Release Agents Market Size & Share Growth Forecast Report (2026-2035)

Industry Insight by Type (Water Based, Solvent Based, Oil Based), by Form (Liquid, Spray, Paste, Solid), by Source (Synthetic, Bio Based), by End Use (Food Processing, Rubber, Plastics, Composites, Concrete, Others)

| Status : Published | Published On : Jul, 2026 | Report Code : VRCH2134 | Industry : Chemicals & Materials | Available Format :

|

Page : 156 |

Release Agents Market Overview

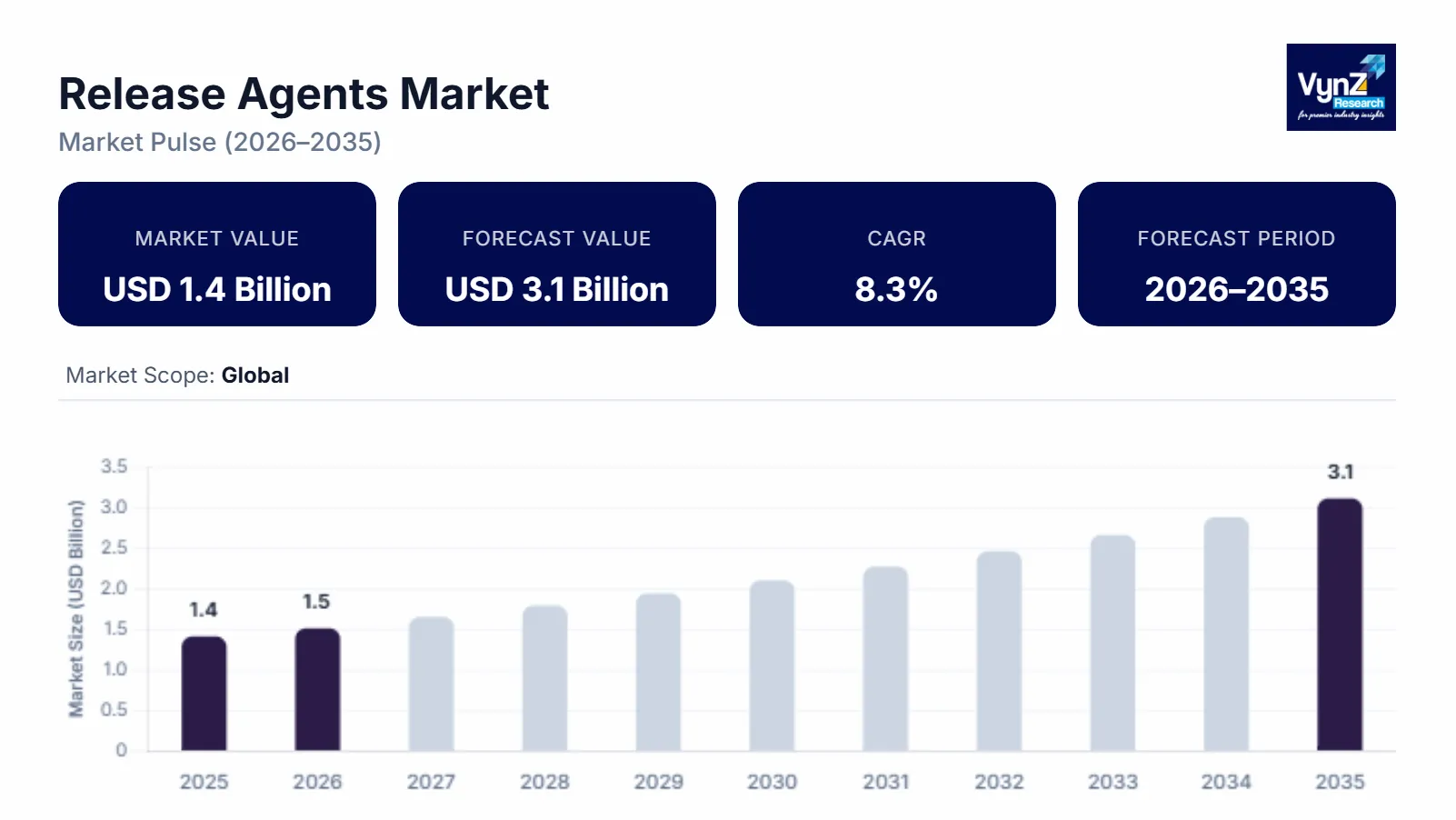

The release agents market size was estimated at about USD 1.4 billion in 2025 and is expected to reach around USD 1.5 billion in 2026, rising to roughly USD 3.1 billion by 2035, growing at approximately 8.3% CAGR from 2026 to 2035.

Research Highlights

- Water based release agents held 48% market share due to increasing food safety and sustainability requirements.

- Liquid release agents captured 57% market share because of superior application efficiency across manufacturing industries.

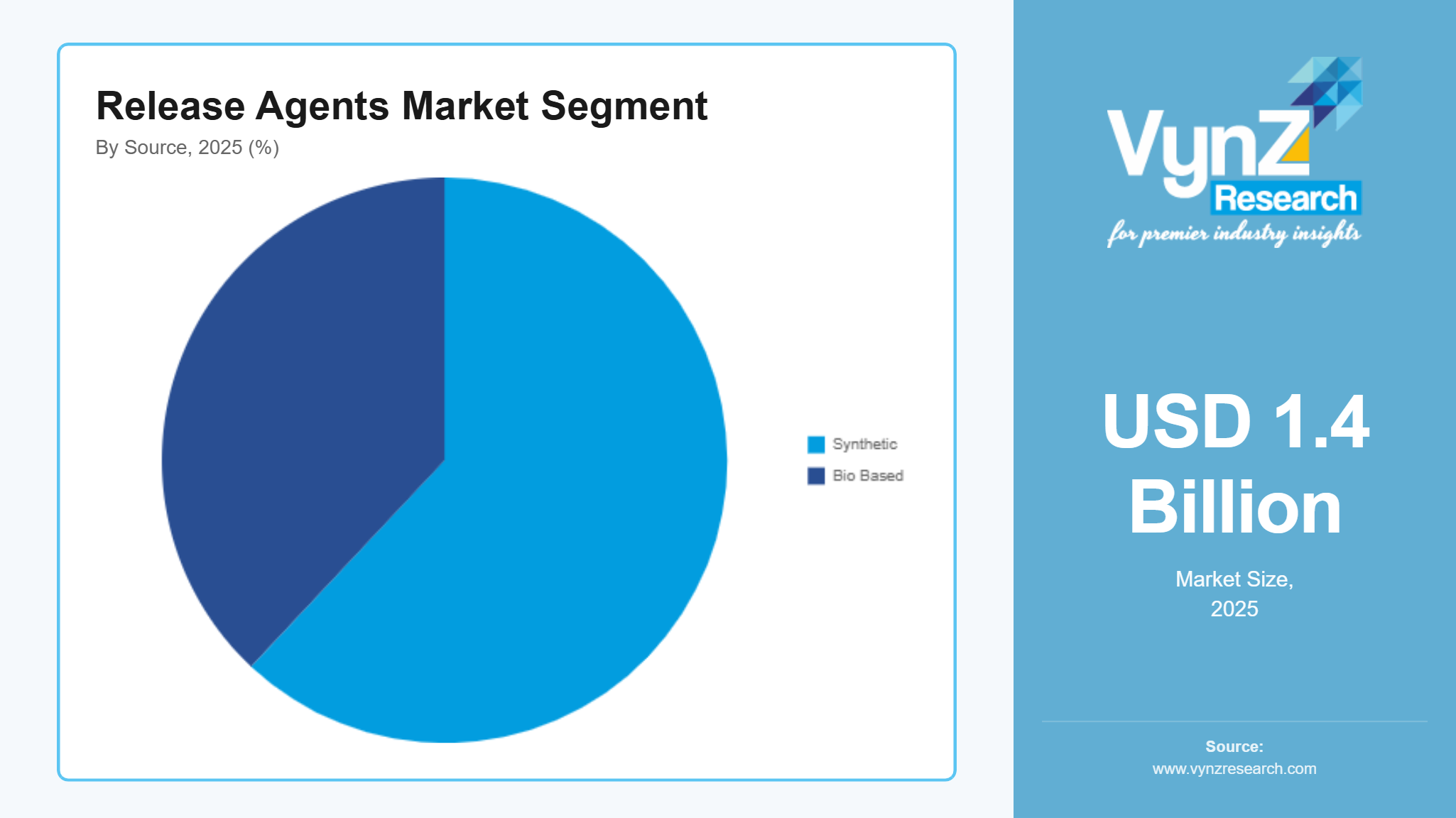

- Synthetic release agents accounted for 62% market share supported by broad industrial usage and cost effectiveness.

- Composites are projected to grow at 9.1% CAGR through 2035 due to growing lightweight material adoption.

- North America held 30% market share in 2025 supported by advanced food processing and stringent regulatory standards.

Market growth is facilitated by expanding food processing activities, increasing demand from the bakery and confectionery industry, and increasing adoption across industrial molding applications along with growing use of bio based and clean label release agent formulations. Growing demand for high quality processed food and ongoing investments in sustainable manufacturing and food safety initiatives are further supporting market expansion across major regions including North America, Europe, and Asia Pacific. According to the Food and Agriculture Organization (FAO), global food processing and value-added food production continue to expand in response to changing consumer demand and urbanization. In addition, the U.S. Food and Drug Administration (FDA) continues to strengthen food safety and manufacturing standards, encouraging the adoption of high-performance food grade release agents across processing industries.

Release Agents Market Dynamics

Market Trends

The market is witnessing notable shifts in sustainable formulation development, food safety compliance and demand for high performance processing aids. One of the key trends shaping the market is the growing adoption of bio based and clean label release agents reflecting changing preferences toward safer ingredients, sustainability and improved processing efficiency. Another emerging trend is the development of multifunctional release agents with enhanced lubrication and anti-sticking performance, driven by technological innovation and stricter regulatory compliance. These developments are encouraging companies to focus on customized formulations, clean production processes, and value-added solutions, thereby redefining competitive dynamics within the market.

Growth Drivers

The growth of the market is largely supported by expanding processed food production which continues to generate consistent demand across bakery, confectionery, dairy and convenience food applications. Increasing investments in food manufacturing facilities and industrial processing infrastructure are further accelerating market expansion. Additionally, growing demand for efficient industrial molding processes is playing a crucial role in boosting adoption. As manufacturers prioritize operational efficiency, product quality and regulatory compliance demand for high performance release agents is expected to remain strong throughout the forecast period.

Market Restraints / Challenges

Despite favorable growth prospects, the market faces few specific hindrances to growth. Fluctuating prices of vegetable oils, specialty chemicals and raw materials continue to affect manufacturing costs and profitability particularly among small and medium sized producers. Furthermore, stringent food safety regulations and formulation compliance requirements pose operational challenges for manufacturers and suppliers. Dependence on specialized raw materials and regulatory approvals can increase development costs and delay product commercialization, impacting market expansion during periods of regulatory change.

Market Opportunities

The market presents significant opportunities in clean label and bio-based release agent formulations, particularly driven by increasing consumer preference for natural ingredients and sustainable food processing solutions. Companies offering environmentally responsible, high-performance formulations are well positioned to capture incremental demand from food manufacturers and industrial processors. Another key opportunity lies in advanced industrial manufacturing applications where increasing investments in specialty molding processes and high-performance materials are creating avenues for stronger profitability and long-term customer relationships. Advancements in formulation technologies, automation and precision processing are also expected to improve manufacturing efficiency and product performance.

Global Release Agents Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 1.4 Billion |

|

Revenue Forecast in 2035 |

USD 3.1 Billion |

|

Growth Rate |

8.3% |

|

Segments Covered in the Report |

Type, Form, Source, End Use |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

AAK AB, Archer Daniels Midland Company, Associated British Foods PLC, Avatar Corporation, Cargill, Dübör Groneweg GmbH & Co. KG, IFC Solutions, Inc., Lallemand, Masterol Foods Pty Ltd, Par-Way Tryson Company, Puratos Group NV, The Bakels Group |

|

Customization |

Available upon request |

Release Agents Market Segmentation

By Type

Water based release agents accounted for the largest market share of approximately 48% in 2025 and are projected to grow at an estimated 8.5% CAGR through 2035 supported by lower environmental impact, improved worker safety and increasing adoption across food processing and industrial molding applications.

Bio based and oil-based release agents are expected to register the fastest growth at around 9.0% CAGR during the forecast period as growing demand for sustainable processing solutions, clean label food production and environmentally responsible industrial chemicals continues to strengthen adoption.

By Form

Liquid release agents held the largest market share of approximately 57% in 2025 and are expected to expand at nearly 8.2% CAGR through 2035 due to its ease of application, uniform surface coverage and widespread use across bakery, confectionery, rubber, plastic, and composite manufacturing industries.

Spray release agents are anticipated to witness the fastest growth at an estimated 8.8% CAGR during the forecast period due to their superior dispensing accuracy, reduced material waste and compatibility with automated manufacturing lines that are supporting increased adoption across modern processing facilities.

By Source

Synthetic release agents accounted for the largest market share of approximately 62% in 2025 and are projected to grow at around 8.0% CAGR through 2035 due to their established industrial performance, cost effectiveness, and broad application across molding and food processing.

Bio based release agents are projected to record the fastest growth at nearly 9.2% CAGR during the forecast period due to increasing sustainability goals, regulatory support for environmentally responsible products and rising consumer preference for natural ingredients are accelerating adoption.

By End Use

Food processing accounted for the highest revenue share of approximately 39% in 2025 and is expected to expand at nearly 8.4% CAGR through 2035 due to strong demand from bakery, confectionery, dairy, and processed food manufacturing.

Composites are expected to register the fastest growth at around 9.1% CAGR during the forecast period supported by increasing use of lightweight materials across aerospace, automotive and wind energy industries. Rubber, plastics, concrete, and other industrial applications continue to contribute steady demand as manufacturers seek higher production efficiency and improved surface quality.

Regional Insights

North America

North America accounted for approximately 30% of the market in 2025 and is projected to expand at an estimated 8.1% CAGR through 2035 due to advanced food processing industries, well established industrial manufacturing and strict food safety regulations across the United States and Canada. Strong demand from commercial bakeries, processed food manufacturers and composite material producers continues to support regional growth. Government regulations combined with growing demand for sustainable processing solutions, are encouraging investments in bio-based release agents and advanced manufacturing technologies.

Europe

Europe represented about 24% of the market in 2025 and is expected to register nearly 8.4% CAGR during the forecast period due to stringent environmental regulations, expanding bakery production and increasing adoption of sustainable food processing technologies across Germany, France, Italy and the United Kingdom. The European Food Safety Authority (EFSA) continues to support food safety and compliance measures that encourage the use of approved processing ingredients and food contact materials.

Asia Pacific

Asia Pacific accounted for approximately 22% of the global market in 2025 and is anticipated to grow at around 8.8% CAGR through 2035 supported by expanding food manufacturing, growing industrialization and increasing demand from bakery, confectionery, plastics and composite industries across China, India, Japan, and Southeast Asia. According to the Food and Agriculture Organization (FAO), rapid urbanization and increasing processed food consumption continue to strengthen manufacturing investments throughout the region.

Rest of the World

The Rest of the World, including Latin America, the Middle East, and Africa, accounted for approximately 24% of the market in 2025 and is projected to grow at nearly 8.6% CAGR through 2035 because increasing investments in food processing infrastructure, industrial manufacturing and packaged food production continue to support regional demand. According to the Food and Agriculture Organization (FAO), investments in food processing and agricultural modernization continue to create long term opportunities across developing regions.

Competitive Landscape / Company Insights

The market is moderately competitive with global and regional players focusing on product innovation, sustainable formulations, pricing strategies and geographic expansion to strengthen their market position. Companies are increasingly investing in research and development, bio-based technologies and regulatory compliant product portfolios to address evolving customer requirements. The U.S. Food and Drug Administration (FDA) and the Food and Agriculture Organization (FAO) continue to support food safety, sustainable manufacturing and efficient processing practices encouraging innovation across the release agents industry.

Mini Profiles

AAK AB focuses on specialty vegetable oils and food processing solutions, supported by extensive global manufacturing, strong customer relationships, and expertise in sustainable ingredient development.

Bakels Group operates in niche bakery ingredient segments, emphasizing high performance release agents, baking efficiency, product consistency, and customized solutions for commercial bakeries worldwide.

Cargill leverages global manufacturing capabilities, integrated supply chains, and advanced food ingredient expertise to strengthen its presence in release agents and food processing applications.

Dübör Groneweg GmbH & Co. KG specializes in bakery release agents and pan oils, supported by innovative formulations, technical expertise, and a strong presence across European food processing markets.

IFC Solutions Inc. focuses on food grade release agents and processing aids, supported by customized formulations, technical service capabilities, and long-standing relationships with industrial food manufacturers.

Key Players

- AAK AB

- Archer Daniels Midland Company

- Associated British Foods PLC

- Avatar Corporation

- Cargill

- Dübör

- Groneweg

- GmbH & Co. KG

- IFC Solutions, Inc.

- Lallemand

- Masterol

- Foods Pty Ltd

- Par-Way Tryson Company

- Puratos

- Group NV

- The Bakels Group

Recent Developments

In August 2025, Archer Daniels Midland Company expanded its specialty food ingredient portfolio with new customer focused innovation initiatives for food manufacturers. The company continued strengthening sustainable ingredient solutions supporting bakery and food processing applications.

In October 2025, Avatar Corporation highlighted expanded production capabilities for specialty food processing ingredients and release agent solutions. The company continued investing in customized formulations to support commercial bakery and industrial food manufacturers.

In August 2025, Masterol Foods Pty Ltd continued expanding its bakery processing solutions to meet growing demand from commercial baking operations. The company strengthened its portfolio of food grade release agents designed to improve production efficiency.

In September 2025, Par-Way Tryson Company expanded its range of food release agent solutions for industrial bakery and food processing customers. The company continued emphasizing high performance formulations that improve processing efficiency and product consistency.

In June 2025, Puratos Group NV opened a new industrial pilot bakery in partnership with AMF Bakery Systems to accelerate product development and commercial innovation. The facility enhances testing capabilities for bakery ingredients and processing solutions used across commercial baking operations.

Global Release Agents Market Coverage

Type Insight and Forecast 2026 - 2035

- Water Based

- Solvent Based

- Oil Based

Form Insight and Forecast 2026 - 2035

- Liquid

- Spray

- Paste

- Solid

Source Insight and Forecast 2026 - 2035

- Synthetic

- Bio Based

End Use Insight and Forecast 2026 - 2035

- Food Processing

- Rubber

- Plastics

- Composites

- Concrete

- Others

Global Release Agents Market by Region

- North America

- By Type

- By Form

- By Source

- By End Use

- By Country - U.S., Canada, Mexico

- Europe

- By Type

- By Form

- By Source

- By End Use

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Type

- By Form

- By Source

- By End Use

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Type

- By Form

- By Source

- By End Use

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Release Agents Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Type

1.2.2. By

Form

1.2.3. By

Source

1.2.4. By

End Use

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Type

5.1.1. Water Based

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Solvent Based

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Oil Based

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Form

5.2.1. Liquid

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Spray

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Paste

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Solid

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.3. By Source

5.3.1. Synthetic

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Bio Based

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By End Use

5.4.1. Food Processing

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Rubber

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Plastics

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Composites

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Concrete

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

5.4.6. Others

5.4.6.1. Market Definition

5.4.6.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Type

6.2. By

Form

6.3. By

Source

6.4. By

End Use

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Type

7.2. By

Form

7.3. By

Source

7.4. By

End Use

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Type

8.2. By

Form

8.3. By

Source

8.4. By

End Use

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Type

9.2. By

Form

9.3. By

Source

9.4. By

End Use

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

AAK AB

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Archer Daniels Midland Company

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Associated British Foods PLC

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Avatar Corporation

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Cargill

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Dübör Groneweg GmbH & Co. KG

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

IFC Solutions, Inc.

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Lallemand

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Masterol Foods Pty Ltd

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Par-Way Tryson Company

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

Puratos Group NV

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

10.12.

The Bakels Group

10.12.1.

Snapshot

10.12.2.

Overview

10.12.3.

Offerings

10.12.4.

Financial

Insight

10.12.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Release Agents Market