Europe ADAS Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by System Type (Adaptive Cruise Control, Blind Spot Detection, Autonomous Emergency Braking, Lane Departure Warning System, Parking Assistance, Forward Collision Warning, Driver Monitoring System, Traffic Sign Recognition), by Sensor Type (Radar Sensors, LiDAR Sensors, Ultrasonic Sensors, Image Sensors, Infrared Sensors), by Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles), by Propulsion Type (Internal Combustion Engine Vehicles, Electric Vehicles, Hybrid Vehicles), by Region (Germany, United Kingdom, France, Italy, Rest of Europe)

| Status : Published | Published On : May, 2026 | Report Code : VRAT9675 | Industry : Automotive & Transportation | Available Format :

|

Page : 123 |

Europe ADAS Market Overview

The Europe ADAS market which was valued at approximately USD 35.5 billion in 2025 and is estimated to rise further up to almost USD 39.0 billion by 2026, is projected to reach around USD 98.4 billion in 2035, expanding at a CAGR of about 10.8% during the forecast period from 2026 to 2035.

Market growth is fueled by rising vehicle safety rules, more electric vehicle production, stronger rollout of intelligent driving assistance tools and more people adopting autonomous and connected mobility services. The surge in need for passenger vehicle safety systems and continued investments into smarter transport infrastructure and road safety programs backed by the European Commission, the European New Car Assessment Program and various regional automotive authorities is helping the market spread further in key places such as Germany, France and the United Kingdom.

Europe ADAS Market Dynamics

Market Trends

The industry is seeing big shifts around smarter safety integration, autonomous driving bits and connected mobility adoption. Higher deployment of advanced driver monitoring systems and autonomous emergency braking solutions shows inclination toward vehicle safety, regulatory compliance and operational efficiency. There is also a shift toward AI enabled mobility platforms and connected vehicle technologies mostly due to rapid digitalization transportation modernization effort. These changes make manufacturers more inclined to build integrated sensor systems, smarter navigation capabilities and predictive safety strategies. Meanwhile reports, and vehicle safety programs supported by the European Commission as well as the European New Car Assessment Program keep pushing adoption forward across Europe.

Growth Drivers

The market is mostly backed by strict vehicle safety regulations and also the increasing demand for connected mobility technologies, which basically keeps demand strong in both passenger vehicles and commercial use cases. More spending on electric vehicle manufacturing, intelligent transportation infrastructure and automotive software development is further speeding up the market’s movement. Consumer sentiment is also shifting toward safer and more technology rich vehicles thereby helping adoption. Since automakers tend to prioritize compliance, fuel efficiency and improved driving assistance functions, demand for intelligent driver assistance systems is expected to stay high across the forecast horizon. Transportation safety initiatives introduced by the European Commission are giving the whole industry expansion an additional boost.

Market Restraints / Challenges

Even with decent growth momentum, the market has obstacles that could slow it down. For example, high rollout costs, semiconductor reliance and complicated software integration keep squeezing profitability, reducing deeper market penetration for mid-tier vehicle manufacturers and smaller supplier ecosystems. Cybersecurity risks and evolving regulatory compliance needs create operational headaches for manufacturers and technology providers. Dependence on imported electronic components and advanced sensing technologies trigger supply chain disruptions, push costs upward and delay product launch during unstable economic conditions. Regulatory organizations and European automotive safety authorities are also tightening cybersecurity and connected vehicle requirements urging industry players to handle more compliance and operating obligations.

Market Opportunities

Opportunities lie in autonomous mobility platforms and electric vehicle safety integration due to increased investment in intelligent transportation infrastructure and connected driving technologies. Businesses that provide AI enabled driver assistance systems, high performance sensors and scalable safety solutions are positioned to gain extra demand from automotive manufacturers and fleet operators. More investment in software defined vehicle technologies, smart mobility ecosystems and digital enabled automotive solutions is opening the door to better margins and long-term commercial partnerships. Advances in artificial intelligence, intelligent traffic management systems and vehicle connectivity technologies are expected to improve operational efficiency and strengthen customer engagement across Europe.

Europe ADAS Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 35.5 Billion |

|

Revenue Forecast in 2035 |

USD 98.4 Billion |

|

Growth Rate |

10.8% |

|

Segments Covered in the Report |

System Type, Sensor Type, Vehicle Type, Propulsion Type |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

Germany, United Kingdom, France, Italy, Rest of Europe |

|

Key Companies |

Aptiv PLC, Autoliv Inc., Continental AG, Denso Corporation, Infineon Technologies AG, Magna International Inc., Mobileye Global Inc., Robert Bosch GmbH, Valeo SA, ZF Friedrichshafen AG |

|

Customization |

Available upon request |

Europe ADAS Market Segmentation

By System Type

In 2025 autonomous emergency braking held about 24% of total revenue due to stricter vehicle safety rules. Over the forecast period it is expected to climb at roughly 10.6% CAGR mainly because collision prevention solutions are getting more attention, while Europe keeps tightening automotive safety compliance expectations.

For driver monitoring systems, growth is anticipated to land around 11.8% supported by the increased focus on driver fatigue detection and intelligent cabin safety integration angle that is becoming standard.

By Sensor Type

Radar sensors held the highest market share in 2025, at around 36%, and this is largely due to wider use in adaptive cruise control and collision avoidance systems. More connected vehicles are being produced and continued investments in advanced mobility technologies are keeping the radar segment moving forward. During the forecast period, radar sensors are expected to expand at nearly 10.2% due to strong adoption by automakers and the broader expansion of autonomous driving capabilities.

LiDAR sensors are expected to post the quickest growth, approximately 12.4%, mostly due to higher deployment in autonomous mobility scenarios and intelligent navigation systems. Improvements in high precision mapping technologies and ongoing spending on premium electric vehicle development are helping adoption increase across Europe.

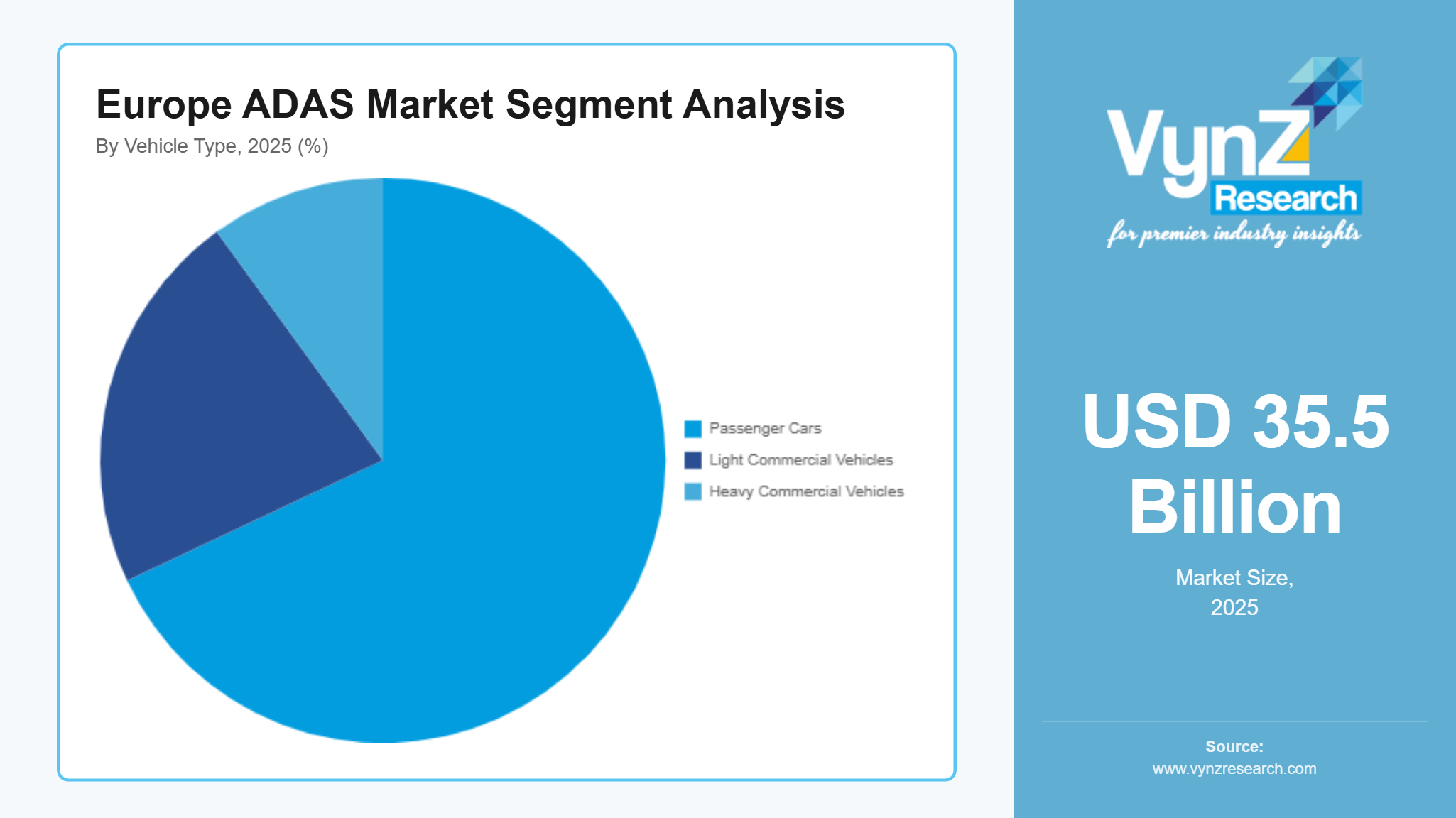

By Vehicle Type

Passenger cars generated the largest revenue share in 2025, at nearly 68%, driven by consumer demand for intelligent safety systems and the growing integration of connected driving technologies in both compact and luxury models. This segment is also forecast to grow around 10.5% CAGR, supported by electric vehicle adoption and tighter regional vehicle safety regulations rolling out across major European automotive markets.

Light commercial vehicles are forecast to grow the fastest, about 11.6%, mainly due to expanding logistics activities, fleet modernization efforts and a growing need for driver safety technologies in urban transportation environments. Rising e commerce activity and commercial fleet electrification are further pushing this segment ahead.

By Propulsion Type

Internal combustion engine vehicles accounted for the largest market share in 2025, around 54% of total revenue due to the huge existing vehicle fleet and continued safety technology integration across conventional platform types. It is expected to grow steadily at about 8.9% as intelligent safety features and connected mobility technologies keep getting upgraded.

Electric vehicles are expected to be the fastest grower over the forecast period, at roughly 13.1% CAGR, because investment in electric mobility infrastructure is increasing and demand for autonomous driving capabilities keeps rising. Automakers are also embedding advanced driver assistance systems into EV platforms to boost safety, improve connectivity and raise driving efficiency.

Regional Insights

Germany

Germany accounted for approximately 31% of the market in 2025, representing nearly USD 11.0 billion in market revenue, driven by strong automotive manufacturing infrastructure, rising electric vehicle production and increasing integration of intelligent safety technologies across premium vehicle platforms. Strong demand from Munich, Stuttgart and Wolfsburg continues to support market growth, particularly across passenger vehicles and connected mobility applications. Government backed automotive innovation programs and vehicle safety regulations supported by the European Commission are further accelerating investments in autonomous driving systems and intelligent mobility technologies.

The United Kingdom

The United Kingdom accounted for approximately 18% of the market in 2025, reaching nearly USD 6.4 billion in market value due to increasing investments in connected mobility infrastructure, intelligent transportation systems and electric vehicle development initiatives. Rising adoption across passenger vehicles, commercial fleets and urban mobility platforms is driving consistent demand for advanced driver assistance technologies. London, Birmingham, and Manchester continue to witness increasing deployment of connected vehicle systems supported by rising consumer preference for technologically advanced and safety integrated automobiles. The market is projected to expand at approximately 10.2% during the forecast period.

France

France contributed approximately 17% of the market in 2025, accounting for nearly USD 6.0 billion in revenue, supported by increasing investments in automotive electrification, smart transportation infrastructure and advanced vehicle safety technologies. Paris, Lyon and Toulouse continue to emerge as important automotive innovation hubs due to rising adoption of connected driving systems and intelligent mobility solutions. Government supported sustainable transportation initiatives and stricter automotive safety standards are further encouraging integration of driver assistance technologies across passenger and commercial vehicles. France is anticipated to register growth of approximately 10.4% during the forecast period.

Rest of Europe

The Rest of Europe segment accounted for approximately 29% of the market in 2025, representing nearly USD 10.3 billion in market value, supported by increasing automotive modernization projects and rising penetration of connected vehicle technologies across countries including Italy, Spain, the Netherlands and Sweden. Growing investments in electric mobility infrastructure, intelligent transportation systems and road safety enhancement programs continue to support long term market expansion across the region. The remaining demand is driven by increasing integration of autonomous safety technologies and expanding adoption of advanced mobility platforms across emerging automotive markets in Europe.

Competitive Landscape / Company Insights

The market is highly competitive with the presence of global automotive technology providers and regional manufacturers focusing on intelligent safety innovation, software integration and geographic expansion. Companies are increasingly investing in research and development, sensor technologies and connected mobility capabilities to strengthen their market position. Vehicle safety regulations and autonomous mobility initiatives supported by the European Commission and regional transportation authorities are further encouraging investments in advanced driver assistance technologies, electric mobility integration and intelligent automotive platforms across Europe.

Mini Profiles

Aptiv PLC focuses on advanced driver assistance technologies, connected mobility systems, and autonomous driving solutions, supported by strong global distribution capabilities, technological expertise, and long-term automotive manufacturing partnerships.

Autoliv Inc. operates in premium automotive safety segments, emphasizing intelligent restraint systems, collision mitigation technologies, and high-performance vehicle protection solutions for global automotive manufacturers.

Continental AG leverages extensive research capabilities, strategic automotive partnerships, and advanced software integration technologies to strengthen its market presence within connected mobility and intelligent safety systems.

Denso Corporation focuses on sensor technologies, vehicle electronics, and intelligent mobility platforms, supported by strong manufacturing efficiency, advanced engineering capabilities, and expanding automotive technology investments.

Infineon Technologies AG emphasizes automotive semiconductor solutions and intelligent sensor technologies, supported by strong innovation capabilities, digital mobility expertise, and increasing investments in autonomous driving infrastructure.

Key Players

- Aptiv PLC

- Autoliv Inc.

- Continental AG

- Denso Corporation

- Infineon Technologies AG

- Magna International Inc.

- Mobileye Global Inc.

- Robert Bosch GmbH

- Valeo SA

- ZF Friedrichshafen AG

Recent Developments

In January 2025, Magna International Inc. expanded its advanced driver assistance engineering operations across Europe to support increasing demand for autonomous driving technologies. The company also strengthened collaborations with automotive manufacturers for next generation sensor integration and intelligent mobility platforms.

In March 2025, Mobileye Global Inc. introduced upgraded surround sensing and autonomous driving software solutions for European automotive manufacturers. The company further expanded partnerships focused on connected vehicle safety technologies and intelligent transportation systems.

In June 2025, Robert Bosch GmbH increased investments in AI enabled driver assistance technologies and automotive semiconductor production capabilities across Europe. The company additionally focused on strengthening radar sensor development for intelligent vehicle safety applications.

In September 2025, Valeo SA expanded its LiDAR technology portfolio for autonomous mobility applications within passenger and commercial vehicle segments. The company also accelerated development of software defined vehicle solutions and connected driving systems across European automotive markets.

In February 2026, ZF Friedrichshafen AG introduced upgraded intelligent braking and lane assistance technologies targeting next generation electric vehicles. The company further strengthened research investments related to autonomous mobility platforms and advanced vehicle safety integration systems.

Europe ADAS Market Coverage

System Type Insight and Forecast 2026 - 2035

- Adaptive Cruise Control

- Blind Spot Detection

- Autonomous Emergency Braking

- Lane Departure Warning System

- Parking Assistance

- Forward Collision Warning

- Driver Monitoring System

- Traffic Sign Recognition

Sensor Type Insight and Forecast 2026 - 2035

- Radar Sensors

- LiDAR Sensors

- Ultrasonic Sensors

- Image Sensors

- Infrared Sensors

Vehicle Type Insight and Forecast 2026 - 2035

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

Propulsion Type Insight and Forecast 2026 - 2035

- Internal Combustion Engine Vehicles

- Electric Vehicles

- Hybrid Vehicles

Region Insight and Forecast 2026 - 2035

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

Europe ADAS Market by Region

- Germany

- By System Type

- By Sensor Type

- By Vehicle Type

- By Propulsion Type

- By Region

- U.K.

- By System Type

- By Sensor Type

- By Vehicle Type

- By Propulsion Type

- By Region

- France

- By System Type

- By Sensor Type

- By Vehicle Type

- By Propulsion Type

- By Region

- Italy

- By System Type

- By Sensor Type

- By Vehicle Type

- By Propulsion Type

- By Region

- Spain

- By System Type

- By Sensor Type

- By Vehicle Type

- By Propulsion Type

- By Region

- Russia

- By System Type

- By Sensor Type

- By Vehicle Type

- By Propulsion Type

- By Region

- Rest of Europe

- By System Type

- By Sensor Type

- By Vehicle Type

- By Propulsion Type

- By Region

Table of Contents for Europe ADAS Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

System Type

1.2.2. By

Sensor Type

1.2.3. By

Vehicle Type

1.2.4. By

Propulsion Type

1.2.5. By

Region

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Europe Market Estimate and Forecast

4.1. Europe Market Overview

4.2. Europe Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By System Type

5.1.1. Adaptive Cruise Control

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Blind Spot Detection

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Autonomous Emergency Braking

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Lane Departure Warning System

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Parking Assistance

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.1.6. Forward Collision Warning

5.1.6.1. Market Definition

5.1.6.2. Market Estimation and Forecast to 2035

5.1.7. Driver Monitoring System

5.1.7.1. Market Definition

5.1.7.2. Market Estimation and Forecast to 2035

5.1.8. Traffic Sign Recognition

5.1.8.1. Market Definition

5.1.8.2. Market Estimation and Forecast to 2035

5.2. By Sensor Type

5.2.1. Radar Sensors

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. LiDAR Sensors

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Ultrasonic Sensors

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Image Sensors

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. Infrared Sensors

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.3. By Vehicle Type

5.3.1. Passenger Cars

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Light Commercial Vehicles

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Heavy Commercial Vehicles

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.4. By Propulsion Type

5.4.1. Internal Combustion Engine Vehicles

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Electric Vehicles

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Hybrid Vehicles

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.5. By Region

5.5.1. Germany

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. United Kingdom

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. France

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Italy

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

5.5.5. Rest of Europe

5.5.5.1. Market Definition

5.5.5.2. Market Estimation and Forecast to 2035

6. Germany Market Estimate and Forecast

6.1. By

System Type

6.2. By

Sensor Type

6.3. By

Vehicle Type

6.4. By

Propulsion Type

6.5. By

Region

7. U.K. Market Estimate and Forecast

7.1. By

System Type

7.2. By

Sensor Type

7.3. By

Vehicle Type

7.4. By

Propulsion Type

7.5. By

Region

8. France Market Estimate and Forecast

8.1. By

System Type

8.2. By

Sensor Type

8.3. By

Vehicle Type

8.4. By

Propulsion Type

8.5. By

Region

9. Italy Market Estimate and Forecast

9.1. By

System Type

9.2. By

Sensor Type

9.3. By

Vehicle Type

9.4. By

Propulsion Type

9.5. By

Region

10. Spain Market Estimate and Forecast

10.1. By

System Type

10.2. By

Sensor Type

10.3. By

Vehicle Type

10.4. By

Propulsion Type

10.5. By

Region

11. Russia Market Estimate and Forecast

11.1. By

System Type

11.2. By

Sensor Type

11.3. By

Vehicle Type

11.4. By

Propulsion Type

11.5. By

Region

12. Rest of Europe Market Estimate and Forecast

12.1. By

System Type

12.2. By

Sensor Type

12.3. By

Vehicle Type

12.4. By

Propulsion Type

12.5. By

Region

13. Company Profiles

13.1.

Aptiv PLC

13.1.1.

Snapshot

13.1.2.

Overview

13.1.3.

Offerings

13.1.4.

Financial

Insight

13.1.5.

Recent

Developments

13.2.

Autoliv Inc.

13.2.1.

Snapshot

13.2.2.

Overview

13.2.3.

Offerings

13.2.4.

Financial

Insight

13.2.5.

Recent

Developments

13.3.

Continental AG

13.3.1.

Snapshot

13.3.2.

Overview

13.3.3.

Offerings

13.3.4.

Financial

Insight

13.3.5.

Recent

Developments

13.4.

Denso Corporation

13.4.1.

Snapshot

13.4.2.

Overview

13.4.3.

Offerings

13.4.4.

Financial

Insight

13.4.5.

Recent

Developments

13.5.

Infineon Technologies AG

13.5.1.

Snapshot

13.5.2.

Overview

13.5.3.

Offerings

13.5.4.

Financial

Insight

13.5.5.

Recent

Developments

13.6.

Magna International Inc.

13.6.1.

Snapshot

13.6.2.

Overview

13.6.3.

Offerings

13.6.4.

Financial

Insight

13.6.5.

Recent

Developments

13.7.

Mobileye Global Inc.

13.7.1.

Snapshot

13.7.2.

Overview

13.7.3.

Offerings

13.7.4.

Financial

Insight

13.7.5.

Recent

Developments

13.8.

Robert Bosch GmbH

13.8.1.

Snapshot

13.8.2.

Overview

13.8.3.

Offerings

13.8.4.

Financial

Insight

13.8.5.

Recent

Developments

13.9.

Valeo SA

13.9.1.

Snapshot

13.9.2.

Overview

13.9.3.

Offerings

13.9.4.

Financial

Insight

13.9.5.

Recent

Developments

13.10.

ZF Friedrichshafen AG

13.10.1.

Snapshot

13.10.2.

Overview

13.10.3.

Offerings

13.10.4.

Financial

Insight

13.10.5.

Recent

Developments

14. Appendix

14.1. Exchange Rates

14.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Europe ADAS Market