Global Substation Automation and Integration Market – Analysis and Forecast (2025-2030)

Industry Insight by Offering (Hardware (Reclose Controllers, Programmable Logical Controllers, Capacitor Banks, Smart Meters, Load Tap Changers, Digital Relays, Fiber-Optic Cables, and Others), Software (Production Management Software, Asset Management Software, and Performance Management Software), and Services (Installation and Commissioning, Up-Gradation and Retrofitting, and Testing, Repair, and Maintenance)), by Type (Transmission Substation and Distribution Substation), by Installation Type (New Installation and Retrofit Installation), by Component (IEDs (Intelligent Electronic Devices), Communication Networks, and SCADA Systems), by Communication (Ethernet, Power Line Communication, Copper Wire, and Optic Fiber), by End-User Industry (Utilities, Steel, Oil & Gas, Mining, Transportation, and Others), and Geography (U.S., Canada, Germany, U.K., France, China, Japan, India, and Rest of the World)

| Status : Published | Published On : Jan, 2024 | Report Code : VRSME9080 | Industry : Semiconductor & Electronics | Available Format :

|

Page : 275 |

Global Substation Automation and Integration Market – Analysis and Forecast (2025-2030)

Industry Insight by Offering (Hardware (Reclose Controllers, Programmable Logical Controllers, Capacitor Banks, Smart Meters, Load Tap Changers, Digital Relays, Fiber-Optic Cables, and Others), Software (Production Management Software, Asset Management Software, and Performance Management Software), and Services (Installation and Commissioning, Up-Gradation and Retrofitting, and Testing, Repair, and Maintenance)), by Type (Transmission Substation and Distribution Substation), by Installation Type (New Installation and Retrofit Installation), by Component (IEDs (Intelligent Electronic Devices), Communication Networks, and SCADA Systems), by Communication (Ethernet, Power Line Communication, Copper Wire, and Optic Fiber), by End-User Industry (Utilities, Steel, Oil & Gas, Mining, Transportation, and Others), and Geography (U.S., Canada, Germany, U.K., France, China, Japan, India, and Rest of the World)

Substation Automation and Integration Market Overview

The Global Substation Automation And Integration Market reached USD 36.3 billion in 2023 and is projected to reach USD 60.2 billion by 2030, with a compound annual growth rate (CAGR) of 6.6% during the period from 2025 to 2030.

The growth of the substation automation and integration market is due to the increasing influence of smart grid infrastructure, aging infrastructure, technology development and integration of primary equipment with modern sensors, protective relays, reduction in transmission and distribution loss, cost-saving, and intelligent electronic device as it smoothly controls the functions and monitors across the substation. Moreover, the increasing requirement to retrofit conventional substations, rapid industrialization, government initiatives to promote substation automation, and R&D activities will drive the market growth of the global substation automation and integration market.

The COVID-19 pandemic has led to a strict lockdown in various countries and various industries are affected by the outburst. The substation automation and integration market have grown owing to the rising demand for data centers that will support digital activities. However, electricity consumption is anticipated to reduce due to commercial spaces working at low capacity and electric utilities might witness a delay in upgrading their grid infrastructure, resulting in having an adverse impact on substation automation and integration market.

Substation Automation and Integration Market Segmentation

Insight by Offering

Based on offering, the global substation automation and integration market is segmented into hardware, software, and services. Hardware is further subdivided into reclose controllers, programmable logical controllers, capacitor banks, smart meters, load tap changers, digital relays, fiber-optic cables, and others. Software is further sub-divided into production management software, asset management software, and performance management software. Services are further subdivided into installation and commissioning, up-gradation and retrofitting, and testing, repair, and maintenance. The hardware segment holds the largest market share in 2020 owing to the introduction of the IEC 61850 standard for substations which incorporates all the control, measurement, and monitors in one protocol, resulting in proper interoperability between intelligent electronic devices (IEDs).

Insight by Type

Based on type, the global substation automation and integration market is divided into transmission substation and distribution substation. Transmission substations dominate the market owing to the rising electricity demand, there is a need to replace the aging infrastructure which cannot sustain the bulk power movements or inferior standards. Thus, investor-owned utilities are experiencing increased spending on transmission substations infrastructure.

Insight by Installation Type

Based on installation type, the global substation automation and integration market is bifurcated into new installation and retrofit installation. Among these segments, the new installation is anticipated to have a high CAGR owing to the rising demand for new power stations and smart grids in various industries. Moreover, the new installation can provide operational safety, reliability and requires low maintenance.

Insight by Component

Based on components, the global substation automation and integration is categorized into IEDs (Intelligent Electronic Devices), communication networks, and SCADA systems. IEDs are one of the major components in the substation automation and integration market and contain digital relays, programmable logic controllers, smart meters/digital transducers, load tap changer controller, capacitor bank controller, and reclose controller. IED offers barrier-free monitoring and control capabilities throughout the substation.

Insight by Communication

Based on communication, the global substation automation and integration market are divided into ethernet, power line communication, copper wire, and optic fiber. The copper wire segment is anticipated to have a high CAGR owing to its low attenuation and interference. Furthermore, the increasing investment in telecommunication and IT will contribute to this segment during the forecast period.

Insight by End-User Industry

Based on the end-user industry, the global substation automation and integration market are segmented into utilities, steel, oil & gas, mining, transportation, and others. The utility segment dominates the market because of the demand-supply gap in the energy sector in developed and developing economies. Moreover, the rising government initiatives towards modernizing power grids and rising investment in power generation through renewable resources will accelerate the growth of the segment.

Global Substation Automation and Integration Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

U.S.D. 36.3 Billion |

|

Revenue Forecast in 2035 |

U.S.D. 60.2 Billion |

|

Growth Rate |

6.6% |

|

Segments Covered in the Report |

By offering, By Type, By Installation Type, By Component, Communication, and By End User Industry |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia-Pacific, Middle East, and Rest of the World |

Industry Dynamics

Substation Automation and Integration Market Growth Drivers

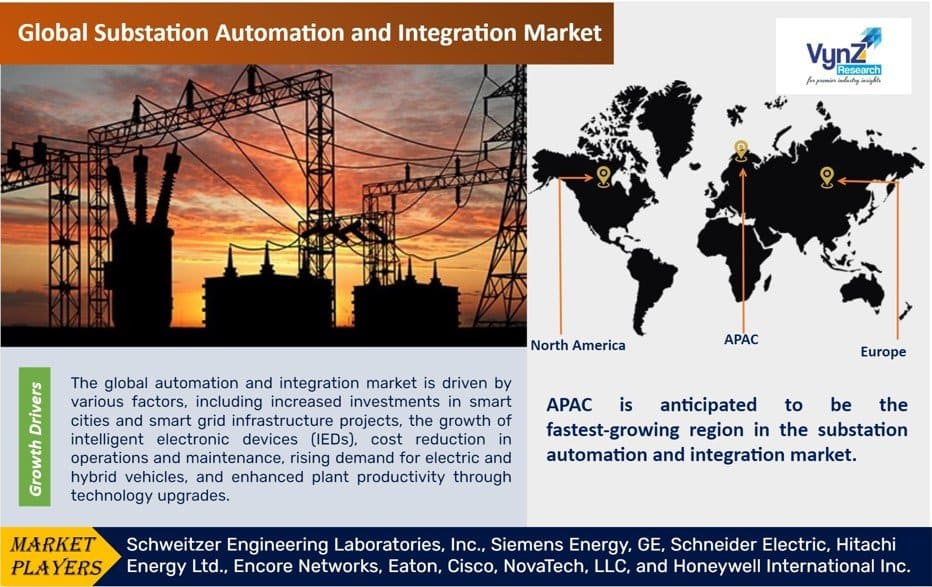

The global automation and integration market is driven by various factors, including increased investments in smart cities and smart grid infrastructure projects, the growth of intelligent electronic devices (IEDs), cost reduction in operations and maintenance, rising demand for electric and hybrid vehicles, and enhanced plant productivity through technology upgrades. Additionally, it offers interlocking and smart load shedding capabilities to ensure grid reliability, performance, and security. According to the International Railway Journal, Germany's federal government has invested $80 million in digital applications to enhance network capacity.

Substation Automation and Integration Market Challenges

The huge capital investment and rigorous governance will hamper the growth of the market. With the increasing use of advanced technologies such as microprocessors and service-oriented architecture (SOA), and the increasing need to integrate various IEDs in substations, the cost of purchasing these substations has increased. The COVID-19 outbreak has slowed down the growth of the power generation industry and renewable energy sector. For instance, China is the primary global producer of clean energy technologies like solar panels, wind turbines, and batteries. Renewable energy companies in China are not able to comply with their deadlines for equipment installation.

Substation Automation and Integration Market Opportunities

The increasing demand for renewable energy projects and the rising adoption of electric and hybrid vehicles are creating lucrative opportunities in the substation automation and integration market. Companies are focusing on investing in sustainable energy infrastructure, investing in solar and wind projects to meet the rising demand for electricity, and minimizing environmental impacts are the opportunities for the growth of the sustainable automation and integration market.

Substation Automation and Integration Market Geographic Overview

APAC is anticipated to be the fastest-growing region in the substation automation and integration market owing to the initiatives by the government to enhance the power and energy sector. For instance, the Indian Government is following a smart infrastructure vision wherein the digitalization of the grid in industrial, commercial, and residential areas, the revival of power distribution utilities, and the electrification of villages will take place. Furthermore, in 2020, the Chinese Government invested $31 billion to revolutionize its grid infrastructure by installing automated substations.

Substation Automation and Integration Market Competitive Insight

The industry players are adopting strategies such as product launches and developments, partnerships, contracts, and mergers and acquisitions to have a strong foothold in the substation automation and integration market.

Hitachi ABB Power Grids launched the new Remote Terminal Unit (RTU) 530 which extends the life of existing power distribution networks and supports the migration to modern technologies with enhanced security features, including secure communication, encryption, and security logging.

Schneider Electric acquired a controlling stake in ETAP Automation Inc. (Dubai), the leading software platform for electrical power systems modeling and simulation, to accelerate and improve the integration of renewables, microgrids, fuel cells, and battery storage technologies to the power grid. The acquisition would pave the way for green data centers, resilient power grids, and decarbonized transport and energy generation.

Some of the key players operating in the substation automation and integration market: are Schweitzer Engineering Laboratories, Inc., Siemens Energy, GE, Schneider Electric, Hitachi Energy Ltd., Encore Networks, Eaton, Cisco, NovaTech, LLC, and Honeywell International Inc.

The Substation Automation and Integration Market report offers a comprehensive market segmentation analysis along with an estimation for the forecast period 2025–2030.

Segments Covered in the Report

- By Offering

- Hardware

- Reclose Controllers

- Programmable Logical Controllers

- Capacitor Banks

- Smart Meters

- Load Tap Changers

- Digital Relays

- Fiber-Optic Cables

- Others

- Software

- Production Management Software

- Asset Management Software

- Performance Management Software

- Services

- Installation and Commissioning

- Up-Gradation and Retrofitting

- Testing, Repair, and Maintenance

- Hardware

- By Type

- Transmission Substation

- Distribution Substation

- By Installation Type

- New Installation

- Retrofit Installation

- By Component

- IEDs (Intelligent Electronic Devices)

- Communication Networks

- SCADA Systems

- By Communication

- Ethernet

- Power Line Communication

- Copper Wire

- Optic Fiber

- By End-User Industry

- Utilities

- Steel

- Oil & Gas

- Mining

- Transportation

- Others

Region Covered in the Report

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- U.K.

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific (APAC)

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Rest of the World (RoW)

- Brazil

- Saudi Arabia

- South Africa

- U.A.E.

- Other Countries

.png "Substation Automation and Integration Market Size")

Source: VynZ Research

.png "Substation Automation and Integration Market Analysis")

Source: VynZ Research

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: 1 888 253 3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Substation Automation and Integration Market