Asia-Pacific Beauty Devices Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Type (Cleansing devices, Hair removal devices, Skin dermal rollers, Acne devices, Light and led therapy and photo rejuvenation devices, Oxygen and steamer devices, Hair growth devices, Cellulite reduction devices, Others), by End User (Beauty clinics, Spas and salons, At home, Others)

| Status : Published | Published On : Feb, 2026 | Report Code : VRHC1330 | Industry : Healthcare | Available Format :

|

Page : 147 |

Asia-Pacific Beauty Devices Market Overview

The Asia Pacific beauty devices market which was valued at approximately USD 4.55 billion in 2025 and is estimated to rise further up to almost USD 5.32 billion by 2026, is projected to reach around USD 21.66 billion in 2035, expanding at a CAGR of about 16.8% during the forecast period from 2026 to 2035.

Market expansion is supported by rising consumer inclination toward noninvasive aesthetic solutions, increasing penetration of home use beauty technologies, and steady innovation in skin rejuvenation, hair removal, and anti-aging devices. Improving affordability of advanced devices and rapid urbanization across developing economies are further contributing to sustained industry growth.

Market development is also reinforced by growing awareness of skin health, hygiene, and aging related concerns, supported indirectly by guidance from government backed public health institutions. The World Health Organization highlights the importance of safe use of personal care technologies, early dermatological intervention, and preventive skin management, which strengthens consumer confidence in regulated beauty devices. Additionally, government initiatives promoting medical device regulation harmonization, local manufacturing, and digital health adoption are supporting industry expansion. These factors are accelerating adoption across key markets including China, Japan, and India, where expanding middle class populations, rising disposable income, and evolving lifestyle preferences continue to drive long term market growth.

Asia-Pacific Beauty Devices Market Dynamics

Market Trends

The industry is experiencing notable shifts in technology usage and consumer behavior, driven by growing preference for noninvasive, home use, and clinically validated aesthetic solutions. One of the key trends shaping the market is the increasing integration of advanced technologies such as radiofrequency, light-based systems, and microcurrent platforms, reflecting consumer inclination toward efficiency, safety, and visible outcomes. Another emerging trend is the rising demand for multifunctional and portable devices, supported by lifestyle changes, urban living patterns, and expanding digital retail penetration. Guidance from government backed public health bodies, including recommendations on safe personal care device usage and skin health awareness issued by international health authorities, is influencing product standardization, quality compliance, and innovation focus across the regional market.

Growth Drivers

The growth of the market is largely supported by rising awareness of skin health, aging management, and personal grooming, which continues to generate consistent demand across both urban and semi urban consumer segments. Increasing investments in local manufacturing, medical device infrastructure, and technology localization initiatives across major economies are further accelerating market expansion. Additionally, improving disposable income levels and growing acceptance of preventive aesthetic care are playing a crucial role in boosting adoption. As consumers increasingly prioritize performance, convenience, and long-term skin maintenance, demand for advanced beauty devices remains strong. Public health initiatives promoting dermatological awareness and hygiene standards, supported by government backed healthcare programs, are reinforcing consumer confidence and supporting sustained market growth.

Market Restraints / Challenges

Despite favorable growth prospects, the market faces certain challenges that may limit its expansion. Regulatory complexity related to device safety, certification, and compliance continues to affect time to market and operational costs, particularly for smaller manufacturers and new entrants. Government health agencies emphasize stringent quality control and post market surveillance for personal care and aesthetic devices, increasing compliance burdens. Furthermore, dependence on imported components, advanced electronics, and specialized manufacturing inputs poses cost and supply chain challenges. Fluctuations in logistics costs and limited availability of skilled technical labor can lead to pricing pressures and scalability constraints, impacting overall market performance during periods of economic volatility.

Market Opportunities

The market presents significant opportunities in the expansion of affordable and technologically advanced home use beauty devices, driven by demographic shifts such as a growing middle-class population and increased focus on self-care. Companies offering customizable, user friendly, and clinically aligned solutions are well positioned to capture incremental demand from younger consumers and aging populations alike. Another key opportunity lies in premium and digital enabled product categories, where rising investments in smart features, connectivity, and data driven personalization are creating avenues for higher margins. Government initiatives supporting digital health ecosystems, medical device innovation, and local production capabilities are expected to further enhance customer engagement and long-term adoption across the region.

Asia-Pacific Beauty Devices Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 4.55 Billion |

|

Revenue Forecast in 2035 |

USD 21.66 Billion |

|

Growth Rate |

16.8% |

|

Segments Covered in the Report |

By Type, By End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

China, India, Japan, Rest of Asia Pacific |

|

Key Companies |

Home Skinovations Ltd., Koninklijke Philips N.V., L’Oreal SA, Lumenis Ltd., Panasonic Corporation, Photomedax Inc., Syneron-Candela, The Procter & Gamble Company, TRIA Beauty Inc |

|

Customization |

Available upon request |

Asia-Pacific Beauty Devices Market Segmentation

By Type

Hair removal devices accounted for the largest share of approximately 24% in 2025, driven by high procedure frequency, long device lifecycles, and strong demand from both professional clinics and at-home users. Regulatory approvals and safety oversight by authorities such as China’s National Medical Products Administration (NMPA), Japan’s Ministry of Health, Labor and Welfare (MHLW), and Australia’s Therapeutic Goods Administration (TGA) support widespread commercialization and sustained adoption across Asia Pacific.

Light/LED therapy and photo rejuvenation devices are expected to register one of the fastest growth rates at a CAGR of around 17.1% from 2026 to 2035, supported by rising demand for non-invasive anti-aging and pigmentation treatments. Government-recognized device classification frameworks under Japan’s Pharmaceuticals and Medical Devices Agency (PMDA) and South Korea’s Ministry of Food and Drug Safety (MFDS) encourage clinical usage and consumer confidence.

Cleansing devices are projected to grow at a CAGR of approximately 15.3%, driven by increasing skincare awareness and daily-use applicability. Consumer device safety standards and cosmetic device monitoring programs promoted by MFDS and regional public health authorities across Southeast Asia continue to reinforce adoption.

Acne devices, hair growth devices, skin dermal rollers, cellulite reduction devices, oxygen and steamer devices, and other niche beauty devices collectively accounted for the remaining share of the market in 2025 and are expected to grow at a moderate CAGR of around 14.2%. Growth across these segments is supported by expanding dermatology services, rising self-care trends, and harmonized cosmetic device regulations implemented by government health agencies across Asia Pacific.

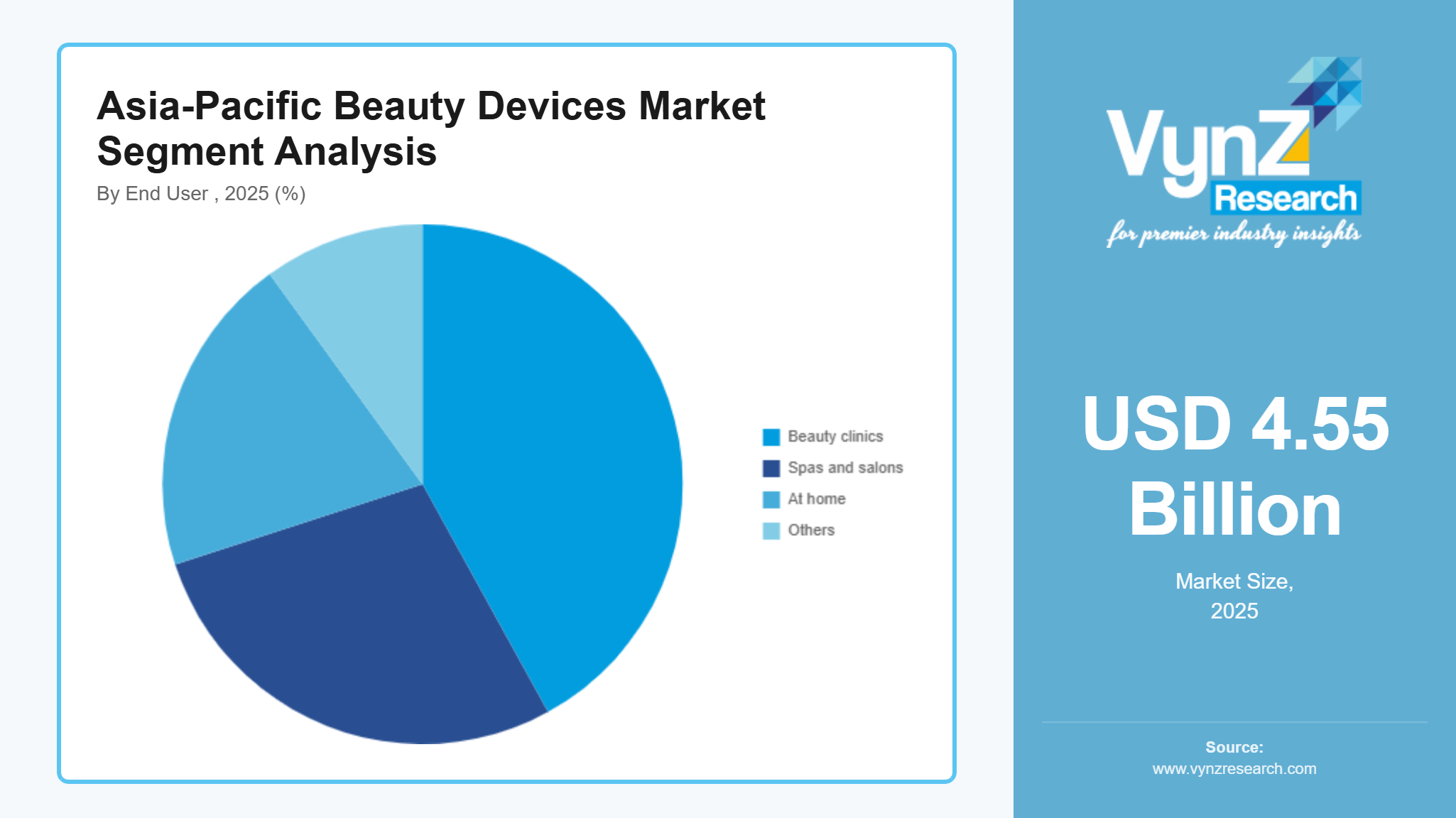

By End User

Beauty clinics accounted for the largest end-user share at approximately 42% in 2025, supported by high patient throughput, access to advanced aesthetic equipment, and structured service delivery. Licensing standards and clinical practice regulations issued by China’s National Health Commission, Japan’s MHLW, and regional health ministries reinforce procedural safety and sustained institutional demand.

The at-home segment is expected to witness the fastest growth at a CAGR of nearly 18.3% during 2026–2035, driven by rising disposable incomes, convenience-oriented consumer behavior, and growing availability of government-approved consumer beauty devices. Regulatory compliance frameworks enforced by TGA, MFDS, and CDSCO (India) support market expansion and product credibility.

Spas and salons, along with other end users, collectively represented the remaining market share in 2025 and are projected to grow at a steady CAGR of around 14.6%. Growth is supported by wellness tourism, urban lifestyle trends, and service-sector compliance guidelines issued by regional government authorities across Southeast Asia and Oceania.

Regional Insights

China

China accounted for approximately 28% of the market in 2025, driven by rapid urbanization, a large consumer base, and strong demand for advanced skincare and aesthetic solutions. Major metropolitan areas such as Beijing, Shanghai, Guangzhou, and Shenzhen continue to lead adoption across dermatology clinics, medical aesthetics centers, and home-use consumers.

Government-supported healthcare modernization initiatives, consumer safety regulations for electronic personal care products, and public awareness programs related to skin health are encouraging investments in technologically advanced beauty devices. Expansion of domestic manufacturing capabilities and strong penetration of e-commerce platforms further strengthen market growth.

India

India represented around 18% of the Asia Pacific market in 2025, supported by rising disposable incomes, growing awareness of personal grooming, and increasing acceptance of non-invasive aesthetic treatments. Cities including Mumbai, Delhi, Bengaluru, and Chennai are emerging as key demand centers for professional and at-home beauty devices.

Government-backed initiatives focused on healthcare accessibility, skill development in wellness and cosmetology services, and regulatory oversight of medical and cosmetic devices are supporting market expansion. Growth of organized retail, digital marketplaces, and dermatology clinics is contributing to sustained demand across both consumer and professional end users.

Japan

Japan accounted for approximately 15% of the market in 2025, driven by an aging population, high standards of personal care, and strong preference for technologically sophisticated beauty solutions. Urban centers such as Tokyo and Osaka remain key hubs for innovation and adoption across clinics and premium consumer segments.

Government-supported public health programs, strict product quality regulations, and emphasis on preventive skincare are encouraging adoption of safe and advanced beauty devices. Continuous innovation in home-use technologies and integration of smart features support steady market growth.

Rest of Asia Pacific

The Rest of Asia Pacific, including South Korea, Australia, Southeast Asia, and other emerging economies, collectively accounted for approximately 14% of the market in 2025. Growth is supported by rising consumer awareness, expanding middle-class populations, and increasing availability of professional aesthetic services in urban centers.

Government-backed healthcare development initiatives, regulatory frameworks for cosmetic and medical devices, and public education programs related to skin and hair health are promoting adoption across these markets. The remaining market demand not specifically covered by China, India, and Japan is included within this segment, representing diverse economies with long-term growth potential.

Together, China, India, Japan, and the Rest of Asia Pacific account for approximately 75% of the total market, with the remaining share distributed across smaller and emerging regional markets within Asia-Pacific.

Competitive Landscape / Company Insights

The market is moderately to highly competitive, with global and regional players focusing on product innovation, pricing strategies, and geographic expansion. Key vendors are investing in R&D, certification compliance, and digital capabilities to enhance safety, performance, and market reach. Adoption is supported by regulatory frameworks enforced by the National Medical Products Administration (China), Central Drugs Standard Control Organization (India), Health Sciences Authority (Singapore), and expanded regulatory coordination initiatives led by the Pharmaceuticals and Medical Devices Agency (Japan), which encourage companies to strengthen market position and expand regional penetration.

Mini Profiles

Home Skinovations Ltd. focuses on at-home aesthetic devices, supported by strong consumer branding, direct-to-consumer distribution, and clinically validated technologies addressing hair removal and skin rejuvenation needs.

Koninklijke Philips N.V. operates across mass and premium beauty device segments, emphasizing performance-driven innovation, strong R&D capabilities, and extensive regional distribution networks across Asia Pacific consumer electronics markets.

L’Oreal SA focuses on technology-enabled beauty solutions, supported by strong brand recognition, dermatology-backed product development, and integration of professional-grade devices into consumer skincare ecosystems.

Panasonic Corporation operates in the mass and mid-range segments, emphasizing engineering reliability, product safety, and wide retail penetration, supported by established consumer electronics manufacturing and regional supply chain efficiency.

TRIA Beauty, Inc. focuses on premium at-home laser-based devices, leveraging clinically tested technologies, regulatory approvals, and digital-first distribution strategies to strengthen presence among tech-savvy beauty consumers.

Key Players

- Home Skinovations Ltd.

- Koninklijke Philips N.V.

- L’Oreal SA

- Lumenis Ltd.

- Panasonic Corporation

- Photomedax Inc.

- Syneron-Candela

- The Procter & Gamble Company

- TRIA Beauty, Inc.

Recent Developments

In January 2026, In Hyderabad, L'Oréal has invested €350 million to create its first global hub for AI-powered beauty technology. Around 2,000 advanced tech jobs are anticipated to be created in Hyderabad as a result of the investment, which is scheduled to be implemented until 2030 to develop and scale AI, digital engineering, and next-generation beauty tech capabilities.

In December 2025, SpectraWAVE, Inc., a pioneer in angiography-based physiology evaluations, enhanced vascular imaging (EVI) of coronary arteries, and the application of artificial intelligence (AI) in medical imaging, has agreed to be acquired by Royal Philips, a world leader in health technology [3]. With over 300 million cases of coronary artery disease, the most common form of heart disease, SpectraWAVE's intravascular imaging and physiological evaluation technologies offer patients cutting-edge treatment options.

In November 2025, Leading energy-based medical device manufacturer Lumenis Be. Ltd. revealed the most recent version of its ground-breaking multi-application aesthetic platform, the Stellar M22 with XPL Technology, which is authorized to treat more than 30 indications and is driven by four state-of-the-art technologies. For patients of every age, gender, or skin type, Stellar M22 offers exceptional patient outcomes and flexible treatment procedures in a single, small device.

In September 2025, Panasonic Industry Co., Ltd., a subsidiary of the Panasonic Group, has plans to significantly increase the amount of MEGTRON multi-layer circuit board materials it can produce worldwide. In order to satisfy the increasing demand in the markets for AI servers and ICT infrastructure, the company intends to invest around 17 billion yen to build a new manufacturing facility at its Ayutthaya Plant in Thailand in order to facilitate the quick adoption of AI technology.

Asia-Pacific Beauty Devices Market Coverage

Type Insight and Forecast 2026 - 2035

- Cleansing devices

- Hair removal devices

- Skin dermal rollers

- Acne devices

- Light and led therapy and photo rejuvenation devices

- Oxygen and steamer devices

- Hair growth devices

- Cellulite reduction devices

- Others

End User Insight and Forecast 2026 - 2035

- Beauty clinics

- Spas and salons

- At home

- Others

Asia-Pacific Beauty Devices Market by Region

- China

- By Type

- By End User

- Japan

- By Type

- By End User

- India

- By Type

- By End User

- South Korea

- By Type

- By End User

- Vietnam

- By Type

- By End User

- Thailand

- By Type

- By End User

- Malaysia

- By Type

- By End User

- Rest of Asia-Pacific

- By Type

- By End User

Table of Contents for Asia-Pacific Beauty Devices Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Type

1.2.2. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Asia-Pacific Market Estimate and Forecast

4.1. Asia-Pacific Market Overview

4.2. Asia-Pacific Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Type

5.1.1. Cleansing devices

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Hair removal devices

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Skin dermal rollers

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Acne devices

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Light and led therapy and photo rejuvenation devices

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.1.6. Oxygen and steamer devices

5.1.6.1. Market Definition

5.1.6.2. Market Estimation and Forecast to 2035

5.1.7. Hair growth devices

5.1.7.1. Market Definition

5.1.7.2. Market Estimation and Forecast to 2035

5.1.8. Cellulite reduction devices

5.1.8.1. Market Definition

5.1.8.2. Market Estimation and Forecast to 2035

5.1.9. Others

5.1.9.1. Market Definition

5.1.9.2. Market Estimation and Forecast to 2035

5.2. By End User

5.2.1. Beauty clinics

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Spas and salons

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. At home

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Others

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

6. China Market Estimate and Forecast

6.1. By

Type

6.2. By

End User

7. Japan Market Estimate and Forecast

7.1. By

Type

7.2. By

End User

8. India Market Estimate and Forecast

8.1. By

Type

8.2. By

End User

9. South Korea Market Estimate and Forecast

9.1. By

Type

9.2. By

End User

10. Vietnam Market Estimate and Forecast

10.1. By

Type

10.2. By

End User

11. Thailand Market Estimate and Forecast

11.1. By

Type

11.2. By

End User

12. Malaysia Market Estimate and Forecast

12.1. By

Type

12.2. By

End User

13. Rest of Asia-Pacific Market Estimate and Forecast

13.1. By

Type

13.2. By

End User

14. Company Profiles

14.1.

Home Skinovations Ltd.

14.1.1.

Snapshot

14.1.2.

Overview

14.1.3.

Offerings

14.1.4.

Financial

Insight

14.1.5.

Recent

Developments

14.2.

Koninklijke Philips N.V.

14.2.1.

Snapshot

14.2.2.

Overview

14.2.3.

Offerings

14.2.4.

Financial

Insight

14.2.5.

Recent

Developments

14.3.

Lumenis Ltd.

14.3.1.

Snapshot

14.3.2.

Overview

14.3.3.

Offerings

14.3.4.

Financial

Insight

14.3.5.

Recent

Developments

14.4.

L’Oreal SA

14.4.1.

Snapshot

14.4.2.

Overview

14.4.3.

Offerings

14.4.4.

Financial

Insight

14.4.5.

Recent

Developments

14.5.

Panasonic Corporation

14.5.1.

Snapshot

14.5.2.

Overview

14.5.3.

Offerings

14.5.4.

Financial

Insight

14.5.5.

Recent

Developments

14.6.

Photomedax Inc.

14.6.1.

Snapshot

14.6.2.

Overview

14.6.3.

Offerings

14.6.4.

Financial

Insight

14.6.5.

Recent

Developments

14.7.

Syneron-Candela

14.7.1.

Snapshot

14.7.2.

Overview

14.7.3.

Offerings

14.7.4.

Financial

Insight

14.7.5.

Recent

Developments

14.8.

The Procter & Gamble Company

14.8.1.

Snapshot

14.8.2.

Overview

14.8.3.

Offerings

14.8.4.

Financial

Insight

14.8.5.

Recent

Developments

14.9.

TRIA Beauty, Inc.

14.9.1.

Snapshot

14.9.2.

Overview

14.9.3.

Offerings

14.9.4.

Financial

Insight

14.9.5.

Recent

Developments

15. Appendix

15.1. Exchange Rates

15.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Asia-Pacific Beauty Devices Market