Next-Generation Large-Scale Energy Storage System Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Technology (Lithium-Ion Battery Systems, Flow Battery Systems), by Storage Duration (Short Duration Storage, Long Duration Storage), by Deployment Type (Grid Connected Storage, Behind-the-Meter Storage), by End User (Utility Companies, Independent Power Producers & Commercial Energy Developers)

| Status : Published | Published On : Mar, 2026 | Report Code : VRSME9199 | Industry : Semiconductor & Electronics | Available Format :

|

Page : 178 |

Next-Generation Large-Scale Energy Storage System Market Overview

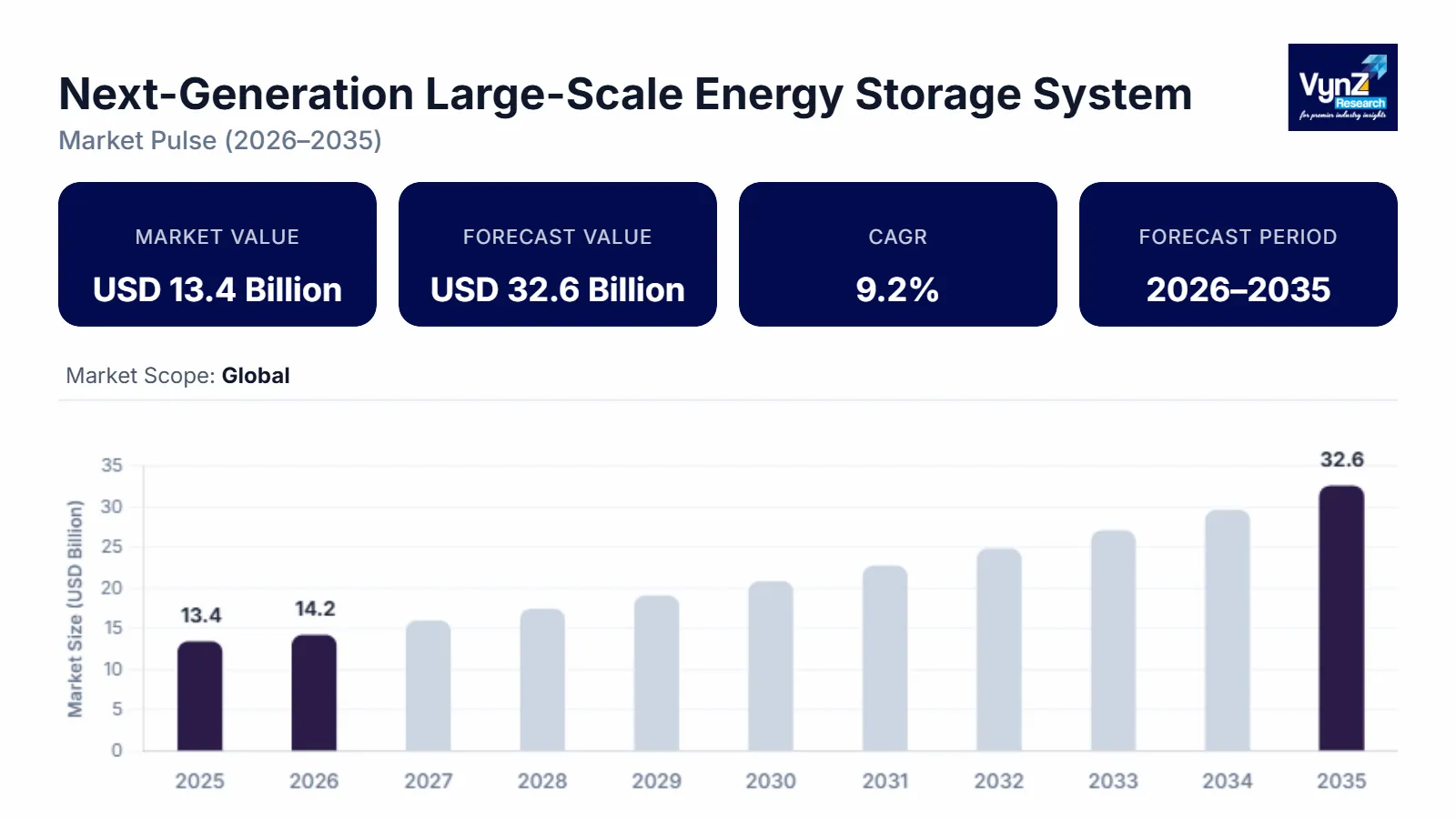

The global next-generation large-scale energy storage system market, which was valued at approximately USD 13.4 billion in 2025 and is estimated to reach around USD 14.2 billion in 2026, is projected to reach approximately USD 32.6 billion by 2035, expanding at a CAGR of about 9.2% during the forecast period from 2026 to 2035.

The market expansion is fueled by three factors which include growing renewable energy usage, increasing electricity consumption, and government-backed clean energy programs together with the rising use of advanced grid-scale storage technologies. Utilities together with independent power producers are making investments in lithium-ion and flow battery systems to achieve two goals which include maintaining grid stability and controlling solar and wind energy fluctuations while they dispatch power. National energy policies and programs from organizations such as the International Energy Agency and regional energy authorities are promoting infrastructure development together with research funding and large-scale storage project deployments throughout North America, Europe and Asia Pacific.

Next-Generation Large-Scale Energy Storage System Market Dynamics

Market Trends

The industry shows a movement toward advanced technologies which enable storage of electricity created by renewable energy and electrical distribution system modernization efforts. The International Energy Agency reports show that energy storage systems have become necessary to control the intermittent power output from solar and wind power sources. The market has seen a surge in demand for high-capacity lithium-ion battery systems and hybrid storage systems combined with digital energy management systems that enhance both grid reliability and operational performance. Energy developers together with utilities require automated monitoring systems, predictive analytics and integrated control platforms as their main technologies for performance enhancement in massive renewable energy projects across all main electricity markets.

The industry now shows increased interest in creating storage solutions which provide extended energy storage to manage peak electricity demand and maintain electrical grid operations. The U.S. Department of Energy developed policy frameworks require organizations to establish extensive storage capacities as a method to improve energy security while achieving their decarbonization objectives.

Growth Drivers

The sector shows strong growth capacity because both renewable energy production and electricity consumption in industrial and urban areas are increasing. International Renewable Energy Agency reports on energy transition progress show that electrical networks need large-scale storage systems to maintain stability while renewable power production continues to increase throughout the world. Advanced storage systems become essential when governments and utilities need to decrease renewable energy curtailment while enhancing their electrical grid operations.

Energy transition policies together with public investment programs function as key drivers which promote the development of next-generation storage solutions. The U.S. Department of Energy manages funding programs and grid modernization projects which finance both pilot studies and actual commercial operations. Utilities and independent power producers are now encouraged to build scalable storage systems which enable them to provide extended energy supply and operate more efficiently through these measures.

Market Restraints / Challenges

High capital costs create a significant obstacle for storage projects which need to handle large-scale storage requirements despite their strong market demand. Energy market entry becomes difficult for battery system technology, grid integration equipment and safety management systems because their associated infrastructure costs create financial obstacles. The International Energy Agency research study shows that project development in various regions experiences delay because both financing restrictions and revenue uncertainty in the market.

The next obstacle involves creating supply chain systems which protect access to essential minerals needed for advanced battery technology development. World Bank reports show that the rising consumption of lithium, cobalt and nickel will create market tensions which result in price swings. Storage developers face operational difficulties and expense variations because they depend on imported materials and need to use particular technologies.

Market Opportunities

The increasing need for long-duration storage systems which enable renewable energy integration together with national energy security requirements creates important business prospects. The International Renewable Energy Agency established energy transition roadmaps which show that storage capacity expansion functions as an essential requirement for organizations to reach their decarbonization targets and achieve better grid resilience.

Smart grid modernization together with digital energy management platforms create new business prospects. The U.S. Department of Energy executes intelligent grid infrastructure programs which promote the use of automated monitoring systems and predictive analytics tools. The implementation of these technologies will raise operational efficiency while creating lasting value for future energy storage systems.

Global Next-Generation Large-Scale Energy Storage System Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 13.4 Billion |

|

Revenue Forecast in 2035 |

USD 32.6 Billion |

|

Growth Rate |

9.2% |

|

Segments Covered in the Report |

Technology, Storage Duration, Deployment Type, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

ABB Ltd., BYD Company Limited, Contemporary Amperex Technology Co., Limited (CATL), Fluence Energy, Inc., Form Energy, Inc., LG Energy Solution Ltd., Panasonic Holdings Corporation, Samsung SDI Co., Ltd., Siemens Energy AG, Tesla, Inc |

|

Customization |

Available upon request |

Next-Generation Large-Scale Energy Storage System Market Segmentation

By Technology

The market in 2025 reached its highest level with lithium-ion battery systems which generated about 48% of total market revenue. Their dominance exists because they operate with high energy density and manufacturing systems which already exist and their technology achieves great success in renewable energy integration projects. The operational efficiency of lithium-based storage solutions together with decreasing battery costs makes them the preferred choice for utilities and grid operators who need to balance solar and wind power. The deployment of large-scale lithium battery installations receives support from national clean energy transition strategies which international energy agencies including the International Energy Agency support to help stabilize electricity grids and decrease the need for renewable energy curtailment.

The forecast period will see flow battery technologies achieve the fastest growth which will expand at a projected CAGR of 9.1%. The increasing demand for long duration storage solutions which can support extended discharge cycles and grid scale energy balancing drives market growth. Research programs supported by the government together with pilot projects which study alternative storage chemistries lead to vanadium and zinc-based flow battery systems becoming more widely adopted. Utilities show interest in these technologies because they want storage infrastructure which can scale up and deliver sustainable performance with longer operational life for renewable energy networks.

By Storage Duration

The market for energy storage systems reached its highest level in 2025 through short duration systems which generated almost 46% of total market revenue. The systems continue to receive widespread deployment for their ability to regulate frequency, stabilize grids and balance renewable energy resources during short cycles. Utilities and independent power producers maintain strong system adoption because the infrastructure requirements for their systems remain low while their systems need rapid implementation. The International Renewable Energy Agency and other institutions promote grid modernization strategies which show how short duration storage systems help power systems maintain operational reliability while managing renewable electricity generation fluctuations.

The market for long duration storage systems is projected to experience the highest growth rate which will achieve an estimated CAGR of 9.4% between the years 2026 and 2035. The increasing demand for electricity together with the rising need for renewable energy sources drives utilities to invest in storage technologies which can sustain their operations through prolonged discharge periods. The technologies of compressed air storage, thermal storage systems and advanced battery chemistries have gained momentum as governments back grid resilience and long-term energy security initiatives. The systems provide optimal energy dispatch flexibility which makes them vital components for power grids that operate mainly on renewable energy sources.

By Deployment Type

Grid connected energy storage systems held the largest share of the market in 2025, accounting for approximately 55% of segment revenue. The infrastructure investment growth which supports national grid development and renewable energy projects creates their dominant market position. Utilities and transmission operators build large storage systems to boost grid reliability while they handle peak power demand. The U.S. Department of Energy established policy frameworks which recognize grid connected storage solutions as essential elements for both power system resilience and effective renewable energy distribution.

The market will see behind the meter storage deployments grow faster with an estimated CAGR of 8.7% during the forecast period. The commercial and industrial energy users who adopt the technology show growth because they want to decrease their electricity expenses while enhancing their energy reliability. The manufacturing facilities and commercial complexes now need advanced storage solutions which help them manage power demand and maintain backup power functions because their business needs continue to rise in areas with fast industrial growth and high electricity consumption.

By End User

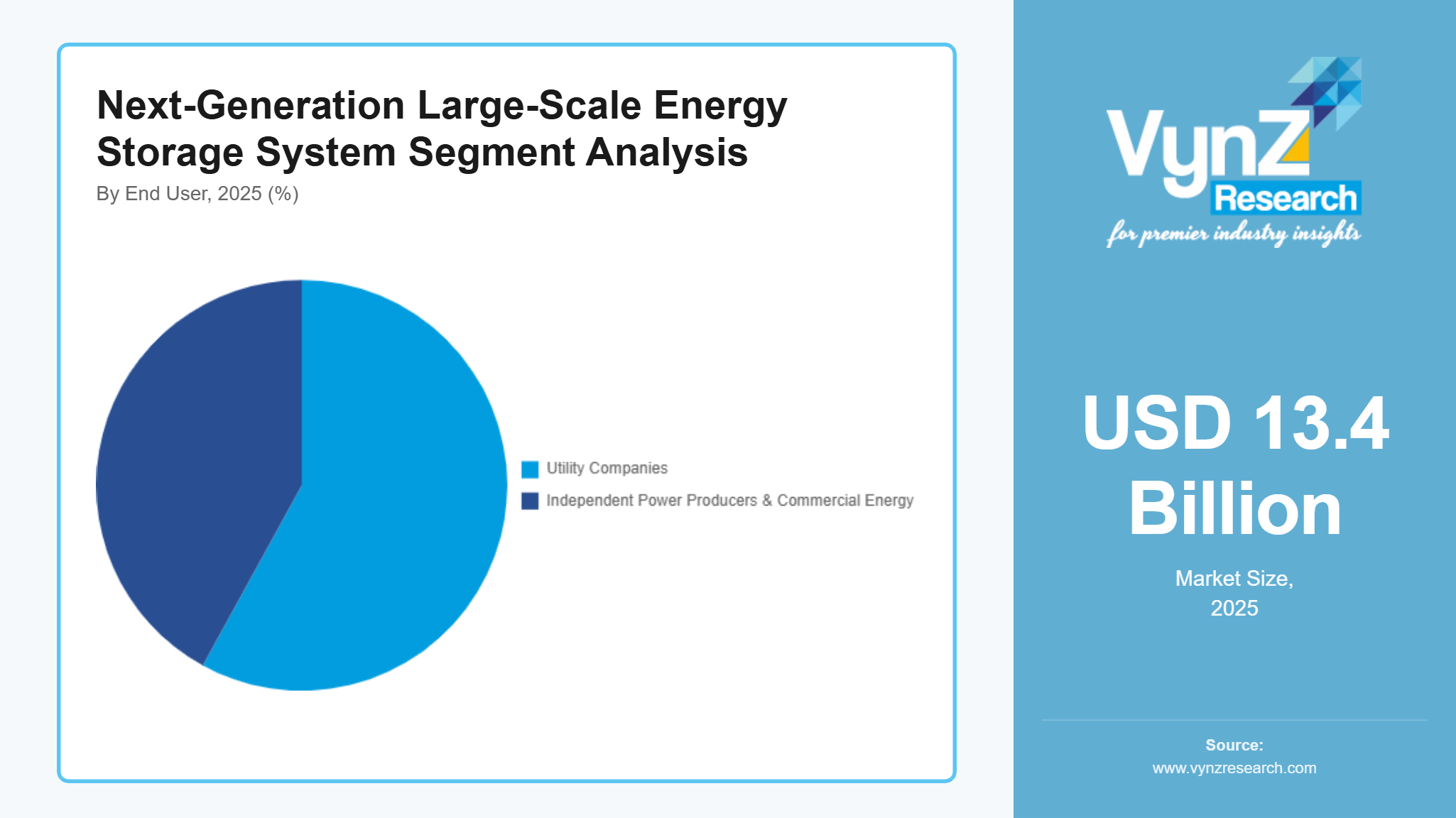

The market in 2025 reached its highest level with utility companies which generated about 58% of total market revenue. The company maintains its leadership position through its extensive investments in grid modernization projects and renewable energy integration initiatives. The utility sector uses large scale storage systems to enhance electricity network stability while handling peak load and improving energy security for their operations. The International Energy Agency published energy transition roadmaps which show how utilities need to expand their storage infrastructure to create decarbonized power systems.

The market for independent power producers and commercial energy developers will experience the fastest growth rate which will achieve an estimated CAGR of 9.2% between 2026 and 2035. The growing financial support for renewable power plants and hybrid energy projects encourages firms to adopt advanced storage systems which guarantee constant electricity delivery. The solar and wind installations which operate at large scale now use energy storage systems to better their dispatch reliability which boosts their total power generation efficiency to achieve market growth.

Regional Insights

North America

North America held nearly 30% of the market during 2025. The region experiences growth because it successfully implements renewable energy systems while having modern grid networks and making substantial financial investments to develop large storage systems. The three leading energy hubs of California, Texas and New York maintain their current operational pace by installing grid scale battery systems which work in combination with solar and wind energy projects. The combination of energy resilience policies and energy storage regulatory frameworks leads to increased demand for new storage systems within utility networks.

The government supports clean energy programs which lead to increased investment in large storage facilities. The U.S. Department of Energy implements strategic initiatives focus on modernizing the grid while integrating renewables and expanding battery storage capabilities. The initiatives enable power plants to implement advanced storage systems which enhance electricity stability and help achieve decarbonization goals.

Asia Pacific

Asia Pacific holds about 27% of the market in 2025 because of its industrial growth, increasing electricity needs and its extensive renewable energy investments. China, Japan, India and South Korea are making substantial investments to develop energy storage systems which will help their electricity grids maintain stability while supporting renewable energy adoption. Major cities like Beijing, Tokyo and Mumbai are now adopting grid-connected storage systems to meet rising electricity needs and maintain stable grid operations.

The region experiences rapid development of next generation storage technologies because of government policies which support renewable energy growth and energy security. The International Renewable Energy Agency established energy transition roadmaps which show that energy storage systems enable countries to implement extensive renewable energy integration while building stable electricity networks for their economies in Asia Pacific.

Europe

The market shows Europe having approximately 21% share in 2025. European Union countries achieve regional growth through their implementation of climate policies, their establishment of renewable energy goals and their grid modernization projects. Germany, the United Kingdom, France and Spain plan to increase their battery storage capacity so they can accommodate rising wind and solar energy production. The energy infrastructure initiatives that cities of Berlin, London and Paris optimize their systems through the integration of cutting-edge grid storage solutions.

The European Commission and other institutions have developed policy frameworks which enable energy storage system growth as part of their decarbonization initiatives. The market grows through regional investments in smart grid technology, renewable energy projects and energy resilience programs which motivate utilities to implement advanced storage systems.

Rest of the World

The market share of the rest of the world which includes Latin America, the Middle East and Africa stand at 22% for 2025. The two regions experience growth because electricity demand increases, renewable energy infrastructure investments rise and grid reliability improvements become more important. Brazil, United Arab Emirates and South Africa are starting to implement energy storage systems which will improve their power systems and enable renewable energy projects.

Global organizations like the World Bank fund energy development initiatives help emerging electricity markets attract infrastructure investments. The storage technology market will grow through two main drivers which include expanded renewable energy projects and upgraded national power distribution systems.

Competitive Landscape / Company Insights

The Next-Generation Large-Scale Energy Storage System market is moderately to highly competitive, with global and regional companies focusing on technology innovation, strategic partnerships, and geographic expansion to strengthen their industry position. Key players are investing in advanced battery chemistries, grid scale storage solutions, and digital energy management platforms to enhance system efficiency and reliability. Adoption is supported by clean energy transition initiatives promoted by the International Energy Agency and grid modernization programs implemented by the U.S. Department of Energy, encouraging companies to expand deployment capabilities and technological expertise.

Mini Profiles

ABB Ltd. focuses on advanced grid infrastructure and energy storage integration technologies, supported by strong global distribution networks, power automation expertise, and established partnerships with utilities implementing large scale renewable energy projects.

BYD Company Limited operates in mass and large-scale battery storage segments, emphasizing performance driven lithium battery technologies, supported by vertically integrated manufacturing capabilities and extensive deployment across renewable and utility storage applications.

Contemporary Amperex Technology Co., Limited (CATL) leverages large scale manufacturing and strategic partnerships with utilities and renewable developers to expand market presence, delivering advanced battery storage technologies with high efficiency and long operational lifecycle.

Fluence Energy, Inc. focuses on integrated grid scale battery storage platforms, supported by digital energy management software, strong project deployment capabilities, and partnerships with utilities seeking scalable renewable energy storage solutions.

Form Energy, Inc. operates in next generation long duration storage solutions, emphasizing innovative iron air battery technologies designed to support multi day energy storage requirements for renewable integration and resilient power systems.

Key Players

- ABB Ltd.

- BYD Company Limited

- Contemporary Amperex Technology Co., Limited (CATL)

- Fluence Energy, Inc.

- Form Energy, Inc.

- LG Energy Solution Ltd.

- Panasonic Holdings Corporation

- Samsung SDI Co., Ltd.

- Siemens Energy AG

- Tesla, Inc.

Recent Developments

In March 2026, Panasonic has launched a liquid cooling systems business for AI data centers. This business focus on cooling systems for high-performance computing & generative AI servers and development of high-capacity cooling units (1,200 kW+) which aligns with rising demand from data centers and cloud computing.

In March 2026, ABB Robotics Partners with NVIDIA to Deliver Industrial-Grade Physical AI at Scale. The collaboration focuses on combining ABB Robotics’ software programming, design and simulation suite, RobotStudio, with the physically accurate simulation power of NVIDIA Omniverse libraries to close technology's long-standing 'sim-to-real’ gap. Developers can simulate robots in digital twins and generate synthetic data to train their physical AI models, enabling businesses of all types and sizes to deploy AI-driven robotics for various industrial workflows.

In February 2026, Google has awarded Form Energy, Inc. a USD billion contract to provide its cutting-edge iron-air batteries for a Minnesota data center project. One of the biggest and longest-lasting battery installations in the world, this project entails the deployment of a massive energy storage system that can provide electricity constantly for up to 100 hours. Iron-air batteries are less expensive for widespread use since they are made of inexpensive materials like iron.

Global Next-Generation Large-Scale Energy Storage System Market Coverage

Technology Insight and Forecast 2026 - 2035

- Lithium-Ion Battery Systems

- Flow Battery Systems

Storage Duration Insight and Forecast 2026 - 2035

- Short Duration Storage

- Long Duration Storage

Deployment Type Insight and Forecast 2026 - 2035

- Grid Connected Storage

- Behind-the-Meter Storage

End User Insight and Forecast 2026 - 2035

- Utility Companies

- Independent Power Producers & Commercial Energy Developers

Global Next-Generation Large-Scale Energy Storage System Market by Region

- North America

- By Technology

- By Storage Duration

- By Deployment Type

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Technology

- By Storage Duration

- By Deployment Type

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Technology

- By Storage Duration

- By Deployment Type

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Technology

- By Storage Duration

- By Deployment Type

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Next-Generation Large-Scale Energy Storage System Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Technology

1.2.2. By

Storage Duration

1.2.3. By

Deployment Type

1.2.4. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Technology

5.1.1. Lithium-Ion Battery Systems

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Flow Battery Systems

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.2. By Storage Duration

5.2.1. Short Duration Storage

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Long Duration Storage

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Deployment Type

5.3.1. Grid Connected Storage

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Behind-the-Meter Storage

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By End User

5.4.1. Utility Companies

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Independent Power Producers & Commercial Energy Developers

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Technology

6.2. By

Storage Duration

6.3. By

Deployment Type

6.4. By

End User

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Technology

7.2. By

Storage Duration

7.3. By

Deployment Type

7.4. By

End User

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Technology

8.2. By

Storage Duration

8.3. By

Deployment Type

8.4. By

End User

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Technology

9.2. By

Storage Duration

9.3. By

Deployment Type

9.4. By

End User

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

ABB Ltd.

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

BYD Company Limited

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Contemporary Amperex Technology Co., Limited (CATL)

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Fluence Energy, Inc.

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Form Energy, Inc.

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

LG Energy Solution Ltd.

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Panasonic Holdings Corporation

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Samsung SDI Co., Ltd.

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Siemens Energy AG

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Tesla, Inc.

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Next-Generation Large-Scale Energy Storage System Market