Europe TIC Market for Aerospace & Aviation Industry Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Sourcing Type (In-house, Outsourced), by Service Type (Testing, Inspection, Certification), by Application / Industry Focus (Electronics testing, Component testing, Emission testing, Durability testing, Others)

| Status : Published | Published On : Mar, 2026 | Report Code : VRAD12048 | Industry : Aerospace and Defense | Available Format :

|

Page : 135 |

Europe TIC Market for Aerospace & Aviation Industry Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Sourcing Type (In-house, Outsourced), by Service Type (Testing, Inspection, Certification), by Application / Industry Focus (Electronics testing, Component testing, Emission testing, Durability testing, Others)

Europe TIC Market for Aerospace & Aviation Industry Overview

The Europe TIC market for aerospace and aviation industry market which was valued at approximately USD 34.2 billion in 2025 and is estimated to rise further up to almost USD 35.6 billion by 2026, is projected to reach around USD 52.8 billion by 2035, expanding at a CAGR of about 4.9% during the forecast period 2026 to 2035.

The market experiences growth because aviation safety regulations become stricter and aircraft systems become more complicated. Air passenger numbers also keep increasing and advanced testing solutions, inspection systems, certification procedures receive wider acceptance. The growing requirement for dependable component testing and regulatory compliance testing, which aerospace manufacturing operations create, brings ongoing development to the aerospace industry.

The combination of government-funded aviation safety frameworks, European Union Aviation Safety Agency regulatory oversight and World Health Organization international safety guidelines establishes the foundation for standardized inspection and certification procedures. The aviation industry market expansion receives support from ongoing investments which target infrastructure upgrades, sustainability requirements and emission tracking systems across all major regions including Germany, France and the United Kingdom, which maintain strong aerospace manufacturing activities and active regulatory enforcement of TIC services.

Europe TIC Market for Aerospace & Aviation Industry Dynamics

Market Trends

Digital inspection systems together with automatic certification systems are taking over the market because people want more precise results which help them monitor everything in real time. The European Union Aviation Safety Agency plus worldwide aviation organizations created regulatory frameworks which help aviation enterprises to implement standardized compliance procedures while using non-destructive testing methods and data-based inspection systems.

European Commission environmental regulations and international aviation authorities emission reduction targets drive the development of services which focus on sustainability. Companies must create complete solutions which combine all their services to deliver extra value through lifecycle assessment and digital traceability because this will help them gain advantage in every market section.

Growth Drivers

The aviation industry requires strict safety regulations which create ongoing demand for both aerospace manufacturing and maintenance services. European markets grew because aviation authorities maintained strict regulatory control over aircraft production and aviation infrastructure modernization projects.

The rising complexity of aircraft systems leads to increased demand for specialized testing and certification services. The industry needs TIC solutions to meet safety requirements because of its dedication to safety and compliance with performance reliability standards, which receive government support through investments in advanced aviation technologies.

Market Restraints / Challenges

Companies face difficulties because their operational expenses increase when certification standards for certification processes change which results in regulatory compliance challenges. The European Commission frameworks show that service providers must dedicate permanent resources to achieve full safety and environmental standards which result in operational difficulties for their business.

Businesses face challenges because they depend on highly skilled workers and they must maintain costly inspection facilities to conduct their operations. The lack of certified professionals together with the need for businesses to spend large amounts of money on capital expenses creates financial difficulties which prevent firms from expanding their operations when economic conditions become unstable.

Market Opportunities

The market shows potential for digital transformation through AI technology and automatic inspection technology implementation. Companies which provide complete solutions with exact precision will gain business from aerospace manufacturers and maintenance service providers.

Sustainability-driven services create new business opportunities which European regulatory agencies will support through their established environmental requirements. The growth of emission monitoring technology together with green aviation technologies has led to more certification services which use digital tools and smart platforms to enhance efficiency and develop enduring customer relationships.

Europe TIC Market for Aerospace & Aviation Industry Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 34.2 Billion |

|

Revenue Forecast in 2035 |

USD 52.8 Billion |

|

Growth Rate |

4.9% |

|

Segments Covered in the Report |

Service Type, Sourcing Type, Application, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

Germany, France, United Kingdom, Italy, Spain, Rest of Europe |

|

Key Companies |

Applus+ Services SA, Bureau Veritas SA, DEKRA SE, DNV AS, Eurofins Scientific SE, Intertek Group plc, SGS SA, TÜV SÜD |

|

Customization |

Available upon request |

Europe TIC Market for Aerospace & Aviation Industry Segmentation

By Service Type

The testing services reached its highest value in 2025 and generated approximately 44% of total market earnings. The necessity of component validation together with material strength testing and performance testing drives the need for these solutions throughout aircraft production and repair operations. The European Union Aviation Safety Agency together with global aviation safety organizations requires ongoing testing from the beginning to the end of product development which creates continuous testing requirements.

The certification segment will experience the highest growth during this period because its market size will increase at a 5.2% CAGR between 2026 and 2035. The demand for compliance solutions drives growth because organizations need to meet international regulations while maintaining safety documentation and traceability requirements. Aviation authorities together with government safety programs enhance certification processes by promoting integrated service models that provide both inspection precision and regulatory compliance.

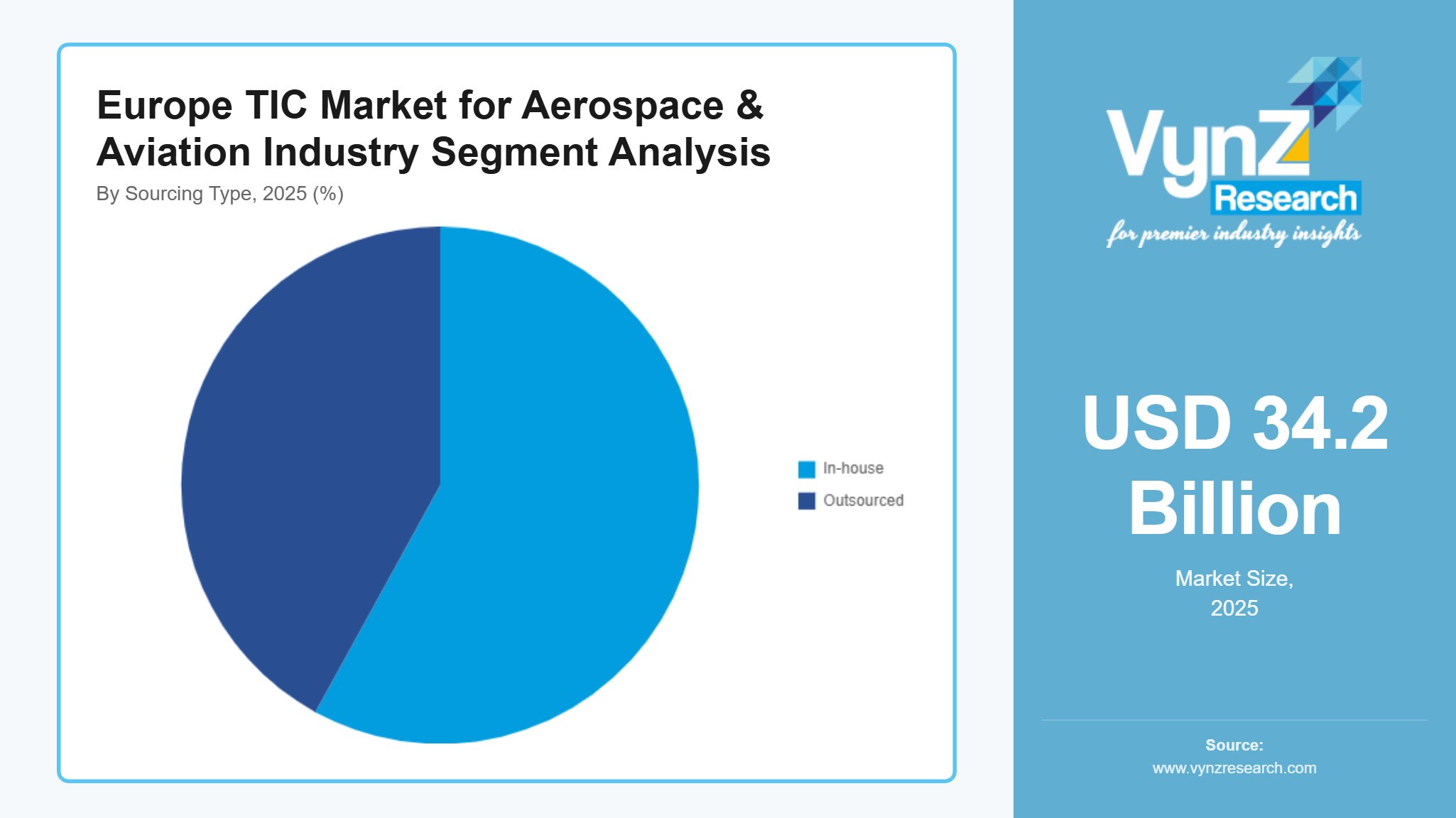

By Sourcing Type

Outsourced services reached 58% in 2025 to become the largest segment of total market revenue. The aerospace industry increasingly depends on third-party TIC providers to deliver specialized knowledge which helps them reduce expenses and meet compliance requirements. Independent service providers deliver testing facilities together with international certification services which aviation authorities and international safety organizations have authorized through regulatory compliance. European clients increasingly demand outsourced services because aerospace component complexity increases while organizations need unbiased testing services to evaluate their components.

The sector of in-house services will expand at a constant rate which will result in a 4.5% CAGR growth throughout this prediction period. The aviation sector requires dedicated inspection facilities which large aerospace manufacturers build to improve internal quality control systems for their internal inspection operations. Companies should increase their internal TIC capabilities in high-volume manufacturing environments because government industrial development programs and domestic aerospace investments provide financial backing.

By Application

The component testing segment generated the highest revenue for the year 2025 which accounted for 36% of total segment income. Structural components require extensive validation to ensure safety while avionics and engine systems need testing to verify their operational performance. European aviation authorities and international safety standards require testing at the component level which creates ongoing testing requirements for manufacturing and maintenance activities. Advanced materials and lightweight components require specialized testing services because their use is increasing.

The emission testing market will grow the most between 2026 and 2035 because emission testing will reach a 5.4% CAGR during that period. The European Commission established environmental regulations and sustainability targets which drive growth through their carbon reduction and fuel efficiency requirements. Government programs promote sustainable aviation practices which help aircraft lifecycle extension programs and maintenance optimization strategies determine which durability testing methods to implement.

By End User

The segment of aerospace manufacturers generated the most market revenue in 2025 when it brought in almost half 49% of total market earnings. Their dominance emerges from testing, inspection together with certification services which clients need during aircraft production and component integration work, combined with the testing services which they require for quality control. Government-backed aerospace manufacturing programs and aviation authority regulatory compliance requirements create ongoing demand for this segment in Germany, France, and the United Kingdom.

The maintenance, repair, and overhaul service providers will grow at a 5.1% CAGR throughout the period from 2026 to 2035. Aircraft fleet expansion together with air traffic rise and airworthiness requirements drive the sector's growth. Government-supported aviation safety programs together with lifecycle maintenance regulations create demand for regular inspection and certification activities which drive ongoing needs for commercial and defense aviation services.

Regional Insights

Germany

Germany maintained a 23% market share of Europe TIC operations for the aerospace and aviation sector during 2025 because of its strong aerospace manufacturing base and advanced engineering capabilities. The major hubs of Hamburg and Munich drive testing and inspection and certification service demand for aircraft production and component validation work. The European Union Aviation Safety Agency and national aviation authorities establish regulatory frameworks which mandate full compliance. Government-funded projects which focus on aviation innovation and sustainability initiatives have created an increased requirement for advanced TIC solutions.

France

France commands 19% of the market because of its developed aerospace sector and aircraft manufacturing base. Toulouse and Paris serve as key centers for aerospace production and certification activities. European Commission regulations create government-supported aviation frameworks which drive inspection and certification service demand. Manufacturers and maintenance operations are increasingly adopting TIC services because of their need to control emissions and develop sustainable aviation technologies.

United Kingdom

The United Kingdom has a 17% market share which results from its advanced aerospace engineering, maintenance repair and overhaul capabilities. London and Bristol serve as primary locations for testing components and certifying those components. Investment in high-precision TIC services will continue to rise because of the government's digital inspection technology initiative and the country's compliance with international aviation safety regulations.

Rest of Europe

The industry landscape for 2025 shows that the rest of Europe which includes Italy, Spain and emerging aerospace markets holds an 18% share. The region experiences growth because of developing aerospace supply chains, increasing industrial activity and the implementation of standard compliance procedures. The European aviation safety regulations will drive TIC service demand because of government-funded infrastructure projects and the requirement for compliance with European aviation safety regulations. The remaining approximately 23% of the market is covered by other smaller European countries not explicitly mentioned, contributing to overall regional expansion.

Competitive Landscape / Company Insights

The market shows a moderate level of competition because established global and regional companies operate their businesses through service innovation, compliance capability development and geographic market expansion. Companies are investing in digital inspection technologies, automation systems and advanced testing facilities to improve their competitive market standing. European Union Aviation Safety Agency and international aviation organizations established regulatory frameworks and safety standards which require organizations to improve their certification processes according to European Union Aviation Safety Agency and international aviation organization standards while building competitive advantages through their quality assurance and complete service delivery.

Mini Profiles

Applus+ Services SA focuses on comprehensive testing, inspection, and certification services, supported by global operational presence, strong technical expertise, and integrated service capabilities that enhance compliance assurance across aerospace and aviation sectors.

Bureau Veritas SA operates in premium and specialized TIC segments, emphasizing regulatory compliance, safety assurance, and performance validation, supported by strong brand recognition and extensive global certification and inspection networks.

DEKRA SE leverages technical expertise and strategic partnerships to expand market presence, offering advanced inspection and certification solutions with strong focus on safety, reliability, and digital inspection technologies across aerospace applications.

Eurofins Scientific SE focuses on specialized testing services, supported by advanced laboratory infrastructure, strong analytical capabilities, and expanding global footprint that strengthens its position in high precision aerospace testing segments.

Intertek Group plc operates in diversified TIC services, emphasizing quality assurance, risk management, and compliance solutions, supported by extensive global network and digital service integration that enhances operational efficiency and customer trust.

Key Players

- Applus+ Services SA

- Bureau Veritas SA

- DEKRA SE

- DNV AS

- Eurofins Scientific SE

- Intertek Group plc

- SGS SA

- TÜV SÜD

Recent Developments

In February 2026, Applus+ strengthened its aerospace inspection capabilities by expanding advanced nondestructive testing services across European facilities. This supports increasing regulatory compliance requirements and rising aircraft component validation demand.

In January 2025, Bureau Veritas focused on expanding digital certification platforms to enhance compliance efficiency and traceability. This aligns with evolving aviation safety regulations and growing need for integrated TIC solutions.

In March 2026, DEKRA advanced its digital inspection services by integrating automation and AI driven assessment tools. This development improves operational efficiency and supports complex aerospace system validation requirements.

In December 2025, Eurofins expanded its aerospace testing capabilities through laboratory upgrades and enhanced analytical services. This initiative supports increasing demand for high precision material and component testing.

In January 2026, SGS invested in digital compliance and certification solutions to strengthen aerospace service offerings. This move enhances real time monitoring and supports stringent safety and regulatory standards across the aviation sector.

Europe TIC Market for Aerospace & Aviation Industry Coverage

Sourcing Type Insight and Forecast 2026 - 2035

- In-house

- Outsourced

Service Type Insight and Forecast 2026 - 2035

- Testing

- Inspection

- Certification

Application / Industry Focus Insight and Forecast 2026 - 2035

- Electronics testing

- Component testing

- Emission testing

- Durability testing

- Others

Europe TIC Market for Aerospace & Aviation Industry by Region

- Germany

- By Sourcing Type

- By Service Type

- By Application / Industry Focus

- U.K.

- By Sourcing Type

- By Service Type

- By Application / Industry Focus

- France

- By Sourcing Type

- By Service Type

- By Application / Industry Focus

- Italy

- By Sourcing Type

- By Service Type

- By Application / Industry Focus

- Spain

- By Sourcing Type

- By Service Type

- By Application / Industry Focus

- Russia

- By Sourcing Type

- By Service Type

- By Application / Industry Focus

- Rest of Europe

- By Sourcing Type

- By Service Type

- By Application / Industry Focus

Table of Contents for Europe TIC Market for Aerospace & Aviation Industry Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Sourcing Type

1.2.2. By

Service Type

1.2.3. By

Application / Industry Focus

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Europe Market Estimate and Forecast

4.1. Europe Market Overview

4.2. Europe Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Sourcing Type

5.1.1. In-house

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Outsourced

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.2. By Service Type

5.2.1. Testing

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Inspection

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Certification

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By Application / Industry Focus

5.3.1. Electronics testing

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Component testing

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Emission testing

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Durability testing

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Others

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

6. Germany Market Estimate and Forecast

6.1. By

Sourcing Type

6.2. By

Service Type

6.3. By

Application / Industry Focus

7. U.K. Market Estimate and Forecast

7.1. By

Sourcing Type

7.2. By

Service Type

7.3. By

Application / Industry Focus

8. France Market Estimate and Forecast

8.1. By

Sourcing Type

8.2. By

Service Type

8.3. By

Application / Industry Focus

9. Italy Market Estimate and Forecast

9.1. By

Sourcing Type

9.2. By

Service Type

9.3. By

Application / Industry Focus

10. Spain Market Estimate and Forecast

10.1. By

Sourcing Type

10.2. By

Service Type

10.3. By

Application / Industry Focus

11. Russia Market Estimate and Forecast

11.1. By

Sourcing Type

11.2. By

Service Type

11.3. By

Application / Industry Focus

12. Rest of Europe Market Estimate and Forecast

12.1. By

Sourcing Type

12.2. By

Service Type

12.3. By

Application / Industry Focus

13. Company Profiles

13.1.

EApplus+ Services SA

13.1.1.

Snapshot

13.1.2.

Overview

13.1.3.

Offerings

13.1.4.

Financial

Insight

13.1.5.

Recent

Developments

13.2.

Bureau Veritas SA

13.2.1.

Snapshot

13.2.2.

Overview

13.2.3.

Offerings

13.2.4.

Financial

Insight

13.2.5.

Recent

Developments

13.3.

DEKRA SE

13.3.1.

Snapshot

13.3.2.

Overview

13.3.3.

Offerings

13.3.4.

Financial

Insight

13.3.5.

Recent

Developments

13.4.

DNV AS

13.4.1.

Snapshot

13.4.2.

Overview

13.4.3.

Offerings

13.4.4.

Financial

Insight

13.4.5.

Recent

Developments

13.5.

Eurofins Scientific SE

13.5.1.

Snapshot

13.5.2.

Overview

13.5.3.

Offerings

13.5.4.

Financial

Insight

13.5.5.

Recent

Developments

13.6.

Intertek Group plc

13.6.1.

Snapshot

13.6.2.

Overview

13.6.3.

Offerings

13.6.4.

Financial

Insight

13.6.5.

Recent

Developments

13.7.

SGS SA

13.7.1.

Snapshot

13.7.2.

Overview

13.7.3.

Offerings

13.7.4.

Financial

Insight

13.7.5.

Recent

Developments

13.8.

TÜV SÜD

13.8.1.

Snapshot

13.8.2.

Overview

13.8.3.

Offerings

13.8.4.

Financial

Insight

13.8.5.

Recent

Developments

14. Appendix

14.1. Exchange Rates

14.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Europe TIC Market for Aerospace & Aviation Industry