North America TIC Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Service Type (Testing, Inspection, Certification), by Sourcing Type (In house, Outsourced), by Industry Vertical (Manufacturing, Healthcare and pharmaceuticals, Energy and power, Oil and gas, Automotive, Aerospace and defense, Consumer goods and retail, Agriculture and food, Information technology and telecommunications, Construction and infrastructure), by End Use (Industrial, Commercial, Public sector)

| Status : Published | Published On : Apr, 2026 | Report Code : VRSME9207 | Industry : Semiconductor & Electronics | Available Format :

|

Page : 132 |

North America TIC Market Overview

The North America testing inspection and certification market which was valued at approximately USD 56.70 billion in 2025 and is estimated to rise further up to almost USD 59.47billion by 2026, and around USD 91.48 billion by 2035, at a CAGR of about 4.9% during the forecast period from 2026 to 2035.

The market grows because businesses need to meet strict regulatory standards while handling more complex supply chains and customers demand better quality assurance and companies adopt digital inspection and certification systems. The market growth in the United States, Canada, and Mexico is driven by increasing requirements for product safety verification in the manufacturing, energy, and consumer goods sectors and by ongoing investment in law enforcement and infrastructure upgrades.

The market grows because businesses need to meet strict regulatory standards while handling more complex supply chains and customers demand better quality assurance and companies adopt digital inspection and certification systems. The market growth in the United States, Canada, and Mexico is driven by increasing requirements for product safety verification in the manufacturing, energy, and consumer goods sectors and by ongoing investment in law enforcement and infrastructure upgrades.

The testing inspection and certification system receives essential support from government organizations and regulatory bodies because they establish standardization frameworks that create compliance requirements. The National Institute of Standards and Technology and occupational safety authorities require organizations to follow safety standards, environmental regulations and performance standards which boosts demand for verification services that are conducted by external parties. International guidelines which receive support from organizations like the World Health Organization establish certification processes for healthcare product safety and environmental control. The regional market experiences stronger demand because public sector agencies establish regulatory frameworks that require product reliability and workplace safety and environmental compliance.

North America TIC Market Dynamics

Market Trends

The industry is experiencing major technological adoption changes together with procurement methods that are controlled by compliance requirements because digital inspection, remote auditing and automated certification systems are becoming more widely used. Digital data-driven assurance systems are becoming the main market trend because industrial operations require better efficiency and traceability and real-time compliance monitoring. The National Institute of Standards and Technology together with occupational safety authorities has enabled regulatory bodies to require organizations to adopt standardized verification systems that use modern technology for their verification requirements.

The new trend focuses on environmental and sustainability compliance because regulations and international safety standards now require businesses to comply with these environmental requirements. Organizations including the World Health Organization have established product safety standards which companies must follow for environmental monitoring and healthcare quality assessment. This requirement has led companies to develop certification solutions which deliver complete value and certified service offerings, resulting in market competition.

Growth Drivers

North America testing inspection and certification market growth depends on strict regulatory requirements which create ongoing need for testing services in manufacturing, energy, healthcare and consumer goods markets. The region's market growth is being driven by rising investments which target industrial infrastructure development, smart manufacturing and energy systems modernization projects. Public sector initiatives which strengthen product safety, workplace standards and environmental compliance systems create additional demand for third-party verification services.

The rising complexity of global supply chains has become a critical factor which fuels industry expansion. Enterprises will maintain high demand for testing inspection and certification services because they need to achieve compliance, operational efficiency and risk reduction. The federal regulatory body safety and quality standards together with World Health Organization healthcare safety guidelines produce government-backed frameworks which establish a need for trustworthy certification processes.

Market Restraints / Challenges

North America testing inspection and certification market faces key obstacles, which will limit its potential expansion despite positive growth outlook. Small and mid-sized enterprises experience decreased operational efficiency because they must handle regulatory requirements which cover multiple industries and jurisdictions. Organizations must establish testing infrastructure and certification protocols and develop their workforce skills, to maintain compliance with all regulatory standards which evolve through time.

Service providers must manage operational difficulties because their work relies heavily on skilled employees and advanced testing equipment. The workforce development and industrial safety reports from the government show that there are not enough trained inspection professionals, which causes service delays and price increases for services. Organizations which depend on imported advanced equipment and specialized expertise will experience cost pressures and reduced scalability, which will lead to market performance decline during times of economic instability.

Market Opportunities

The market provides digital inspection and automated inspection solutions with advanced artificial intelligence, data analytics and remote monitoring technologies as its main growth drivers. Companies that provide integrated certification platforms with technology enablement will capture additional demand from manufacturing, healthcare and energy markets, which require better compliance performance. The government initiatives which support digital transformation and industrial automation will assist organizations in adopting advanced verification systems.

The sustainability services market provides another crucial business opportunity, which will expand through green infrastructure investments and regulatory enforcement. Environmental protection agencies and World Health Organization global health and safety guidelines establish frameworks which push organizations to adopt testing services and certification services. The regional market will benefit from smart inspection tool advancements and automated compliance system enhancements, which will enable better service efficiency and client relationship development.

North America TIC Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 56.70 Billion |

|

Revenue Forecast in 2035 |

USD 91.48 Billion |

|

Growth Rate |

4.9% |

|

Segments Covered in the Report |

By Service Type, By Sourcing Type, By Industry Vertical, By End Use |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

United States, Canada, Mexico |

|

Key Companies |

ALS Limited, Applus+, Bureau Veritas, DEKRA, DNV, Element Materials Technology, Eurofins Scientific, Intertek Group plc, SGS SA, TÜV SÜD |

|

Customization |

Available upon request |

North America TIC Market Segmentation

By Service Type

Testing services reached 54% of its total testing market in 2025 because it provided requirements for manufacturing, consumer goods, and healthcare products which needed ongoing product testing and regulatory compliance. The sector growth will continue because industries require frequent testing and essential quality standards which maintain testing standards, with the segment expected to grow at 4.6% annually.

The inspection segment will achieve maximum growth during the forecast period because energy and industrial sectors need to monitor their infrastructure, verify asset integrity and safeguard operational safety functions. The construction and industrial automation sectors drive market expansion as organizations increase their investment in these areas, which results in a market growth rate of 5.3%.

The certification market grows because international trading partners need to comply with standardization requirements. Export-oriented industries require third-party validation services, which drive market growth at 4.7% annually.

By Sourcing Type

In house services accounted for approximately 58% share of the market in 2025, supported by strong preference among large enterprises for internal control, faster turnaround, and confidentiality in critical operations. The market maintains a steady growth rate of 4.2% because businesses with high compliance requirements continue to depend on their internal resources.

The demand for cost savings and specialized skills will lead to faster growth in outsourced services. Companies select third party providers because regulatory frameworks have become more complicated, which leads to a segment expansion rate of 5.6%.

Small and mid-sized companies expand their operations because cross border trade and new compliance regulations create challenges that drive them to embrace outsourcing solutions, which add 5.1% market expansion to their business growth.

By Industry Vertical

Manufacturing accounted for approximately 32% share of the market in 2025, supported by high production volumes and continuous need for quality assurance across industrial operations. The segment expands at 4.7% growth rate because industry standardization requirements need automated solutions to operate.

The healthcare sector will experience maximum growth because medical devices and pharmaceuticals need regulatory validation and medical device certification requirements have become more stringent. The segment will grow at 5.5% because healthcare organizations and regulatory authorities develop patient safety protocols and compliance rules.

The oil and gas, energy and power sectors will continue their expansion because companies invest in safety upgrades and infrastructure improvements, which lead to 4.8% annual growth.

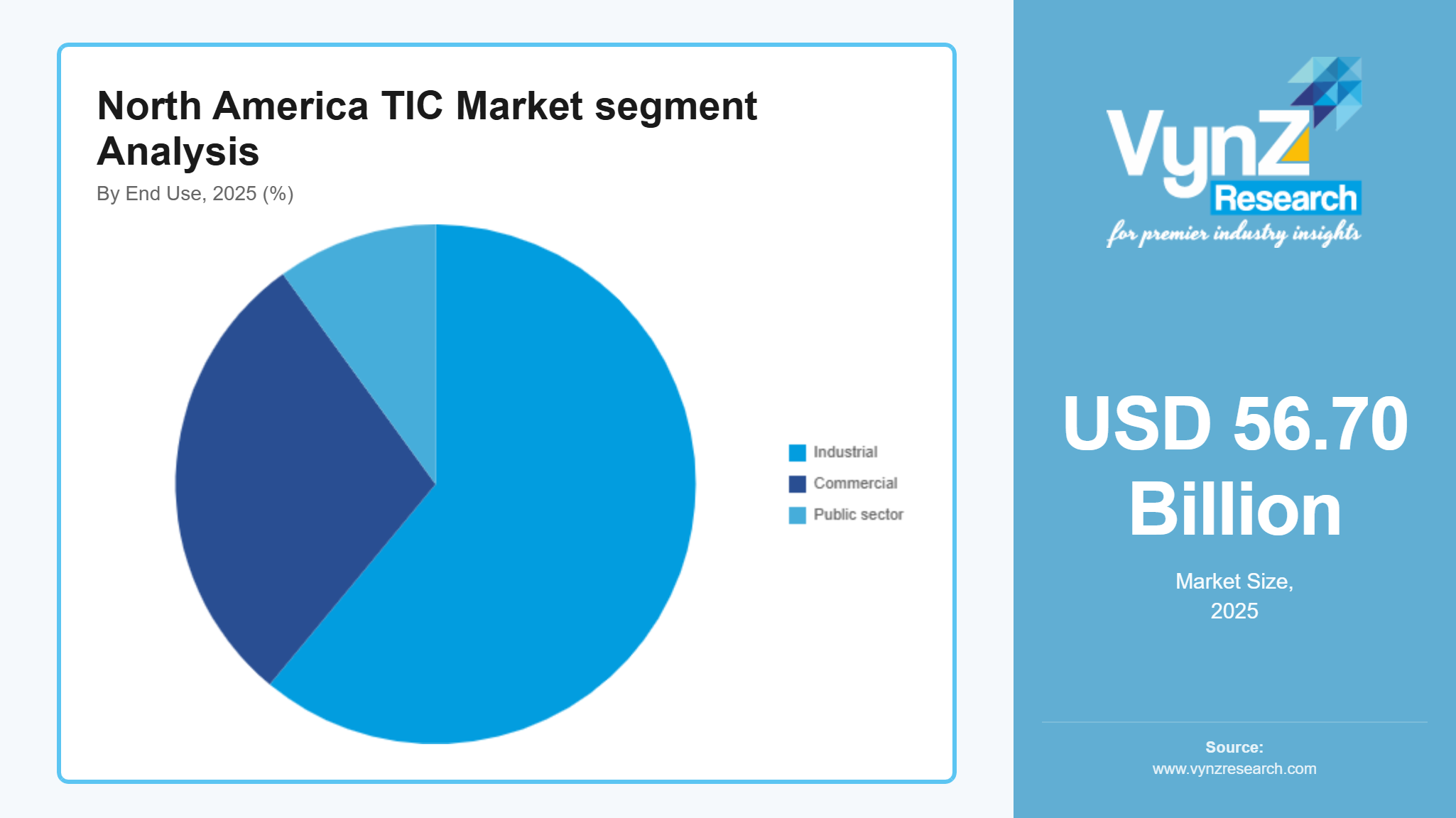

By End Use

Industrial applications accounted for approximately 61% share of the market in 2025, supported by strong demand from manufacturing, energy, and heavy industries where operational safety and compliance remain critical. The industrial modernization investments will sustain market growth at 4.6% for the entire period.

Commercial applications will expand quickly because service sector companies grow their operations in healthcare and retail and logistics. The market will expand at 5.2% because companies need to establish standardized quality assurance procedures.

Public sector applications maintain their growth trajectory because government agencies spend on infrastructure projects and enforce regulations, which leads to 4.4% growth during the entire forecast period.

Regional Insights

United States

The market in 2025 experienced its 52% share from the United States because of its strict regulatory compliance needs, advanced industrial facilities, high manufacturing, healthcare and energy sector demand. The industrial centers of New York, Texas and California sustain market expansion through their ongoing need for testing and inspection and certification services. National Institute of Standards and Technology and workplace safety authorities establish regulatory control which drives industry adoption across various sectors.

Canada

The Canadian market achieved a 14% share in 2025 because of its continuous industrial activities and strong regulatory systems which govern safety and environmental protection. The energy sector, construction sector and healthcare sector are experiencing rising demand for compliance services because of their increasing adoption of compliance services. The major urban areas and industrial regions of Toronto and Alberta and Vancouver are driving market growth.

Mexico

The Mexican market achieved a 12% share in 2025 because of its growing manufacturing sector and strong connections to worldwide supply networks. International standards create demand for quality assurance and certification services which industrial clusters and export production hubs need to succeed. Monterrey and Mexico City have developed into primary demand locations. The market develops through increasing regulatory compliance with international standards, which ensures product quality and workplace safety. Smaller North American economies not mentioned in this study handle the remaining market requirements.

Competitive Landscape / Company Insights

The market has moderate competition because international and local companies operate in the market through their service development, pricing methods and technological system implementation. Firms use digital inspection platforms, automation systems and data analytics tools to boost their market strength through their investment activities. Government agencies including the National Institute of Standards and Technology and safety authorities establish regulatory frameworks and compliance standards which force companies to improve their service delivery and accreditation processes and operational performance throughout the market.

Mini Profiles

Applus+ focuses on testing inspection and certification services across industrial sectors, supported by strong global compliance capabilities and diversified service portfolio, enabling consistent quality assurance across energy, automotive, and infrastructure markets.

Bureau Veritas operates in premium and regulated compliance segments, emphasizing safety assurance, sustainability verification, and risk management services, strengthening its position across manufacturing, marine, and construction industries globally.

DEKRA leverages advanced safety inspection expertise and strong automotive testing capabilities to expand market presence, supported by extensive certification networks and focus on mobility safety and industrial quality assurance solutions.

Eurofins Scientific focuses on laboratory testing and analytical services across healthcare, food, and environmental sectors, supported by strong scientific infrastructure and high precision diagnostic capabilities enabling global regulatory compliance.

Intertek Group plc operates in diversified quality assurance and certification segments, emphasizing product testing, inspection, and compliance solutions, supported by strong global laboratory networks and digital quality assurance platforms.

Key Players

- ALS Limited

- Applus+

- Bureau Veritas

- DEKRA

- DNV

- Element Materials Technology

- Eurofins Scientific

- Intertek Group plc

- SGS SA

- TÜV SÜD

Recent Developments

In January 2026, SGS SA expanded its digital assurance portfolio by strengthening cybersecurity testing and ESG verification capabilities across North America. This development supports its strategy to enhance digital compliance services and improve integrated risk assessment solutions across industrial sectors.

In November 2025, Intertek Group plc expanded its testing capabilities in the United States through the acquisition of a specialized materials testing laboratory. This move strengthens its presence in construction and building materials testing while enhancing its regional service network.

In February 2025, Bureau Veritas reported strong growth in its sustainability and supply chain assurance services across global markets. The company continued expanding its digital inspection solutions to support increasing demand for ESG compliance and industrial certification services.

In August 2025, DEKRA expanded its automotive testing and safety inspection services in North America to support growing demand for mobility and connected vehicle certification. This initiative strengthens its position in vehicle safety, autonomous systems testing, and industrial inspection services.

In June 2025, Eurofins Scientific enhanced its laboratory testing capacity in the United States by expanding food, environmental, and pharmaceutical testing facilities. This expansion supports rising regulatory compliance needs and increasing demand for high precision analytical testing services.

North America TIC Market Coverage

Service Type Insight and Forecast 2026 - 2035

- Testing

- Inspection

- Certification

Sourcing Type Insight and Forecast 2026 - 2035

- In house

- Outsourced

Industry Vertical Insight and Forecast 2026 - 2035

- Manufacturing

- Healthcare and pharmaceuticals

- Energy and power

- Oil and gas

- Automotive

- Aerospace and defense

- Consumer goods and retail

- Agriculture and food

- Information technology and telecommunications

- Construction and infrastructure

- Marine and shipping

End Use Insight and Forecast 2026 - 2035

- Industrial

- Commercial

- Public sector

North America TIC Market by Region

- U.S.

- By Service Type

- By Sourcing Type

- By Industry Vertical

- By End Use

- Canada

- By Service Type

- By Sourcing Type

- By Industry Vertical

- By End Use

- Mexico

- By Service Type

- By Sourcing Type

- By Industry Vertical

- By End Use

Table of Contents for North America TIC Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Service Type

1.2.2. By

Sourcing Type

1.2.3. By

Industry Vertical

1.2.4. By

End Use

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. North Market Estimate and Forecast

4.1. North Market Overview

4.2. North Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Service Type

5.1.1. Testing

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Inspection

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Certification

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Sourcing Type

5.2.1. In house

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Outsourced

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Industry Vertical

5.3.1. Manufacturing

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Healthcare and pharmaceuticals

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Energy and power

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Oil and gas

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Automotive

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.3.6. Aerospace and defense

5.3.6.1. Market Definition

5.3.6.2. Market Estimation and Forecast to 2035

5.3.7. Consumer goods and retail

5.3.7.1. Market Definition

5.3.7.2. Market Estimation and Forecast to 2035

5.3.8. Agriculture and food

5.3.8.1. Market Definition

5.3.8.2. Market Estimation and Forecast to 2035

5.3.9. Information technology and telecommunications

5.3.9.1. Market Definition

5.3.9.2. Market Estimation and Forecast to 2035

5.3.10. Construction and infrastructure

5.3.10.1. Market Definition

5.3.10.2. Market Estimation and Forecast to 2035

5.3.11. Marine and shipping

5.3.11.1. Market Definition

5.3.11.2. Market Estimation and Forecast to 2035

5.4. By End Use

5.4.1. Industrial

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Commercial

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Public sector

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

6. U.S. Market Estimate and Forecast

6.1. By

Service Type

6.2. By

Sourcing Type

6.3. By

Industry Vertical

6.4. By

End Use

7. Canada Market Estimate and Forecast

7.1. By

Service Type

7.2. By

Sourcing Type

7.3. By

Industry Vertical

7.4. By

End Use

8. Mexico Market Estimate and Forecast

8.1. By

Service Type

8.2. By

Sourcing Type

8.3. By

Industry Vertical

8.4. By

End Use

9. Company Profiles

9.1.

ALS Limited

9.1.1.

Snapshot

9.1.2.

Overview

9.1.3.

Offerings

9.1.4.

Financial

Insight

9.1.5.

Recent

Developments

9.2.

Applus+

9.2.1.

Snapshot

9.2.2.

Overview

9.2.3.

Offerings

9.2.4.

Financial

Insight

9.2.5.

Recent

Developments

9.3.

Bureau Veritas

9.3.1.

Snapshot

9.3.2.

Overview

9.3.3.

Offerings

9.3.4.

Financial

Insight

9.3.5.

Recent

Developments

9.4.

DEKRA

9.4.1.

Snapshot

9.4.2.

Overview

9.4.3.

Offerings

9.4.4.

Financial

Insight

9.4.5.

Recent

Developments

9.5.

DNV

9.5.1.

Snapshot

9.5.2.

Overview

9.5.3.

Offerings

9.5.4.

Financial

Insight

9.5.5.

Recent

Developments

9.6.

Element Materials Technology

9.6.1.

Snapshot

9.6.2.

Overview

9.6.3.

Offerings

9.6.4.

Financial

Insight

9.6.5.

Recent

Developments

9.7.

Eurofins Scientific

9.7.1.

Snapshot

9.7.2.

Overview

9.7.3.

Offerings

9.7.4.

Financial

Insight

9.7.5.

Recent

Developments

9.8.

Intertek Group plc

9.8.1.

Snapshot

9.8.2.

Overview

9.8.3.

Offerings

9.8.4.

Financial

Insight

9.8.5.

Recent

Developments

9.9.

SGS SA

9.9.1.

Snapshot

9.9.2.

Overview

9.9.3.

Offerings

9.9.4.

Financial

Insight

9.9.5.

Recent

Developments

9.10.

TÜV SÜD

9.10.1.

Snapshot

9.10.2.

Overview

9.10.3.

Offerings

9.10.4.

Financial

Insight

9.10.5.

Recent

Developments

10. Appendix

10.1. Exchange Rates

10.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

North America TIC Market