Europe Autonomous Vehicle Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Vehicle Type (Passenger Cars, Commercial Vehicles), by Level of Autonomy (Level 1, Level 2, Level 3, Level 4, Level 5), by Application (Transportation, Defense, Logistics, Industrial), by Region (Germany, U.K., France, Italy, Rest of Europe)

| Status : Published | Published On : May, 2026 | Report Code : VRAT9675 | Industry : Automotive & Transportation | Available Format :

|

Page : 143 |

Europe Autonomous Vehicle Market Overview

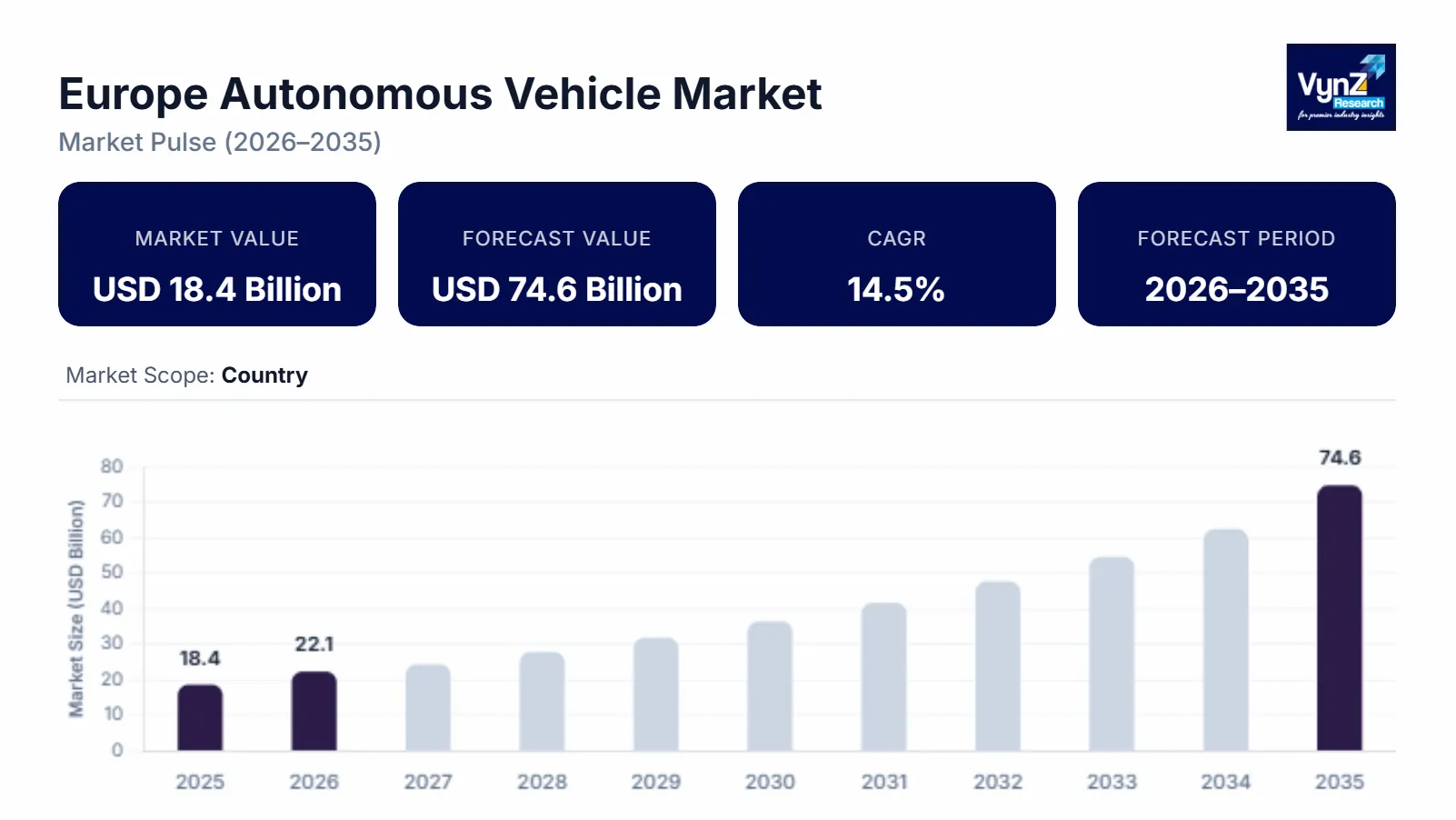

The Europe autonomous vehicle market size was valued at about USD 18.4 billion in 2025 and is projected to grow from nearly USD 22.1 billion in 2026 to roughly USD 74.6 billion by 2035, expanding at a CAGR of approximately 14.5% during 2026–2035.

Market Highlights

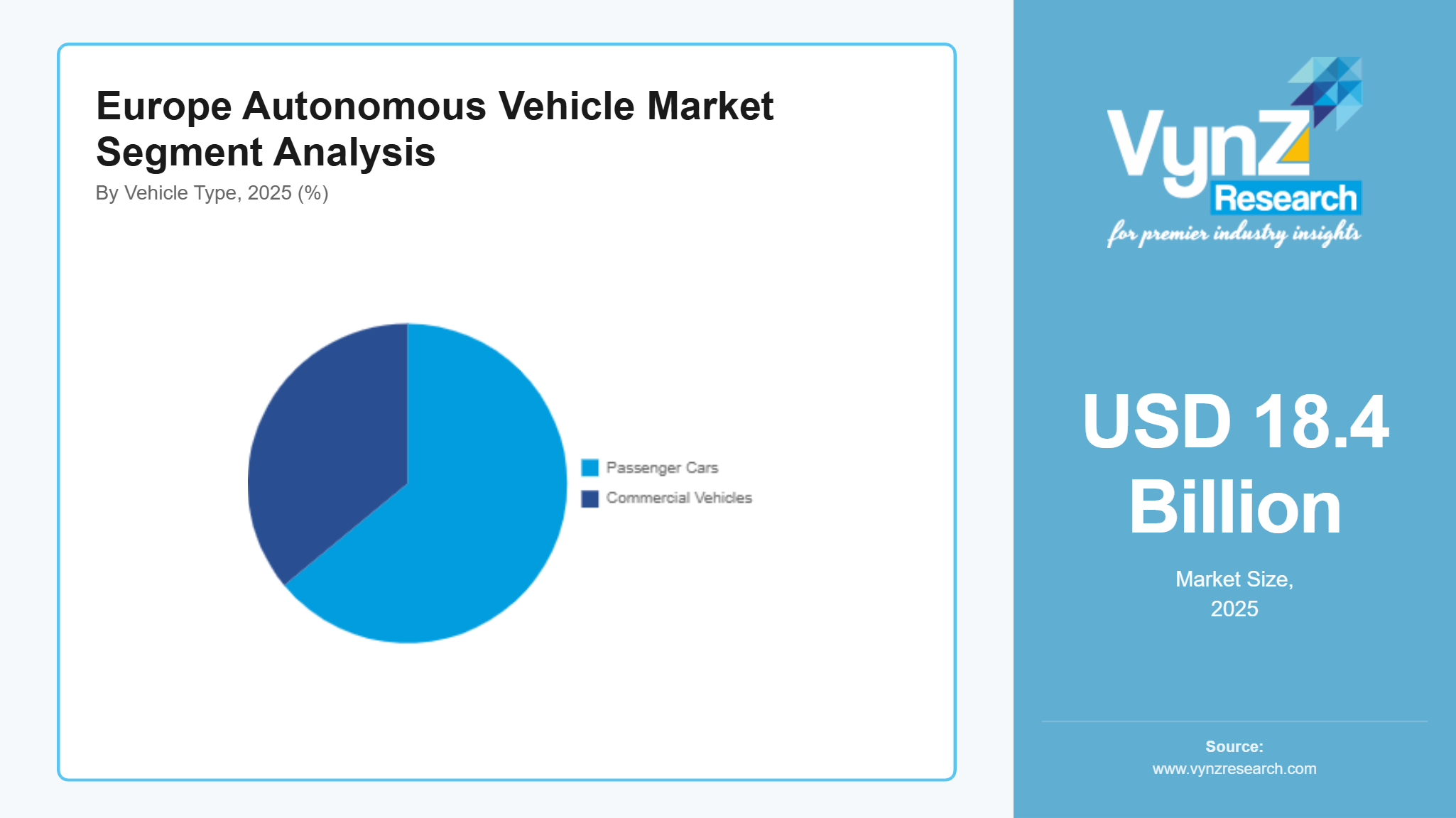

- Passenger cars led 2025 with 64% revenue share due to rising ADAS and connected mobility adoption.

- Level 2 systems held 38% market share in 2025 driven by advanced driver assistance features.

- Germany dominated in 2025 with 24% market share due to higher intelligent transport infrastructure investments.

- Commercial vehicles will grow fastest at 15.1% CAGR due to autonomous logistics and fleet optimization demand.

- Level 4 systems will expand ai 16.4% CAGR driven by AI and vehicle-to-infrastructure communication developments.

Market growth is driven by increase in deploying advanced driver assistance systems and connected mobility infrastructure. There are also supportive regulations promoting automated transportation technologies and artificial intelligence enabled driving systems. Demand for safer roadways and more efficient urban movement is helping the industry to expand across Germany, the U.K., and France. The European Commission mobility and transport efforts support connected and autonomous mobility ecosystems in the region through investments in intelligent transport systems and cross border autonomous vehicle testing corridors. Road safety frameworks of the European Road Safety Observatory and UNECE vehicle automation rules push car producers toward using more advanced safety technologies. At the same time public outlay for smart city mobility infrastructure, vehicle electrification, and digital transport networks is promoting commercialization of passenger vehicles and commercial vehicles throughout Europe.

Europe Autonomous Vehicle Market Dynamics

Market Trends

The market is moving toward connected, software defined, and safety integrated mobility ecosystems supported by regional transport modernization initiatives. Regulatory frameworks coming from the European Commission and UNECE automated lane keeping system rules are pushing faster development of autonomous driving technologies that emphasize vehicle safety, traffic efficiency, and emission reduction. More deployment of artificial intelligence enabled navigation systems, vehicle to infrastructure communication, and heavier sensor integration is changing the way product development happens across both passenger and commercial mobility platforms.

Growth Drivers

The market growth is driven by higher investments in connected transportation infrastructure and deeper integration of advanced driver assistance technologies in newer vehicle platforms. Public mobility transition programs supported by the European Commission and the national transport authorities are helping the rollout of intelligent transport systems and autonomous mobility test corridors across city areas and logistics networks. With more focus on road safety and traffic optimization from the European Road Safety Observatory, the adoption of automated driving solutions is being encouraged among automakers and fleet operators. Electric vehicle adoption is expanding and with higher investments in artificial intelligence, semiconductor technologies and smart mobility infrastructure, it should keep long term industry expansion moving in both commercial and passenger transportation.

Market Restraints / Challenges

Even with good growth signals the market still has obstacles around regulatory complexity, cybersecurity threats, and high costs of technology integration. Vehicle automation systems need lots of validation, software testing, and compliance approvals under continuously changing European transport and safety regulations, and that becomes a real commercialization barrier for manufacturers. Data privacy, software reliability, and weaker vehicle networks are also real challenges.

Market Opportunities

Real opportunities lie in autonomous logistics networks, smart urban mobility systems, and digitally connected transport infrastructure due to regional sustainability initiatives. Government backed investments under European smart mobility and climate transition programs are encouraging people and companies to adopt low emission autonomous transportation technologies across freight, public transit, and shared mobility use cases. Higher deployment of 5G enabled transport systems, AI driven fleet optimization platforms, and vehicle to infrastructure communication tools are opening doors for technology providers and automotive manufacturers to build longer term service capabilities. Companies with scalable software platforms, autonomous fleet management systems, and integrated mobility solutions should gain from increased spending on digital transportation modernization across Germany, France, and the Nordic region.

Europe Autonomous Vehicle Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 18.4 Billion |

|

Revenue Forecast in 2035 |

USD 74.6 Billion |

|

Growth Rate |

14.5% |

|

Segments Covered in the Report |

Vehicle Type, Level of Autonomy, Application, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

Germany, U.K., France, Italy, Rest of Europe |

|

Key Companies |

Bayerische Motoren Werke AG, Ford Motor Co, General Motors Co, Hyundai Motor Co, Mercedes-Benz Group AG, Renault SA, Tesla Inc, Toyota Motor Corp, Volkswagen AG, Volvo AB ADR |

|

Customization |

Available upon request |

Europe Autonomous Vehicle Market Segmentation

By Vehicle Type

Passenger cars were the leader of the market in 2025, making up around 64% of the total revenue driven by the constantly rising advanced driver assistance systems, connected mobility and semi-autonomous tech. Regulatory measures from the European Commission and UNECE vehicle safety rules push the industry toward automated safety features for passenger transport platforms and investments in electric passenger mobility, smarter transport infrastructure, and urban traffic management schemes are helping the segment expand over the longer run across Germany , France and the U.K.

Commercial vehicles are expected to grow the quickest between 2026 and 2035, with a projected CAGR of 15.1%. A lot of the momentum comes from the increased appetite for autonomous logistics workflows, fleet optimization tools, and intelligent freight transportation setups. Public funding aimed at smart logistics infrastructure and connected transport corridors is also making it easier to adopt autonomous commercial mobility options across regional supply chains.

By Level of Autonomy

In 2025, Level 2 autonomous systems held the biggest share, contributing about 38% of overall revenue due to installation of lane centering support, adaptive cruise control and driver monitoring features across mass market passenger cars. Safety requirements backed by European transport regulators and vehicle assessment schemes support adoption of partially automated driving systems among local automotive makers.

Level 4 autonomous systems are expected to grow fastest during 2026 to 2035, with an estimated CAGR of 16.4% supported by improvements in artificial intelligence, high precision mapping capabilities, and vehicle to infrastructure communication technologies. Pilot efforts backed by European smart mobility initiatives and autonomous driving testing corridors are helping commercialize automated transport.

By Application

In 2025, transportation applications held about 49% of the market due to higher funding for linked public transit, smarter city mobility infrastructure and advanced traffic control technologies. Government supported smart mobility programs keep encouraging deployment of autonomous passenger transport systems to reduce congestion, boost road safety, and lower transport emissions.

Logistics applications are projected to register the fastest growth over the forecast window, with an estimated CAGR of 15.7% due to the growing demand for automated freight movement, warehouse mobility automation, and last mile delivery optimization within regional supply chains. Public funding for intelligent freight corridors, digital logistics infrastructure, and industrial automation programs is supporting the deployment of autonomous logistics vehicles across distribution and manufacturing activities.

By End User

In 2025, automotive manufacturers and mobility service providers controlled the market with about 58% of overall revenue coming from them which was due to ongoing spending into autonomous driving software platforms, connected car ecosystems, and mobility integration tools. Strategic alliances between automakers, semiconductor manufacturers, and artificial intelligence developers are promoting self-driving mobility across Europe.

From 2026 to 2035, logistics operators and industrial fleet owners are projected to grow the fastest with a CAGR around 14.8% due to rising requirement for operational automation, better fuel efficiency, and digitally linked fleet management systems aimed at industrial transport work. Investments in autonomous freight mobility, warehouse automation, and smart industrial logistics infrastructure are helping adoption increase across regional manufacturing settings and supply chain ecosystems.

Regional Insights

Germany

Germany held around 24% of the market in 2025 due to strong automotive making capabilities, more mature mobility infrastructure, and more investment in intelligent transport systems. The big industrial centers in Munich, Stuttgart and Berlin adopt autonomous mobility tech in both private rides and freight style commercial vehicles. Regulations of the Federal Ministry for Digital and Transport and national autonomous driving guidelines push commercialization of Level 3 and Level 4 driving features.

The U.K.

The U.K. represented about 18% of the market in 2025 due to continuous investments in connected mobility ecosystems, rollout of autonomous pilot projects and supportive transport innovation policies. Cities like London, Birmingham and Manchester deploy more smarter transportation autonomous public transit systems. The Centre for Connected and Autonomous Vehicles and the Department for Transport launch programs that support research, testing and commercialization of advanced autonomous mobility options.

France

France held roughly 15% of the market in 2025 and will grow fast due to heavier investment in sustainable transport systems, wider autonomous mobility pilot corridors, and stronger adoption of electric self-driving vehicles close to urban areas. Paris, Lyon and Toulouse are basically key hubs for connected mobility innovation and intelligent transport deployments. Regulatory approaches backed by the French Ministry of Ecological Transition and smart mobility initiatives are encouraging inclusion of autonomous tools in public transportation and logistics infrastructure.

Italy

Italy captured about 11% of the market in 2025 supported by the whole modernization of transportation infrastructure and the growing adoption of connected mobility solutions. More investments in intelligent urban transport systems in places like Milan, Rome and Turin boost travel efficiency and reduce congestion. Government transport modernization programs and sustainability driven mobility initiatives are encouraging inclusion of advanced driver assistance and semi-autonomous driving systems across various regional automotive networks.

Rest of Europe

The rest of Europe, along with Spain, the Netherlands, Sweden, and Norway roughly made up about 12% of the market in 2025 due to higher investment in smart transport infrastructure, connected public mobility systems and autonomous logistics networks. Government led sustainability steps and intelligent transport programs across Nordic and Western European economies push adoption of autonomous and electric mobility solutions for both passenger travel and industrial applications. The rest of the market share belongs to the smaller European economies where emerging autonomous mobility chances are growing and investments into connected transportation infrastructure are rising.

Competitive Landscape / Company Insights

The market is moderately competitive with automotive manufacturers, semiconductor providers, and mobility technology companies trying to integrate artificial intelligence into connected mobility platforms and autonomous driving software to strengthen their market position. Companies are investing in research and development, smart mobility partnerships and digital transportation ecosystems to commercialize passenger and commercial vehicle segments. The regulatory frameworks from the European Commission and UNECE autonomous vehicle guidelines are also pushing innovation, safety compliance, and advanced autonomous driving technologies across the industry.

Mini Profiles

Bayerische Motoren Werke AG focuses on premium autonomous mobility solutions, connected vehicle technologies, and advanced driver assistance systems, supported by strong brand recognition, engineering expertise, and expanding investments in artificial intelligence driven transportation platforms.

Ford Motor Co operates across passenger and commercial autonomous vehicle segments, emphasizing intelligent fleet management, connected mobility ecosystems, and scalable transportation technologies through strategic software partnerships and digital mobility initiatives.

General Motors Co leverages autonomous driving software development, electric mobility integration, and strategic technology collaborations to strengthen market presence across connected transportation, logistics automation, and intelligent urban mobility applications.

Hyundai Motor Co focuses on smart mobility platforms, electric autonomous vehicles, and artificial intelligence enabled transportation systems, supported by growing investments in robotics, semiconductor integration, and connected mobility infrastructure development.

Mercedes-Benz Group AG emphasizes luxury autonomous mobility technologies, advanced safety integration, and intelligent driving systems, supported by premium vehicle positioning, innovation focused research programs, and strong engineering capabilities across Europe.

Key Players

- Bayerische Motoren Werke AG

- Ford Motor Co

- General Motors Co

- Hyundai Motor Co

- Mercedes-Benz Group AG

- Renault SA

- Tesla Inc

- Toyota Motor Corp

- Volkswagen AG

- Volvo AB ADR

Recent Developments

In April 2025, Renault SA introduced its new software defined electric commercial vehicle platform developed through Ampere for next generation connected mobility applications. The company expanded focus on scalable autonomous ready vehicle architecture designed to improve fleet efficiency and intelligent transportation integration.

In May 2026, Tesla Inc expanded deployment of its Full Self Driving supervised software across additional European markets including Lithuania following regulatory approvals in the Netherlands. The company continued investments in artificial intelligence based autonomous mobility systems and connected driving technologies across Europe.

In Apri, 2025, Toyota Motor Corp announced a strategic collaboration with Waymo to accelerate development and deployment of autonomous driving technologies for next generation mobility platforms. The partnership focuses on improving road safety, software integration, and intelligent transportation capabilities across connected vehicle ecosystems.

In May 2025, Volkswagen AG expanded investments in intelligent mobility technologies and autonomous driving software integration across its connected vehicle portfolio in Europe. The company continued strengthening digital mobility capabilities through artificial intelligence enabled driver assistance and vehicle connectivity systems.

In May 2026, Volvo AB ADR increased focus on autonomous freight transportation and connected commercial mobility solutions across European logistics operations. The company continued development of intelligent fleet management systems and automated transport technologies aimed at improving operational efficiency and road safety.

Europe Autonomous Vehicle Market Coverage

Vehicle Type Insight and Forecast 2026 - 2035

- Passenger Cars

- Commercial Vehicles

Level of Autonomy Insight and Forecast 2026 - 2035

- Level 1

- Level 2

- Level 3

- Level 4

- Level 5

Application Insight and Forecast 2026 - 2035

- Transportation

- Defense

- Logistics

- Industrial

Region Insight and Forecast 2026 - 2035

- Germany

- U.K.

- France

- Italy

- Rest of Europe

Europe Autonomous Vehicle Market by Region

- Germany

- By Vehicle Type

- By Level of Autonomy

- By Application

- By Region

- U.K.

- By Vehicle Type

- By Level of Autonomy

- By Application

- By Region

- France

- By Vehicle Type

- By Level of Autonomy

- By Application

- By Region

- Italy

- By Vehicle Type

- By Level of Autonomy

- By Application

- By Region

- Spain

- By Vehicle Type

- By Level of Autonomy

- By Application

- By Region

- Russia

- By Vehicle Type

- By Level of Autonomy

- By Application

- By Region

- Rest of Europe

- By Vehicle Type

- By Level of Autonomy

- By Application

- By Region

Table of Contents for Europe Autonomous Vehicle Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Vehicle Type

1.2.2. By

Level of Autonomy

1.2.3. By

Application

1.2.4. By

Region

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Europe Market Estimate and Forecast

4.1. Europe Market Overview

4.2. Europe Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Vehicle Type

5.1.1. Passenger Cars

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Commercial Vehicles

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.2. By Level of Autonomy

5.2.1. Level 1

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Level 2

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Level 3

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Level 4

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. Level 5

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.3. By Application

5.3.1. Transportation

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Defense

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Logistics

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Industrial

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.4. By Region

5.4.1. Germany

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. U.K.

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. France

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Italy

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Rest of Europe

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

6. Germany Market Estimate and Forecast

6.1. By

Vehicle Type

6.2. By

Level of Autonomy

6.3. By

Application

6.4. By

Region

7. U.K. Market Estimate and Forecast

7.1. By

Vehicle Type

7.2. By

Level of Autonomy

7.3. By

Application

7.4. By

Region

8. France Market Estimate and Forecast

8.1. By

Vehicle Type

8.2. By

Level of Autonomy

8.3. By

Application

8.4. By

Region

9. Italy Market Estimate and Forecast

9.1. By

Vehicle Type

9.2. By

Level of Autonomy

9.3. By

Application

9.4. By

Region

10. Spain Market Estimate and Forecast

10.1. By

Vehicle Type

10.2. By

Level of Autonomy

10.3. By

Application

10.4. By

Region

11. Russia Market Estimate and Forecast

11.1. By

Vehicle Type

11.2. By

Level of Autonomy

11.3. By

Application

11.4. By

Region

12. Rest of Europe Market Estimate and Forecast

12.1. By

Vehicle Type

12.2. By

Level of Autonomy

12.3. By

Application

12.4. By

Region

13. Company Profiles

13.1.

Bayerische Motoren Werke AG

13.1.1.

Snapshot

13.1.2.

Overview

13.1.3.

Offerings

13.1.4.

Financial

Insight

13.1.5.

Recent

Developments

13.2.

Ford Motor Co

13.2.1.

Snapshot

13.2.2.

Overview

13.2.3.

Offerings

13.2.4.

Financial

Insight

13.2.5.

Recent

Developments

13.3.

General Motors Co

13.3.1.

Snapshot

13.3.2.

Overview

13.3.3.

Offerings

13.3.4.

Financial

Insight

13.3.5.

Recent

Developments

13.4.

Hyundai Motor Co

13.4.1.

Snapshot

13.4.2.

Overview

13.4.3.

Offerings

13.4.4.

Financial

Insight

13.4.5.

Recent

Developments

13.5.

Mercedes-Benz Group AG

13.5.1.

Snapshot

13.5.2.

Overview

13.5.3.

Offerings

13.5.4.

Financial

Insight

13.5.5.

Recent

Developments

13.6.

Renault SA

13.6.1.

Snapshot

13.6.2.

Overview

13.6.3.

Offerings

13.6.4.

Financial

Insight

13.6.5.

Recent

Developments

13.7.

Tesla Inc

13.7.1.

Snapshot

13.7.2.

Overview

13.7.3.

Offerings

13.7.4.

Financial

Insight

13.7.5.

Recent

Developments

13.8.

Toyota Motor Corp

13.8.1.

Snapshot

13.8.2.

Overview

13.8.3.

Offerings

13.8.4.

Financial

Insight

13.8.5.

Recent

Developments

13.9.

Volkswagen AG

13.9.1.

Snapshot

13.9.2.

Overview

13.9.3.

Offerings

13.9.4.

Financial

Insight

13.9.5.

Recent

Developments

13.10.

Volvo AB ADR

13.10.1.

Snapshot

13.10.2.

Overview

13.10.3.

Offerings

13.10.4.

Financial

Insight

13.10.5.

Recent

Developments

14. Appendix

14.1. Exchange Rates

14.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Europe Autonomous Vehicle Market