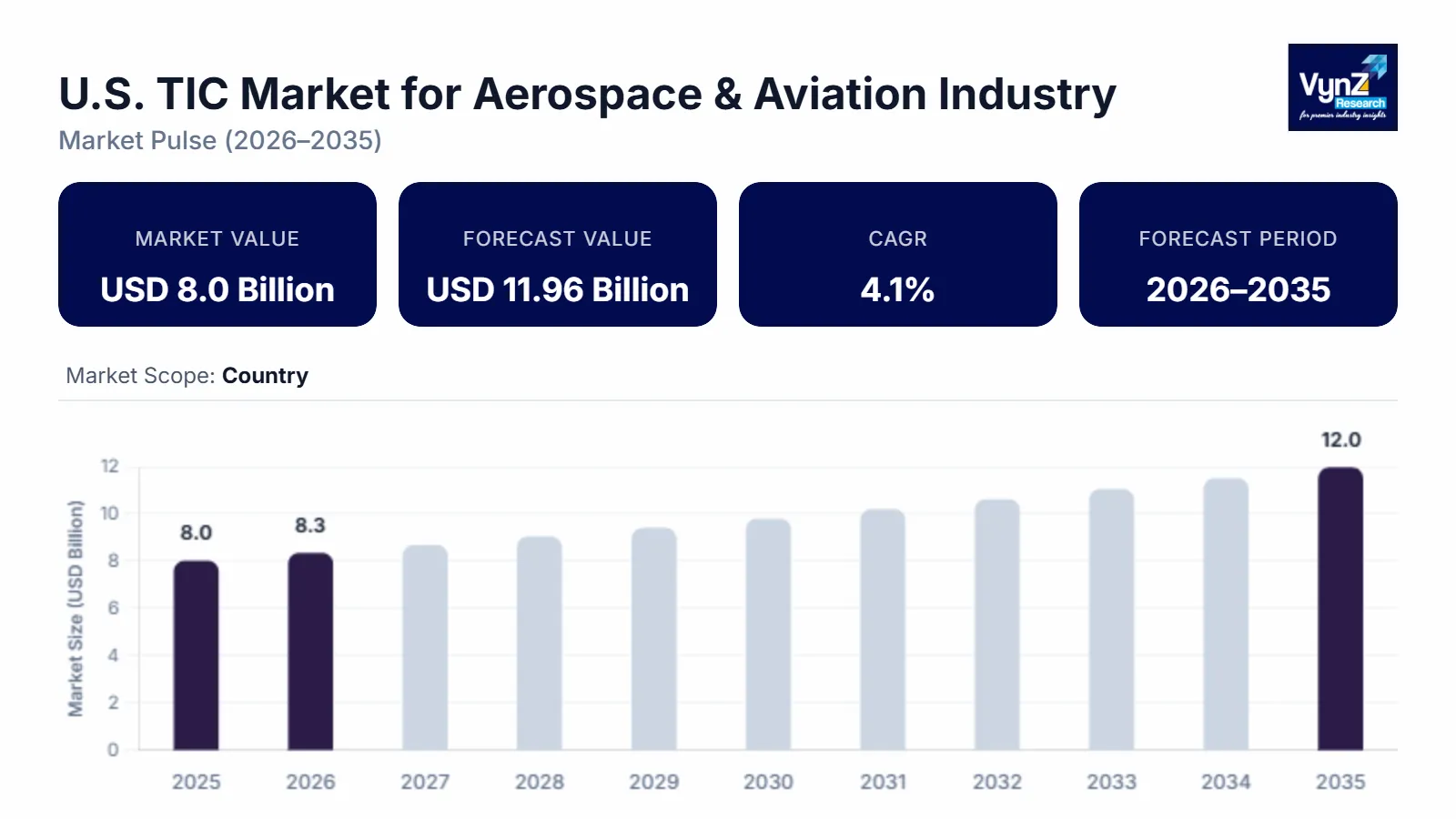

The U.S. TIC market for aerospace and aviation industry which was valued at approximately USD 8.0 billion in 2025 and is estimated to rise further up to almost USD 8.25 billion by 2026, is projected to reach around USD 11.96 billion by 2035, expanding at a CAGR of about 4.1% during the forecast period from 2026 to 2035.

The market experiences growth through three drivers which are strict regulatory requirements, more complicated aircraft systems, and increased demand for testing and certification services which testing organizations use for their work. The TIC services now handle more commercial and defense aviation safety validation requirements because the demand for safety validation has increased across both sectors.

The combination of government supported frameworks and aviation safety standards creates a foundation for market growth which regulatory bodies such as the Federal Aviation Administration use to enforce compliance with mandatory inspection and certification procedures. The International Civil Aviation Organization established global benchmarks which create a basis for standardized safety practices that increase the need for standardized TIC services. The market continues to grow because aircraft fleet modernization investments and maintenance infrastructure development work continue in California, Texas and Washington across important regions.

Top of Form

Bottom of Form

U.S. TIC Market for Aerospace & Aviation Industry Dynamics

Market Trends

The industry is currently undergoing a fundamental transition toward digital inspection methods and sophisticated quality assurance systems which operate according to new regulatory standards and safety protocols that aviation authorities require. The Federal Aviation Administration has established safety guidelines which mandate organizations to implement continuous monitoring processes and predictive maintenance systems together with standardized certification methods for enhancing their operational reliability. The industry has accelerated its adoption of non-destructive testing technologies together with automated inspection systems and data driven compliance tools which enhance precision while shortening inspection durations. The ongoing integration of digital platforms together with real-time monitoring solutions throughout aerospace manufacturing and maintenance operations is transforming service delivery systems while creating heightened demand for TIC solutions which require precise measurements.

Growth Drivers

The industry experiences market growth because of two main factors which include heightened safety regulations, rising investment levels in aerospace manufacturing and maintenance facilities. The commercial and defense aviation sectors continue to expand their fleets which creates ongoing demand for testing and certification services needed to support maintenance repair and overhaul operations. The International Civil Aviation Organization established regulatory frameworks and global safety standards which promote unified compliance methods that drive market adoption. The industry will continue to demand essential testing for performance validation and safety assurance together with lifecycle testing across all primary end user divisions.

Market Restraints / Challenges

The market encounters multiple difficulties which arise from two main factors that include elevated costs for regulatory compliance, the operational challenges that come with modern testing and certification processes. The costs of service provision increase for smaller companies because they must maintain compliance with both Federal Aviation Administration regulations and multiple safety standard updates. Companies require both specialized testing facilities and skilled staff members and advanced testing instruments to operate at their full potential. Companies face financial challenges and service acceptance issues because of their need to balance these two elements with the changing patterns of aerospace production.

Market Opportunities

The market provides growth potential through the development of digital testing, automated testing systems which benefit from improved predictive analytics and smart inspection technology. The aerospace industry now requires specialized certification services because of the increase in funding for next generation aircraft systems and sustainable aviation technologies. The International Civil Aviation Organization leads global alignment efforts which allow government-supported aviation safety initiatives to promote standardized TIC framework use for insect testing. Companies that provide technology-based integrated solutions which deliver high accuracy measurements are positioned to obtain new customer demand while extending their existing service contracts.

U.S. TIC Market for Aerospace & Aviation Industry Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 8.0 Billion |

|

Revenue Forecast in 2035 |

USD 11.96 Billion |

|

Growth Rate |

4.1% |

|

Segments Covered in the Report |

Service Type, Sourcing Type, End Use |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

West, South, Midwest |

|

Key Companies |

Applus+, Bureau Veritas, DEKRA, Element Materials Technology, Intertek Group, MISTRAS Group, SGS SA, TÜV Rheinland, TÜV SÜD, UL Solutions |

|

Customization |

Available upon request |

U.S. TIC Market for Aerospace & Aviation Industry Segmentation

By Service Type

Testing services accounted for the largest market share in 2025, representing approximately 42% of total revenue, supported by high frequency usage across component validation, material analysis, and system level performance checks. Testing protocols need to remain strict because aerospace systems become more intricate while Federal Aviation Administration regulations introduce new testing standards, which creates ongoing demand for testing through all manufacturing and maintenance activities.

The period from 2026 to 2035 will see certification services develop into the fastest expanding sector that will achieve a growth rate of 4.5% annually throughout the entire forecast period. The aviation industry needs to meet international standards while aircraft operations across borders require standardized permits, which leads to the present growth trend. Certification service usage in commercial and defense aviation sectors has increased because new aircraft programs and International Civil Aviation Organization safety frameworks have introduced new safety standards.

By Sourcing Type

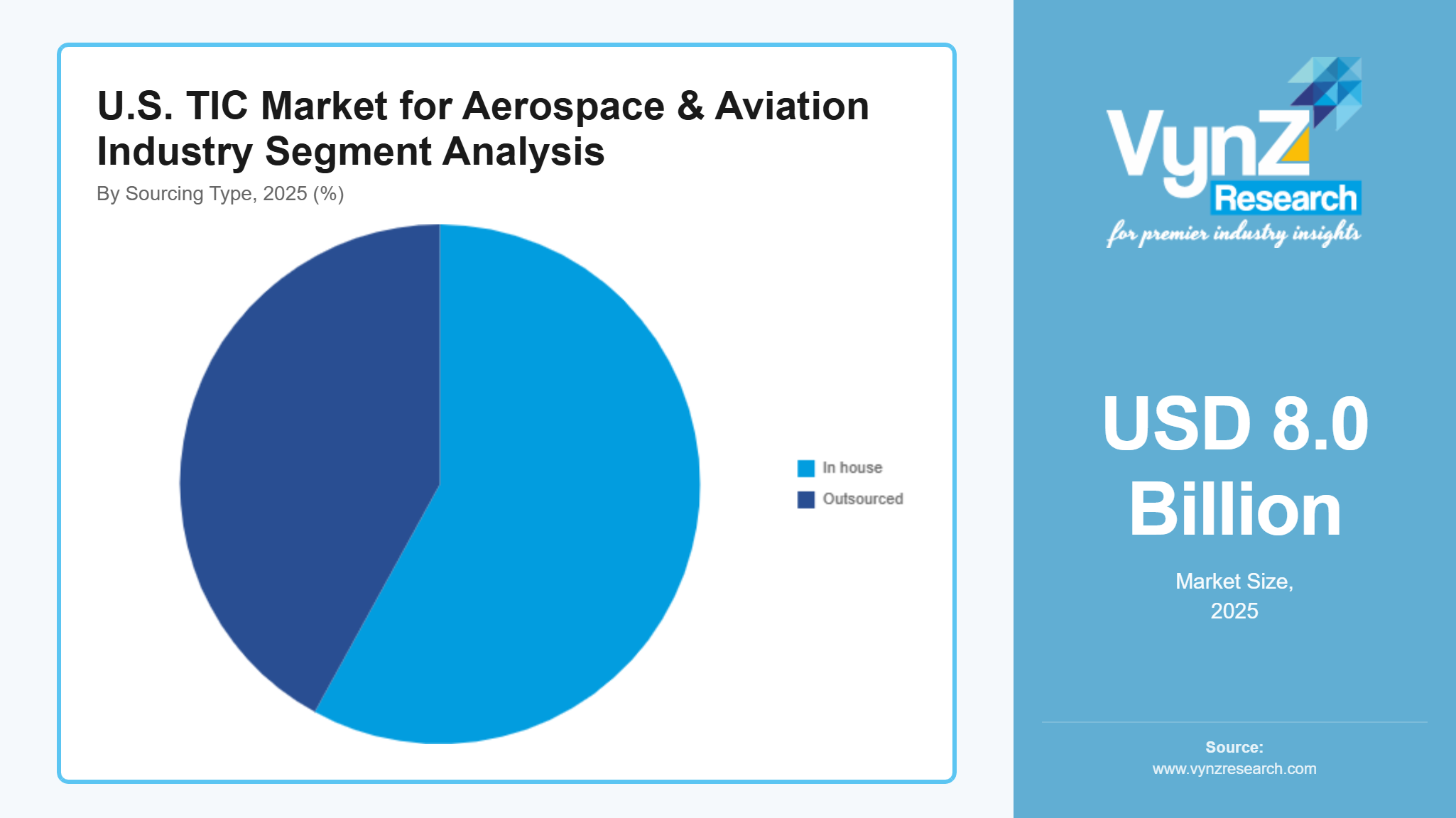

In house services held a majority share in 2025, contributing approximately 58% of total market revenue, as aerospace manufacturers continue to prioritize internal quality control, faster turnaround times, and integration with production workflows. The presence of established testing infrastructure together with skilled personnel availability in large aerospace companies enables them to dominate essential testing and inspection operations.

The growth rate for outsourced services exceeds all other services because organizations seek to reduce expenses while acquiring specialized knowledge. Third party service providers attract adoption through their capacity to deliver advanced testing technologies together with scalable solutions which become available to small and mid-sized enterprises. The increasing need for independent verification together with compliance assurance is driving expansion across different segments.

By End Use

Aerospace manufacturing accounted for the highest revenue share in 2025, representing approximately 46% of the market, supported by increasing aircraft production, integration of advanced materials, and stringent quality requirements across supply chains. The continuous investments into production facilities together with the development of regulatory compliance frameworks lead to ongoing demand for TIC services in this segment.

Commercial aviation will experience the most rapid expansion because air passenger traffic increases while airlines grow their fleets and maintenance repair and overhaul activities expand. Defense aviation also contributes significantly, supported by government spending on military aircraft modernization and strict safety validation requirements, ensuring sustained demand across multiple end use segments.

Regional Insights

West

The United States West region accounted for approximately 28% of the market in 2025 because strong aerospace manufacturing presence and advanced technology adoption dominated key hubs in California and Washington. The Federal Aviation Administration's strict regulatory oversight together with the high concentration of aircraft production and maintenance facilities creates continuous demand for testing and inspection and certification services. Increasing investments in digital inspection technologies and infrastructure modernization are further strengthening regional market performance.

South

The South region achieved a 24% market share in 2025 through expanding aerospace manufacturing activities and defense aviation operations across states such as Texas and Florida. The military aviation programs experience growth because of increasing maintenance repair and overhaul operations and rising government spending. The region experiences increased adoption of standardized TIC services because International Civil Aviation Organization safety standards require regulatory bodies to align with international safety standards.

Midwest

The United States Midwest region achieved 18% market share in 2025 because its industrial manufacturing ability and component testing process development in Ohio and Illinois create demand for testing services. The market maintains steady demand because advanced testing technologies and compliance requirements continue to increase their adoption. The remaining share of the market is covered by other regions not included above which ensures that regional distribution stays within the established market balance range.

Competitive Landscape / Company Insights

The industry operates with moderate competitiveness because both international and domestic companies compete through their service development, price determination and their efforts to enter new markets. Companies are increasingly investing in advanced testing technologies digital inspection systems and automation capabilities to enhance their market presence. Compliance-driven service improvements result from regulatory frameworks and safety standards which the Federal Aviation Administration establishes while organizations use International Civil Aviation Organization global standards to create unique market advantages.

Mini Profiles

Applus+ focuses on inspection, testing, and certification services for aerospace systems, supported by strong global presence, technical expertise, and cost-efficient service delivery across complex industrial and aviation applications.

Bureau Veritas operates in premium compliance and certification segments, emphasizing safety assurance, regulatory expertise, and high-performance inspection services across aerospace manufacturing and maintenance ecosystems.

DEKRA leverages extensive technical expertise and regulatory alignment to expand market presence, supported by strong inspection capabilities, certification services, and growing demand across aviation safety and compliance segments.

Element Materials Technology focuses on advanced material testing and laboratory services, supported by specialized infrastructure, global laboratory network, and strong expertise in aerospace component validation and performance testing.

Intertek Group operates in global assurance and certification segments, emphasizing quality, safety, and performance testing services, supported by strong brand recognition and integrated service offerings across aerospace supply chains.

Key Players

- Applus+

- Bureau Veritas

- DEKRA

- Element Materials Technology

- Intertek Group

- MISTRAS Group

- SGS SA

- TÜV Rheinland

- TÜV SÜD

- UL Solutions

Recent Developments

In April 2026, Intertek initiated a strategic review to potentially separate its energy and infrastructure division from core testing operations to improve capital efficiency and focus.

The move aims to enhance profitability and streamline operations amid evolving market dynamics and investor expectations.

In February 2025, SGS reported higher annual sales and profit growth, supported by increased demand for quality assurance and sustainability services across global supply chains.

The company also expanded its acquisition strategy in 2025, completing multiple acquisitions to strengthen service capabilities and market reach.

In February 2026, Bureau Veritas released its 2025 financial results, highlighting steady revenue growth and continued expansion across global certification and inspection services.

The company is focusing on sustainability driven services and digital transformation initiatives to strengthen its aerospace and industrial portfolio.

In 2025, Element Materials Technology continued expanding its advanced materials testing capabilities, particularly in aerospace and high-performance engineering sectors.

The company is investing in specialized laboratory infrastructure and strategic collaborations to support next generation aircraft development and compliance testing.

In 2025, DEKRA expanded its aerospace and mobility testing services, focusing on digital inspection and safety validation technologies.

The company is strengthening its position through investments in automation and certification services aligned with evolving global aviation safety standards.

U.S. TIC Market for Aerospace & Aviation Industry Coverage

Service Type Insight and Forecast 2026 - 2035

- Testing

- Inspection

- Certification

Sourcing Type Insight and Forecast 2026 - 2035

- In house

- Outsourced

End Use Insight and Forecast 2026 - 2035

- Aerospace manufacturing

- Commercial aviation

- Defense aviation

U.S. TIC Market for Aerospace & Aviation Industry by Region

- West

- By Service Type

- By Sourcing Type

- By End Use

- South

- By Service Type

- By Sourcing Type

- By End Use

- Midwest

- By Service Type

- By Sourcing Type

- By End Use

Table of Contents for U.S. TIC Market for Aerospace & Aviation Industry Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Service Type

1.2.2. By

Sourcing Type

1.2.3. By

End Use

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. U.S. Market Estimate and Forecast

4.1. U.S. Market Overview

4.2. U.S. Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Service Type

5.1.1. Testing

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Inspection

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Certification

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Sourcing Type

5.2.1. In house

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Outsourced

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By End Use

5.3.1. Aerospace manufacturing

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Commercial aviation

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Defense aviation

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

6. West Market Estimate and Forecast

6.1. By

Service Type

6.2. By

Sourcing Type

6.3. By

End Use

7. South Market Estimate and Forecast

7.1. By

Service Type

7.2. By

Sourcing Type

7.3. By

End Use

8. Midwest Market Estimate and Forecast

8.1. By

Service Type

8.2. By

Sourcing Type

8.3. By

End Use

9. Company Profiles

9.1.

Applus+

9.1.1.

Snapshot

9.1.2.

Overview

9.1.3.

Offerings

9.1.4.

Financial

Insight

9.1.5.

Recent

Developments

9.2.

Bureau Veritas

9.2.1.

Snapshot

9.2.2.

Overview

9.2.3.

Offerings

9.2.4.

Financial

Insight

9.2.5.

Recent

Developments

9.3.

DEKRA

9.3.1.

Snapshot

9.3.2.

Overview

9.3.3.

Offerings

9.3.4.

Financial

Insight

9.3.5.

Recent

Developments

9.4.

Element Materials Technology

9.4.1.

Snapshot

9.4.2.

Overview

9.4.3.

Offerings

9.4.4.

Financial

Insight

9.4.5.

Recent

Developments

9.5.

Intertek Group

9.5.1.

Snapshot

9.5.2.

Overview

9.5.3.

Offerings

9.5.4.

Financial

Insight

9.5.5.

Recent

Developments

9.6.

MISTRAS Group

9.6.1.

Snapshot

9.6.2.

Overview

9.6.3.

Offerings

9.6.4.

Financial

Insight

9.6.5.

Recent

Developments

9.7.

SGS SA

9.7.1.

Snapshot

9.7.2.

Overview

9.7.3.

Offerings

9.7.4.

Financial

Insight

9.7.5.

Recent

Developments

9.8.

TÜV Rheinland

9.8.1.

Snapshot

9.8.2.

Overview

9.8.3.

Offerings

9.8.4.

Financial

Insight

9.8.5.

Recent

Developments

9.9.

TÜV SÜD

9.9.1.

Snapshot

9.9.2.

Overview

9.9.3.

Offerings

9.9.4.

Financial

Insight

9.9.5.

Recent

Developments

9.10.

UL Solutions

9.10.1.

Snapshot

9.10.2.

Overview

9.10.3.

Offerings

9.10.4.

Financial

Insight

9.10.5.

Recent

Developments

10. Appendix

10.1. Exchange Rates

10.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

U.S. TIC Market for Aerospace & Aviation Industry