North America Electric Vehicle Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Component (Battery Pack & High Voltage Components, Electric Motor, Brake, Wheel & Suspension, Body & Chassis, Low Voltage Electric Components), by Propulsion Type (Battery Electric Vehicle (BEV), Plug-in Hybrid Electric Vehicle (PHEV), Hybrid Electric Vehicle (HEV), Fuel Cell Electric Vehicle (FCEV)), by Vehicle Type (Passenger Vehicles, Commercial Vehicles), by Power Output (Less than 100 kW, 100–250 kW, Above 250 kW), by Vehicle Class (Low-priced, Mid-priced, Luxury), by EV Charging Points (Normal Charging, Super Charging), by Vehicle Drive Type (Front-Wheel Drive (FWD), Rear-Wheel Drive (RWD), All-Wheel Drive (AWD))

| Status : Published | Published On : Jul, 2026 | Report Code : VRAT9673 | Industry : Automotive & Transportation | Available Format :

|

Page : 131 |

North America Electric Vehicle Market Overview

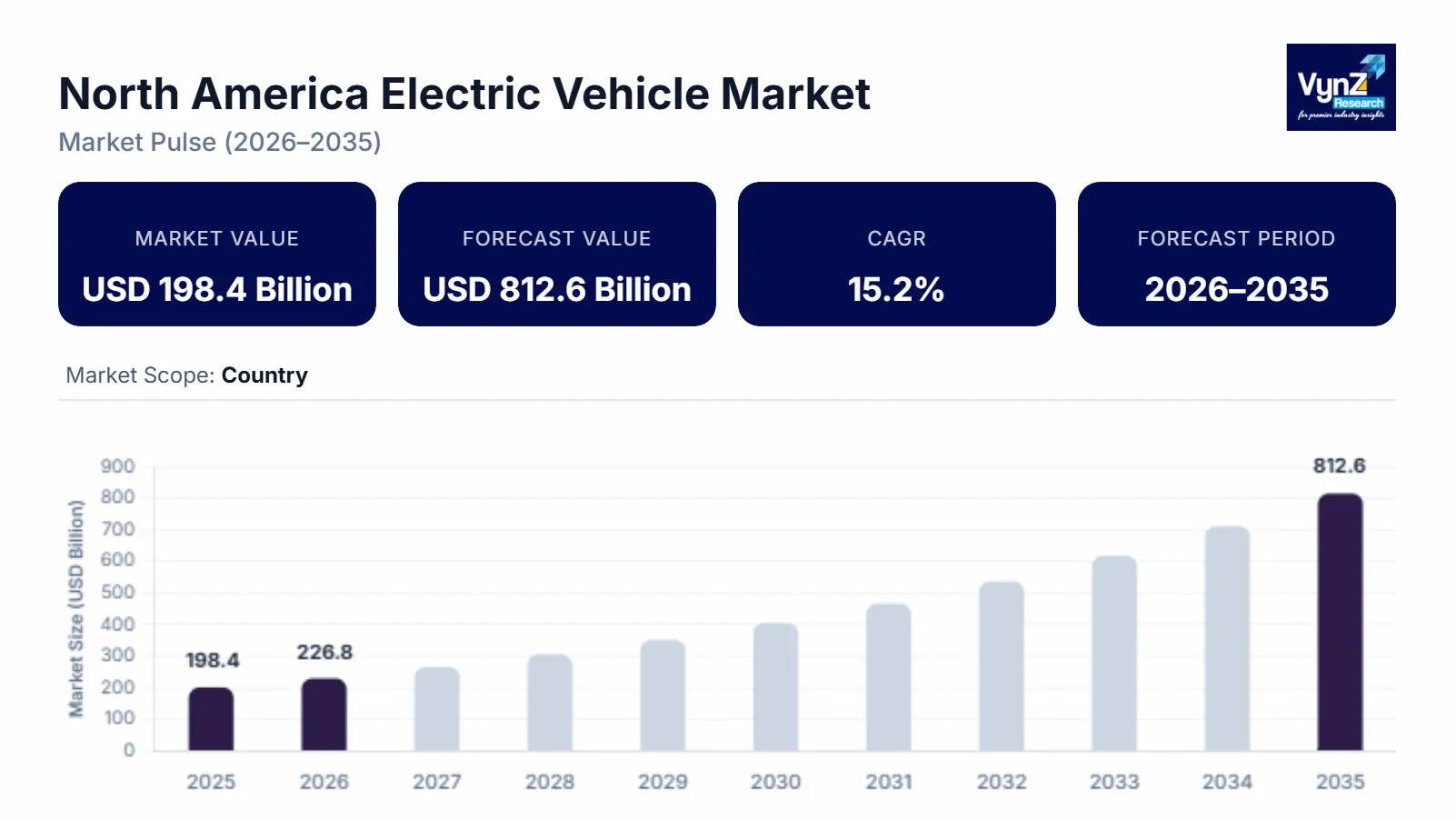

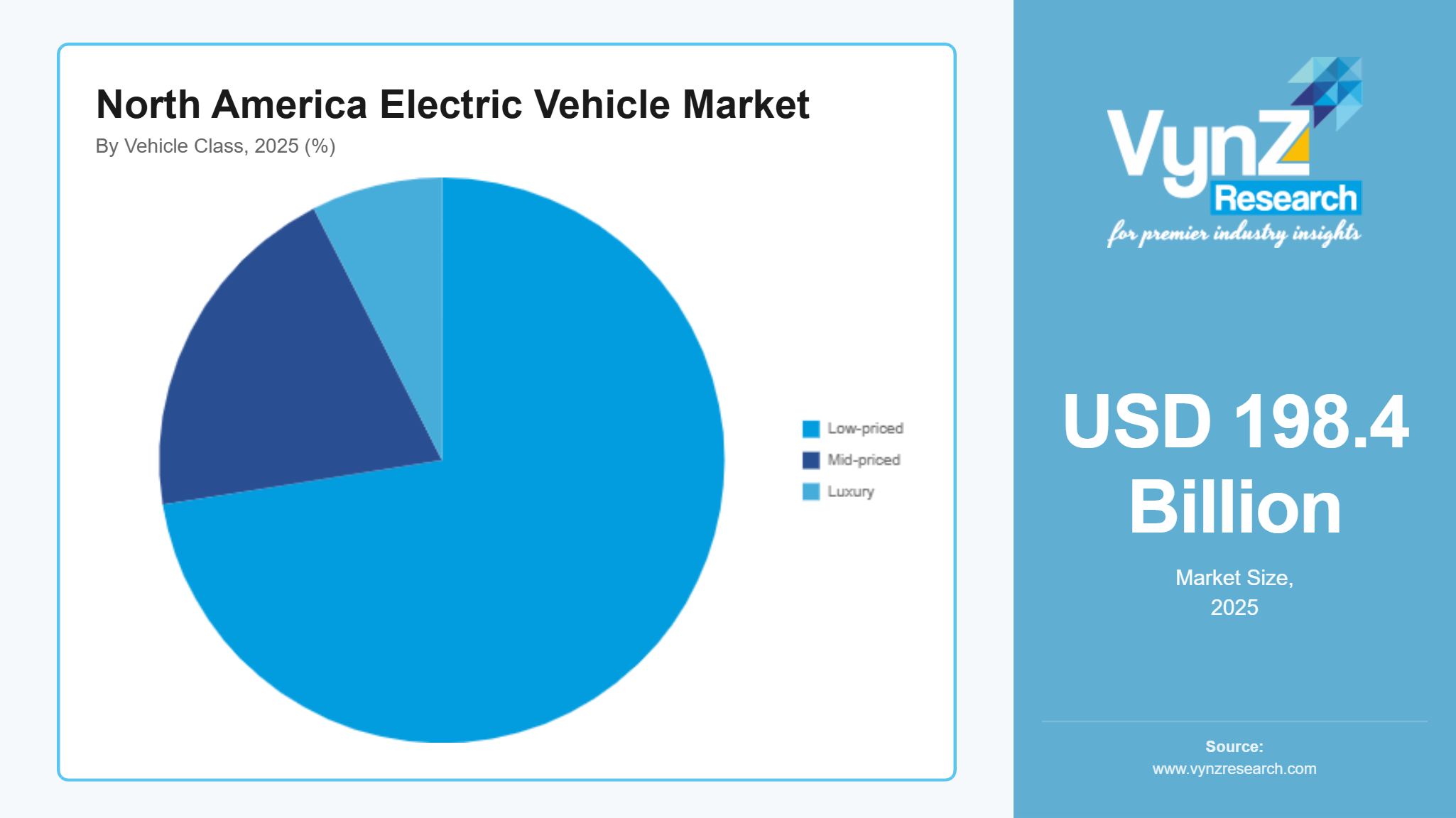

The North America electric vehicle market size was estimated at about USD 198.4 billion in 2025 and is expected to reach around USD 226.8 billion in 2026, rising up to roughly USD 812.6 billion by 2035, growing at approximately 15.2% CAGR from 2026 to 2035.

Research Highlights

- Battery electric vehicles held 52.8% market share in 2025 due to charging infrastructure expansion and declining battery costs.

- Passenger vehicles captured 72.5% market share in 2025 because of higher consumer adoption and government purchase incentives.

- Normal charging accounted for 61.4% market share in 2025, supported by widespread residential and workplace infrastructure deployment.

- The Plug-in hybrid electric vehicles market is projected to expand at 16.4% CAGR due to growing demand.

- The United States represented 58% market share in 2025, supported by manufacturing expansion and federal clean transportation initiatives.

Market growth is supported by expanding electric vehicle adoption, supportive federal and state incentive programs and continuous investments in charging infrastructure, along with increasing deployment of advanced battery technologies. Increasing demand for zero emission passenger and commercial mobility, along with ongoing investments under the U.S. Department of Energy, the Joint Office of Energy and Transportation, and Natural Resources Canada to expand charging networks and strengthen domestic battery manufacturing continues to support industry expansion across major regions including California, Texas, and Ontario. The International Energy Agency (IEA) also reports sustained growth in electric vehicle sales across North America, reinforcing long term market development.

North America Electric Vehicle Market Dynamics

Market Trends

The industry is witnessing notable shifts in battery technology, charging infrastructure and consumer purchasing preferences. One of the key trends shaping the market is the rapid adoption of lithium iron phosphate and next generation battery chemistries, reflecting growing demand for improved safety, longer driving range and lower ownership costs. Another emerging trend is the expansion of fast charging networks, supported by funding from the U.S. Department of Energy, the Joint Office of Energy and Transportation, and Natural Resources Canada, while the International Energy Agency (IEA) highlights continued growth in public charging infrastructure across North America, encouraging manufacturers to develop connected and software defined electric vehicles.

Growth Drivers

The growth of the market is largely supported by favorable government policies and expanding domestic electric vehicle manufacturing, which continue to generate consistent demand across passenger and commercial transportation. Increasing investments in battery production facilities, charging infrastructure and critical mineral supply chains are further accelerating market expansion. Additionally, stricter vehicle emission standards established by the U.S. Environmental Protection Agency (EPA) and investments promoted by the U.S. Department of Energy are boosting adoption, while the International Energy Agency (IEA) reports sustained increases in electric vehicle sales and infrastructure development throughout the region.

Market Restraints / Challenges

Despite favorable growth prospects, the market faces certain challenges that may limit its expansion. High battery production costs and dependence on critical minerals continue to affect profitability and market penetration, particularly among price sensitive consumers. Furthermore, uneven charging infrastructure deployment poses operational challenges for manufacturers and service providers, while dependence on imported battery materials and processing technologies can result in cost pressures and supply disruptions. The U.S. Geological Survey (USGS) and the International Energy Agency (IEA) have identified critical mineral supply security as an important challenge for long term electric vehicle industry growth.

Market Opportunities

The market presents significant opportunities in domestic battery manufacturing and advanced charging infrastructure, particularly driven by supportive industrial policies and rising demand for zero emission mobility. Companies offering high performance batteries, smart charging systems and connected mobility solutions are well positioned to capture growing demand from passenger vehicle owners, fleet operators and commercial transport providers. Another key opportunity lies in vehicle to grid technologies and battery recycling, where increasing investments supported by the U.S. Department of Energy and research highlighted by the National Renewable Energy Laboratory (NREL) are creating long term opportunities for sustainable value creation and improved energy management.

North America Electric Vehicle Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 198.4 Billion |

|

Revenue Forecast in 2035 |

USD 812.6 Billion |

|

Growth Rate |

15.2% |

|

Segments Covered in the Report |

By Component, By Propulsion Type, By Vehicle Type, By Power Output, By Vehicle Class, By EV Charging Points, By Vehicle Drive Type |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

United States, Canada, Mexico, Rest of North America |

|

Key Companies |

BMW, Canoo, Daimler AG, Ford Motor Company, General Motors, Honda Motor, Hyundai, Nissan, Tesla, Toyota Motor Corporation |

|

Customization |

Available upon request |

North America Electric Vehicle Market Segmentation

By Propulsion Type

Battery electric vehicles accounted for the largest market share of approximately 52.8% in 2025, supported by expanding public charging infrastructure, declining battery costs and strong federal and state purchase incentives.

Plug in hybrid electric vehicles continue to maintain stable demand where charging accessibility remains limited and will expand at 16.4% CAGR through the forecast period due to higher funding and growing demand.

By Vehicle Type

Passenger vehicles represented the dominant share of nearly 72.5% in 2025 because of higher consumer adoption, broader model availability and expanding incentives for zero emission transportation.

Commercial vehicles are projected to register the highest growth at approximately 15.9% CAGR during the forecast period as fleet operators accelerate electrification to reduce operating costs and comply with sustainability targets.

By EV Charging Points

Normal charging infrastructure accounted for an estimated 61.4% market share in 2025 due to widespread residential installations and workplace charging facilities that meet daily commuting requirements.

Super charging is expected to witness the fastest expansion, advancing at nearly 16.1% CAGR through 2035 due to increase in demand for reduced charging time and improved convenience for long distance travel and continued investments in high power charging corridors by public agencies and private operators.

By Vehicle Class

Mid-priced vehicles held the largest revenue share of around 49.8% in 2025 influenced by balanced pricing, improving battery range and increasing availability across multiple vehicle categories.

Luxury electric vehicles are anticipated to record the fastest growth at approximately 15.8% CAGR during the forecast period as manufacturers introduce premium models equipped with advanced driver assistance systems, connected technologies and higher performance batteries.

Regional Insights

United States

The United States accounted for approximately 58% of the market in 2025 due to strong domestic vehicle production, expanding charging infrastructure and favorable federal and state incentive programs. Major automotive manufacturing hubs including California, Michigan and Texas continue to strengthen market demand through rising electric vehicle adoption. The U.S. Department of Energy and the U.S. Environmental Protection Agency (EPA) continue to support battery manufacturing, charging infrastructure expansion, and vehicle electrification through clean transportation initiatives.

Canada

Canada represented an estimated 12% share of the regional market in 2025, supported by growing electric vehicle adoption, expanding battery supply chain investments and abundant critical mineral resources. Demand continues to increase across Ontario, Quebec, and British Columbia as governments promote cleaner transportation and manufacturing competitiveness. Natural Resources Canada continues to support zero emission vehicle adoption through purchase incentives and charging infrastructure investments, strengthening long term industry development.

Mexico

Mexico accounted for approximately 7% of the market in 2025 for the increasing automotive manufacturing investments and the expansion of export oriented electric vehicle production facilities. The country continues to attract global manufacturers due to its established automotive supply chain and strategic trade connectivity.

Rest of North America

The rest of North America contributed an estimated 11% of the market in 2025 due to steady investments in charging infrastructure and increasing awareness of sustainable transportation solutions. Government agencies and public utilities are expanding clean mobility initiatives to improve electric vehicle accessibility and reduce transport related emissions. According to the International Energy Agency (IEA), continued infrastructure investments are expected to support long term adoption across smaller regional markets. The remaining 12% of the regional market is collectively represented by other countries and territories across North America that are not covered individually in this analysis.

Competitive Landscape / Company Insights

The market is highly competitive, with global and regional manufacturers focusing on battery innovation, software integration, manufacturing expansion and charging ecosystem development to strengthen their market positions. Companies are increasing investments in research and development, advanced battery technologies and localized production to improve supply chain resilience and cost efficiency. The U.S. Department of Energy continues to support domestic battery manufacturing and critical mineral processing, while the International Energy Agency (IEA) highlights increasing investments in electric vehicle production and charging infrastructure across North America, intensifying market competition.

Mini Profiles

BMW develops premium electric vehicles and advanced battery technologies, supported by strong brand recognition, continuous innovation, and an expanding manufacturing network across North America.

Canoo focuses on purpose built electric mobility platforms for commercial and lifestyle applications, leveraging flexible vehicle architecture and strategic partnerships to strengthen market presence.

Daimler AG offers electric trucks, buses, and premium passenger vehicles, emphasizing performance, operational efficiency, and advanced connected mobility solutions for commercial and consumer markets.

Ford Motor Company manufactures a broad portfolio of electric passenger and commercial vehicles, supported by extensive dealership networks, domestic production, and continued investments in battery technology.

General Motors focuses on scalable electric vehicle platforms and battery innovation, backed by localized manufacturing, advanced software integration, and strategic investments in North American electrification initiatives.

Key Players

- BMW

- Canoo

- Daimler AG

- Ford Motor Company

- General Motors

- Honda Motor

- Hyundai

- Nissan

- Tesla

- Toyota Motor Corporation

Recent Developments

In January 2025, Hyundai announced the expansion of electric vehicle production capacity at its North American manufacturing facilities to support growing regional demand. The investment is expected to strengthen local supply chains and improve delivery timelines for new electric models.

In January 2025, Honda Motor confirmed plans to introduce an affordable electric vehicle priced below USD 30,000 for the North American market by 2026 under its Honda 0 Series. The model will be manufactured locally to accelerate the company's regional electrification strategy.

In January 2025, Tesla launched the redesigned Model Y for the United States, Canada, and Mexico, with deliveries beginning in March 2025. The refreshed model features updated styling and improved technology to strengthen its position in the regional electric vehicle market.

In January 2026, Toyota Motor Corporation reported strong performance for several electrified vehicle models in the United States, reflecting continued investments in electrification and product portfolio expansion. The company also continued advancing battery technology and next generation electric vehicle development.

In January 2025, Volkswagen recorded a significant recovery in North American electric vehicle sales, led by higher demand for the ID.4 following the resumption of deliveries. The company continued strengthening its electric vehicle portfolio and regional manufacturing capabilities to support future growth.

North America Electric Vehicle Market Coverage

Component Insight and Forecast 2026 - 2035

- Battery Pack & High Voltage Components

- Electric Motor

- Brake

- Wheel & Suspension

- Body & Chassis

- Low Voltage Electric Components

Propulsion Type Insight and Forecast 2026 - 2035

- Battery Electric Vehicle (BEV)

- Plug-in Hybrid Electric Vehicle (PHEV)

- Hybrid Electric Vehicle (HEV)

- Fuel Cell Electric Vehicle (FCEV)

Vehicle Type Insight and Forecast 2026 - 2035

- Passenger Vehicles

- Commercial Vehicles

Power Output Insight and Forecast 2026 - 2035

- Less than 100 kW

- 100–250 kW

- Above 250 kW

Vehicle Class Insight and Forecast 2026 - 2035

- Low-priced

- Mid-priced

- Luxury

EV Charging Points Insight and Forecast 2026 - 2035

- Normal Charging

- Super Charging

Vehicle Drive Type Insight and Forecast 2026 - 2035

- Front-Wheel Drive (FWD)

- Rear-Wheel Drive (RWD)

- All-Wheel Drive (AWD)

North America Electric Vehicle Market by Region

- U.S.

- By Component

- By Propulsion Type

- By Vehicle Type

- By Power Output

- By Vehicle Class

- By EV Charging Points

- By Vehicle Drive Type

- Canada

- By Component

- By Propulsion Type

- By Vehicle Type

- By Power Output

- By Vehicle Class

- By EV Charging Points

- By Vehicle Drive Type

- Mexico

- By Component

- By Propulsion Type

- By Vehicle Type

- By Power Output

- By Vehicle Class

- By EV Charging Points

- By Vehicle Drive Type

Table of Contents for North America Electric Vehicle Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Component

1.2.2. By

Propulsion Type

1.2.3. By

Vehicle Type

1.2.4. By

Power Output

1.2.5. By

Vehicle Class

1.2.6. By

EV Charging Points

1.2.7. By

Vehicle Drive Type

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. North Market Estimate and Forecast

4.1. North Market Overview

4.2. North Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Component

5.1.1. Battery Pack & High Voltage Components

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Electric Motor

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Brake

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Wheel & Suspension

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Body & Chassis

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.1.6. Low Voltage Electric Components

5.1.6.1. Market Definition

5.1.6.2. Market Estimation and Forecast to 2035

5.2. By Propulsion Type

5.2.1. Battery Electric Vehicle (BEV)

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Plug-in Hybrid Electric Vehicle (PHEV)

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Hybrid Electric Vehicle (HEV)

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Fuel Cell Electric Vehicle (FCEV)

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.3. By Vehicle Type

5.3.1. Passenger Vehicles

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Commercial Vehicles

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By Power Output

5.4.1. Less than 100 kW

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. 100–250 kW

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Above 250 kW

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.5. By Vehicle Class

5.5.1. Low-priced

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Mid-priced

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Luxury

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.6. By EV Charging Points

5.6.1. Normal Charging

5.6.1.1. Market Definition

5.6.1.2. Market Estimation and Forecast to 2035

5.6.2. Super Charging

5.6.2.1. Market Definition

5.6.2.2. Market Estimation and Forecast to 2035

5.7. By Vehicle Drive Type

5.7.1. Front-Wheel Drive (FWD)

5.7.1.1. Market Definition

5.7.1.2. Market Estimation and Forecast to 2035

5.7.2. Rear-Wheel Drive (RWD)

5.7.2.1. Market Definition

5.7.2.2. Market Estimation and Forecast to 2035

5.7.3. All-Wheel Drive (AWD)

5.7.3.1. Market Definition

5.7.3.2. Market Estimation and Forecast to 2035

6. U.S. Market Estimate and Forecast

6.1. By

Component

6.2. By

Propulsion Type

6.3. By

Vehicle Type

6.4. By

Power Output

6.5. By

Vehicle Class

6.6. By

EV Charging Points

6.7. By

Vehicle Drive Type

7. Canada Market Estimate and Forecast

7.1. By

Component

7.2. By

Propulsion Type

7.3. By

Vehicle Type

7.4. By

Power Output

7.5. By

Vehicle Class

7.6. By

EV Charging Points

7.7. By

Vehicle Drive Type

8. Mexico Market Estimate and Forecast

8.1. By

Component

8.2. By

Propulsion Type

8.3. By

Vehicle Type

8.4. By

Power Output

8.5. By

Vehicle Class

8.6. By

EV Charging Points

8.7. By

Vehicle Drive Type

9. Company Profiles

9.1.

BMW

9.1.1.

Snapshot

9.1.2.

Overview

9.1.3.

Offerings

9.1.4.

Financial

Insight

9.1.5.

Recent

Developments

9.2.

Canoo

9.2.1.

Snapshot

9.2.2.

Overview

9.2.3.

Offerings

9.2.4.

Financial

Insight

9.2.5.

Recent

Developments

9.3.

Daimler AG

9.3.1.

Snapshot

9.3.2.

Overview

9.3.3.

Offerings

9.3.4.

Financial

Insight

9.3.5.

Recent

Developments

9.4.

Ford Motor Company

9.4.1.

Snapshot

9.4.2.

Overview

9.4.3.

Offerings

9.4.4.

Financial

Insight

9.4.5.

Recent

Developments

9.5.

General Motors

9.5.1.

Snapshot

9.5.2.

Overview

9.5.3.

Offerings

9.5.4.

Financial

Insight

9.5.5.

Recent

Developments

9.6.

Honda Motor

9.6.1.

Snapshot

9.6.2.

Overview

9.6.3.

Offerings

9.6.4.

Financial

Insight

9.6.5.

Recent

Developments

9.7.

Hyundai

9.7.1.

Snapshot

9.7.2.

Overview

9.7.3.

Offerings

9.7.4.

Financial

Insight

9.7.5.

Recent

Developments

9.8.

Nissan

9.8.1.

Snapshot

9.8.2.

Overview

9.8.3.

Offerings

9.8.4.

Financial

Insight

9.8.5.

Recent

Developments

9.9.

Tesla

9.9.1.

Snapshot

9.9.2.

Overview

9.9.3.

Offerings

9.9.4.

Financial

Insight

9.9.5.

Recent

Developments

9.10.

Toyota Motor Corporation

9.10.1.

Snapshot

9.10.2.

Overview

9.10.3.

Offerings

9.10.4.

Financial

Insight

9.10.5.

Recent

Developments

10. Appendix

10.1. Exchange Rates

10.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

North America Electric Vehicle Market