Wire Harness Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Component (Wires, Connectors, Terminals, Others), by Material (Copper, Aluminum, Others), by Voltage (Low Voltage Wiring Harness, High Voltage Wiring Harness), by Application (Automotive, Aerospace and Defense, Electronics and Electrical, Industrial Machinery, Medical Equipment, Others)

| Status : Published | Published On : Mar, 2026 | Report Code : VRSME9201 | Industry : Semiconductor & Electronics | Available Format :

|

Page : 190 |

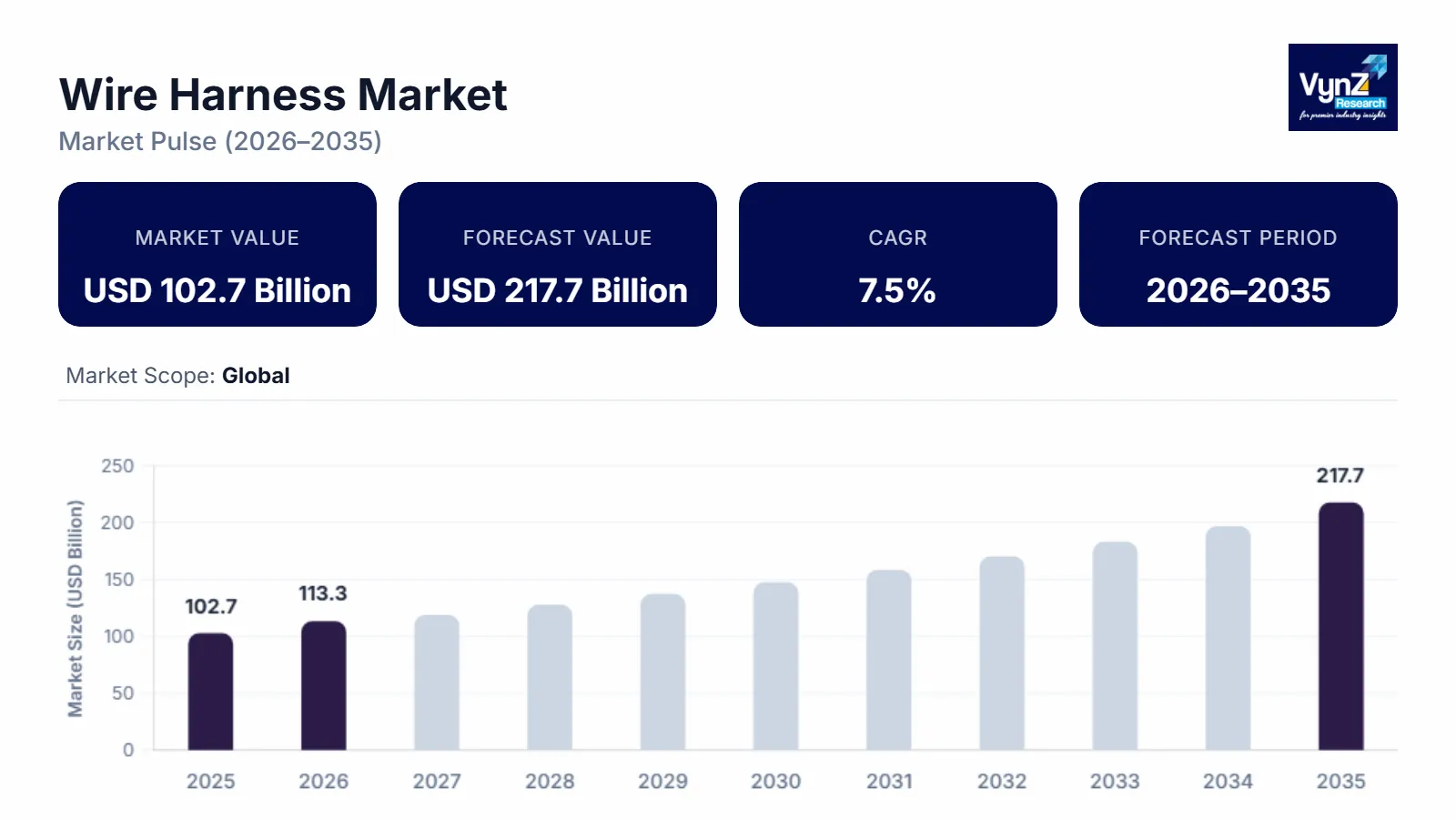

Wire Harness Market Overview

The wire harness market which was valued at approximately USD 102.7 billion in 2025 and is estimated to reach around USD 113.3 billion in 2026, is projected to reach close to USD 217.7 billion by 2035, expanding at a CAGR of about 7.5% during the forecast period from 2026 to 2035.

The market is primarily driven by the rapid expansion of the automotive, electronics, and industrial manufacturing sectors, where wire harnesses are essential for organizing and transmitting electrical power and signals efficiently. In the automotive industry, the growing production of passenger and commercial vehicles significantly increases the demand for advanced wiring systems used in power distribution, infotainment systems, lighting, safety components, and engine management. The ongoing transition toward electric vehicles (EVs) and hybrid vehicles further accelerates demand, as these vehicles require more complex wiring architectures to support battery systems, power electronics, and advanced driver-assistance systems (ADAS). Additionally, the increasing integration of electronic features such as connectivity, sensors, and digital control units in modern vehicles is raising the overall wiring content per vehicle, thereby expanding the market.

Wire Harness Market Dynamics

Market Trends

The electrification of vehicles and the rapid growth of electric vehicles (EVs) are significantly driving demand in the wire harness market. Unlike conventional internal combustion engine vehicles, EVs rely heavily on advanced electrical architectures to manage power distribution, battery connectivity, and communication between electronic components. Electric vehicles require specialized high-voltage wire harness systems that connect key components such as battery packs, inverters, electric motors, charging systems, and power control units. Under the Bipartisan Infrastructure Law, about US$7.5 billion has been allocated to develop a nationwide EV charging network targeting 500,000 public chargers by 2030. The National Electric Vehicle Infrastructure (NEVI) Program alone provides US$5 billion in funding to states to deploy high-speed chargers along major highways. As global governments introduce stricter emission regulations and provide incentives to promote clean mobility, automakers are accelerating the production of battery electric vehicles and hybrid vehicles, which increases the need for complex wiring systems. Additionally, EV platforms incorporate advanced features such as battery management systems, regenerative braking, and thermal management, all of which require reliable wiring networks. The rising integration of connected technologies and electronic control units further increases wiring complexity in EV architectures.

Growth Drivers

The rapid adoption of electric and hybrid vehicles is one of the most important growth drivers for the wire harness market. Unlike conventional vehicles, electric and hybrid vehicles require more complex electrical architectures to support battery systems, electric motors, power electronics, and charging units. These vehicles rely on high-voltage wiring harnesses to efficiently transmit power between critical components such as battery packs, inverters, and electric drive systems. As governments worldwide implement strict emission regulations and offer incentives to promote clean transportation, automakers are significantly increasing investments in electric and hybrid vehicle production. The Government of India launched the Faster Adoption and Manufacturing of Hybrid and Electric Vehicles (FAME) program to accelerate EV and hybrid vehicle adoption across the country. The FAME-II schemes allocated about US$1.4 billion to support the deployment of around 1.6 million electric and hybrid vehicles, including buses, passenger cars, and two- and three-wheelers. This shift toward electrified mobility increases the demand for advanced and durable wiring systems capable of handling higher electrical loads. In addition, hybrid vehicles combine both internal combustion engines and electric power systems, which further increases the wiring complexity. The integration of battery management systems, regenerative braking technologies, and advanced electronic control units also require sophisticated wiring networks.

Market Restraints / Challenges

Volatility in raw material prices is a major challenge for the wire harness market because key materials such as copper, aluminum, plastics, and insulation compounds are essential for manufacturing wiring systems. Copper, which is widely used due to its high electrical conductivity and reliability, often experiences significant price fluctuations in global commodity markets. These fluctuations can increase manufacturing costs and make it difficult for wire harness producers to maintain stable profit margins. Since raw materials represent a substantial portion of the overall production cost, sudden increases in prices can directly impact the pricing strategies of manufacturers. Additionally, supply disruptions, geopolitical tensions, and changes in global trade policies can further influence the availability and cost of these materials. Automotive and electronics manufacturers also demand cost-effective components, which puts additional pressure on wire harness suppliers to control expenses despite rising material costs. In some cases, manufacturers attempt to shift toward alternative materials such as aluminum wiring to reduce costs, but this requires design adjustments and additional testing.

Market Opportunities

The expansion of electric vehicle (EV) charging infrastructure is creating significant growth opportunities for the wire harness market. As the adoption of electric vehicles increases globally, governments and private companies are investing heavily in building extensive charging networks to support EV users. Charging stations require advanced electrical wiring systems to efficiently transmit high-voltage power between grid connections, charging units, and vehicle batteries. Wire harness assemblies are essential components within charging equipment, enabling safe and reliable electrical connectivity between multiple electronic and power management systems. The European Union has introduced the Alternative Fuels Infrastructure Facility (AFIF) to accelerate the deployment of EV charging infrastructure across member states. Between 2021 and 2025, the program allocated about €2.3 billion for alternative fuel infrastructure, with a large share directed toward EV charging stations along key transport corridors. In addition, fast-charging and ultra-fast charging technologies require high-capacity wiring solutions capable of handling higher electrical loads and ensuring thermal stability. The development of public charging stations, residential charging units, and commercial charging hubs is further increasing demand for specialized wiring assemblies. Governments in regions such as North America, Europe, and Asia-Pacific are introducing policies and funding programs to accelerate the deployment of EV charging infrastructure.

Global Wire Harness Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 102.7 Billion |

|

Revenue Forecast in 2035 |

USD 217.7 Billion |

|

Growth Rate |

7.5% |

|

Segments Covered in the Report |

Component, Material, Voltage, Application |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia-Pacific, Rest of the World |

|

Key Companies |

Yazaki Corporation, Sumitomo Electric Industries, Ltd., Aptiv PLC, Lear Corporation, Furukawa Electric Co., Ltd., Leoni AG, Amphenol Corporation, TE Connectivity Ltd., Samvardhana Motherson International Limited, PKC Group Ltd., Nexans S.A., Coroplast Fritz Müller GmbH & Co. KG |

|

Customization |

Available upon request |

Wire Harness Market Segmentation

By Component

Wires are the largest category with a market share of around 45% in 2025, due to their fundamental role as the primary medium for transmitting electrical power and signals across wire harness systems. Every harness assembly relies on multiple insulated wires to connect electronic components, control units, sensors, and power sources across vehicles and equipment. The increasing integration of electronic systems in automobiles, industrial machinery, and consumer electronics significantly increases the number of wires required per system. Additionally, the growth of electric vehicles and connected automotive technologies further expands the wiring content per vehicle. Manufacturers also use specialized wiring types designed for high temperature, high voltage, and durability in harsh environments.

Connectors are the fastest-growing category with a CAGR of about 7.7% during the forecast period, due to the increasing need for reliable and modular electrical connections across advanced electronic systems. Connectors enable secure attachment between wiring systems and electronic modules such as sensors, control units, infotainment systems, and power electronics. With the rapid expansion of electric vehicles, autonomous driving technologies, and connected vehicle platforms, the number of electronic modules within vehicles is increasing significantly. This trend drives the demand for high-performance connectors capable of handling high-speed data transmission and higher electrical loads. Manufacturers are also developing compact, lightweight, and corrosion-resistant connector designs to support modern vehicle architectures.

By Material

Copper is the largest category with a market share of about 80% in 2025, due to its superior electrical conductivity, durability, and reliability in electrical wiring applications. Copper wiring provides efficient power transmission with minimal energy loss, making it the preferred material for most automotive, industrial, and electronic wire harness systems. Its flexibility and resistance to corrosion also allow it to perform reliably in demanding operating conditions such as high temperatures and vibration environments. In automotive applications, copper wiring is widely used for engine control units, infotainment systems, lighting systems, and safety electronics. Despite price fluctuations, manufacturers continue to rely heavily on copper due to its consistent performance and established manufacturing processes.

Aluminum is the fastest-growing category during the forecast period, due to increasing efforts by manufacturers to reduce vehicle weight and improve energy efficiency. Aluminum wiring is significantly lighter than copper, which helps reduce overall vehicle mass and improve fuel efficiency or electric vehicle battery range. Automotive manufacturers are increasingly adopting aluminum wire harness solutions in power distribution systems and battery connections. Advances in aluminum conductor technology and improved insulation materials are helping overcome earlier challenges related to conductivity and durability. In addition, the relatively lower cost of aluminum compared to copper makes it an attractive alternative for large-scale wiring applications. Electric vehicle manufacturers are particularly exploring aluminum-based harnesses to support lightweight vehicle architectures.

By Voltage

Low voltage wiring harness is the largest category with a market share of about 75% in 2025, due to its widespread use across conventional vehicles and a wide range of electronic devices. These wiring systems typically operate below 60 volts and are used in applications such as lighting systems, infotainment units, dashboard electronics, climate control systems, and sensors. Most passenger and commercial vehicles rely heavily on low-voltage electrical networks to support everyday electronic functionalities. The rapid integration of advanced driver-assistance systems, connectivity features, and digital dashboards further increases demand for low-voltage wiring networks. Additionally, low-voltage harness systems are widely used in consumer electronics, telecommunications equipment, and industrial automation devices.

High voltage wiring harness is the fastest-growing category with a CAGR of about 7.9% during the forecast period, driven primarily by the rapid expansion of electric and hybrid vehicles worldwide. High-voltage harness systems are designed to handle voltages above 60 volts and are essential for connecting battery packs, inverters, electric motors, and charging systems in electric vehicles. As global automakers accelerate electrification strategies, the demand for specialized high-voltage wiring solutions continues to increase. These harnesses require advanced insulation materials and safety features to handle higher electrical loads and thermal conditions.

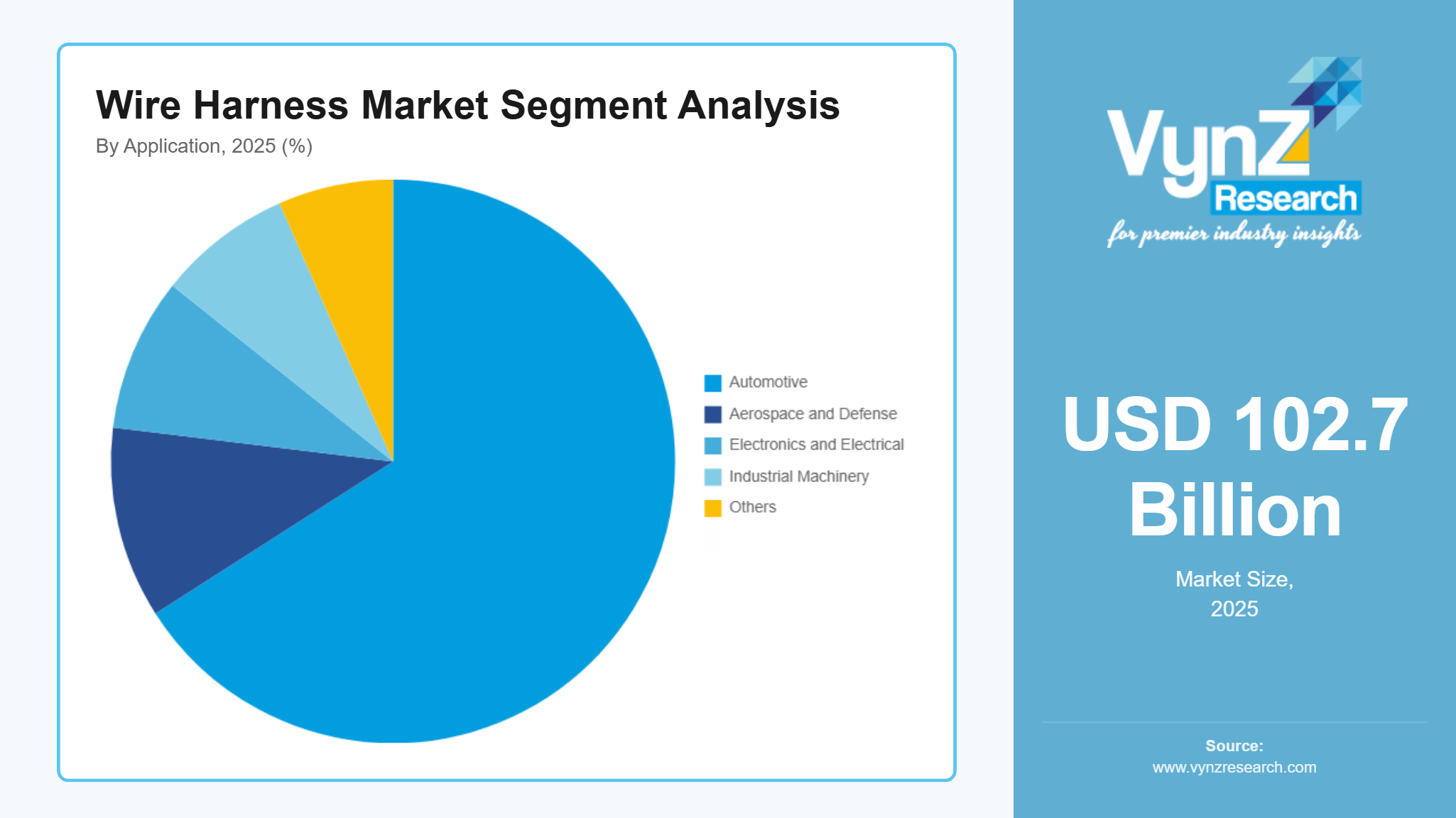

By Application

Automotive is the largest category with a market share of approx. 60% in 2025, due to the extensive use of wire harness systems across modern vehicles. Wire harnesses connect numerous electrical and electronic components such as engines, sensors, lighting systems, infotainment units, and safety systems. The growing production of passenger cars, commercial vehicles, and electric vehicles significantly increases the demand for wiring assemblies. Modern vehicles incorporate hundreds of electrical connections to support advanced driver-assistance systems, connectivity features, and digital control units. Additionally, the shift toward electric and hybrid powertrains further increases the complexity and volume of wiring systems required. Automotive manufacturers also focus on improving wiring efficiency to support lightweight vehicle architectures and enhanced electrical performance.

Electronics and electrical is the fastest-growing category with a CAGR of about 8.2% during the forecast period, due to the rapid expansion of consumer electronics, telecommunications equipment, and smart devices. Products such as smartphones, computers, home appliances, and networking devices rely on compact and efficient wiring systems for internal connectivity. The growth of data centers, 5G communication infrastructure, and smart home technologies is further increasing the demand for reliable wire harness assemblies. In addition, industrial electronics and automation systems require specialized wiring solutions to ensure stable power and signal transmission. Manufacturers are increasingly developing miniaturized and high-performance harness designs to support compact electronic devices.

Regional Insights

Asia-Pacific

Asia-Pacific is the largest regional market for the wire harness market, supported by the strong presence of automotive manufacturing hubs and large-scale electronics production facilities. Countries such as China, Japan, South Korea, and India dominate global vehicle manufacturing and consumer electronics production, which significantly increases demand for wire harness systems. China leads the region due to its massive electric vehicle production capacity and strong supply chain for automotive components. The region also hosts many leading wire harness manufacturers and suppliers, creating an efficient manufacturing ecosystem. Government support has enabled China to build the largest EV charging network in the world, accounting for roughly 65% of global charging infrastructure and about 60% of electric light-duty vehicle stock. Rapid industrialization and expanding infrastructure projects further increase the demand for wiring systems in industrial equipment and machinery. Additionally, governments across Asia-Pacific are investing heavily in electric mobility and smart manufacturing initiatives. The combination of strong automotive output, electronics manufacturing dominance, and cost-effective production capabilities continues to strengthen the region’s leadership in the global wire harness market.

North America

North America is the fastest-growing region in the wire harness market, driven by increasing investments in electric vehicle manufacturing and advanced automotive technologies. The United States leads the region with strong automotive innovation, significant electric vehicle investments, and the presence of major technology and automotive companies. Automakers are expanding EV production facilities and investing in next-generation vehicle platforms, which require advanced electrical architecture and high-voltage wiring systems. In addition, the region is witnessing growing demand for wire harness systems in aerospace, defense, and industrial automation sectors. Government policies promoting clean energy, electric mobility, and advanced manufacturing are further accelerating the adoption of modern electrical systems. Investments in EV charging infrastructure and renewable energy projects also contribute to the rising demand for advanced wiring assemblies.

Europe

Europe maintains a strong presence in the wire harness market due to its advanced automotive industry and strict environmental regulations promoting vehicle electrification. Countries such as Germany, France, Italy, and the United Kingdom are major automotive production centers and are actively investing in electric and hybrid vehicle technologies. The region is home to several leading automotive manufacturers and component suppliers that require highly sophisticated wiring systems. European Union policies encouraging low-emission vehicles and sustainable mobility are accelerating the transition toward electric powertrains. This shift increases the need for high-voltage wiring harnesses used in electric vehicle battery systems and power electronics. The Spanish government announced a €700 million investment plan to accelerate electric vehicle adoption and strengthen the domestic automotive industry. Approximately €400 million will subsidize EV purchases, while €300 million will support charging infrastructure expansion across the country. In addition, the region’s strong aerospace and industrial automation sectors contribute to demand for specialized wiring solutions. Continuous investments in automotive innovation and electrification strengthen Europe’s position in the global wire harness market.

Rest of the World

The rest of the world, including Latin America, the Middle East, and Africa, is experiencing gradual growth in the wire harness market due to increasing industrialization and expanding automotive production. In Latin America, countries such as Brazil and Mexico are strengthening their automotive manufacturing sectors, which drives demand for vehicle wiring systems. Mexico has become an important automotive manufacturing hub supplying vehicles and components to North America. In the Middle East, investments in infrastructure development, renewable energy projects, and industrial facilities are supporting the demand for electrical wiring assemblies. Meanwhile, African countries such as South Africa are gradually expanding automotive assembly operations and industrial manufacturing capabilities. Although market maturity varies across these regions, rising industrial activities and infrastructure development are expected to support steady growth in wire harness demand.

Competitive Landscape / Company Insights

The wire harness market is moderately fragmented, characterized by the presence of large global automotive component manufacturers alongside numerous regional suppliers specializing in customized wiring solutions. Major companies compete primarily on manufacturing scale, technological capabilities, cost efficiency, and long-term supply agreements with automotive and electronics manufacturers. Leading global players such as Yazaki Corporation, Sumitomo Electric Industries, Ltd., and Aptiv PLC dominate the market through extensive global production networks, strong relationships with major automotive OEMs, and broad portfolios of automotive electrical distribution systems. These companies benefit from high production volumes, strong research and development capabilities, and advanced manufacturing technologies that allow them to support the growing complexity of vehicle electrical architectures.

In addition, companies such as Lear Corporation, Furukawa Electric Co., Ltd., and Leoni AG compete by providing advanced wiring systems designed for electric vehicles, autonomous driving platforms, and connected vehicle technologies. Their strategies often focus on lightweight harness development, modular wiring architectures, and high-voltage wiring systems required for electric powertrains. Meanwhile, suppliers such as Amphenol Corporation and TE Connectivity Ltd. leverage their strong expertise in connectors and electronic interconnect technologies to support increasingly complex electrical systems across automotive, aerospace, and industrial sectors.

Mini Profiles

Yazaki Corporation is one of the world’s largest manufacturers of automotive wiring harnesses and electrical distribution systems, supplying major global automotive manufacturers with advanced electrical components and vehicle wiring solutions.

Sumitomo Electric Industries, Ltd. is a leading supplier of automotive wiring harnesses and electrical components, known for its advanced materials technology and global manufacturing network.

Aptiv PLC develops advanced automotive electrical architecture and connectivity solutions, including high-performance wire harness systems, connectors, and vehicle data networks.

Lear Corporation is a major automotive technology company that produces electrical distribution systems, including wire harnesses and vehicle connectivity solutions.

Furukawa Electric Co., Ltd. (Japan) manufactures automotive wiring harnesses, electronic components, and advanced materials used in automotive and industrial electrical systems.

Key Players

- Yazaki Corporation

- Sumitomo Electric Industries, Ltd.

- Aptiv PLC

- Lear Corporation

- Furukawa Electric Co., Ltd.

- Leoni AG

- Amphenol Corporation

- TE Connectivity Ltd.

- Samvardhana Motherson International Limited

- PKC Group Ltd.

- Nexans S.A.

- Coroplast Fritz Müller GmbH & Co. KG

Recent Developments

In January 2026, Aptiv PLC announced the expansion of its high-voltage wiring harness production capacity to support the growing demand for electric vehicle electrical architectures from global automotive manufacturers.

In December 2025, Yazaki Corporation introduced a next-generation lightweight automotive wiring harness designed to reduce vehicle weight and improve energy efficiency in electric and hybrid vehicles.

In October 2025, Sumitomo Electric Industries, Ltd. developed a new high-voltage wiring system optimized for electric vehicle battery and power distribution applications, improving thermal performance and electrical safety.

In September 2025, Samvardhana Motherson International Limited expanded its automotive wiring harness manufacturing facility in India to strengthen supply capabilities for global electric vehicle platforms.

In July 2025, Lear Corporation launched an advanced electrical distribution system platform designed to support next-generation connected and autonomous vehicles.

In May 2025, Leoni AG announced a strategic restructuring initiative focused on strengthening its automotive wiring systems business and expanding its electric mobility solutions portfolio.

Global Wire Harness Market Coverage

Component Insight and Forecast 2026 - 2035

- Wires

- Connectors

- Terminals

- Others

Material Insight and Forecast 2026 - 2035

- Copper

- Aluminum

- Others

Voltage Insight and Forecast 2026 - 2035

- Low Voltage Wiring Harness

- High Voltage Wiring Harness

Application Insight and Forecast 2026 - 2035

- Automotive

- Aerospace and Defense

- Electronics and Electrical

- Industrial Machinery

- Medical Equipment

- Others

Global Wire Harness Market by Region

- North America

- By Component

- By Material

- By Voltage

- By Application

- By Country - U.S., Canada, Mexico

- Europe

- By Component

- By Material

- By Voltage

- By Application

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Component

- By Material

- By Voltage

- By Application

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Component

- By Material

- By Voltage

- By Application

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Wire Harness Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Component

1.2.2. By

Material

1.2.3. By

Voltage

1.2.4. By

Application

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Component

5.1.1. Wires

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Connectors

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Terminals

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Others

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.2. By Material

5.2.1. Copper

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Aluminum

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Others

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By Voltage

5.3.1. Low Voltage Wiring Harness

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. High Voltage Wiring Harness

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By Application

5.4.1. Automotive

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Aerospace and Defense

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Electronics and Electrical

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Industrial Machinery

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Medical Equipment

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

5.4.6. Others

5.4.6.1. Market Definition

5.4.6.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Component

6.2. By

Material

6.3. By

Voltage

6.4. By

Application

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Component

7.2. By

Material

7.3. By

Voltage

7.4. By

Application

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Component

8.2. By

Material

8.3. By

Voltage

8.4. By

Application

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Component

9.2. By

Material

9.3. By

Voltage

9.4. By

Application

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Yazaki Corporation

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Sumitomo Electric Industries, Ltd.

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Aptiv PLC

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Lear Corporation

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Furukawa Electric Co., Ltd.

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Leoni AG

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Amphenol Corporation

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

TE Connectivity Ltd.

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Samvardhana Motherson International Limited

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

PKC Group Ltd.

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

Nexans S.A.

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

10.12.

Coroplast Fritz Müller GmbH & Co. KG

10.12.1.

Snapshot

10.12.2.

Overview

10.12.3.

Offerings

10.12.4.

Financial

Insight

10.12.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Wire Harness Market