Europe Sports Nutrition Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Product Category (Sports Protein Products, Sports Non-Protein Products), by Product Type (Vitamins, Minerals, Enzymes, Fatty Acids, Protein & Amino Acids, Botanicals, Nitrous Oxide Boosters, Other Sports Supplements), by Distribution Channel (Supermarkets / Hypermarkets, Convenience Stores, Specialist Stores, Online Retail Stores, Other Distribution Channels), by Retail Format (Brick-and-Mortar, E-commerce Channels), by Consumer Group (Athletes, Bodybuilders, Lifestyle Users / Recreational Users)

| Status : Published | Published On : Mar, 2026 | Report Code : VRFB11041 | Industry : Food & Beverage | Available Format :

|

Page : 145 |

Europe Sports Nutrition Market Overview

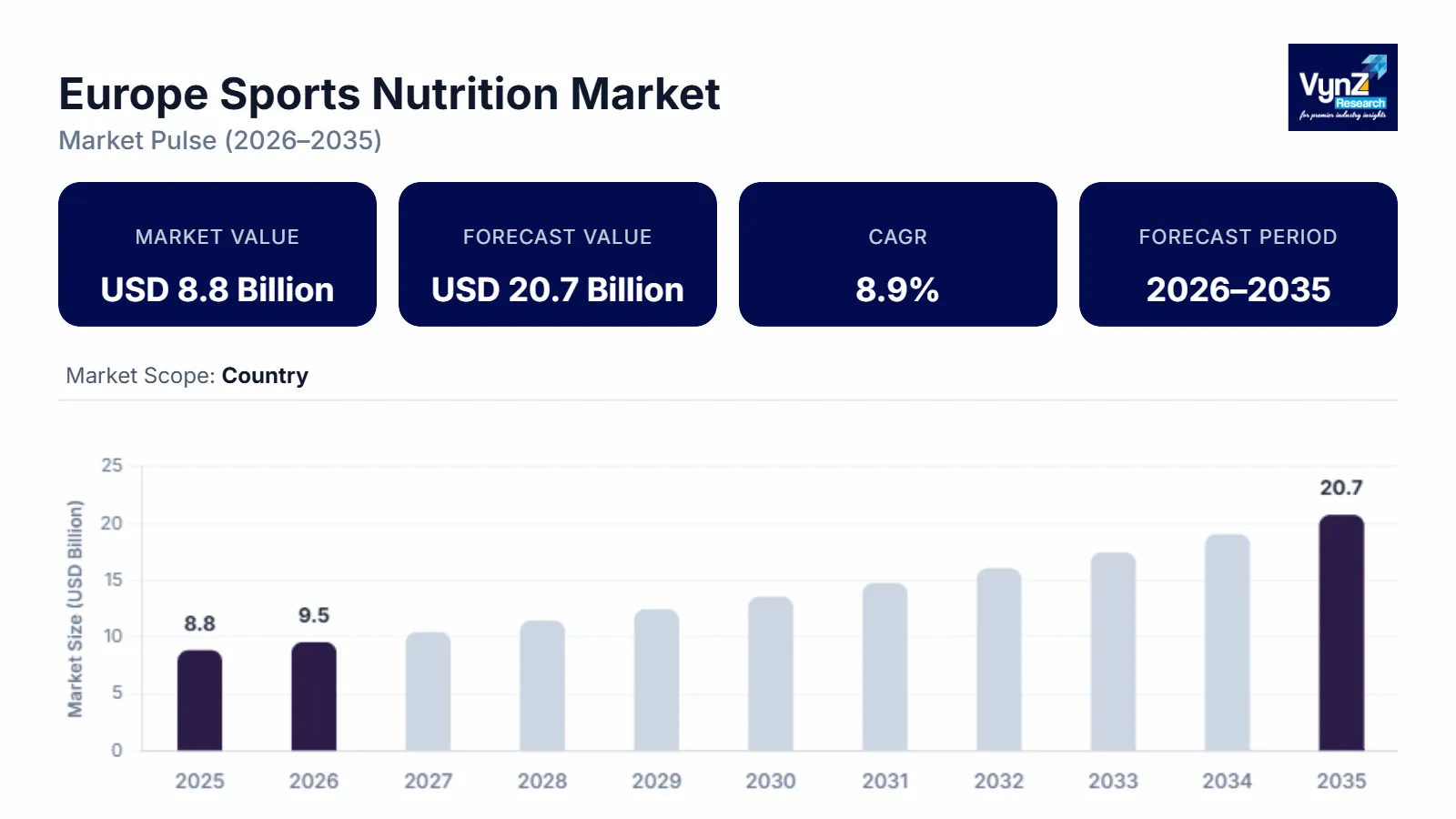

The Europe sports nutrition market was valued at USD 8.8 billion in 2025 and is estimated to reach USD 9.5 billion in 2026. The market is projected to grow to approximately USD 20.7 billion by 2035, registering a compound annual growth rate of 8.9% during 2026-2035.

The market experiences growth because more people participate in both fitness activities and recreational sports while demand for protein supplements increases and companies create new plant-based and functional nutrition products. More lifestyle consumers use sports nutrition products to help them with energy needs and recovery processes and weight management activities. The European Commission and World Health Organization reported that European countries have increased their physical activity awareness through preventive health programs which created a higher demand for nutritional supplements and performance-enhancing food products.

The industry outlook improves because government health promotion programs and food supplement regulations create better market conditions. The European Food Safety Authority and other institutions establish active lifestyle programs and nutrition labeling transparency and product safety standards which boost consumer confidence and increase product use among people. European sports nutrition market expansion continues because supportive policies and rising investments in fitness infrastructure and sports participation across the United Kingdom, Germany and France.

Europe Sports Nutrition Market Dynamics

Market Trends

The industry is undergoing significant changes in how consumers behave and which products they prefer to use. The market experiences growth because consumers now choose plant-based and clean-label sports nutrition products which use natural materials and sustainable sourcing and disclose food content through clear labeling. The increasing popularity of vegan protein, organic supplements and functional beverages is driving manufacturers to create a wider range of products for their offerings.

E-commerce distribution for sports nutrition products is currently experiencing expansion because digital technology becomes more widespread and online fitness communities continue to grow. The European Food Safety Authority and the World Health Organization both monitor regulatory content to assess how increased knowledge about nutritional supplements and active lifestyles impacts European consumer product purchasing decisions and product development.

Growth Drivers

The market expands because more people now participate in fitness activities and organized sports which creates ongoing demand from athletes and gym users and lifestyle consumers. The market expansion in European countries receives additional support from increasing expenditures on fitness infrastructure and sports clubs and wellness programs.

The market growth for fitness facilities, wellness programs and sports clubs sees major acceleration through increasing investments from European economies. The market experiences strong demand for protein supplements, energy bars and sports beverages because consumers seek solutions for energy management, muscle recovery and weight control. The European Commission establishes health promotion programs which boost local community knowledge about nutrition and physical activity throughout regional markets.

Market Restraints / Challenges

The market encounters specific obstacles which will impede its scheduled development despite its promising growth potential. The ingredient approval process, health claim process and supplement labeling process create regulatory challenges which manufacturers must navigate to develop products and enter markets. European food safety compliance requirements increase operational expenses for businesses which operate in several nations.

Manufacturers and suppliers face operational difficulties because their production processes depend on fluctuating raw material costs for key components which include whey protein, amino acids and special ingredient compounds. The manufacturing process relies on imported raw material and global dairy supply chains which result in cost pressures and price fluctuations that reduce profit margins during periods of economic instability and supply chain problems.

Market Opportunities

The market provides substantial opportunities through personalized sports nutrition products and functional sports nutrition products which experience growing demand because of demographic changes and increasing health awareness among consumers. The market for fitness enthusiasts and professional athletes requires companies which provide customized supplements, plant-based protein blends and targeted performance nutrition solutions to capture their business.

The market opportunities for premium sports nutrition products emerge from high-quality product investments which create exclusive product lines that lead to business profit growth through digital wellness platforms. Digital fitness tracking technology, nutrition applications and online wellness communities are advancing consumer engagement while sports nutrition brands in Europe grow their market presence.

Europe Sports Nutrition Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 8.8 Billion |

|

Revenue Forecast in 2035 |

USD 20.7 Billion |

|

Growth Rate |

8.9% |

|

Segments Covered in the Report |

Product Category, Product Type, Distribution Channel, Formulation, Retail Format, Consumer Group |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

United Kingdom, Germany, France, Rest of Europe |

|

Key Companies |

Abbott Laboratories, Atlantic Grupa d.d., Coca-Cola Company, Glanbia plc, Herbalife Ltd., Nestlé S.A., Olimp Laboratories, PepsiCo Inc., Prozis Group, Science in Sport plc |

|

Customization |

Available upon request |

Europe Sports Nutrition Market Segmentation

By Product Category

The market saw its biggest segment growth through sports protein products which generated approximately 64% of total revenue in 2025. Athletes and fitness enthusiasts consume protein powders and ready-to-drink beverages and nutrition bars in high amounts which enables these products to maintain their market dominance. The increasing number of gym memberships and structured sports participation across European countries creates ongoing demand for protein-based recovery and muscle-building products.

The fastest market growth will occur in sports non-protein products which are projected to achieve an 8.6% CAGR during the forecast period. The increasing demand for performance supplements inclusive of creatine and BCAAs and pre-workout formulations has led to more lifestyle consumers adopting these products to enhance their endurance and workout efficiency.

By Product Type

The protein and amino acid supplements market held the largest segment revenue share in 2025 with its 37% share. Professional athletes and recreational fitness users demand these products because they help with muscle recovery and strength development and endurance improvement. The expansion of product availability through fitness stores and digital retail channels drives continuous market development.

Botanicals and functional supplements are expected to grow at the fastest pace with an estimated CAGR of about 9.1% during the forecast period. European sports nutrition markets show segment expansion because consumers increasingly prefer plant-based nutrition and herbal performance enhancers and natural recovery ingredients.

By Distribution Channel

Supermarkets and hypermarkets accounted for the largest share of the Europe sports nutrition market in 2025, contributing roughly 41% of total distribution revenue. Retail networks and product visibility together with the growing availability of sports nutrition products in grocery chains enable these stores to maintain their market dominance.

Online retail stores will grow the fastest because they will achieve an estimated 9.3% CAGR. The combination of e-commerce platform growth and subscription models for supplements and digital marketing through fitness influencers has made it easier for consumers to access products and interact with brands.

By Formulation

Powder-based formulations became the market leader in 2025 because they generated almost 39% of total segment revenue. The product gained popularity because it allows users to customize their dosage and delivers higher protein content and its bulk packaging option provides cost benefits. Fitness professionals and athletes prefer powders as their choice for post-workout recovery drinks and nutritional shakes.

The market will grow the fastest through liquid and ready-to-drink formulations which will achieve an 8.8% CAGR during the forecast period. The increasing demand for convenient and portable nutrition products is driving manufacturers to create more ready-to-consume sports beverages and protein drinks.

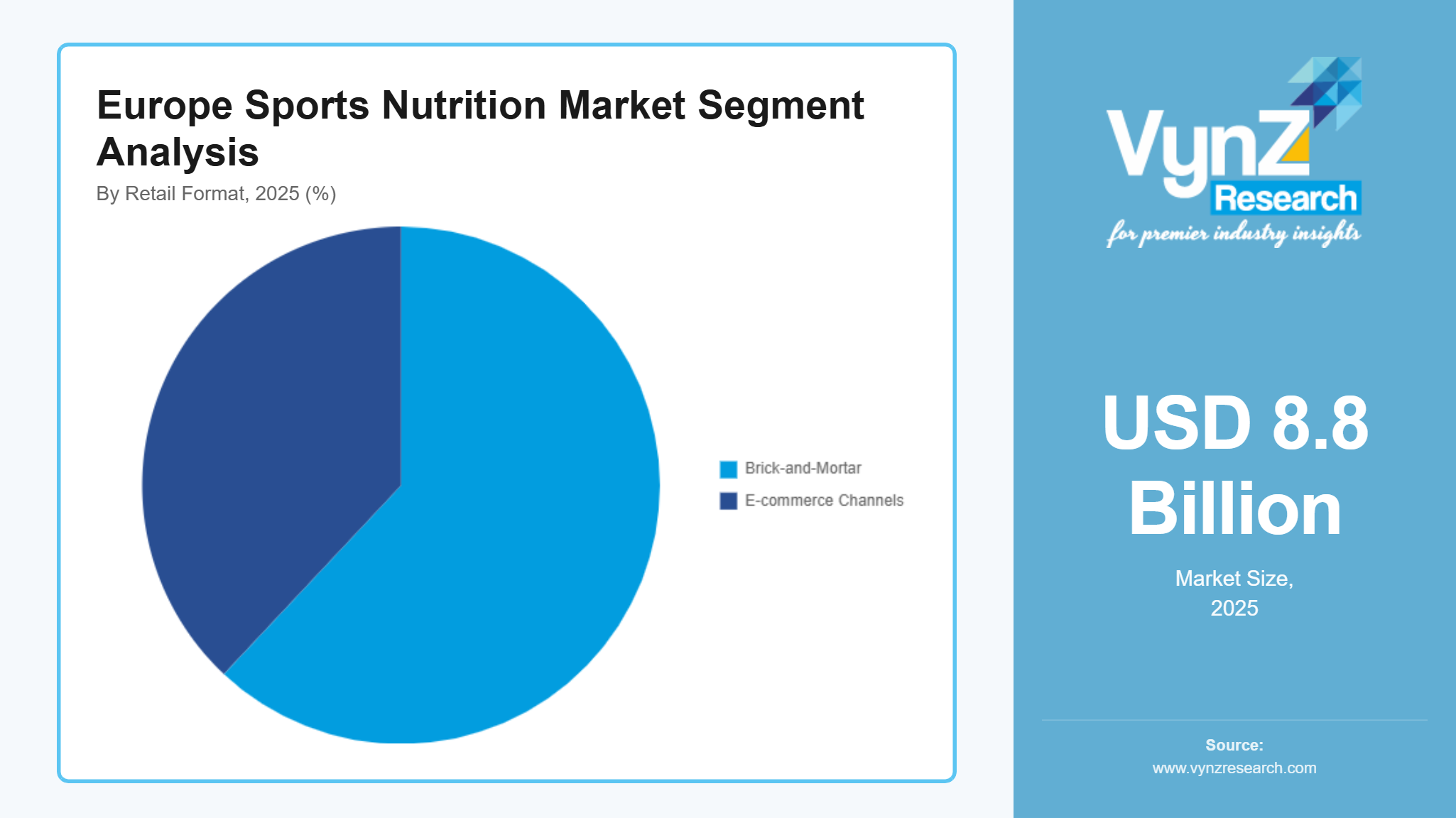

By Retail Format

The market in 2025 generated 62% of its total revenue through brick-and-mortar retail stores. Physical stores such as supermarkets and pharmacies and specialty fitness outlets remain important purchasing points as consumers often prefer direct product verification and in-store recommendations before purchase.

E-commerce channels will experience the fastest growth according to projections which estimate a 9.4% CAGR during the forecast period. Online fitness communities and direct-to-consumer supplement brands and improved logistics networks have created conditions that enable digital retail channels to grow rapidly.

By Consumer Group

The market in 2025 saw lifestyle users and recreational consumers control 46% of total market demand. Urban populations are adopting sports nutrition products because they become more health-conscious and pursue weight management goals and engage in fitness activities outside of professional sports.

Bodybuilders and professional athletes are expected to register the fastest growth during the forecast period with an estimated CAGR of 8.7%. The segment growth continues through competitive sports expansion and professional training program development and the rising need for specialized performance supplements.

Regional Insights

United Kingdom

The United Kingdom accounted for approximately 32% of the market in 2025 because of its active fitness culture, high gym membership rates, growing protein supplement and functional sports drink consumption. The market continues to expand because urban areas like London, Manchester and Birmingham maintain strong demand for their products.

The UK Department of Health and Social Care supports government health initiatives which promote active lifestyles and balanced nutrition to increase sports participation and drive demand for dietary supplements and sports nutrition products throughout the country.

Germany

The regional market shows Germany accounting for 22% because consumers have strong knowledge about functional nutrition while more people take part in recreational fitness activities. Urban areas including Berlin, Munich and Hamburg experience ongoing market expansion because people want to purchase protein powders and performance supplements and energy drinks.

The Federal Ministry of Food and Agriculture backs nutrition awareness programs which monitor food quality to create transparency about dietary supplement labeling and product safety standards. This helps build consumer trust which enables market growth.

France

France experiences growth due to fitness infrastructure expansion, more people participating in sports and consumers learning about performance nutrition. The major cities of Paris and Lyon function as important centers for sports nutrition product sales which encompass protein bars and recovery supplements and energy beverages.

The French Ministry of Health runs government health promotion programs and nutrition awareness initiatives which create an active lifestyle and balanced diet commitment among people. France holds approximately 16% of the regional market.

Rest of Europe

Italy, Spain and Netherlands collectively control approximately 30% of the market. The countries achieve market expansion through two factors which include rising consumer interest in preventive healthcare, increasing sports participation, expanding sports nutrition product distribution through retail and online channels.

Competitive Landscape / Company Insights

The market is moderately to highly competitive, with global and regional players focusing on product innovation, pricing strategies, and geographic expansion. Key companies are investing in advanced protein formulations, plant-based supplements, and digital marketing platforms to strengthen brand visibility and consumer engagement. Adoption is supported by regulatory oversight and nutrition guidance frameworks established by the European Food Safety Authority and health promotion initiatives from the World Health Organization, which encourage transparency, product safety, and consumer trust across the European sports nutrition market.

Mini Profiles

Abbott Laboratories focuses on clinical nutrition and performance-support supplements, supported by strong global distribution networks, established healthcare partnerships, and recognized nutrition brands that strengthen presence across medical and sports nutrition segments.

Atlantic Grupa d.d. operates in mass and functional nutrition segments, emphasizing product performance, regional brand strength, and diversified beverage and nutrition portfolios that support expanding sports and energy nutrition markets across Europe.

Coca-Cola Company leverages strategic partnerships and extensive beverage distribution networks to expand market presence, offering energy and functional drinks that cater to active consumers and fitness enthusiasts across European markets.

Glanbia plc focuses on sports protein powders, performance nutrition ingredients, and functional supplements, supported by strong brand recognition, advanced ingredient research capabilities, and global distribution channels serving athletes and lifestyle consumers.

Nestlé S.A. operates in premium and functional nutrition segments, emphasizing product innovation, nutritional science, and brand trust, supported by extensive retail distribution networks and strong research capabilities in health and performance nutrition.

Key Players

- Abbott Laboratories

- Atlantic Grupa d.d.

- Coca-Cola Company

- Glanbia plc

- Herbalife Ltd.

- Nestlé S.A.

- Olimp

- Laboratories

- PepsiCo Inc.

- Prozis

- Group

- Science in Sport plc

Recent Developments

In March 2025, Abbott Laboratories introduced new formulations within its performance nutrition portfolio, focusing on protein-based recovery and endurance nutrition products aimed at athletes and active consumers across European markets.

In February 2026, Glanbia plc expanded its Optimum Nutrition portfolio across European markets, strengthening distribution partnerships and increasing investment in performance nutrition products targeting fitness enthusiasts and professional athletes.

In October 2025, Nestlé S.A. expanded its functional and performance nutrition portfolio in Europe, focusing on protein-based beverages and functional supplements targeting active lifestyle consumers and sports enthusiasts.

In July 2025, PepsiCo Inc strengthened its presence in the European sports nutrition and functional beverage market through expanded distribution of performance drinks and hydration products across major retail networks.

In January 2026, Science in Sport plc announced new product innovations in endurance fueling and recovery nutrition, supported by research collaborations with European sports science institutes to enhance performance-focused supplement formulations.

Europe Sports Nutrition Market Coverage

Product Category Insight and Forecast 2026 - 2035

- Sports Protein Products

- Sports Non-Protein Products

Product Type Insight and Forecast 2026 - 2035

- Vitamins

- Minerals

- Enzymes

- Fatty Acids

- Protein & Amino Acids

- Botanicals

- Nitrous Oxide Boosters

- Other Sports Supplements

Distribution Channel Insight and Forecast 2026 - 2035

- Supermarkets / Hypermarkets

- Convenience Stores

- Specialist Stores

- Online Retail Stores

- Other Distribution Channels

Retail Format Insight and Forecast 2026 - 2035

- Brick-and-Mortar

- E-commerce Channels

Consumer Group Insight and Forecast 2026 - 2035

- Athletes

- Bodybuilders

- Lifestyle Users / Recreational Users

Europe Sports Nutrition Market by Region

- Germany

- By Product Category

- By Product Type

- By Distribution Channel

- By Retail Format

- By Consumer Group

- U.K.

- By Product Category

- By Product Type

- By Distribution Channel

- By Retail Format

- By Consumer Group

- France

- By Product Category

- By Product Type

- By Distribution Channel

- By Retail Format

- By Consumer Group

- Italy

- By Product Category

- By Product Type

- By Distribution Channel

- By Retail Format

- By Consumer Group

- Spain

- By Product Category

- By Product Type

- By Distribution Channel

- By Retail Format

- By Consumer Group

- Russia

- By Product Category

- By Product Type

- By Distribution Channel

- By Retail Format

- By Consumer Group

- Rest of Europe

- By Product Category

- By Product Type

- By Distribution Channel

- By Retail Format

- By Consumer Group

Table of Contents for Europe Sports Nutrition Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Product Category

1.2.2. By

Product Type

1.2.3. By

Distribution Channel

1.2.4. By

Retail Format

1.2.5. By

Consumer Group

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Europe Market Estimate and Forecast

4.1. Europe Market Overview

4.2. Europe Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Product Category

5.1.1. Sports Protein Products

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Sports Non-Protein Products

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.2. By Product Type

5.2.1. Vitamins

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Minerals

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Enzymes

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Fatty Acids

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. Protein & Amino Acids

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.2.6. Botanicals

5.2.6.1. Market Definition

5.2.6.2. Market Estimation and Forecast to 2035

5.2.7. Nitrous Oxide Boosters

5.2.7.1. Market Definition

5.2.7.2. Market Estimation and Forecast to 2035

5.2.8. Other Sports Supplements

5.2.8.1. Market Definition

5.2.8.2. Market Estimation and Forecast to 2035

5.3. By Distribution Channel

5.3.1. Supermarkets / Hypermarkets

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Convenience Stores

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Specialist Stores

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Online Retail Stores

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Other Distribution Channels

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.4. By Retail Format

5.4.1. Brick-and-Mortar

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. E-commerce Channels

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.5. By Consumer Group

5.5.1. Athletes

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Bodybuilders

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Lifestyle Users / Recreational Users

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

6. Germany Market Estimate and Forecast

6.1. By

Product Category

6.2. By

Product Type

6.3. By

Distribution Channel

6.4. By

Retail Format

6.5. By

Consumer Group

7. U.K. Market Estimate and Forecast

7.1. By

Product Category

7.2. By

Product Type

7.3. By

Distribution Channel

7.4. By

Retail Format

7.5. By

Consumer Group

8. France Market Estimate and Forecast

8.1. By

Product Category

8.2. By

Product Type

8.3. By

Distribution Channel

8.4. By

Retail Format

8.5. By

Consumer Group

9. Italy Market Estimate and Forecast

9.1. By

Product Category

9.2. By

Product Type

9.3. By

Distribution Channel

9.4. By

Retail Format

9.5. By

Consumer Group

10. Spain Market Estimate and Forecast

10.1. By

Product Category

10.2. By

Product Type

10.3. By

Distribution Channel

10.4. By

Retail Format

10.5. By

Consumer Group

11. Russia Market Estimate and Forecast

11.1. By

Product Category

11.2. By

Product Type

11.3. By

Distribution Channel

11.4. By

Retail Format

11.5. By

Consumer Group

12. Rest of Europe Market Estimate and Forecast

12.1. By

Product Category

12.2. By

Product Type

12.3. By

Distribution Channel

12.4. By

Retail Format

12.5. By

Consumer Group

13. Company Profiles

13.1.

Abbott Laboratories

13.1.1.

Snapshot

13.1.2.

Overview

13.1.3.

Offerings

13.1.4.

Financial

Insight

13.1.5.

Recent

Developments

13.2.

Atlantic Grupa d.d.

13.2.1.

Snapshot

13.2.2.

Overview

13.2.3.

Offerings

13.2.4.

Financial

Insight

13.2.5.

Recent

Developments

13.3.

Coca-Cola Company

13.3.1.

Snapshot

13.3.2.

Overview

13.3.3.

Offerings

13.3.4.

Financial

Insight

13.3.5.

Recent

Developments

13.4.

Glanbia plc

13.4.1.

Snapshot

13.4.2.

Overview

13.4.3.

Offerings

13.4.4.

Financial

Insight

13.4.5.

Recent

Developments

13.5.

Herbalife Ltd.

13.5.1.

Snapshot

13.5.2.

Overview

13.5.3.

Offerings

13.5.4.

Financial

Insight

13.5.5.

Recent

Developments

13.6.

Nestlé S.A.

13.6.1.

Snapshot

13.6.2.

Overview

13.6.3.

Offerings

13.6.4.

Financial

Insight

13.6.5.

Recent

Developments

13.7.

Olimp Laboratories

13.7.1.

Snapshot

13.7.2.

Overview

13.7.3.

Offerings

13.7.4.

Financial

Insight

13.7.5.

Recent

Developments

13.8.

PepsiCo Inc.

13.8.1.

Snapshot

13.8.2.

Overview

13.8.3.

Offerings

13.8.4.

Financial

Insight

13.8.5.

Recent

Developments

13.9.

Prozis Group

13.9.1.

Snapshot

13.9.2.

Overview

13.9.3.

Offerings

13.9.4.

Financial

Insight

13.9.5.

Recent

Developments

13.10.

Science in Sport plc

13.10.1.

Snapshot

13.10.2.

Overview

13.10.3.

Offerings

13.10.4.

Financial

Insight

13.10.5.

Recent

Developments

14. Appendix

14.1. Exchange Rates

14.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Europe Sports Nutrition Market