Monomaterial Packaging Films Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Material Type (Polyethylene, Polypropylene, Others), by Packaging Type (Flexible Packaging, Pouches, Bags, Others), by Distribution Channel (Offline, Online), by End Use (Food and Beverage, Personal Care, Pharmaceutical, Others)

| Status : Published | Published On : Apr, 2026 | Report Code : VRFB11042 | Industry : Food & Beverage | Available Format :

|

Page : 170 |

Monomaterial Packaging Films Market Overview

The global monomaterial packaging films market which was valued at approximately USD 6.36 billion in 2025 and is estimated to rise further up to almost USD 6.85 billion by 2026, is projected to reach around USD 12.90 billion in 2035, expanding at a CAGR of about 7% during the forecast period from 2026 to 2035.

Sustainable packaging regulations drive market growth because businesses need recyclable materials and must decrease plastic waste while their circular economy packaging solutions become more popular. The market extends across China, Germany and the United States because food and beverage packaging needs create demand and countries develop their waste management systems and recycling programs.

The growth path receives extra support from environmental policies which governments implement and from worldwide sustainability standards. The United Nations Environment Program and national plastic waste reduction policies create regulatory initiatives which support the shift to recyclable packaging according to established packaging standards. Public sector programs which support extended producer responsibility and plastic recycling targets lead to faster industrial and consumer packaging adoption of monomaterial films. Major economies establish environmental agencies and policy mandates which drive recycling infrastructure investments to enhance supply chain capabilities and create enduring demand in worldwide packaging markets.

Monomaterial Packaging Films Market Dynamics

Market Trends

The industry is experiencing changes because people now choose eco-friendly packaging materials and companies use different technologies. The market trend shows that companies now use recyclable monomaterial structures because they need to meet environmental requirements and optimize their material usage. The United Nations Environment Program and national plastic reduction policies create frameworks that help countries decrease their use of multi-layer plastics. The packaging industry is now using more polyethylene and polypropylene films because of this increase.

The market trend currently shows that businesses use advanced barrier technologies because they need to meet innovation goals and comply with regulatory requirements. The businesses develop high-performance coatings and functional packaging solutions to protect product quality while allowing for recycling. The extended producer responsibility policies that governments back in Europe and Asia Pacific regions help this transition to circular economy.

Growth Drivers

The market establishes itself through regulatory forces which require businesses to decrease plastic waste and use recyclable materials, thus creating demand in the food, beverage market and consumer goods market. The increasing investments in recycling infrastructure and sustainable manufacturing solutions lead to greater adoption of new systems. The government programs which promote circular economy methods drive companies to adopt mono structured packaging as their new packaging standard.

The increasing need for flexible packaging solutions is driving industry expansion. The industry needs lightweight and recyclable films, which manufacturers provide because they want to achieve cost-effectiveness and regulatory compliance. The sustainable packaging innovation which public sector entities finance leads to expanded market development in all major commercial regions.

Market Restraints / Challenges

The market struggles because multi-layer packaging delivers better performance than current options, which limits their use in environments that need high barrier protection. Regulatory bodies need to create simple processes for organizations to manage patent rights because complex compliance processes hinder their ability to enter cost-sensitive markets.

The costs of polymer raw material dependence increase because price changes and supply chain risks create financial burdens. The government environmental evaluations show that developing countries lack recycling infrastructure, which limits their ability to operate recycling systems successfully at scale.

Market Opportunities

The regulations and consumer preferences create business opportunities. The recyclable high-performance film manufacturers will gain market share in the food industry and consumer goods sector. The government programs that support plastic waste reduction will help businesses adopt sustainable packaging practices.

The market potential, which combines advanced material innovation with smart packaging systems, offers additional growth opportunities. The development of high barrier coatings requires investment support for automation to create better operational results and productivity. The public sector programs which support sustainable manufacturing practices will create new opportunities for business expansion in the future.

Global Monomaterial Packaging Films Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 6.36 Billion |

|

Revenue Forecast in 2035 |

USD 12.90 Billion |

|

Growth Rate |

7% |

|

Segments Covered in the Report |

Material Type, Packaging Type, Distribution Channel, End Use |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

Asia Pacific, Europe, North America, Rest of the World |

|

Key Companies |

Amcor plc, Berry Global Inc., Borealis AG, Constantia Flexibles Group GmbH, Dow Inc., ExxonMobil Corporation, Huhtamaki Oyj, Mondi plc, Sealed Air Corporation, UFlex Limited |

|

Customization |

Available upon request |

Monomaterial Packaging Films Market Segmentation

By Material Type

The market reached its highest market share in 2025 through polyethylene based films which generated 48% of total market revenues. The product excels because it serves multiple flexible packaging purposes and achieves high recycling success while existing waste management systems can process its materials. The demand for recyclable plastics combined with government supported sustainability frameworks which reduce multilayer packaging structures has increased in food and consumer goods markets.

The forecast period between 2026 and 2035 will see polypropylene based films achieve the highest growth rate because they will record a CAGR of 7.5% during this time. The market will expand because businesses now prefer lightweight packaging which offers better mechanical strength and barrier protection performance. Segment growth will continue because processed food packaging and industrial applications show increasing market adoption.

By Packaging Type

Flexible packaging formats accounted for the largest market share in 2025, contributing approximately 62% of segment revenue. The product achieves market dominance because it offers cost savings through lower material requirements while consumers increasingly prefer lightweight portable packing methods. The manufacturing industry now shifts to flexible monomaterial films because regulatory bodies push companies to decrease waste while they apply sustainable materials across their production processes.

The market for pouch-based packaging will experience the fastest growth which will reach an estimated CAGR of 7.2% between 2026 and 2035. Market growth happens because more people want convenient packaging solutions which stay fresh for longer periods and provide better function. The market segment grows because food and beverage companies successfully use personal care products.

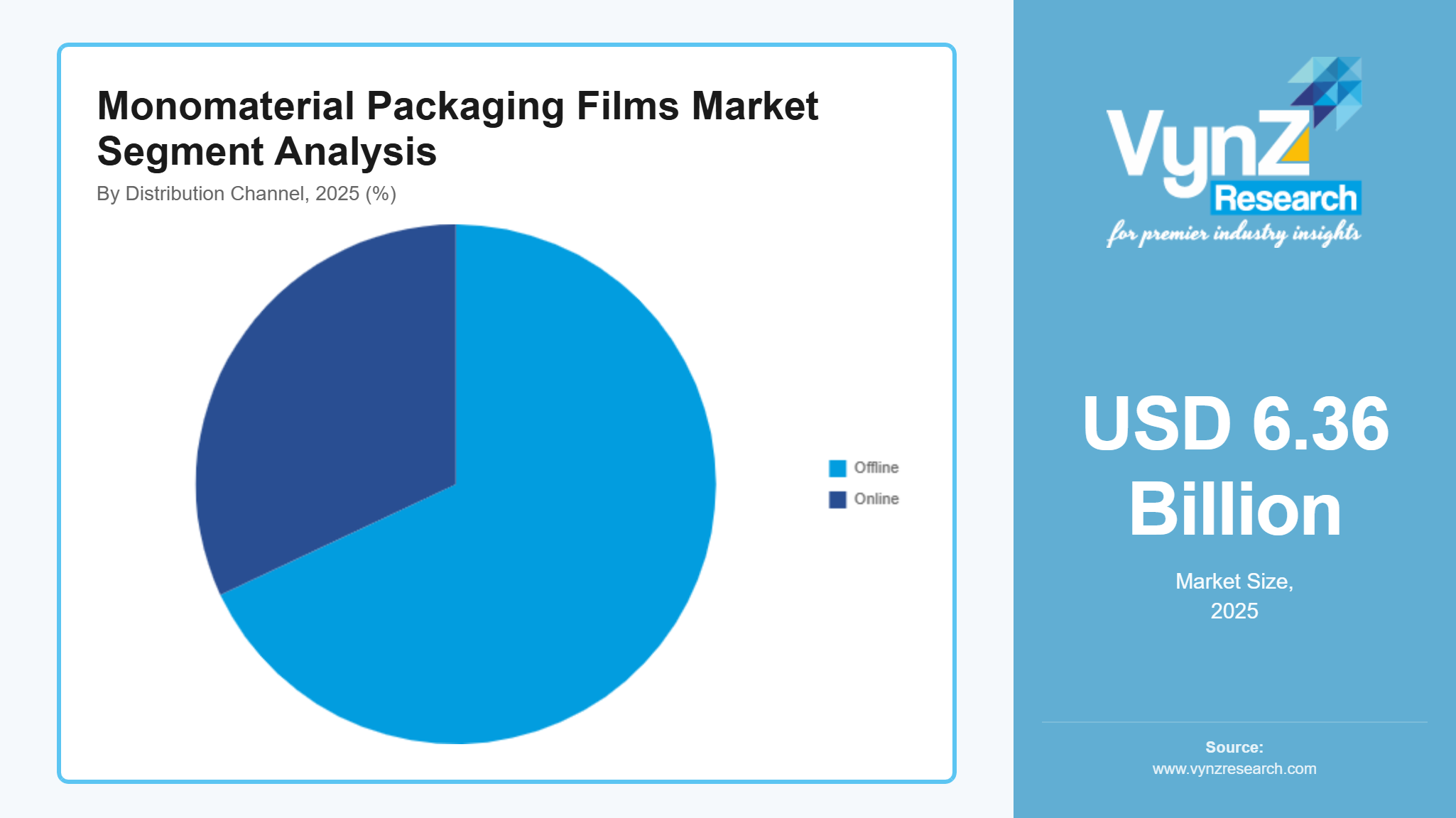

By Distribution Channel

The year 2025 saw offline distribution channels control 68% of total market revenue which marked their highest market share. The established supply chains and bulk procurement practices together with direct manufacturer to industry partnerships create the conditions which enable their market dominance. Industrial buyers continue to prioritize product validation which technical support and long-term supplier contracts create strong advantages for offline channels.

Online distribution will achieve the highest growth rate because it will show a CAGR of approximately 6.9% throughout the entire forecast period. Procurement process digitalization has created market expansion which enables the development of advanced logistics systems that provide customers with better pricing information. Businesses can now use digital platforms to reach more customers while their supply chains run more efficiently.

By End Use

The food and beverage sector accounted for the largest market share in 2025 when it generated 52% of total revenue. The package design leads the market because high consumption patterns combine with growing demand for packaged food products and regulations require the use of safe sustainable packaging materials. Government programs which establish food safety guidelines and packaging regulations have increased worldwide market adoption of their packaging solutions.

Personal care and pharmaceutical applications are expected to register the fastest growth, with an estimated CAGR of 7.1% during 2026 to 2035. The market expansion occurs because businesses now require hygienic packaging solutions which protect their products while meeting regulations for sensitive product usage. The consumer goods industry expands because more people want to buy sustainable packaging which will lead to market growth in the future.

Regional Insights

Asia Pacific

The Asia Pacific region will hold an approximate 46% share of the market by 2025 because its manufacturing activities, food processing industries and sustainable packaging solution needs continue to grow. The major urban centers of Shanghai, Mumbai and Tokyo enable food and consumer goods industries to maintain their high demand for flexible packaging. The regional market performance improves because governmental programs which promote plastic waste reduction and recycling receive backing from environmental agencies and national sustainability initiatives while businesses adopt recyclable film materials. The public policies which support circular economy frameworks together with waste management infrastructure investments drive market expansion. The industrial production growth and export packaging demand increase maintain this region's market leadership position.

Europe

Europe will capture an estimated 20% of the market in 2025 because its strict environmental laws and effective policy enforcement mechanisms protect packaging sustainability. The United Kingdom, France and Germany will see higher adoption rates for recyclable materials because environmental regulations require them to implement European environmental regulations. The food, personal care and pharmaceutical sectors require constant market growth because their needs keep increasing. The government programs which support extended producer responsibility and plastic recycling targets push manufacturers to switch to monomaterial products. The regional market development receives additional support from companies which use sustainable materials together with advanced packaging technologies.

North America

The North American market will have a 16% share by 2025 because companies demand more sustainable packaging solutions and the packaged food and retail sectors operate strongly in the region. The package goods market in New York, Los Angeles and Chicago has continuous demand because residents practice environmental responsibility in their packaging choices.

The government programs which receive backing from environmental protection agencies will make recycling infrastructure better while they motivate people to use recyclable products. The packaging industry now receives support from companies who invest in packaging innovations together with their digital supply chain systems.

Rest of the World

The global market in 2025 has 18% of its total value coming from Latin America, Middle East, Africa and the rest of the world. The two regions will experience growth because urban areas are developing and retail businesses are expanding and sustainable packaging products are becoming more popular. The food and consumer goods sectors in Brazil, the United Arab Emirates and South Africa are seeing higher demand for flexible packaging products. The government environmental programs and waste management initiatives will lead to more adoption of recyclable packaging materials but not as quickly as developed countries.

Competitive Landscape / Company Insights

The market displays moderate to high levels of competition because two types of competitors exist who work to develop new products and establish new pricing methods and expand their businesses into new markets. Companies are increasing their research and development spending together with their sustainable material technology investments to achieve better market results. The regulatory frameworks and environmental guidelines which government bodies and international organizations establish, push manufacturers to develop better recyclability standards, achieve higher material efficiency and create product lines which match circular economy standards while the competition between major regions becomes more intense.

Mini Profiles

Amcor plc focuses on sustainable flexible packaging and monomaterial film solutions, supported by strong global distribution networks, established brand recognition, and cost efficient large scale manufacturing capabilities across key regions.

Berry Global Inc. operates in mass packaging segments, emphasizing performance driven plastic solutions, scalable production systems, and material innovation to support cost efficiency and sustainability requirements across industrial and consumer applications.

Constantia Flexibles Group GmbH leverages strategic partnerships and advanced material engineering capabilities to expand market presence, focusing on recyclable flexible packaging solutions and strong integration with global food and pharmaceutical supply chains.

Dow Inc. focuses on polymer and material science solutions, supported by extensive research and development capabilities, global supply chain strength, and innovation in sustainable and high-performance packaging materials.

ExxonMobil Corporation leverages integrated petrochemical operations and global production infrastructure to expand market presence, focusing on high quality polymer resins and efficient supply capabilities supporting advanced packaging applications.

Key Players

- Amcor plc

- Berry Global Inc.

- Borealis AG

- Constantia Flexibles Group GmbH

- Dow Inc.

- ExxonMobil Corporation

- Huhtamaki Oyj

- Mondi plc

- Sealed Air Corporation

- UFlex Limited

Recent Developments

In February, 2025, Borealis AG expanded its circular polyolefin solutions for mono material packaging films, focusing on improving recyclability and material efficiency. The initiative supports regulatory compliance with European sustainability frameworks and circular economy targets.

In March, 2025, Huhtamaki Oyj introduced recyclable mono material flexible packaging solutions aimed at replacing multilayer laminates. The development emphasizes enhanced barrier performance and alignment with global packaging waste reduction initiatives.

In June, 2025, Mondi plc launched advanced mono material film solutions designed for food packaging applications. The company highlighted improved product protection, reduced material usage, and compatibility with established recycling streams.

In August, 2025, Sealed Air Corporation enhanced its sustainable packaging portfolio by developing mono material film technologies focused on lightweight and recyclable solutions. The initiative supports operational efficiency and reduced environmental impact across supply chains.

In January, 2026, UFlex Limited strengthened its product offerings by introducing high performance mono material films for flexible packaging applications. The development focuses on improved durability, cost efficiency, and compliance with sustainability regulations.

Global Monomaterial Packaging Films Market Coverage

Material Type Insight and Forecast 2026 - 2035

- Polyethylene

- Polypropylene

- Others

Packaging Type Insight and Forecast 2026 - 2035

- Flexible Packaging

- Pouches

- Bags

- Others

Distribution Channel Insight and Forecast 2026 - 2035

- Offline

- Online

End Use Insight and Forecast 2026 - 2035

- Food and Beverage

- Personal Care

- Pharmaceutical

- Others

Global Monomaterial Packaging Films Market by Region

- North America

- By Material Type

- By Packaging Type

- By Distribution Channel

- By End Use

- By Country - U.S., Canada, Mexico

- Europe

- By Material Type

- By Packaging Type

- By Distribution Channel

- By End Use

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Material Type

- By Packaging Type

- By Distribution Channel

- By End Use

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Material Type

- By Packaging Type

- By Distribution Channel

- By End Use

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Monomaterial Packaging Films Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Material Type

1.2.2. By

Packaging Type

1.2.3. By

Distribution Channel

1.2.4. By

End Use

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Material Type

5.1.1. Polyethylene

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Polypropylene

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Others

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Packaging Type

5.2.1. Flexible Packaging

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Pouches

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Bags

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Others

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.3. By Distribution Channel

5.3.1. Offline

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Online

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By End Use

5.4.1. Food and Beverage

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Personal Care

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Pharmaceutical

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Others

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Material Type

6.2. By

Packaging Type

6.3. By

Distribution Channel

6.4. By

End Use

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Material Type

7.2. By

Packaging Type

7.3. By

Distribution Channel

7.4. By

End Use

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Material Type

8.2. By

Packaging Type

8.3. By

Distribution Channel

8.4. By

End Use

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Material Type

9.2. By

Packaging Type

9.3. By

Distribution Channel

9.4. By

End Use

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Amcor plc

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Berry Global Inc.

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Borealis AG

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Constantia Flexibles Group GmbH

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Dow Inc.

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

ExxonMobil Corporation

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Huhtamaki Oyj

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Mondi plc

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Sealed Air Corporation

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

UFlex Limited

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Monomaterial Packaging Films Market