Inter-City eVTOL Aircraft Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Platform Type (Electric VTOL Aircraft, Hybrid VTOL Aircraft), by Application (Passenger Transport, Cargo Transport, Emergency Medical Services, Logistics and Delivery), by End Use (Commercial Operators, Government & Defense, Logistics Companies)

| Status : Published | Published On : May, 2026 | Report Code : VRAD12050 | Industry : Aerospace and Defense | Available Format :

|

Page : 164 |

Inter-City eVTOL Aircraft Market Overview

The inter-city eVTOL aircraft market which was valued at approximately USD 1.4 billion in 2025 and is estimated to rise further up to almost USD 1.6 billion in 2026, is projected to reach around USD 7.6 billion by 2035, expanding at a CAGR of about 18.5% during the forecast period from 2026 to 2035.

The demand for high-speed inter-city mobility solutions drives market expansion because urban traffic congestion increases in major metropolitan corridors while electric propulsion systems and autonomous aviation technologies continue to develop. Also, sustainable aviation and next-generation air mobility platforms gain wider acceptance. The growing demand for time-efficient inter-city transportation solutions which produce low emissions benefits both commercial and institutional aviation systems.

The urban air mobility ecosystem receives support through ongoing infrastructure development which includes vertiport construction, charging network establishment and air traffic management system integration. The government-backed aerospace innovation programs together with advanced mobility initiatives help early-stage commercialization throughout North America, Europe and Asia Pacific regions which have established regulatory frameworks and active aviation modernization efforts to support eVTOL aircraft deployment.

Inter-City eVTOL Aircraft Market Dynamics

Market Trends

The market is experiencing major technology changes because the aviation industry is transitioning to completely electric and self-flying aerial transport systems. The market shows a key trend of moving toward distributed electric propulsion systems because people prefer urban air mobility networks to have better energy efficiency, reduced emissions and extended flight range capabilities. The worldwide civil aviation modernization standards combined with sustainable aviation programs are now using short-haul air transport electrification as their primary development target according to their respective national standards.

Growth Drivers

Market growth depends mainly on increasing passenger needs for rapid inter-city transportation solutions which create permanent demand throughout busy city areas and thriving business districts. The market expands further because cities spend more on developing urban air mobility infrastructures which include vertiports, charging networks and complete aviation systems. The government aviation authorities and smart mobility programs support advanced air mobility development by creating pilot certification systems and building infrastructure readiness programs.

Market Restraints / Challenges

The market faces particular barriers which prevent it from reaching its expected growth potential. The regulatory framework creates a challenging environment for airspace operators because it results in unpredictable certification processes which especially affect new market entrants and equipment providers. The current development of aviation regulatory frameworks needs further time to completely support autonomous electric flight systems which results in regional certification delays.

Market Opportunities

The market creates strong business prospects between urban air mobility systems and inter-city air taxi services because electric propulsion systems and autonomous aviation technology make significant operational enhancements. The market demand for premium passengers and time-sensitive transportation solutions between urban areas will be satisfied by companies which provide scalable aircraft solutions that operate at high performance levels while using less energy.

Global Inter-City eVTOL Aircraft Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 1.4 Billion |

|

Revenue Forecast in 2035 |

USD 7.6 Billion |

|

Growth Rate |

18.5% |

|

Segments Covered in the Report |

Platform Type, Application, End Use |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Airbus, Archer Aviation, Beta Technologies, Boeing, Embraer, EHang Holdings, Joby Aviation, Lilium, Vertical Aerospace, Volocopter |

|

Customization |

Available upon request |

Inter-City eVTOL Aircraft Market Segmentation

By Platform Type

The year 2025 saw Electric VTOL aircraft lead the revenue market with a 62% share which resulted from people adopting fully electric propulsion systems, their lower operational expenses and the aircraft's growing compliance with worldwide sustainability standards and zero-emission aviation objectives. The combination of regulatory aviation frameworks that support decarbonization and electric mobility together with government-supported urban air mobility programs establish the segment's continuous growth in all developed aviation markets.

The period from 2026 to 2035 will see Hybrid VTOL aircraft experience faster growth with a projected CAGR of 19.6%, which results from their ability to operate longer distances while carrying more weight and their capacity to function across extended inter-city travel times. The adoption of next-generation propulsion systems and transitional aviation technologies receives support from increased investments in these technologies, especially in areas where charging infrastructure remains incomplete and hybrid systems enable continuous operational performance.

By Application

Passenger transport held the largest market share in 2025, accounting for approximately 58% of total revenue, driven by rising demand for high-speed inter-city mobility solutions, increasing urban congestion, and growing preference for premium air taxi services. Smart mobility programs supported by government funding, together with aviation modernization initiatives, make it easier for passenger-focused air mobility networks to expand their operations.

The forecast period will see logistics and delivery applications achieve the highest growth rate with their projected 20.4% CAGR, which results from the increasing need for businesses to move cargo quickly between cities, the expansion of e-commerce ecosystems and the rising adoption of time-sensitive aerial delivery solutions. Emergency medical services experience steady adoption growth with a 17.8% CAGR, which results from people needing faster response times and the healthcare field adopting air medical evacuation systems into their advanced infrastructure.

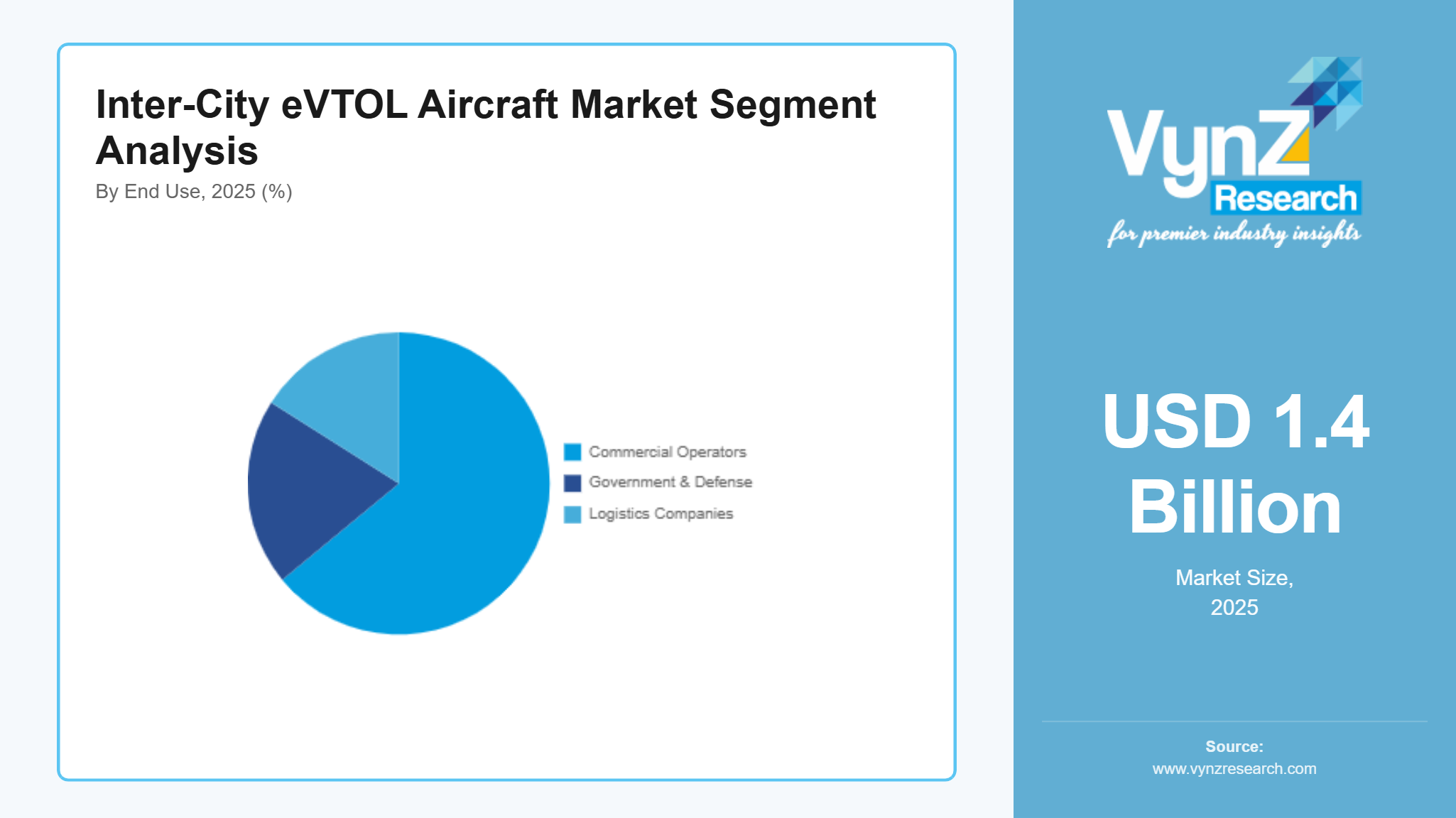

By End Use

Commercial operators accounted for the largest revenue share in 2025 at approximately 64%, which resulted from air taxi services entering their commercial phase, urban air mobility platforms receiving private sector funding and customers demanding high-end inter-city transportation services. Commercial eVTOL certification and deployment gains regulatory support from aviation authorities, which enhances this segment's market position.

Government & defense applications will achieve the highest growth rate between 2026 and 2035 with a 19.1% CAGR, which results from military financing of advanced aerial mobility systems that provide surveillance capabilities and rapid transport services and strategic mobility operations. The logistics sector shows strong growth at an 18.7% CAGR because businesses require fast freight services and aerial logistics networks become part of supply chain modernization initiatives in major economies.

Regional Insights

North America

The market in 2025 achieved 34% market share from North America because aerospace innovation ability, advanced air mobility infrastructure investment and initial aviation regulatory approval from Federal Aviation Administration both contributed to market growth. Intercity aerial mobility solutions receive their first usage in New York, Los Angeles and San Francisco because those cities need premium passenger transport and high-speed business travel corridors. The government provides electric aircraft research and development funding and pilot urban air mobility programs, which create conditions for large companies to invest in eVTOL deployment ecosystems. The regional market performance improved through enhanced cooperation between aerospace manufacturers and mobility service providers, which studied digital air traffic integration platforms to achieve faster commercialization development in urban corridor areas.

Europe

European markets achieved 28% market share in 2025 because the European Union Aviation Safety Agency framework enables sustainable aviation regulatory compliance and countries work towards carbon-free transportation systems. Germany, France, the United Kingdom and the Netherlands currently demonstrate increased utilization of advanced air mobility technologies for their inter-city passenger and regional transport needs. Government-supported green mobility initiatives together with public funding for aerospace electrification projects drive market growth in the industry. The integration of smart mobility infrastructure together with increasing funding for vertiport construction and aviation digitalization development creates better conditions for deploying new systems. The Western and Central European economies experience sustained market demand because their regions depend on improved inter-city transport systems and decreased local traffic congestion.

Asia Pacific

The market in Asia Pacific reached 26% of the market share in 2025 because rapid urbanization, growing middle-class population and need for effective inter-city transport solutions created market demand. The countries lead advanced air mobility system development through their complete aerospace manufacturing networks and increasing investment in smart transportation systems. The government operates smart city projects and aviation modernization programs which drive electric aviation technology development through eVTOL research funding, pilot corridor testing and infrastructure building funding. Major cities in Beijing, Shanghai, Tokyo and Mumbai currently face increased demand for speedy inter-city transportation solutions because their traffic situation becomes more congested, which digital aviation platforms use to enhance their operational capabilities throughout the area.

Rest of the World

The market in 2025, which includes Latin America, the Middle East, and Africa, reached a market share of 12% for the rest of the world. The regions experience economic development because countries increase their aviation infrastructure investments, people start using advanced mobility solutions and countries begin using sustainable transport technologies. The United Arab Emirates, Brazil and South Africa are currently assessing pilot projects for their urban air mobility systems. Middle East governments fund aviation diversification programs and smart mobility projects, especially in the UAE and Saudi Arabia, which promote eVTOL systems for tourism and inter-city travel and delivery services.

Competitive Landscape / Company Insights

The market maintains a competitive level between moderate and high because global aerospace manufacturers, advanced air mobility startups and aviation technology providers all work on developing new aircraft designs while they pursue certification and expand their operations to new areas. Companies are increasing their research and development spending together with their autonomous flight system development and battery efficiency research to improve their competitive advantage in the market. The competition in the market has intensified because both government aviation authorities and international civil aviation organizations have established sustainable air mobility systems for low-emission transport development. The growing partnerships between public sector aviation assets and private aerospace companies are determining how emerging urban air mobility systems will commercialize their products in markets around the world.

Mini Profiles

Airbus focuses on advanced aerospace and electric vertical take-off and landing aircraft development, supported by strong global brand recognition and extensive aviation manufacturing capabilities across commercial and defense aviation ecosystems worldwide.

Beta Technologies operates in the niche advanced air mobility segment, emphasizing performance-driven electric aircraft design, long-range efficiency, and integrated charging infrastructure solutions supporting sustainable regional and inter-city aviation networks.

Joby Aviation leverages strong digital aviation innovation and strategic partnerships with mobility platforms to expand market presence, focusing on high-performance eVTOL aircraft and scalable urban air taxi commercialization models globally.

Embraer focuses on regional aerospace and hybrid-electric aircraft solutions, supported by strong manufacturing expertise and established airline partnerships, enabling expansion into next-generation sustainable inter-city air mobility systems.

EHang Holdings leverages autonomous flight technology and digital aviation systems to expand market presence, focusing on pilotless eVTOL aircraft solutions supported by strong integration of smart city and urban mobility ecosystems.

Key Players

- Airbus

- Archer Aviation

- Beta Technologies

- Boeing

- Embraer

- EHang Holdings

- Joby Aviation

- Lilium

- Vertical Aerospace

- Volocopter

Recent Developments

In March 2026, Archer Aviation advanced its commercial air taxi readiness program by expanding FAA-supported flight testing under urban air mobility integration frameworks in the United States. The company also strengthened its operational ecosystem by enhancing collaboration with aviation regulators for certification and airspace integration readiness.

In January 2026, Volocopter progressed its European commercialization strategy by expanding validation flights for its electric air taxi system across key urban corridors. The company also strengthened partnerships with European aviation authorities to support certification and operational deployment in regulated airspace environments.

In November 2025, Lilium accelerated its eVTOL development program by enhancing its jet-powered electric aircraft testing phase for inter-city mobility applications. The company also focused on improving aircraft range efficiency and progressing toward commercial certification in European aviation markets.

In July 2025, Vertical Aerospace expanded its VX4 eVTOL aircraft development program through additional test flight validation and strengthened collaboration with international aviation partners. The initiative focused on improving aircraft safety systems and accelerating regulatory approval for commercial deployment.

In August 2025, Boeing increased its investment in advanced air mobility research by supporting next-generation electric and hybrid VTOL aircraft development programs. The company also strengthened its aerospace innovation partnerships to support future integration of urban and inter-city air mobility solutions.

Global Inter-City eVTOL Aircraft Market Coverage

Platform Type Insight and Forecast 2026 - 2035

- Electric VTOL Aircraft

- Hybrid VTOL Aircraft

Application Insight and Forecast 2026 - 2035

- Passenger Transport

- Cargo Transport

- Emergency Medical Services

- Logistics and Delivery

End Use Insight and Forecast 2026 - 2035

- Commercial Operators

- Government & Defense

- Logistics Companies

Global Inter-City eVTOL Aircraft Market by Region

- North America

- By Platform Type

- By Application

- By End Use

- By Country - U.S., Canada, Mexico

- Europe

- By Platform Type

- By Application

- By End Use

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Platform Type

- By Application

- By End Use

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Platform Type

- By Application

- By End Use

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Inter-City eVTOL Aircraft Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Platform Type

1.2.2. By

Application

1.2.3. By

End Use

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Platform Type

5.1.1. Electric VTOL Aircraft

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Hybrid VTOL Aircraft

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.2. By Application

5.2.1. Passenger Transport

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Cargo Transport

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Emergency Medical Services

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Logistics and Delivery

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.3. By End Use

5.3.1. Commercial Operators

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Government & Defense

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Logistics Companies

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Platform Type

6.2. By

Application

6.3. By

End Use

6.3.1.

U.S. Market Estimate and Forecast

6.3.2.

Canada Market Estimate and Forecast

6.3.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Platform Type

7.2. By

Application

7.3. By

End Use

7.3.1.

Germany Market Estimate and Forecast

7.3.2.

France Market Estimate and Forecast

7.3.3.

U.K. Market Estimate and Forecast

7.3.4.

Italy Market Estimate and Forecast

7.3.5.

Spain Market Estimate and Forecast

7.3.6.

Russia Market Estimate and Forecast

7.3.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Platform Type

8.2. By

Application

8.3. By

End Use

8.3.1.

China Market Estimate and Forecast

8.3.2.

Japan Market Estimate and Forecast

8.3.3.

India Market Estimate and Forecast

8.3.4.

South Korea Market Estimate and Forecast

8.3.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Platform Type

9.2. By

Application

9.3. By

End Use

9.3.1.

Brazil Market Estimate and Forecast

9.3.2.

Saudi Arabia Market Estimate and Forecast

9.3.3.

South Africa Market Estimate and Forecast

9.3.4.

U.A.E. Market Estimate and Forecast

9.3.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Airbus

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Archer Aviation

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Beta Technologies

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Boeing

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Embraer

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

EHang Holdings

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Joby Aviation

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Lilium

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Vertical Aerospace

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Volocopter

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Inter-City eVTOL Aircraft Market