Cargo Shipping Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Shipping Type (Container Shipping, Bulk Shipping, Breakbulk Shipping, RoRo (Roll-on/Roll-off) Shipping), by Vessel Type (Container Ships, Bulk Carriers, Tankers, General Cargo Ships, RoRo Ships, Others), by Service Type (Liner Shipping Services, Tramp Shipping Services, Freight Forwarding, Shipping Brokerage, Integrated Logistics Services), by End Use Industry (Manufacturing, Oil & Gas / Energy, Agriculture & Food, Retail & E-commerce, Automotive, Chemicals, Pharmaceuticals)

| Status : Published | Published On : Apr, 2026 | Report Code : VRAT9668 | Industry : Automotive & Transportation | Available Format :

|

Page : 190 |

Cargo Shipping Market Overview

The cargo shipping market which was valued at approximately USD 15.17 billion in 2025 and is estimated to reach around USD 16.61 billion in 2026, is projected to reach close to USD 30.62 billion by 2035, expanding at a CAGR of about 7.0% during the forecast period from 2026 to 2035.

The cargo shipping market is primarily driven by the central role of maritime transport in global trade and supply chains, spanning containerized freight, dry bulk commodities, liquid bulk, and specialized cargoes. Demand is supported by growth in international merchandise trade, ongoing diversification of manufacturing and sourcing, and the expansion of e-commerce and time-sensitive replenishment networks that increase the need for reliable port-to-port and intermodal connectivity. Industry operations are also being reshaped by digitalization across booking, documentation, tracking, and port call optimization, improving visibility and asset utilization.

At the same time, regulatory pressure to reduce emissions is accelerating investment in energy-efficiency measures and alternative fuel readiness; the IMO’s EEXI and CII requirements have applied from 2023 and are designed to improve ship energy efficiency and reduce carbon intensity over time. The market is supported by trade activity, port and logistics infrastructure investment, and fleet modernization initiatives aimed at improving efficiency, reliability, and environmental performance.

Cargo Shipping Market Dynamics

Market Trends

The increasing adoption of digitalization and smart shipping technologies is significantly transforming the cargo shipping market by enhancing efficiency, transparency, and coordination across global supply chains. Shipping companies and port authorities are actively integrating advanced technologies such as artificial intelligence, Internet of Things (IoT), blockchain, and big data analytics to streamline operations and improve overall performance. These technologies enable optimized route planning, real-time cargo tracking, and advanced fleet management, allowing companies to make data-driven decisions and improve service reliability. In Asia-Pacific, governments like India are investing heavily through initiatives such as the Sagarmala Programme and Maritime Vision 2047, which include funding for port digitalization, smart logistics platforms, and advanced tracking systems, with overall maritime investments exceeding $140 billion in recent years. Digital platforms are playing a crucial role in connecting various stakeholders, including ports, shipping lines, freight forwarders, and logistics providers, ensuring seamless communication and faster documentation processes. Smart port initiatives, including automated cargo handling systems, digital twins, and port community systems, are improving operational speed and reducing turnaround times.

Growth Drivers

Key drivers of the cargo shipping market include the scale and persistence of seaborne trade flows, continued reliance on maritime transport for bulk raw materials and energy commodities, and expanding containerized trade supported by manufacturing output and retail replenishment. According to UNCTAD, global seaborne trade growth was modest in 2024 (about 2.2%) and is expected to slow in 2025 (around 0.5%) before returning to a higher average pace over 2026–2030, underscoring both the market’s long-term demand base and its sensitivity to macroeconomic and geopolitical conditions. Infrastructure investment in ports, hinterland connectivity, and intermodal logistics also supports demand by improving throughput and reducing dwell time. In addition, decarbonization requirements are prompting fleet renewal and efficiency upgrades; the IMO’s EEXI and CII measures (in force since 2023) require ships to improve technical energy efficiency and manage operational carbon intensity, reinforcing demand for compliant tonnage and performance-driven services.

Market Restraints / Challenges

Key challenges for the cargo shipping market include high exposure to geopolitical risk and weather-related disruptions at major chokepoints, which can force rerouting, raise fuel and insurance costs, and reduce schedule reliability. Freight rates and profitability can also be volatile due to shifting supply–demand balance, capacity additions, and bunker fuel price fluctuations. Compliance costs are rising as environmental regulation tightens; meeting IMO efficiency requirements and navigating regional measures (such as carbon pricing and fuel standards) can require significant capital investment in retrofits, alternative-fuel capable newbuilds, and operational optimization. In addition, port congestion and landside bottlenecks can extend turnaround times and create knock-on delays across networks. Cybersecurity risk is also increasing as shipping and ports digitize operational systems and documentation, elevating the importance of resilient IT and data governance practices.

Market Opportunities

The cargo shipping market offers significant opportunities in digital trade enablement, port efficiency programs, and decarbonization-led fleet and service innovation. As shippers seek higher visibility and reliability, there is growing demand for end-to-end solutions that integrate ocean carriage with freight forwarding, customs documentation, and inland logistics, supported by real-time tracking and analytics. Another opportunity lies in operational efficiency and congestion reduction through data sharing, berth window discipline, and just-in-time arrival practices that lower waiting time and fuel consumption. Sustainability is a major opportunity area as carriers invest in energy-saving devices, hull and propeller upgrades, wind-assist technologies, and alternative fuels such as methanol- and ammonia-ready designs to meet tightening requirements and customer Scope 3 expectations. Emerging trade corridors and continued investment in port and hinterland infrastructure particularly in Asia-Pacific, the Middle East, and parts of Africa also support network expansion and feeder services, enabling growth in both containerized and bulk shipping segments.

Global Cargo Shipping Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 15.17 Billion |

|

Revenue Forecast in 2035 |

USD 30.62 Billion |

|

Growth Rate |

7.0% |

|

Segments Covered in the Report |

Cargo Type, Ship Type, Service Type, End Use Industry |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia-Pacific, Latin America, Middle East & Africa |

|

Key Companies |

A.P. Moller - Maersk, MSC Mediterranean Shipping Company, CMA CGM Group, COSCO Shipping Holdings, Hapag-Lloyd, Ocean Network Express (ONE), Evergreen Marine Corp., Yang Ming Marine Transport, ZIM Integrated Shipping Services, Mitsui O.S.K. Lines (MOL) |

|

Customization |

Available upon request |

Cargo Shipping Market Segmentation

By Shipping Method

Container shipping is the largest shipping-method segment with a market share of about 45% in 2025, supported by standardized container handling, extensive liner networks, and strong demand for transporting manufactured goods and consumer products. The segment benefits from scale economies, high service frequency on major lanes, and improving digital workflows for booking and documentation. However, rate levels and service reliability can fluctuate with capacity cycles, port congestion, and route disruptions.

RoRo shipping is the fastest-growing segment with a CAGR of 7.2% during the forecast period, primarily driven by increasing global automotive trade and rising exports of vehicles and heavy machinery. Unlike container shipping, RoRo allows cargo to be directly driven on and off vessels, significantly improving loading efficiency and reducing handling damage. The expansion of electric vehicle exports, industrial equipment transportation, and infrastructure-related machinery shipments is accelerating demand.

By Vessel Type

Container ships are the largest segment with a market share of about 40% in 2025, due to the dominance of containerized cargo in international trade, container ships account for the largest share in the vessel segment. These ships are designed for high-capacity transport with standardized loading systems, enabling cost-effective and efficient long-distance shipping. Major global trade routes heavily rely on container vessels, particularly for transporting manufactured goods. The continued growth of global trade and supply chain integration further supports the strong demand for container ships.

RoRo ships are the fastest-growing segment with a CAGR of 7.5% during the forecast period, due to the rising demand for vehicle and heavy equipment transportation, RoRo ships are the fastest-growing vessel segment. Their design, which includes ramps and multiple decks, allows for faster loading and unloading compared to traditional vessels.

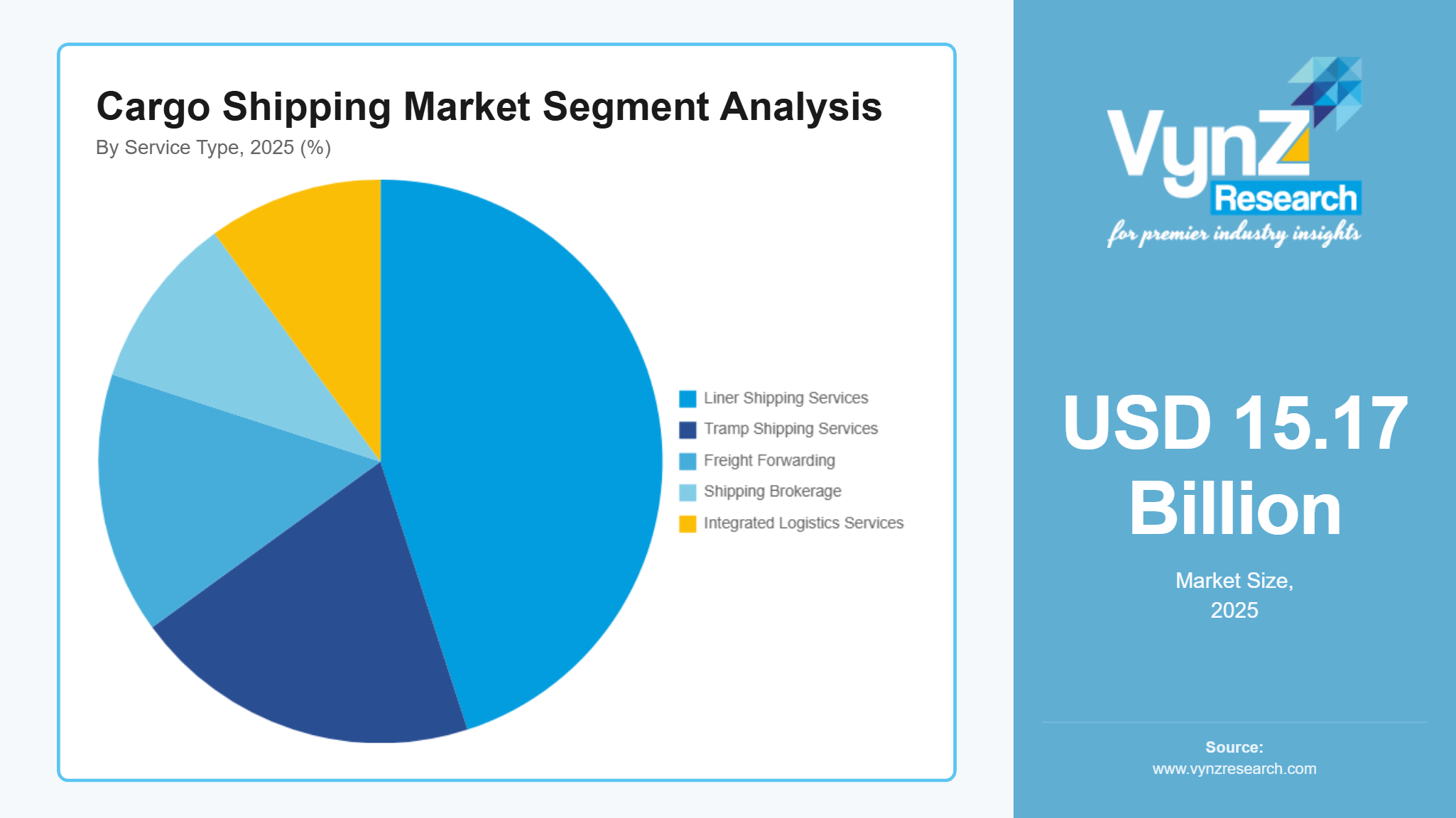

By Service Type

Liner shipping services are the largest category with a market share of about 45% in 2025, due to the need for reliable and scheduled transportation of goods, liner shipping services dominate the service segment. These services operate on fixed routes and timetables, making them essential for containerized trade and supply chain planning. Businesses depend on the predictability and consistency of liner services for timely delivery, which supports their widespread adoption across global trade networks.

Integrated logistics services are the fastest-growing category with a CAGR of 7.7% during the forecast period, due to the increasing demand for end-to-end supply chain solutions, integrated logistics services are the fastest-growing segment. These services combine transportation, warehousing, inventory management, and distribution into a single solution. The rapid growth of e-commerce, globalization, and the need for cost optimization and supply chain visibility are key factors driving the expansion of this segment.

By End Use Industry

Manufacturing is the largest end-use category with a market share of about 30% in 2025, supported by sustained movement of intermediate goods, components, and finished products across global production networks. Shipping demand is reinforced by inventory replenishment cycles, diversification of sourcing, and the continued need to move heavy and high-volume inputs such as metals, minerals, and industrial materials. Integrated ocean-and-inland logistics, schedule reliability, and port connectivity are key service requirements for manufacturing shippers.

Retail & e-commerce is the fastest-growing end-use category with a CAGR of 7.9% during the forecast period, owing to increasing cross-border order flows, higher frequency replenishment, and the need for flexible capacity allocation to meet seasonal peaks. Growth is further supported by expansion of omni-channel distribution networks, greater use of freight forwarding and digital platforms to procure capacity, and improving visibility through tracking and data integration across carriers, ports, and inland logistics providers.

Regional Insights

North America

North America is a major regional market for cargo shipping, supported by high containerized import volumes, strong demand for energy and agricultural exports, and large-scale port and inland logistics networks. The United States plays a central role through major gateway ports on the Pacific, Atlantic, and Gulf coasts and extensive rail connectivity that supports intermodal freight distribution. In 2026, the U.S. Department of Transportation announced ~$488 million funding to upgrade ports, improve cargo handling capacity, and streamline logistics operations Market dynamics in the region are influenced by inventory cycles, consumer demand, and port productivity, as well as exposure to disruptions that can shift volumes across coasts and gateways. Increasing focus on emissions performance and transparency is also shaping contracting and operational practices for carriers and shippers serving North American trade lanes.

Asia-Pacific

Asia-Pacific is the largest region with a market share of about 40% in 2025, and it is also fastest-growing region during the forecast period, driven by its role as the world’s leading manufacturing base and a major hub for containerized exports and intra-Asia trade. China, Southeast Asia, and India support strong demand across container, bulk, and tanker segments, while major transshipment hubs enable extensive feeder connectivity. Growth is reinforced by port capacity expansion, logistics infrastructure investment, and rising South–South trade flows. India secured over ₹12 lakh crore (≈$145+ billion) in maritime investments during India Maritime Week 2025, with significant allocation toward port development, shipping, and sustainability. The region is also advancing adoption of digital port systems and automation to improve turnaround times and resilience, while carriers and ports increasingly invest in efficiency and alternative-fuel readiness to align with tightening emissions requirements.

Europe

Europe maintains a strong position in cargo shipping due to large consumer markets, diversified industrial trade flows, and dense port and hinterland connectivity across the North Sea, Mediterranean, and Baltic regions. Major hubs and gateways support high container throughput and significant bulk and energy cargo movements. Regulatory developments are particularly influential in the region, including the application of carbon pricing to maritime transport through the EU ETS framework, which increases the importance of emissions-efficient operations, contracting practices, and investment in cleaner technologies. The European Union has launched the Global Gateway Initiative, allocating around €300 billion (2021–2027) for global infrastructure, including ports, maritime corridors, and logistics networks. Europe’s continued focus on port modernization, digital trade facilitation, and supply chain resilience supports steady demand for cargo shipping services.

Latin America

The rest of the world, comprising the Middle East & Africa and Latin America, represents a rapidly developing segment of the global cargo shipping market, driven by expanding trade activities, strategic geographic positioning, and increasing government focus on maritime infrastructure. Governments across these regions are investing in port expansion, modernization, and the development of integrated logistics hubs to enhance cargo handling capacity and strengthen their roles in global trade networks. The Middle East is emerging as a major transshipment hub connecting key international routes, while African nations are improving port connectivity and regional trade integration to support growing cargo volumes. Latin America is focusing on strengthening export-oriented infrastructure, particularly for commodities such as oil, minerals, and agricultural products, by upgrading ports and bulk handling facilities. There are a strong push toward public-private partnerships and foreign investments to accelerate infrastructure development and improve operational efficiency. Governments are also implementing regulatory reforms and adopting digital port technologies to streamline cargo movement, reduce congestion, and enhance supply chain performance.

Competitive Landscape / Company Insights

The cargo shipping market is competitive and characterized by the presence of large global liner operators, diversified shipping groups, and specialized bulk and tanker owners, alongside freight forwarders and integrated logistics providers. Major container carriers such as A.P. Moller - Maersk, MSC, CMA CGM, COSCO Shipping, Hapag-Lloyd, and Ocean Network Express (ONE) maintain strong positions through extensive service networks, large fleets, long-term shipper relationships, and growing logistics capabilities that extend beyond port-to-port transport. Competitive advantages are often tied to scale, service frequency, schedule reliability, terminal access, digital customer platforms, and the ability to offer end-to-end solutions including warehousing, customs brokerage, and inland transportation.

Other shipping and logistics providers compete by focusing on specific trade lanes, cargo types, and value-added services such as project cargo, temperature-controlled logistics, dangerous goods handling, and time-critical intermodal distribution. Across the market, digitalization is a key differentiator, with carriers investing in online booking, dynamic pricing, real-time tracking, and automated documentation to improve customer experience and reduce administrative friction. Sustainability is also becoming a competitive factor as shippers increasingly evaluate carriers on emissions performance and decarbonization roadmaps, encouraging investment in energy-saving technologies and alternative-fuel vessels. Competitive strategies commonly include fleet renewal, alliances and network partnerships, terminal and equipment investments to improve service reliability, and expansion of integrated logistics offerings to capture a greater share of supply chain spend.

Mini Profiles

A.P. Moller - Maersk is a global shipping and logistics company with a large container shipping fleet and expanding end-to-end logistics capabilities including terminal operations, inland transport, and supply chain services.

MSC Mediterranean Shipping Company is one of the world’s largest container shipping operators, providing global liner services and logistics offerings through an extensive network of routes and port calls.

CMA CGM Group operates global container shipping services and has expanded into logistics and air cargo, supporting integrated transport solutions across key trade lanes.

COSCO Shipping Holdings is a major global shipping group with container shipping operations and broader maritime logistics capabilities, supporting international trade across Asia, Europe, and the Americas.

Hapag-Lloyd is a leading global liner shipping company providing container services across major East–West and North–South trades, with ongoing investment in fleet modernization and digital customer platforms.

Key Players

- A.P. Møller – Mærsk A/S (Maersk)

- Mediterranean Shipping Company S.A.

- CMA CGM S.A.

- COSCO SHIPPING Holdings Co., Ltd.

- Hapag-Lloyd Aktiengesellschaft

- Ocean Network Express Pte. Ltd.

- Evergreen Marine Corporation (Taiwan) Ltd.

- Yang Ming Marine Transport Corporation

- ZIM Integrated Shipping Services Ltd.

- Mitsui O.S.K. Lines, Ltd.

Recent Developments

January 2026 – TE Connectivity Ltd. announced the expansion of its aerospace interconnect manufacturing facility in Europe to support rising demand for high-reliability connectors and wiring systems used in next-generation commercial and defense aircraft.

December 2025 – Amphenol Corporation introduced a new lightweight high-speed aerospace connector platform designed to support advanced avionics networks and high-bandwidth aircraft data transmission systems.

October 2025 – GKN Aerospace Services Limited announced a collaboration with major aircraft manufacturers to develop advanced electrical wiring interconnection systems for more electric aircraft architectures and future hybrid-electric aviation platforms.

June 2025 – Carlisle Interconnect Technologies launched a new range of high-temperature aerospace cables and wiring harness solutions designed to support high-power electrical systems and advanced avionics in modern aircraft platforms.

Global Cargo Shipping Market Coverage

Shipping Type Insight and Forecast 2026 - 2035

- Container Shipping

- Bulk Shipping

- Breakbulk Shipping

- RoRo (Roll-on/Roll-off) Shipping

Vessel Type Insight and Forecast 2026 - 2035

- Container Ships

- Bulk Carriers

- Tankers

- General Cargo Ships

- RoRo Ships

- Others

Service Type Insight and Forecast 2026 - 2035

- Liner Shipping Services

- Tramp Shipping Services

- Freight Forwarding

- Shipping Brokerage

- Integrated Logistics Services

End Use Industry Insight and Forecast 2026 - 2035

- Manufacturing

- Oil & Gas / Energy

- Agriculture & Food

- Retail & E-commerce

- Automotive

- Chemicals

- Pharmaceuticals

Global Cargo Shipping Market by Region

- North America

- By Shipping Type

- By Vessel Type

- By Service Type

- By End Use Industry

- By Country - U.S., Canada, Mexico

- Europe

- By Shipping Type

- By Vessel Type

- By Service Type

- By End Use Industry

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Shipping Type

- By Vessel Type

- By Service Type

- By End Use Industry

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Shipping Type

- By Vessel Type

- By Service Type

- By End Use Industry

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Cargo Shipping Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Shipping Type

1.2.2. By

Vessel Type

1.2.3. By

Service Type

1.2.4. By

End Use Industry

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Shipping Type

5.1.1. Container Shipping

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Bulk Shipping

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Breakbulk Shipping

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. RoRo (Roll-on/Roll-off) Shipping

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.2. By Vessel Type

5.2.1. Container Ships

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Bulk Carriers

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Tankers

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. General Cargo Ships

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. RoRo Ships

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.2.6. Others

5.2.6.1. Market Definition

5.2.6.2. Market Estimation and Forecast to 2035

5.3. By Service Type

5.3.1. Liner Shipping Services

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Tramp Shipping Services

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Freight Forwarding

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Shipping Brokerage

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Integrated Logistics Services

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.4. By End Use Industry

5.4.1. Manufacturing

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Oil & Gas / Energy

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Agriculture & Food

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Retail & E-commerce

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Automotive

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

5.4.6. Chemicals

5.4.6.1. Market Definition

5.4.6.2. Market Estimation and Forecast to 2035

5.4.7. Pharmaceuticals

5.4.7.1. Market Definition

5.4.7.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Shipping Type

6.2. By

Vessel Type

6.3. By

Service Type

6.4. By

End Use Industry

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Shipping Type

7.2. By

Vessel Type

7.3. By

Service Type

7.4. By

End Use Industry

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Shipping Type

8.2. By

Vessel Type

8.3. By

Service Type

8.4. By

End Use Industry

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Shipping Type

9.2. By

Vessel Type

9.3. By

Service Type

9.4. By

End Use Industry

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

A.P. Møller – Mærsk A/S (Maersk)

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Mediterranean Shipping Company S.A.

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

CMA CGM S.A.

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

COSCO SHIPPING Holdings Co., Ltd.

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Hapag-Lloyd Aktiengesellschaft

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Ocean Network Express Pte. Ltd.

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Evergreen Marine Corporation (Taiwan) Ltd.

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Yang Ming Marine Transport Corporation

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

ZIM Integrated Shipping Services Ltd.

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Mitsui O.S.K. Lines, Ltd.

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Cargo Shipping Market