Europe Light Electric Charging Station Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Product Type (Hybrid Electric Vehicles (HEVs), Plug-in Hybrid Electric Vehicles (PHEVs), Battery Electric Vehicles (BEVs)), by Voltage Type (24V, 36V, 48V, 60V, 72V), by Application (Personal mobility / personal use, Commercial applications, Sports, Shared mobility solutions), by Battery Type (Lithium cobalt batteries, Lithium-ion polymer batteries, Nickel metal hydride batteries)

| Status : Published | Published On : Mar, 2026 | Report Code : VRSME9201 | Industry : Semiconductor & Electronics | Available Format :

|

Page : 140 |

Europe Light Electric Charging Station Market Overview

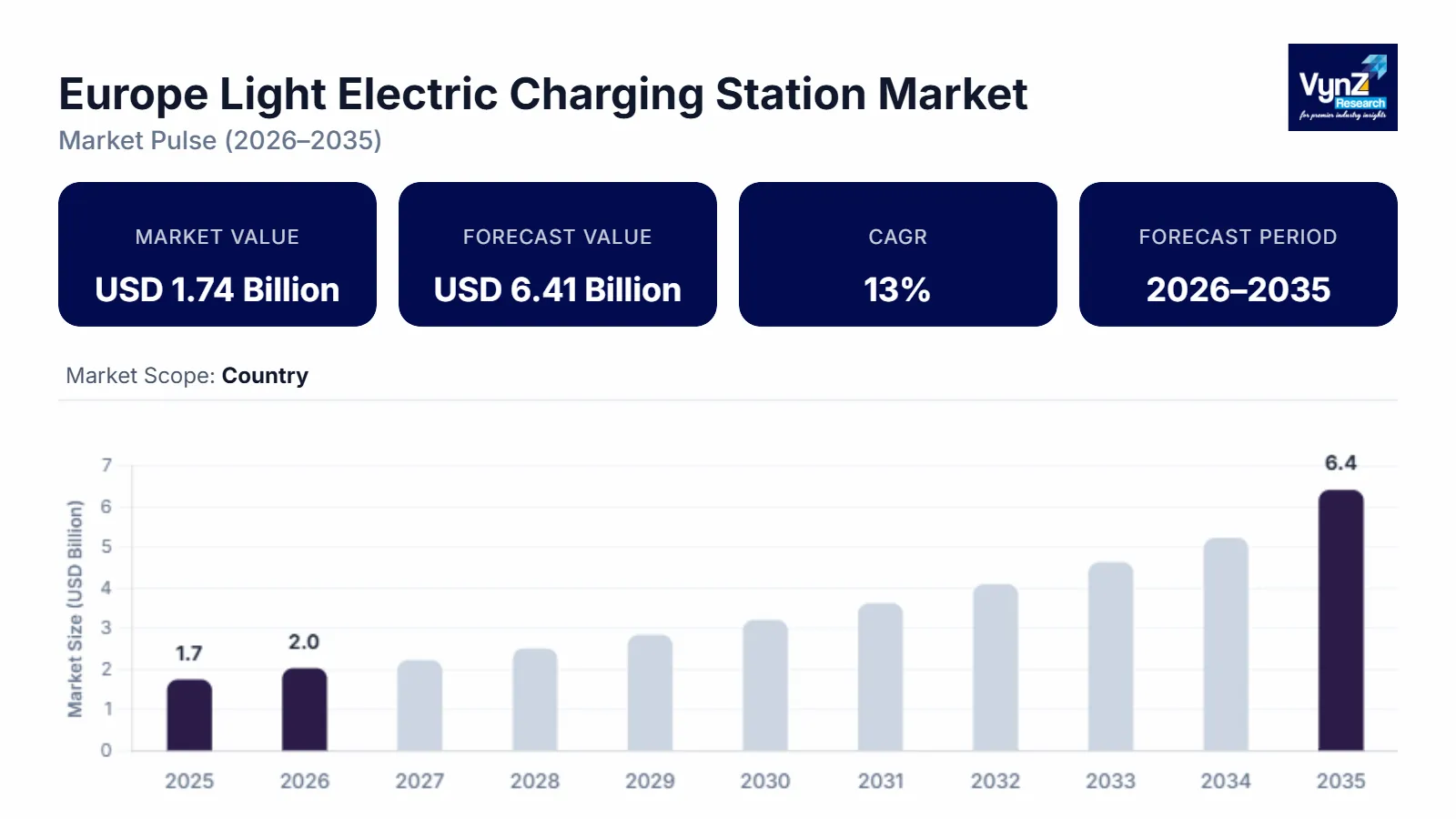

The Europe light electric charging station market which was valued at approximately USD 1.74 billion in 2025 and is estimated to rise further up to almost USD 2.02 billion in 2026, is projected to reach around USD 6.41 billion in 2035, expanding at a CAGR of about 13% during the forecast period 2026 to 2035.

Electric mobility adoption in urban transportation systems leads to a gradual market expansion which creates new opportunities for market development. The market experiences growth because European economies are installing micromobility charging stations and increasing their electric bicycle and scooter fleets while backing low emission transport solutions through strong policy support. The sector experiences growth because regulatory frameworks create incentives for both sustainable mobility practices and the electrification of short distance transport services.

Public charging infrastructure investments are increasing according to reports from the European Commission and the International Energy Agency which document their role in building electric mobility ecosystems. Government backed initiatives that support the development of zero emission mobility corridors and urban charging networks are creating positive effects for the industry. The rising demand for shared mobility services and last mile delivery solutions is driving the installation of charging stations in major urban markets throughout Germany, France, and the Netherlands because public investment and municipal sustainability programs are accelerating infrastructure development.

Europe Light Electric Charging Station Market Dynamics

Market Trends

The market experiences substantial changes because cities now establish charging stations and integrate micromobility systems into their transportation networks. Public charging solutions for electric bicycles and electric scooters experience rapid growth as the main industry trend because people now prefer sustainable transportation options that help with efficient urban mobility and low emission travel. European Union mobility frameworks now recommend municipalities to build compact charging networks which enable electrified transport corridors and smart city systems to operate shared micromobility services.

Digital mobility platforms and grid optimization systems together with standard regulatory frameworks verify the emerging trend which combines smart charging technologies with connected infrastructure systems. The European Commission together with the International Energy Agency published reports which reveal that urban charging points now use intelligent energy management systems for efficient load balancing and optimal electricity distribution.

Growth Drivers

The market expands due to increasing light electric mobility solution usage across European cities which creates permanent demand for charging stations in residential areas and public transport stations and commercial locations. Industry expansion receives further momentum from increasing investments in sustainable urban mobility infrastructure which receive support from national climate transition programs and European Union transport decarbonization strategies.

Regulatory frameworks that promote electric mobility receive active support which results in improved adoption rates. The European Commission’s Sustainable and Smart Mobility Strategy requires extensive electric charging infrastructure implementation to help achieve both emission reduction objectives and better urban air quality results. The forecast period will see continuous demand for charging stations which handle electric scooters and electric bicycles and light electric delivery vehicles because transportation authorities prefer energy efficient systems that decrease carbon emissions.

Market Restraints / Challenges

The market possesses good growth potential but the market encounters multiple obstacles which restrict market development in smaller cities and emerging regional territories. The public charging infrastructure installation process faces multiple obstacles because organizations need to deal with both grid connections and public charging equipment installation costs and the whole permitting process. The European Environment Agency reports that European cities experience charging access problems because their charging infrastructure distribution remains uneven.

Charging network operators and equipment suppliers must deal with operational difficulties because their systems depend heavily on energy infrastructure. Micromobility corridors which experience rapid growth will face both higher costs and delays in installation because the area needs to depend on grid capacity enhancements together with renewable energy sources. Government assessments about urban electrification strategies conclude that market performance during infrastructure changes will depend on energy demand management and grid modernization as critical requirements for large charging station rollouts.

Market Opportunities

The market presents significant opportunities in expanding integrated micromobility charging ecosystems, particularly driven by urban sustainability initiatives and growing demand for shared electric transport services. Companies that provide modular charging infrastructure which uses minimal space and enables expansion will see heightened demand from shared mobility operators and logistics firms and municipal transport authorities who operate electric vehicle fleets.

Smart grid technology combined with charging stations that use renewable energy to generate power offers another major market opportunity. The European Green Deal and regional clean mobility programs which receive government support will lead to funding for intelligent energy infrastructure development which enables electric mobility growth. European cities will benefit from digital energy management platforms together with connected charging systems and automated monitoring systems which improve operational performance and provide better accessibility for users while establishing long term infrastructure development paths.

Europe Light Electric Charging Station Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 1.74 Billion |

|

Revenue Forecast in 2035 |

USD 6.41 Billion |

|

Growth Rate |

13% |

|

Segments Covered in the Report |

By Product, By Voltage, By Application and By Battery |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

Western Europe, Northern Europe and Southern Europe |

|

Key Companies |

BMW, Ford Motor Company, Groupe Renault, Mercedes Benz, Peugeot S.A., Stellantis, Tesla, Toyota Motor Corporation, Volkswagen AG |

|

Customization |

Available upon request |

Europe Light Electric Charging Station Market Segmentation

By Product Type

The market in 2025 recorded its highest revenue for battery electric vehicles which generated about 54% of all segment earnings. The current situation shows that electric transportation solutions are becoming more common because of regulatory frameworks which support zero emission transportation systems. The European Union climate and mobility regulations expect that all short distance transportation systems need to become fully electric which will drive users to choose battery electric vehicles as their main means of transportation.

The market will experience its strongest growth for plug in hybrid electric vehicles during the forecast period which will see an annual growth rate of 13.6% between 2026 and 2035. The transitional mobility strategies which European transportation networks adopted create growth opportunities because hybrid vehicles can function alongside fully electric vehicle fleets. The vehicles need available charging stations which enable their systems to achieve maximum energy output and minimal fuel usage.

By Voltage Type

The 48V voltage category market dominance in 2025 reached a total of 31% which resulted in the largest market share for this voltage category. The segment demonstrates power efficiency and compatibility with light electric vehicles which includes electric scooters and bicycles that people use for their daily transportation needs. The European municipal authorities back urban transport electrification methods through their support of mid voltage systems which provide dependable charging capabilities while preserving grid operational efficiency. Shared micromobility fleets are expanding their operations which creates increased demand for charging stations that work with this voltage system.

The 72V segment will achieve its fastest growth during the forecast period between 2026 and 2035 because it requires a 14.1% annual growth rate. Higher voltage systems are increasingly deployed for commercial micromobility fleets and cargo oriented electric vehicles requiring faster charging cycles and improved energy efficiency. The implementation of electric cargo bicycles and delivery scooters by logistics operators drives up the need for high voltage charging stations which can handle the heavy operational demands of urban logistics systems.

By Application

The market in 2025 saw personal mobility applications as its primary revenue source which generated approximately 46% of total segment earnings. The increasing usage of electric bicycles and scooters for daily commuting needs in European cities creates a steady requirement for public charging stations to meet charging needs. The urban mobility programs which seek to decrease traffic congestion and carbon emissions, through their support of micromobility, create a need for charging station installation at residential areas and public transit stations and bicycle parking locations.

Shared mobility services will grow at the highest rate during the forecast period, which will see an annual growth rate of 14.4%. The widespread growth of electric scooter sharing and bicycle sharing services in major cities has prompted service operators to build extensive networks of charging stations. The shared micromobility fleet and its charging infrastructure will expand because of municipal mobility policies which promote multimodal transport systems.

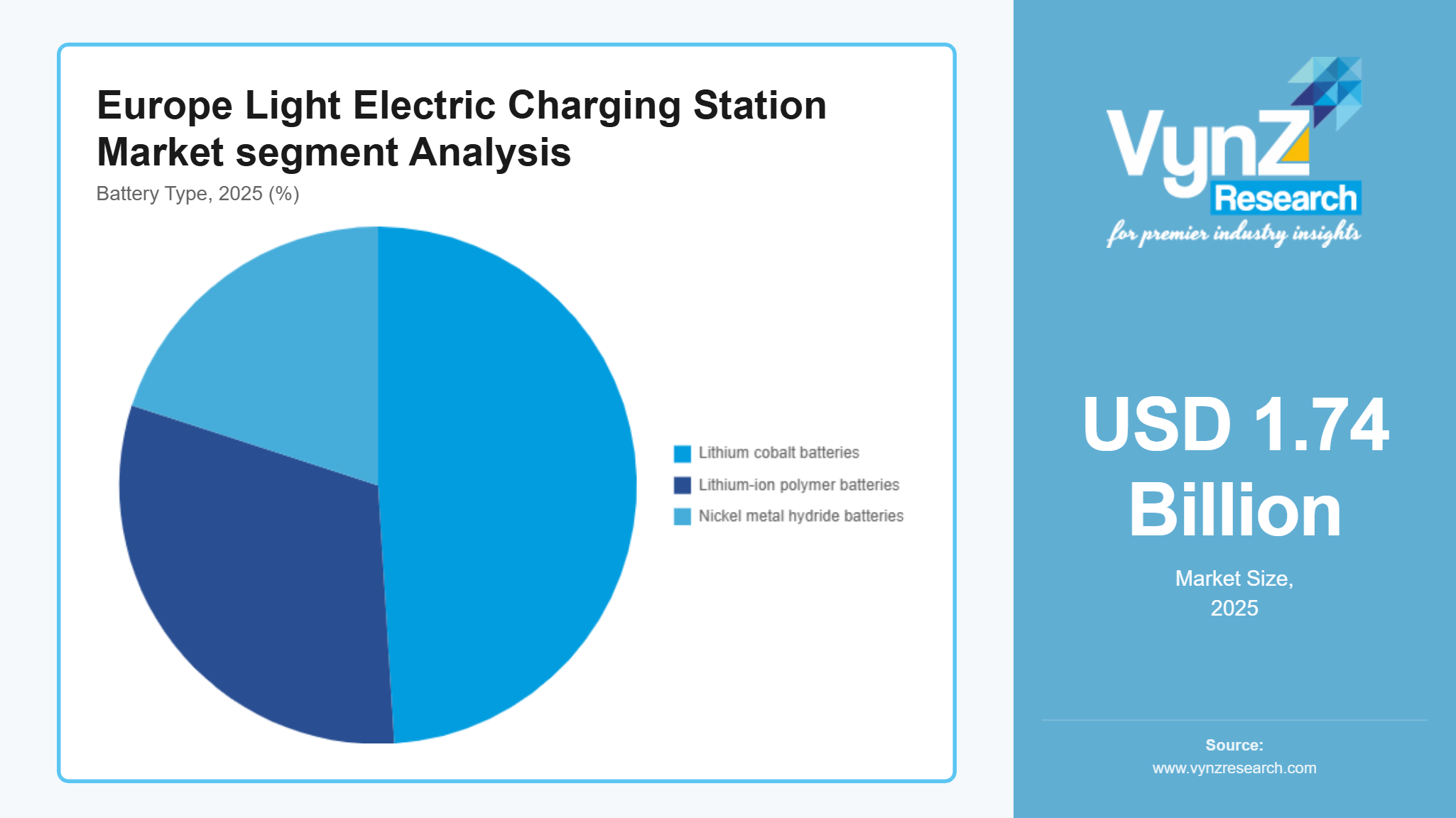

By Battery

The market in 2025 saw lithium-ion polymer batteries achieve the highest market share by generating 49% of total segment revenue. The battery technology enjoys widespread use because it delivers high energy density, lightweight design and faster charging speed than traditional batteries. The advantages of lithium-ion polymer batteries make them suitable for electric scooters and bicycles which operate in urban environments. The expansion of charging infrastructure which supports these batteries has become a main focus of municipal mobility planning efforts across Europe.

The market for lithium cobalt batteries will experience the fastest growth period which will see a 13.9% annual growth rate from 2026 to 2035. The integration of advanced battery chemical technologies and better energy storage solutions into high performance electric mobility systems has become a major trend. The vehicle manufacturers who develop improved battery performance and charging efficiency will create a higher demand for charging stations which can serve both commercial and shared mobility systems.

Regional Insights

Western Europe

The Western Europe held about 38% market share of the market in 2025 because electric vehicles gained popularity together with established urban charging systems. Germany, France and the Netherlands maintain their role as top countries for infrastructure development because their sustainability policies and their spending on low emission transport systems create a sustainable development framework. Berlin, Paris and Amsterdam have emerging micromobility services that create demand for special electric bicycle and scooter charging stations.

Clean transportation programs from the government enhance market performance across the different areas. European Commission Sustainable and Smart Mobility Strategy created policy frameworks which dedicated their focus to developing urban transport electrification and public charging network expansion. The International Energy Agency reports that Western Europe functions as a main center for electric mobility innovation together with infrastructure investments which lead cities to develop charging stations at public transportation and urban mobility hubs.

Northern Europe

Northern Europe represents approximately 23% of the market in 2025 and continues to witness steady expansion due to strong environmental policies and high adoption of electric mobility solutions. Sweden, Denmark and Norway established strict carbon neutrality goals which accelerated the electrification of their transportation systems that include micromobility transport methods. Urban centers including Stockholm, Copenhagen and Oslo are deploying charging infrastructure to support electric scooter sharing programs and bicycle mobility networks.

The development of infrastructure projects receives major support from climate programs which governments have created. Market growth throughout the region receives support from national mobility programs which promote zero emission transportation together with investments in renewable energy charging systems. European energy authorities and environmental agencies report that Northern European countries have established themselves as the most advanced markets for electric mobility and charging station deployment.

Southern Europe

The market share of Southern Europe reached approximately 17% in 2025 because investments in sustainable transport and urban mobility improvements increased. Spain, Italy and Portugal are expanding their micromobility infrastructure to all major urban centers which include Madrid, Barcelona and Milan. The region experiences growth because tourists need urban mobility services and more people are using electric scooters and bicycles for short trips.

Municipal transportation networks receive new charging infrastructure because government programs foster green transport solutions and emission reduction targets. The European Commission supports national recovery programs and urban sustainability policies which encourage cities to build electric mobility infrastructure in public spaces and tourist pathways. Western Europe Northern Europe and Southern Europe share more than 78% of total market revenue while the rest of Europe and emerging urban markets outside this analysis section receive the remaining market share.

Competitive Landscape / Company Insights

The market shows a competitive market structure which ranges from moderate competition to high competition as international and domestic market players concentrate on developing new charging systems and establishing pricing frameworks and expanding their operational territories. The market position of companies depends on their smart charging technology and energy management system and integrated mobility platform investments. The European Commission's Sustainable and Smart Mobility Strategy and International Energy Agency infrastructure programs which support electric mobility charging network development across urban transport systems serve as governmental backing for adoption.

Mini Profiles

BMW focuses on advanced electric mobility solutions and charging ecosystem integration, supported by strong brand recognition, extensive European distribution networks, and continuous investment in electrification technologies for sustainable transportation systems.

Ford Motor Company operates in mass and commercial electric mobility segments, emphasizing performance, affordability, and scalable vehicle platforms, supported by expanding electrification programs and partnerships strengthening charging infrastructure deployment.

Groupe Renault leverages regional manufacturing strength and strategic alliances to expand electric mobility presence, offering compact electric vehicles and mobility platforms supported by efficient supply chains and strong European market penetration.

Mercedes Benz focuses on premium electric mobility technologies and integrated charging services, supported by high brand value, advanced vehicle engineering capabilities, and continued investment in luxury electric mobility innovation.

Tesla operates in premium electric mobility and charging infrastructure segments, emphasizing high performance electric vehicles and proprietary charging networks supported by advanced battery technology and strong digital ecosystem integration.

Key Players

- BMW

- Ford Motor Company

- Groupe Renault

- Mercedes Benz

- Peugeot S.A.

- Stellantis

- Tesla

- Toyota Motor Corporation

- Volkswagen AG

Recent Developments

In March 2026, Volkswagen AG and XPeng Inc. have started mass production of their first jointly developed electric vehicle (EV) in China, deepening a partnership that highlights how global automakers are increasingly turning to Chinese EV makers for technology as competition in the world’s largest car market intensifies.

In December 2025, BBVA and Stellantis have been authorized by the Central Bank of Argentina and the Secretariat of Industry and Commerce to take joint control of FCA Compañía Financiera, a firm until now wholly owned by Stellantis and specializing in auto financing for the brands owned by the auto giant.

In June 2025, Mercedes-Benz and 24-Autohöfe, the German truck stop chain have collaborated to expand electric vehicle (EV) charging infrastructure along Germany’s highways. The partnership starts with the launch of the first Mercedes-Benz High-Power Charging Hub at the 24-Autohof location in Wernberg-Köblitz situated at the Oberpfälzer Wald highway interchange. This marks the first of more than ten such premium charging parks planned for the 24-Autohöfe network.

Europe Light Electric Charging Station Market Coverage

Product Type Insight and Forecast 2026 - 2035

- Hybrid Electric Vehicles (HEVs)

- Plug-in Hybrid Electric Vehicles (PHEVs)

- Battery Electric Vehicles (BEVs)

Voltage Type Insight and Forecast 2026 - 2035

- 24V

- 36V

- 48V

- 60V

- 72V

Application Insight and Forecast 2026 - 2035

- Personal mobility / personal use

- Commercial applications

- Sports

- Shared mobility solutions

Battery Type Insight and Forecast 2026 - 2035

- Lithium cobalt batteries

- Lithium-ion polymer batteries

- Nickel metal hydride batteries

Europe Light Electric Charging Station Market by Region

- Germany

- By Product Type

- By Voltage Type

- By Application

- By Battery Type

- U.K.

- By Product Type

- By Voltage Type

- By Application

- By Battery Type

- France

- By Product Type

- By Voltage Type

- By Application

- By Battery Type

- Italy

- By Product Type

- By Voltage Type

- By Application

- By Battery Type

- Spain

- By Product Type

- By Voltage Type

- By Application

- By Battery Type

- Russia

- By Product Type

- By Voltage Type

- By Application

- By Battery Type

- Rest of Europe

- By Product Type

- By Voltage Type

- By Application

- By Battery Type

Table of Contents for Europe Light Electric Charging Station Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Product Type

1.2.2. By

Voltage Type

1.2.3. By

Application

1.2.4. By

Battery Type

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Europe Market Estimate and Forecast

4.1. Europe Market Overview

4.2. Europe Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Product Type

5.1.1. Hybrid Electric Vehicles (HEVs)

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Plug-in Hybrid Electric Vehicles (PHEVs)

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Battery Electric Vehicles (BEVs)

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Voltage Type

5.2.1. 24V

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. 36V

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. 48V

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. 60V

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. 72V

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.3. By Application

5.3.1. Personal mobility / personal use

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Commercial applications

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Sports

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Shared mobility solutions

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.4. By Battery Type

5.4.1. Lithium cobalt batteries

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Lithium-ion polymer batteries

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Nickel metal hydride batteries

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

6. Germany Market Estimate and Forecast

6.1. By

Product Type

6.2. By

Voltage Type

6.3. By

Application

6.4. By

Battery Type

7. U.K. Market Estimate and Forecast

7.1. By

Product Type

7.2. By

Voltage Type

7.3. By

Application

7.4. By

Battery Type

8. France Market Estimate and Forecast

8.1. By

Product Type

8.2. By

Voltage Type

8.3. By

Application

8.4. By

Battery Type

9. Italy Market Estimate and Forecast

9.1. By

Product Type

9.2. By

Voltage Type

9.3. By

Application

9.4. By

Battery Type

10. Spain Market Estimate and Forecast

10.1. By

Product Type

10.2. By

Voltage Type

10.3. By

Application

10.4. By

Battery Type

11. Russia Market Estimate and Forecast

11.1. By

Product Type

11.2. By

Voltage Type

11.3. By

Application

11.4. By

Battery Type

12. Rest of Europe Market Estimate and Forecast

12.1. By

Product Type

12.2. By

Voltage Type

12.3. By

Application

12.4. By

Battery Type

13. Company Profiles

13.1.

BMW

13.1.1.

Snapshot

13.1.2.

Overview

13.1.3.

Offerings

13.1.4.

Financial

Insight

13.1.5.

Recent

Developments

13.2.

Ford Motor Company

13.2.1.

Snapshot

13.2.2.

Overview

13.2.3.

Offerings

13.2.4.

Financial

Insight

13.2.5.

Recent

Developments

13.3.

Groupe Renault

13.3.1.

Snapshot

13.3.2.

Overview

13.3.3.

Offerings

13.3.4.

Financial

Insight

13.3.5.

Recent

Developments

13.4.

Mercedes Benz

13.4.1.

Snapshot

13.4.2.

Overview

13.4.3.

Offerings

13.4.4.

Financial

Insight

13.4.5.

Recent

Developments

13.5.

Peugeot S.A.

13.5.1.

Snapshot

13.5.2.

Overview

13.5.3.

Offerings

13.5.4.

Financial

Insight

13.5.5.

Recent

Developments

13.6.

Stellantis

13.6.1.

Snapshot

13.6.2.

Overview

13.6.3.

Offerings

13.6.4.

Financial

Insight

13.6.5.

Recent

Developments

13.7.

Tesla

13.7.1.

Snapshot

13.7.2.

Overview

13.7.3.

Offerings

13.7.4.

Financial

Insight

13.7.5.

Recent

Developments

13.8.

Toyota Motor Corporation

13.8.1.

Snapshot

13.8.2.

Overview

13.8.3.

Offerings

13.8.4.

Financial

Insight

13.8.5.

Recent

Developments

13.9.

Volkswagen AG

13.9.1.

Snapshot

13.9.2.

Overview

13.9.3.

Offerings

13.9.4.

Financial

Insight

13.9.5.

Recent

Developments

14. Appendix

14.1. Exchange Rates

14.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Europe Light Electric Charging Station Market