North America Light Electric Charging Station Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Charging Station Type (Public Charging Stations, Private Charging Stations), by Charging Technology (Level 1 Charging, Level 2 Charging, DC Fast Charging), by Application (Residential, Commercial, Public Infrastructure), by End User (Individual Consumers, Commercial Fleet Operators, Government Organizations, Others)

| Status : Published | Published On : Jul, 2026 | Report Code : VRAT9673 | Industry : Automotive & Transportation | Available Format :

|

Page : 132 |

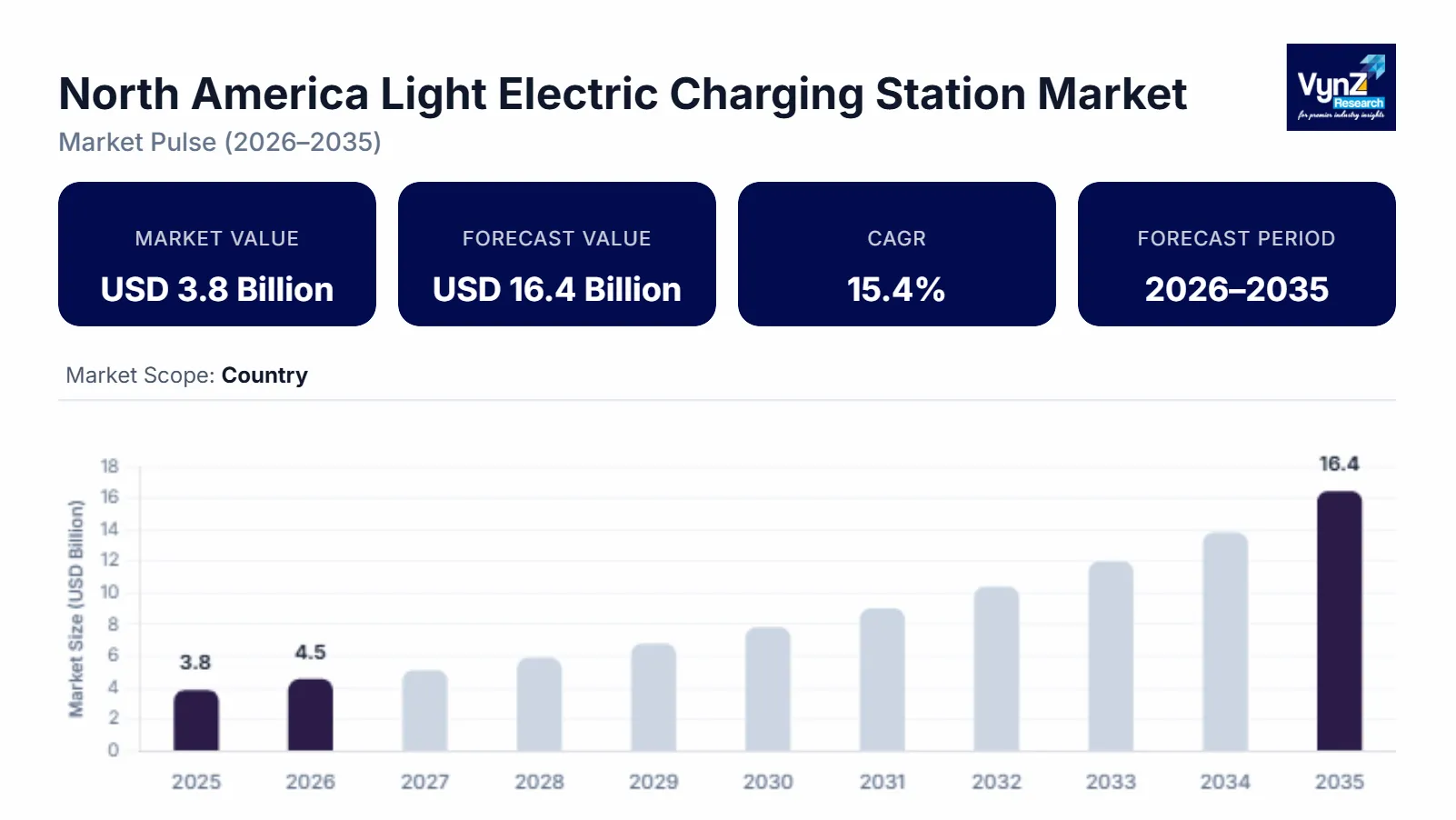

North America Light Electric Charging Station Market Overview

The North America light electric charging station market size was estimated at about USD 3.8 billion in 2025 and is expected to reach around USD 4.5 billion in 2026, rising up to roughly USD 16.4 billion by 2035, growing at approximately 15.4% CAGR from 2026 to 2035.

Research Highlights

- Public charging stations captured 56.8% market share in 2025, driven by expanding government funded charging infrastructure.

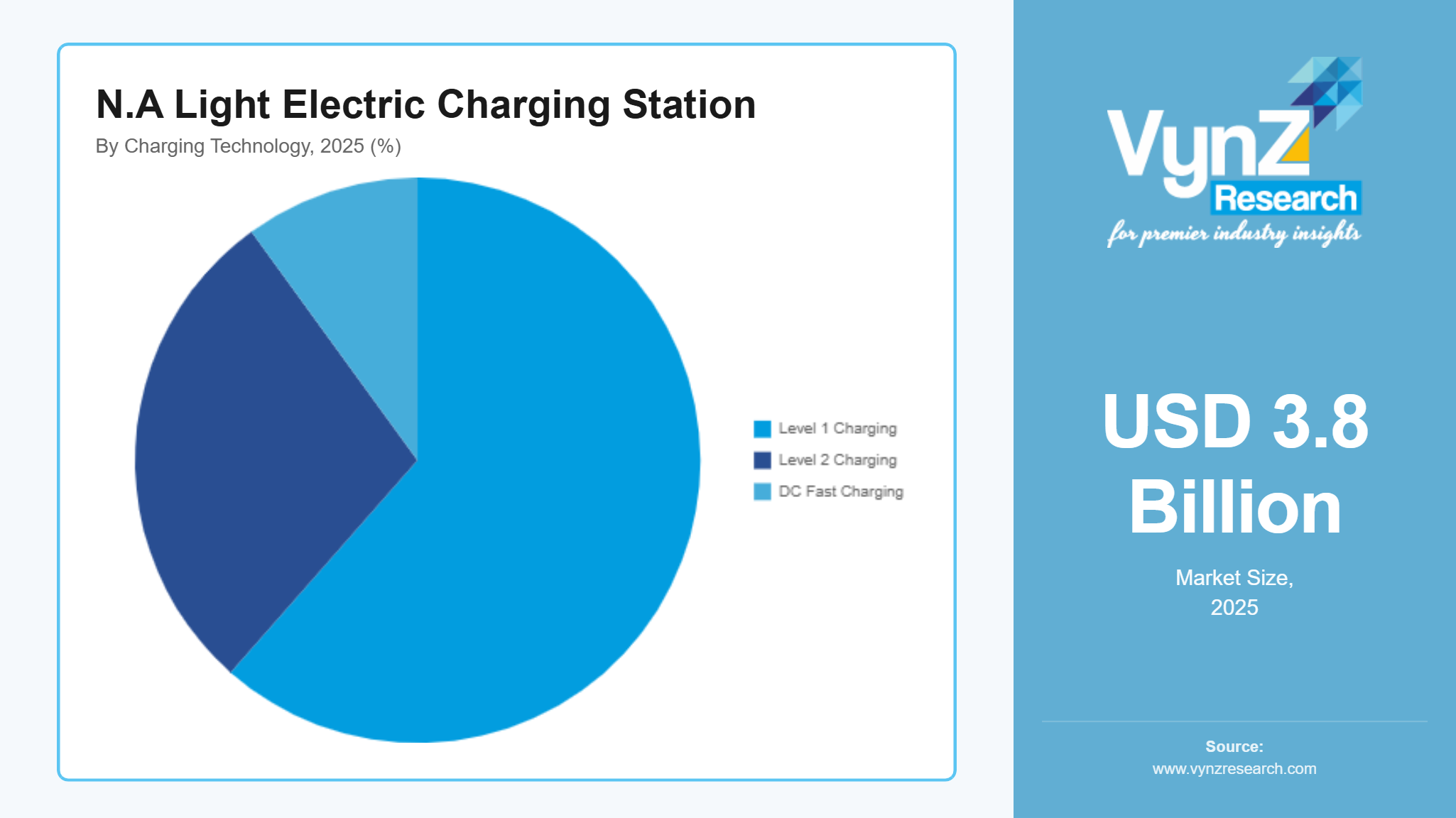

- Level 2 charging accounted for 61.5% share in 2025, supported by broad residential and commercial deployment.

- Individual consumers held 51.4% market share in 2025, owing to rising light electric vehicle ownership.

- Commercial applications are expected to witness the fastest growth at 16.4% CAGR supported by the increasing charging installations.

- The United States represented 5.9% market share in 2025, driven by federal funding and widespread EV adoption.

Market growth is supported by expanding light electric vehicle adoption, supportive public funding for charging infrastructure and rapid advancements in smart charging technologies along with increasing deployment of connected charging solutions. Growing demand for convenient urban and commercial charging facilities and continued investments under the U.S. Department of Energy, the U.S. Joint Office of Energy and Transportation and Natural Resources Canada are further supporting industry expansion across major markets including California, Texas, and Ontario.

North America Light Electric Charging Station Market Dynamics

Market Trends

The industry is witnessing notable shifts in smart charging technologies, digital connectivity and urban mobility infrastructure. One of the key trends shaping the market is the deployment of networked and interoperable charging stations reflecting growing demand for efficient energy management, remote monitoring and improved user convenience. The U.S. Department of Energy continues to support interoperability and charging reliability through national infrastructure initiatives while Natural Resources Canada promotes expanded charging accessibility to accelerate electric mobility. Another emerging trend is the integration of renewable energy and energy storage with charging networks, driven by clean transportation policies and grid modernization efforts. The National Renewable Energy Laboratory (NREL) and the U.S. Department of Energy continue to publish research supporting smart charging and grid integration.

Growth Drivers

The growth of the market is largely supported by increasing adoption of light electric vehicles which continues to generate sustained demand across urban transportation, commercial fleets and shared mobility applications. Rising investments in public charging infrastructure through programs led by the U.S. Department of Energy, the Federal Highway Administration and Natural Resources Canada are further accelerating market expansion. Additionally, supportive government incentives and emissions reduction policies are playing a crucial role in boosting adoption. As consumers, businesses and municipalities prioritize energy efficiency and sustainable transportation, demand for advanced charging infrastructure is expected to remain strong throughout the forecast period.

Market Restraints / Challenges

Despite favorable growth prospects, the market faces certain challenges that may limit its expansion. High installation costs and grid upgrade requirements continue to affect profitability and deployment particularly among smaller operators and rural communities. Furthermore, approval complexity and dependence on critical electrical equipment pose operational challenges for charging station developers and suppliers. Reliance on imported components and extended procurement timelines can increase project costs and delay installations during periods of supply chain disruption. The U.S. Government Accountability Office (GAO) has highlighted permitting, supply chain and infrastructure coordination as important implementation challenges.

Market Opportunities

The market presents significant opportunities in fast charging infrastructure particularly driven by expanding electric vehicle ownership and supportive transportation policies. Companies offering scalable, high performance and digitally connected charging solutions are well positioned to capture increasing demand from municipalities, commercial operators and workplace charging projects. The Joint Office of Energy and Transportation continues to support nationwide deployment of reliable charging infrastructure. Another key opportunity lies in integrating charging stations with renewable energy and smart grid technologies where growing investments in intelligent energy management are creating avenues for higher operational efficiency and long-term customer relationships. Advancements supported by the National Renewable Energy Laboratory (NREL) and the U.S. Department of Energy are expected to improve charging efficiency, grid flexibility and customer experience across the region.

North America Light Electric Charging Station Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 3.8 Billion |

|

Revenue Forecast in 2035 |

USD 16.4 Billion |

|

Growth Rate |

15.4% |

|

Segments Covered in the Report |

By Charging Station Type, By Charging Technology, By Application, By End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

United States, Canada, Mexico, Rest of North America |

|

Key Companies |

ABB Ltd., Blink Charging Co., ChargePoint Holdings Inc., Eaton Corporation plc, EV Connect Inc., FLO Services USA Inc., FreeWire Technologies Inc., Schneider Electric SE, Siemens AG, Tesla Inc. |

|

Customization |

Available upon request |

North America Light Electric Charging Station Market Segmentation

By Charging Station Type

Public charging stations accounted for the largest market share of approximately 56.8% in 2025 and are projected to expand at an estimated 15.7% CAGR through 2035. Their leadership is supported by increasing deployment across highways, urban centers, retail complexes, workplaces and public parking facilities, where accessibility remains essential for expanding electric mobility.

Private charging stations are expected to register the fastest growth, advancing at an estimated 16.2% CAGR during the forecast period due to growing ownership of light electric vehicles, increasing installation of residential charging equipment and growing workplace charging initiatives continue to support demand.

By Charging Technology

Level 2 charging held the largest market share of approximately 61.5% in 2025 and is expected to grow at an estimated 15.3% CAGR through 2035 due to its widespread adoption across residential properties, commercial facilities, workplaces and public destinations is supported by balanced charging speed, relatively lower installation costs and broad compatibility with passenger electric vehicles.

DC Fast Charging is projected to record the highest growth, expanding at an estimated 17.1% CAGR during the forecast period owing to increasing demand for rapid charging, fleet electrification and long-distance travel infrastructure is accelerating investments across major transportation corridors and urban charging hubs.

By Application

Public infrastructure accounted for the largest market share of approximately 45.9% in 2025 and is anticipated to expand at nearly 15.8% CAGR through 2035 because of strong government investments, increasing electric vehicle registrations and expansion of charging corridors continue to strengthen this segment.

Commercial applications are expected to witness the fastest growth, advancing at an estimated 16.4% CAGR during the forecast period supported by the increasing charging installations across retail centers, office buildings, hospitality facilities, fleet depots and mixed-use developments continue to support expansion.

By End User

Individual consumers accounted for the largest market share of approximately 51.4% in 2025 and are expected to grow at an estimated 15.4% CAGR through 2035 due to growing consumer adoption of electric vehicles, supportive purchase incentives and expanding residential charging infrastructure continue to strengthen demand.

Commercial fleet operators are projected to register the fastest growth, recording an estimated 16.6% CAGR during the forecast period supported by fleet electrification initiatives, operational cost optimization and corporate emissions reduction strategies are driving investment in dedicated charging infrastructure.

Regional Insights

United States

The United States accounted for approximately 59% of the market in 2025 supported by rapid electric vehicle adoption, expanding public charging infrastructure and sustained federal investments. Strong demand across California, Texas, Florida and New York continues to strengthen market expansion as public agencies and private operators accelerate charging network deployment. The U.S. Department of Energy and the Joint Office of Energy and Transportation continue to support nationwide charging infrastructure through the National Electric Vehicle Infrastructure program while the Federal Highway Administration promotes charging corridor development across interstate highways.

Canada

Canada accounted for approximately 16% of the regional market in 2025 and is expected to expand at an estimated 15.8% CAGR through 2035 supported by increasing electric vehicle ownership, national decarbonization policies and continued deployment of charging infrastructure across urban and highway networks. The Government of Canada and Natural Resources Canada continue investing in public charging stations through the Zero Emission Vehicle Infrastructure Program, strengthening nationwide charging accessibility.

Mexico

Mexico held nearly 5% of the market in 2025 and is projected to register an estimated 16.1% CAGR during the forecast period due to expanding urban infrastructure, increasing electric mobility investments, and gradual development of public charging networks. The Secretariat of Energy (SENER) continues to support clean energy transition policies, while the Federal Electricity Commission (CFE) is strengthening charging infrastructure and grid readiness through national energy initiatives. Increasing private sector investments, adoption of electric passenger vehicles and charging installations across commercial facilities continue to support sustained market growth, particularly in major metropolitan areas and industrial corridors.

Rest of North America

The Rest of North America accounted for approximately 20% of the regional market in 2025 and is expected to grow at an estimated 15.2% CAGR through 2035 supported by increasing investments in sustainable transportation infrastructure, gradual adoption of light electric vehicles and government initiatives promoting clean mobility solutions. Regional authorities are encouraging the deployment of public charging stations to improve accessibility and support low emission transportation goals.

Competitive Landscape / Company Insights

The market is moderately competitive with global and regional companies emphasizing charging technology innovation, network expansion, software integration and strategic partnerships to strengthen their market position. Companies are increasingly investing in smart charging platforms, fast charging infrastructure and interoperable solutions to improve reliability and user experience. The U.S. Department of Energy, the Joint Office of Energy and Transportation, and the National Renewable Energy Laboratory (NREL) continue to support industry development through research, infrastructure programs and technical standards that encourage wider deployment of advanced charging networks.

Mini Profiles

ABB Ltd. focuses on smart EV charging solutions, DC fast chargers, and energy management technologies, supported by strong engineering expertise, an extensive regional presence, and continuous investments in charging infrastructure innovation.

Blink Charging Co. operates in the public and commercial charging segments, emphasizing network expansion, flexible charging solutions, and cloud-based management platforms to strengthen customer engagement across North America.

ChargePoint Holdings Inc. leverages an extensive charging network, digital software platforms, and strategic partnerships to expand market presence, enabling scalable charging solutions for residential, commercial, and fleet applications.

Eaton Corporation plc specializes in power management and electric vehicle charging infrastructure, supported by advanced electrical technologies, grid integration capabilities, and a well-established industrial distribution network.

FreeWire Technologies Inc. develops battery integrated charging systems that improve deployment flexibility, reduce installation complexity, and support fast charging applications across commercial locations and transportation networks.

Key Players

- ABB Ltd.

- Blink Charging Co.

- ChargePoint Holdings Inc.

- Eaton Corporation plc

- EV Connect Inc.

- FLO Services USA Inc.

- FreeWire

- Technologies Inc.

- Schneider Electric SE

- Siemens AG

- Tesla Inc.

Recent Developments

In January 2025, Siemens AG expanded its electric vehicle charging portfolio with enhanced charging infrastructure and digital energy management capabilities for commercial applications. The initiative strengthened support for scalable, grid integrated charging solutions across North America.

In May 2025, Tesla Inc. continued expanding its Supercharger network across North America while opening additional charging locations to a wider range of electric vehicle brands through NACS adoption. The expansion improved charging accessibility and accelerated interoperability across the regional charging ecosystem.

In May 2025, Schneider Electric SE expanded collaborations to accelerate EV charging infrastructure deployment by integrating smart energy management with charging solutions. The strategy focused on improving energy efficiency and supporting commercial electrification projects.

In February 2026, EV Connect Inc. strengthened its charging management platform with new software capabilities designed to improve charger reliability, network visibility, and fleet charging operations. The enhancements supported increasing demand for connected charging infrastructure across commercial locations.

In March 2026, FLO Services USA Inc. expanded its fast-charging network across North America by deploying additional public charging stations and strengthening partnerships with site hosts. The expansion aimed to improve charging accessibility and support growing electric vehicle adoption across the region.

North America Light Electric Charging Station Market Coverage

Charging Station Type Insight and Forecast 2026 - 2035

- Public Charging Stations

- Private Charging Stations

Charging Technology Insight and Forecast 2026 - 2035

- Level 1 Charging

- Level 2 Charging

- DC Fast Charging

Application Insight and Forecast 2026 - 2035

- Residential

- Commercial

- Public Infrastructure

End User Insight and Forecast 2026 - 2035

- Individual Consumers

- Commercial Fleet Operators

- Government Organizations

- Others

North America Light Electric Charging Station Market by Region

- U.S.

- By Charging Station Type

- By Charging Technology

- By Application

- By End User

- Canada

- By Charging Station Type

- By Charging Technology

- By Application

- By End User

- Mexico

- By Charging Station Type

- By Charging Technology

- By Application

- By End User

Table of Contents for North America Light Electric Charging Station Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Charging Station Type

1.2.2. By

Charging Technology

1.2.3. By

Application

1.2.4. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. North Market Estimate and Forecast

4.1. North Market Overview

4.2. North Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Charging Station Type

5.1.1. Public Charging Stations

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Private Charging Stations

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.2. By Charging Technology

5.2.1. Level 1 Charging

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Level 2 Charging

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. DC Fast Charging

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By Application

5.3.1. Residential

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Commercial

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Public Infrastructure

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.4. By End User

5.4.1. Individual Consumers

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Commercial Fleet Operators

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Government Organizations

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Others

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

6. U.S. Market Estimate and Forecast

6.1. By

Charging Station Type

6.2. By

Charging Technology

6.3. By

Application

6.4. By

End User

7. Canada Market Estimate and Forecast

7.1. By

Charging Station Type

7.2. By

Charging Technology

7.3. By

Application

7.4. By

End User

8. Mexico Market Estimate and Forecast

8.1. By

Charging Station Type

8.2. By

Charging Technology

8.3. By

Application

8.4. By

End User

9. Company Profiles

9.1.

ABB Ltd.

9.1.1.

Snapshot

9.1.2.

Overview

9.1.3.

Offerings

9.1.4.

Financial

Insight

9.1.5.

Recent

Developments

9.2.

Blink Charging Co.

9.2.1.

Snapshot

9.2.2.

Overview

9.2.3.

Offerings

9.2.4.

Financial

Insight

9.2.5.

Recent

Developments

9.3.

ChargePoint Holdings Inc.

9.3.1.

Snapshot

9.3.2.

Overview

9.3.3.

Offerings

9.3.4.

Financial

Insight

9.3.5.

Recent

Developments

9.4.

Eaton Corporation plc

9.4.1.

Snapshot

9.4.2.

Overview

9.4.3.

Offerings

9.4.4.

Financial

Insight

9.4.5.

Recent

Developments

9.5.

EV Connect Inc.

9.5.1.

Snapshot

9.5.2.

Overview

9.5.3.

Offerings

9.5.4.

Financial

Insight

9.5.5.

Recent

Developments

9.6.

FLO Services USA Inc.

9.6.1.

Snapshot

9.6.2.

Overview

9.6.3.

Offerings

9.6.4.

Financial

Insight

9.6.5.

Recent

Developments

9.7.

FreeWire Technologies Inc.

9.7.1.

Snapshot

9.7.2.

Overview

9.7.3.

Offerings

9.7.4.

Financial

Insight

9.7.5.

Recent

Developments

9.8.

Schneider Electric SE

9.8.1.

Snapshot

9.8.2.

Overview

9.8.3.

Offerings

9.8.4.

Financial

Insight

9.8.5.

Recent

Developments

9.9.

Siemens AG

9.9.1.

Snapshot

9.9.2.

Overview

9.9.3.

Offerings

9.9.4.

Financial

Insight

9.9.5.

Recent

Developments

9.10.

Tesla Inc.

9.10.1.

Snapshot

9.10.2.

Overview

9.10.3.

Offerings

9.10.4.

Financial

Insight

9.10.5.

Recent

Developments

10. Appendix

10.1. Exchange Rates

10.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

North America Light Electric Charging Station Market