Shipping Containers Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Container Type (Dry Storage Containers, Refrigerated Containers (Reefer), Tank Containers, Special Containers), by Size (Small Containers (Up to 20 Feet), Large Containers (Above 20 Feet / 40 Feet & High Cube)), by End-Use Industry (Consumer Goods, Food & Beverages, Chemicals, Pharmaceuticals, Industrial Products), by Material (Steel Containers, Aluminum Containers, Fiber-Reinforced/Composite), by Application (Sea Transport, Rail Transport, Road Transport, Intermodal Transport), by Ownership (Shipper-Owned Containers (SOC), Carrier-Owned Containers (COC), Leasing Containers)

| Status : Published | Published On : Apr, 2026 | Report Code : VRAT9671 | Industry : Automotive & Transportation | Available Format :

|

Page : 210 |

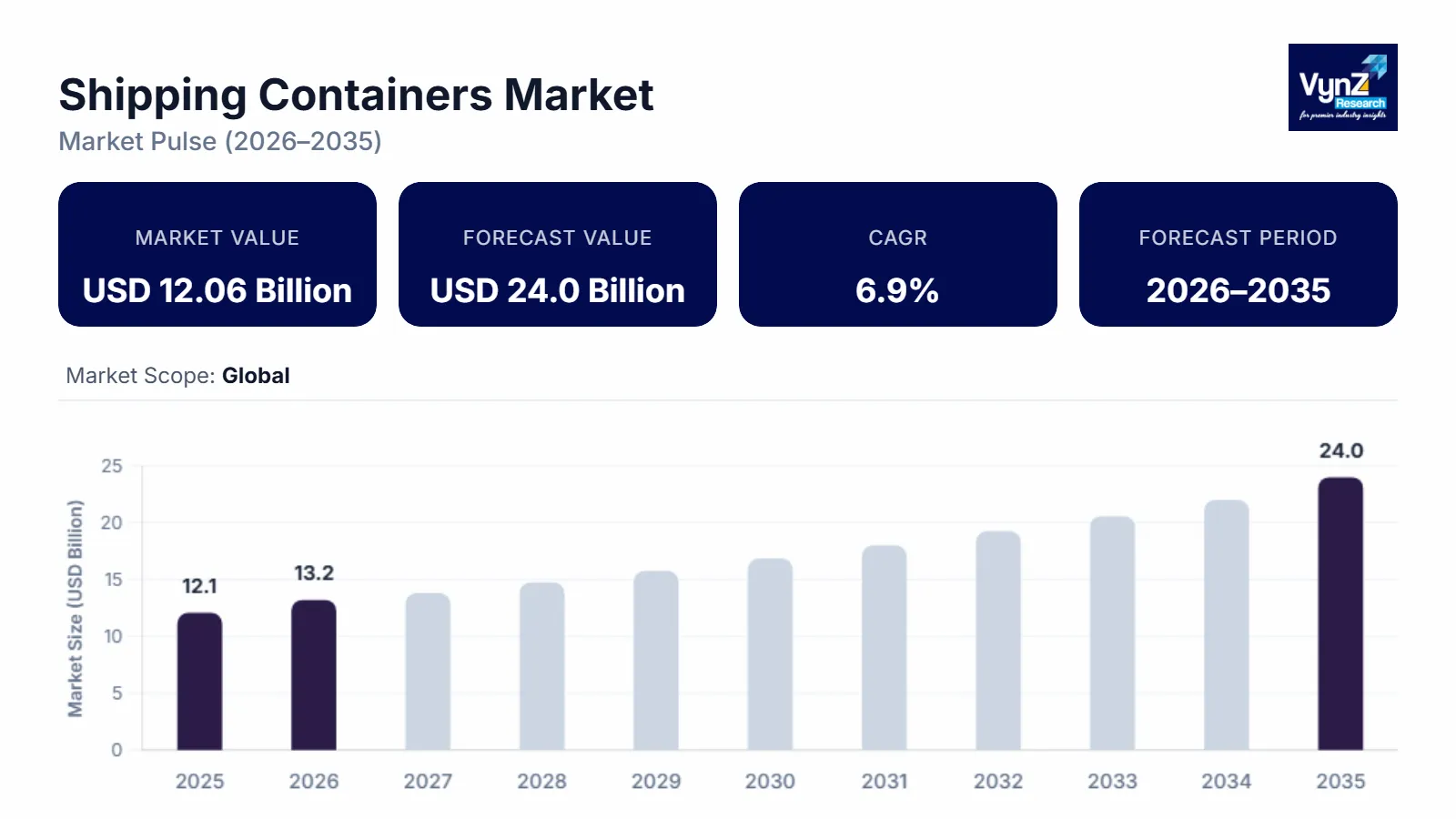

Shipping Containers Market Overview

The shipping containers market, which was valued at approximately USD 12.06 billion in 2025 and is estimated to reach around USD 13.2 billion in 2026, is projected to reach close to USD 24.0 billion by 2035, expanding at a CAGR of about 6.9% during the forecast period from 2026 to 2035.

The shipping containers industry has a number of key drivers, which include sustained levels of containerised trade, with increasing numbers of shipments being carried by sea and now moving by road and rail on standardised containers. As manufacturers continue to export their products into new markets and e-commerce continues to expand its supply chain capabilities, there will be an ongoing requirement for shipping lines, freight forwarders, ports, and inland distributors to have access to sufficient numbers of containers to meet the needs of customers and shippers.

Replacement demand for used containers is another driver. As containers reach the end of their useful life, they will require repair, refurbishment, or disposal. This creates a recurring procurement cycle for shipping lines, leasing companies, and cargo owners who utilise this type of equipment. Increasing demand from refrigerated (reefer) containers due to rising cold chain requirements for food imports, exports, and pharmaceutical logistics, as well as tank containers for the transportation of chemicals and other liquid cargo requiring ISO compliant equipment, are additional drivers for growth..

Shipping Containers Market Dynamics

Market Trends

IoT and real-time tracking technology is transforming the shipping container industry by providing an opportunity for increased control and efficiency at each point along the global supply chain using increased levels of visibility. Real-time monitoring allows the use of IoT-enabled shipping containers to collect data on important factors, including temperature, humidity, vibration, and security conditions, which provides the ability for all parties involved with the shipment to continuously track the shipment during its travel. Continuous shipment tracking enables logistics companies and shippers to reduce loss, prevent damage to cargo, and provide prompt responses to shipment disruptions and delays. Real-time data analytics enable predictive maintenance and routing, resulting in lower operational costs and improved delivery times. The European Union has also provided significant funding to support smart ports and digital freight corridors in Europe, totalling over €80+ billion through programmes such as Horizon Europe and Connecting Europe Facility (CEF) that include real-time tracking systems for containers using IoT. The increasing number of high value and temperature sensitive goods shipped globally, such as pharmaceuticals and perishable food products, will continue to drive growth in this area due to the need for ensuring that quality and safety standards are maintained.

Growth Drivers

The increasing number of e-commerce transactions and cross-border trading is resulting in an increase in demand in the shipping containers market, as both transactions and purchases made through e-retailers grow globally. The proliferation of digital commerce platforms (DCPs) has increased the need for companies that ship products to provide scalable, reliable, and efficient shipping options to meet the growing demands of DCPs and their customers. In response to consumer expectations for faster delivery times and broader product offerings, logistics providers are being pushed to maximise container utilisation rates and optimise transportation networks. Funding institutions such as the World Bank have also provided approximately USD 2 billion to support the development of dedicated freight corridors (DFCs) and the enhancement of logistics infrastructure, which will improve the efficiency of cargo movement and enable higher volumes of trade to flow. Furthermore, the implementation of international trade agreements (ITAs) and the globalisation of supply chains (GSCS) has further driven container movement between manufacturing hubs and consumption markets. These increases in trade activity have generated additional demand for standardised containers, fleet capacity increases, and enhanced logistics infrastructure.

Market Restraints / Challenges

Key challenges in the shipping container industry consist of vulnerability to worldwide commodity cycles and the volatile nature of freight prices. Volatility in freight prices may influence demand for new containers, use levels of existing units, and income from leasing these units. These factors can be influenced by price volatility in raw materials such as steel used to manufacture these products. Additionally, changes in production capacity can rapidly create a surplus or shortage in this product category. Furthermore, the cost of moving empty containers from one lane to another, combined with local area shortages due to equipment imbalances on trade routes, can further limit the ability to meet customer needs. Collectively, these factors can create variability in pricing, lead times, and profitability across the container manufacturing, leasing, and trading value chain.

Market Opportunities

The shipping containers market offers significant opportunities in specialty equipment, container leasing and fleet management services, and digital solutions that improve tracking, condition monitoring, and utilisation. As global supply chains prioritise resilience and visibility, there is growing interest in smart-container capabilities that support real-time location, door events, and temperature or shock monitoring where needed. In India, under the PM Gati Shakti National Master Plan, the government has outlined over USD 1.2 trillion in infrastructure investments, including multimodal logistics parks, inland container depots, and digital freight systems that directly support container utilisation, tracking technologies, and intermodal expansion. Another opportunity lies in container lifecycle services, inspection, repair, refurbishment, and resale, which can extend asset life and improve total cost of ownership for carriers, leasing companies, and shippers. In addition, rising infrastructure investment in ports, terminals, and inland intermodal hubs in emerging markets can increase demand for standardised container equipment and related services.

Global Shipping Containers Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 12.06 Billion |

|

Revenue Forecast in 2035 |

USD 24.0 Billion |

|

Growth Rate |

6.9% |

|

Segments Covered in the Report |

Container Type, Size, End-Use Industry, Material, Application, Ownership |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia-Pacific, Latin America, Middle East & Africa |

|

Key Companies |

China International Marine Containers (Group) Co., Ltd. (CIMC), Dong Fang International Container (DFIC), CXIC Group Containers Co., Ltd., Singamas Container Holdings Limited, Maersk Container Industry A/S (MCI), Triton International Limited, Textainer Group Holdings Limited, Florens Container Services, Touax Group, Sea Box, Inc. |

|

Customization |

Available upon request |

Shipping Containers Market Segmentation

By Container Type

Dry storage containers are the largest category, with a market share of about 55% in 2025. This dominance can be attributed to their universal application for general cargo transportation on major sea-based and intermodal routes around the world. As a result, they are the predominant type of equipment used for transporting consumer goods, industrial products, and other packaged commodities. They also support repetitive demand from the need to replace or lease new build containers, as well as those being leased or purchased. In addition, due to their ability to operate flexibly, be standardised globally, and functionally compatible with terminal, railroad, and truck-based freight movements, this segment will continue to dominate trade lanes.

Refrigerated containers are the fastest growing category, with a CAGR of 7.2% during the forecast period, because there is an expanding requirement for cold chain logistics for the transportation of food products and pharmaceuticals. The demand for this product will grow as a result of increased global trade of perishable items, increased strictness in regards to quality standards, and an increased amount of reefer equipment being utilised in both marine and land-based intermodal distribution.

By Size

Large containers are the larger category, with a market share of about 65% in 2025, as there were significant transportation economies of scale for large volumes of cargo, and they were also used extensively on major ocean shipping lanes and inland intermodal routes. Both the 40 foot and high cube formats have been widely adopted to optimise the unit cost of logistics for most consumer and industrial products, thereby sustaining demand from both new equipment purchases and lease fleets. Also, the extensive use of common handling infrastructure developed around the large standard size of these formats will support their ongoing high usage rates and repetitive replacement cycle.

Small containers are the faster growing category during the forecast period, because of customer needs for flexible options for shipping smaller amounts on shorter hauls or for improving a shipper's ability to manage their payload within government mandated road weight limitations. Additionally, small containers can better accommodate a shipper's need to move smaller volumes of freight over some trade lanes. In addition, 20 foot containers are gaining acceptance for heavy freight, as the limiting factor is often weight versus volume for such commodity types and industrial shipments.

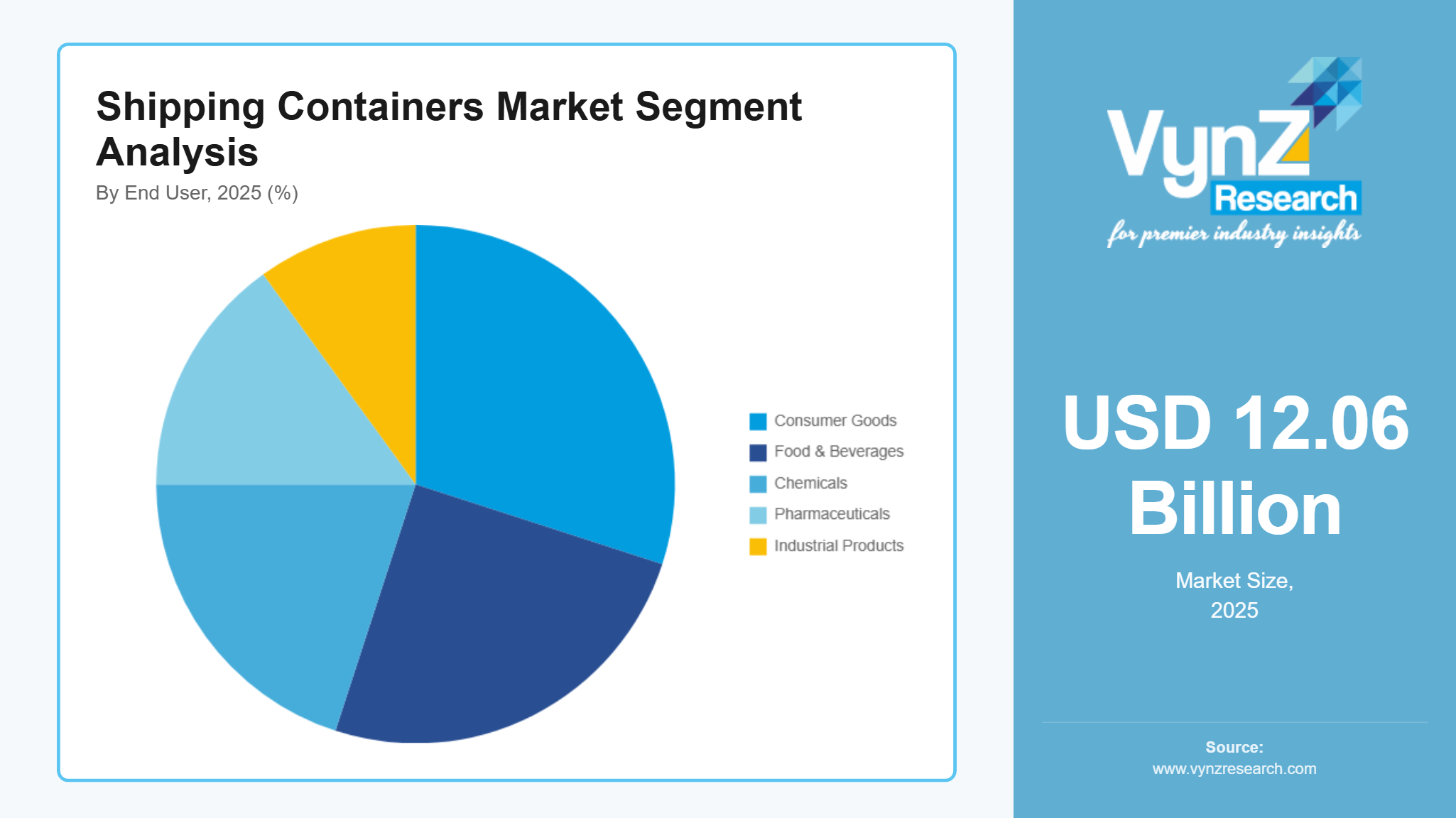

By End Use Industry

Consumer goods are the largest category, with a market share of about 30% in 2025, as containerised cargo for manufactured goods throughout the world. Additionally, high volume containerised shipments of manufactured product are moving through global ocean freight and inland distribution networks. As a result, dry storage containers are commonly utilised to ship packaged retail goods, electronics, household products, and finished goods. This results in recurring equipment usage from both carrier owned and leased fleets. The large scale of this commodity is reflective of the importance that containerisation plays in facilitating global merchandise commerce and the supply chain requirements of an omnichannel.

Pharmaceuticals are the fastest growing category, with a CAGR of 7.4% during the forecast period, as there is greater demand from both the medical industry and regulatory agencies for more secure and reliable cold chain transportation and storage methods for medications, vaccines, and other high value health care products being transported across international borders. The pharmaceutical market will see additional growth due to increased use of refrigerated shipping containers, enhanced regulations governing the safe handling of perishable items, and better technology such as electronic monitoring systems.

By Material

Steel containers are the largest category, with a market share of about 70% in 2025, primarily because of the large scale adoption of Corten steel and other steel grades, which are strong, durable, relatively inexpensive to manufacture, and can be built to ISO standards for standard equipment. Due to their ability to provide structural performance, maintainability, repairability, and an already well established global production chain, steel will remain the dominant material used for dry storage containers and most specialty containers. As a result of the existing inventory of steel containers throughout the world and ongoing maintenance requirements to replace those containers at end of life, steel's position as the leading container type worldwide is expected to remain unchanged.

Fibre-reinforced composite is the fastest growing category, with a CAGR of 7.7% during the forecast period, due to the selective use of composites in applications that offer the opportunity to reduce life cycle costs through reduced weight, reduced corrosion, and improved thermal performance. Composites represent a small percentage of the total fleet when compared to steel. However, there has been growing interest in niche applications such as specialised logistics and highly corrosive environments.

By Application

Sea transport is the largest category, with a market share of about 65% in 2025, because the primary function for which ISO containers were developed was to be used on ships at sea, and they are the basis upon which ocean freight shipments take place. Because of high volumes of sea-borne commerce, extensive network coverage of liner shipping companies that provide regular cargo service from one port to another, and the presence of many large ports and significant transshipment points, there is a very strong demand for both standard and specialised types of containers for use in marine applications. The inland segment of transportation provides the secondary function by providing final delivery of goods.

Intermodal transport is the fastest growing category during the forecast period, as the goal for all parties involved is to increase end to end logistics efficiencies through the combination of movement of goods by sea, rail, and highway into one standard shipping unit. Increased use of inland container terminals and rail intermodal service, along with development of distribution centres and regional distribution networks, has increased container usage from just being moved from one port to another.

By Ownership

Leasing containers is the largest category, with a market share of about 45% in 2025, largely due to the prevalent use of operating leasing contracts, which allow shipping companies and logistics companies to have better flexibility to plan their routes, replace their equipment, and size their fleets. The large lessors will have diversified global fleets along with depot locations, which will enable them to manage their container availability, relocate, and offer life cycle services. Additionally, they are able to fund new equipment purchases and provide containers throughout various economic cycles, thus providing significant volumes of revenue on an ongoing basis.

Shipper-owned containers (SOC) is the fastest growing category during the forecast period, as some cargo owners and freight forwarders increase ownership to improve equipment availability and control costs on select trade lanes and for specialised requirements. SOC usage can be attractive where shipper-specific positioning, dedicated equipment, or supply assurance is prioritised. Carrier-owned containers (COC) remain an important portion of the installed base for many liner operators, while SOC growth is expected to be stronger as adoption broadens among larger shippers and logistics intermediaries.

Regional Insights

North America

North America represents one of the largest regional markets for shipping containers, thanks to strong imports, well developed intermodal rail networks, and large distribution systems relying on containerised cargo flow. Due to both its massive consumer market and large volume of container traffic at major West Coast, Gulf Coast, and East Coast ports, the United States accounts for the majority of this regional demand for container equipment, depot services, and repositioning. As an example, over the last few years the federal government has provided nearly USD 500 million of funding through programmes such as the Port Infrastructure Development Program (PIDP) to modernise port capabilities, increase cargo handling efficiencies, and improve intermodal connections. Additionally, under various infrastructure and climate related funding initiatives, the US federal government has committed approximately USD 3 billion to update port infrastructure, improve container vessel turnaround times, and implement advanced technology and equipment at seaports throughout the country. The numerous inland logistics linkages available to users within North America, such as extensive rail based intermodal corridors and substantial warehouse capacities, contribute significantly to facilitating the movement of containers beyond seaport terminals and promote continued usage of dry and specialty containers. Trade with both Asia and Europe are also key factors driving regional demand for shipping containers.

Asia-Pacific

Asia-Pacific is the largest region, with a market share of about 45% in 2025, and it is also the fastest growing region during the forecast period, due to its established position as the world’s leading container production area and a central point for exporting and importing via containers. The PRC has become the dominant manufacturer of standard dry containers and other speciality containers, as well as the most substantial manufacturing base and supply chain for steel and components. A number of Indian maritime investment commitments are valued above USD 135 billion, of which a majority are intended to develop ports, container terminals, and digital logistics systems to manage increasing import and export volumes. Container movement volume through some of China’s major ports, as well as those in Southeast Asia and Northeast Asia, will sustain high levels of demand for repositioning, depot service, and equipment supply. An increase in regional intra-Asia trade will likewise increase the amount of regional container flow. Government backed investments in port and logistics infrastructure will total over USD 100 billion in China alone through large scale BRI projects, including additional construction on container ports and expansion into global trade connectivity. Growth within this region will additionally be fuelled by continued investment in port, terminal, and inland logistics infrastructure.

Europe

Europe is a significant player in the shipping containers industry because of high volumes of imports and exports, an extensive web of seaports, and highly developed railway and inland waterway systems to facilitate intermodal movement of containerised freight. In accordance with these factors, the EU has made substantial investments of €6.2 billion on over 100 transportation related projects, including many related to container handling facilities and upgrade of inland waterway container logistics. Further, the European Investment Bank will continue to provide funding for additional port projects; it recently provided a €90 million loan to the Port of Rotterdam to electrify its container terminals and enhance the infrastructure of those facilities. The EIB also awarded a grant totalling €70 million to the Port of Rotterdam to fund efficient container processing and sustainable operations. Other key ports like Rotterdam, Antwerp-Bruges, Hamburg, and other main Mediterranean ports have driven constant container traffic, thus driving continuous demand for the maintenance and operation of containerised cargo through various modes of trade.

Rest of the World

Rest of the world, including Latin America and Middle East and Africa, is witnessing steady growth in shipping container demand as international trade in agricultural commodities, consumer goods, and manufacturing products grows and port and logistics service improvements continue in targeted markets. The growth in international container traffic across both Atlantic and Pacific routes supports strong demand for standard dry containers, and where there is an abundance of exports from the region, such as produce, refrigerated containers will also be needed. Major transshipment ports in the Middle East, and the increasing trade volumes flowing through them, support the demand for available containers for shipment into other countries and regions, while equipment availability, depot services, and cost-effective relocation of containers will be increasingly important. For certain areas within Africa, demand is influenced by developing port capabilities, high dependency on imported manufactured goods, and growing production of agricultural commodities, which could lead to higher demand for reefers on specific routes. In addition, African governments have identified annual infrastructure gaps estimated at approximately USD 170 billion and are making substantial investments in the modernisation of ports, container handling facilities, and trade corridors.

Competitive Landscape / Company Insights

Manufacturing has a high degree of concentration among the world’s top manufacturers. In terms of manufacturing, most new ISO containers are supplied from a limited number of major players that are almost all located in China. These firms are able to leverage their economies of scale and produce standard containers using a common base of raw materials, steel, and components. Certification procedures, combined with existing relationships with the largest shipping lines and the majority of the world’s largest leasing companies, contribute to this level of concentration. However, there exists a diverse array of participants throughout the broader downstream ecosystem surrounding container manufacturing, including leasing companies, traders, and networks of depots and repair facilities. Compared to manufacturing, container leasing is slightly more fragmented and, while still dominated by a handful of large lessor based fleets, these fleets have grown significantly in size and expanded their geographic presence. Thus, they can support new equipment purchases by financing those purchases and continue to supply carriers with either long term or short term leases.

In contrast, other types of participants in the value chain are competing with one another through differentiation in areas such as reefers, tanks, offshore containers, modifying existing containers for specific uses, and developing digital solutions to track and manage usage. Additionally, companies are providing greater availability of specialty containers designed to meet the needs of customers engaged in cold chain logistics and chemical logistics, while also delivering services related to inspecting, repairing, refurbishing, and reselling used containers to maximise asset life.

Mini Profiles

China International Marine Containers (Group) Co., Ltd. (CIMC) is a global container manufacturing company producing standard dry containers as well as a range of specialty containers and related logistics equipment.

Triton International Limited is a global container leasing company with a large fleet that supports shipping lines and logistics operators through leasing and related equipment services.

Textainer Group Holdings Limited is a container leasing company providing standard and specialized containers to shipping lines and other customers, supported by global depot and service networks.

CXIC Group Containers Co., Ltd. is a container manufacturer producing ISO-standard containers, including dry containers and specialty units such as tanks and customized equipment.

Singamas Container Holdings Limited is a container manufacturing company known for producing standard and specialized shipping containers for global customers.

Key Players

- China International Marine Containers (Group) Co., Ltd. (CIMC)

- Dong Fang International Container (DFIC)

- CXIC Group Containers Co., Ltd.

- Singamas Container Holdings Limited

- Maersk Container Industry A/S (MCI)

- Triton International Limited

- Textainer Group Holdings Limited

- Florens Container Services

- Touax Group

- Sea Box, Inc.

Recent Developments

December 2025 – China International Marine Containers (Group) Co., Ltd. (CIMC) reported plans to invest approximately CNY 3 billion to build a new container manufacturing plant in Yinzhou, Ningbo, China, adding capacity for ISO container production.

December 2025 – Textainer Group Holdings Limited announced it had completed the acquisition of Seaco, expanding its intermodal container leasing platform and global fleet scale.

June 2025 – Maersk Container Industry (MCI) highlighted continued uptake of its upgraded Star Cool 1.1 reefer technology, including deliveries of tens of thousands of units since launch and availability of ultra-low GWP refrigerant options (including R1234yf) designed to meet relevant safety requirements for thermal containers.

May 2025 – Textainer Group Holdings Limited announced an agreement to acquire Seaco, signalling continued consolidation activity in the container leasing segment.

May 2025 – Florens International Limited announced a change in its Board leadership, appointing a new Director and Chairman, reflecting ongoing governance and operational strengthening among major container leasing platforms.

Global Shipping Containers Market Coverage

Container Type Insight and Forecast 2026 - 2035

- Dry Storage Containers

- Refrigerated Containers (Reefer)

- Tank Containers

- Special Containers

Size Insight and Forecast 2026 - 2035

- Small Containers (Up to 20 Feet)

- Large Containers (Above 20 Feet / 40 Feet & High Cube)

End-Use Industry Insight and Forecast 2026 - 2035

- Consumer Goods

- Food & Beverages

- Chemicals

- Pharmaceuticals

- Industrial Products

Material Insight and Forecast 2026 - 2035

- Steel Containers

- Aluminum Containers

- Fiber-Reinforced/Composite

Application Insight and Forecast 2026 - 2035

- Sea Transport

- Rail Transport

- Road Transport

- Intermodal Transport

Ownership Insight and Forecast 2026 - 2035

- Shipper-Owned Containers (SOC)

- Carrier-Owned Containers (COC)

- Leasing Containers

Global Shipping Containers Market by Region

- North America

- By Container Type

- By Size

- By End-Use Industry

- By Material

- By Application

- By Ownership

- By Country - U.S., Canada, Mexico

- Europe

- By Container Type

- By Size

- By End-Use Industry

- By Material

- By Application

- By Ownership

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Container Type

- By Size

- By End-Use Industry

- By Material

- By Application

- By Ownership

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Container Type

- By Size

- By End-Use Industry

- By Material

- By Application

- By Ownership

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Shipping Containers Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Container Type

1.2.2. By

Size

1.2.3. By

End-Use Industry

1.2.4. By

Material

1.2.5. By

Application

1.2.6. By

Ownership

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Container Type

5.1.1. Dry Storage Containers

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Refrigerated Containers (Reefer)

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Tank Containers

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Special Containers

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.2. By Size

5.2.1. Small Containers (Up to 20 Feet)

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Large Containers (Above 20 Feet / 40 Feet & High Cube)

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By End-Use Industry

5.3.1. Consumer Goods

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Food & Beverages

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Chemicals

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Pharmaceuticals

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Industrial Products

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.4. By Material

5.4.1. Steel Containers

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Aluminum Containers

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Fiber-Reinforced/Composite

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.5. By Application

5.5.1. Sea Transport

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Rail Transport

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Road Transport

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Intermodal Transport

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

5.6. By Ownership

5.6.1. Shipper-Owned Containers (SOC)

5.6.1.1. Market Definition

5.6.1.2. Market Estimation and Forecast to 2035

5.6.2. Carrier-Owned Containers (COC)

5.6.2.1. Market Definition

5.6.2.2. Market Estimation and Forecast to 2035

5.6.3. Leasing Containers

5.6.3.1. Market Definition

5.6.3.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Container Type

6.2. By

Size

6.3. By

End-Use Industry

6.4. By

Material

6.5. By

Application

6.6. By

Ownership

6.6.1.

U.S. Market Estimate and Forecast

6.6.2.

Canada Market Estimate and Forecast

6.6.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Container Type

7.2. By

Size

7.3. By

End-Use Industry

7.4. By

Material

7.5. By

Application

7.6. By

Ownership

7.6.1.

Germany Market Estimate and Forecast

7.6.2.

France Market Estimate and Forecast

7.6.3.

U.K. Market Estimate and Forecast

7.6.4.

Italy Market Estimate and Forecast

7.6.5.

Spain Market Estimate and Forecast

7.6.6.

Russia Market Estimate and Forecast

7.6.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Container Type

8.2. By

Size

8.3. By

End-Use Industry

8.4. By

Material

8.5. By

Application

8.6. By

Ownership

8.6.1.

China Market Estimate and Forecast

8.6.2.

Japan Market Estimate and Forecast

8.6.3.

India Market Estimate and Forecast

8.6.4.

South Korea Market Estimate and Forecast

8.6.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Container Type

9.2. By

Size

9.3. By

End-Use Industry

9.4. By

Material

9.5. By

Application

9.6. By

Ownership

9.6.1.

Brazil Market Estimate and Forecast

9.6.2.

Saudi Arabia Market Estimate and Forecast

9.6.3.

South Africa Market Estimate and Forecast

9.6.4.

U.A.E. Market Estimate and Forecast

9.6.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

China International Marine Containers (Group) Co., Ltd. (CIMC)

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Dong Fang International Container (DFIC)

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

CXIC Group Containers Co., Ltd.

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Singamas Container Holdings Limited

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Maersk Container Industry A/S (MCI)

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Triton International Limited

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Textainer Group Holdings Limited

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Florens Container Services

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Touax Group

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Sea Box, Inc.

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Shipping Containers Market