Medical Coding Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Classification System (International Classification of Diseases (ICD), Current Procedural Terminology (CPT), Healthcare Common Procedure Coding System (HCPCS), Systematized Nomenclature of Medicine – Clinical Terms (SNOMED CT)), by Offering (Outsourced Medical Coding Services, In-house Medical Coding Services, Software Solutions, AI / Automation Tools), by Delivery Mode (Cloud-based Solutions, On-premise Coding Systems, Hybrid / Managed Services), by Application (Radiology Coding, Oncology Coding, Cardiology Coding, Pathology Coding, Surgery / Procedure Coding), by Function (Code Assignment and Validation, Analytics and Reporting, Compliance and Audit Management, Revenue Cycle Optimization, Data Quality Management), by End User (Hospitals and Large Healthcare Facilities, Physician Practices, Clinics, and Diagnostic Centers, Insurance Providers and Payers, Specialty and Ambulatory Care Center)

| Status : Published | Published On : Mar, 2026 | Report Code : VRHC1329 | Industry : Healthcare | Available Format :

|

Page : 179 |

Global Medical Coding Market Overview

The global medical coding market which was valued at approximately USD 9.32 billion in 2025 and is estimated to reach around USD 10.23 billion in 2026, is projected to reach roughly USD 23.74 billion by 2035, expanding at a CAGR of about 9.8% during the forecast period from 2026 to 2035.

The market expands because more healthcare facilities use electronic health record systems and more hospitals need to comply with regulations that mandate precise clinical documentation. Healthcare organizations need effective revenue cycle management solutions which automated coding systems and AI-powered tools provide. Market growth in North America, Europe and Asia Pacific Oceania region stems from hospitals, clinics, insurance systems needing accurate billing and compliance solutions. Ongoing health IT modernization projects and digital health initiatives receive government funding. The World Health Organization states that standardized medical coding improves healthcare data interoperability and patient safety while public health agencies establish coding standards and offer financial incentives to promote advanced coding technology adoption. The combination of health infrastructure funding and reimbursement policy changes drives market expansion for regions that use structured data exchange and compliance programs to improve their clinical and administrative processes.

Medical Coding Market Dynamics

Market trends

The medical coding sector is experiencing major changes because digital health solutions become essential and organizations need to follow regulations and more businesses adopt automation. The industry is currently developing through the introduction of automated and AI-enhanced coding systems which provide better efficiency and precise results while decreasing administrative tasks according to worldwide digital health frameworks approved by leading public health organizations. Healthcare systems now need to share health data across different platforms which leads organizations to select cloud-based health information management systems as their primary solution. The current market changes drive vendors to build solution portfolios which deliver integrated analytics real-time coding validation and quality assurance capabilities that reshape medical coding competition between vendors while enabling structured clinical data sharing. Public health agencies together with national digital health frameworks maintain their position that standardized coded health information forms the essential foundation to assess health system quality and safety and operational performance.

Growth drivers

The market expansion finds its primary driver in the ongoing requirement to boost revenue cycle performance together with billing compliance needs which create continuous requirements from medical facilities and insurance companies. Market growth receives acceleration from organizations upgrading their health IT infrastructure and expanding their electronic health record systems which receive support from government funding programs that promote interoperability development. The healthcare sector experiences growth through two main forces which include regulatory requirements that demand updated coding standards together with quality reporting regulations that organizations need to follow to enhance their coding accuracy and operational productivity.

Market Restraints / Challenges

The market displays a positive growth projection but it encounters multiple obstacles which will hinder its upward progress. The main obstacle for organizations stems from the expensive and complicated process of moving their existing systems to new coding platforms which particularly affects smaller providers and resource-limited organizations because it hinders their ability to adopt new technology and grow their operations. The workforce experiences operational difficulties because of two factors which include the lack of qualified coders and the need for specialized workers, which creates backlogged work and inconsistent quality during times of increased clinical demand and economic instability.

Market opportunities

The market provides major growth prospects through AI-based coding automation systems which use predictive analytics to handle rising clinical data and advanced value-based care requirements. The healthcare sector requires solutions which can expand to handle rising demand from integrated delivery networks and government health systems and payers who want to enhance their resource management functions. The development of remote coding services and cloud-based coding abilities presents, as businesses invest in secure digital platforms and create outsourcing frameworks, a new market opening that enables them to build enduring relationships with clients. The development of natural language processing technology together with intelligent workflow solutions will boost coding efficiency while decreasing errors, which will improve clinical documentation quality and sustain market expansion.

Global Global Medical Coding Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 9.32 Billion |

|

Revenue Forecast in 2035 |

USD 23.74 Billion |

|

Growth Rate |

9.8% |

|

Segments Covered in the Report |

Classification System, Offering, Delivery Mode, Application, Function, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

3M Health Information Systems, AGS Health, Access Healthcare, Athenahealth, Cognizant, eClinicalWorks, GeBBS Healthcare Solutions, iMedX, Inc., Nuance Communications (Microsoft), Optum360 |

|

Customization |

Available upon request |

Medical Coding Market Segmentation

By Classification System

The international classification of diseases (ICD) segment accounted for the largest share of the medical coding market in 2025, representing approximately 48% of total revenue. The dominance of this segment results from the fact that hospitals and healthcare providers have adopted regulatory requirements while the system requires extended periods between updates and the system is capable of producing different types of clinical documentation and medical reports. The use of ICD coding has become the standard practice for North America, Europe and Asia Pacific because healthcare organizations must comply with coding regulations while also meeting reimbursement requirements.

The current procedural terminology (CPT) segment is projected to register the fastest growth, with an estimated CAGR of 11.8% during the forecast period from 2026 to 2035. The expansion of this market segment will continue to rise because more outpatient procedures take place and more organizations adopt digital coding platforms which will enable them to connect with AI-assisted billing solutions.

By Offering

The largest market share in 2025 was held by outsourced medical coding services which generated about 52% of revenue. This service became popular because it helps organizations save operating costs while bringing them trained coders and helping them meet regulatory standards. Healthcare facilities in developing and developed regions use outsourced services to ensure their coding work is accurate while they need to decrease administrative work and safeguard their reimbursement process.

The estimated growth rate for in-house coding services from 2026 to 2035 is expected to reach 12.2%. The growth of this market will proceed because organizations will adopt automated coding platforms and staff members will undergo upskilling programs and organizations will require real-time coding validation to achieve their quality reporting goals. The segment of digital health infrastructure expands because organizations invest in digital health infrastructure and the government encourages them to develop systems that allow users to share coding information.

By Delivery Mode

The largest deployment segment of cloud-based medical coding solutions achieved 55% market share in 2025. Healthcare providers now use those platforms because they provide scalable security and remote access capabilities which help them achieve operational efficiency while meeting their regulatory obligations. Cloud-based coding solutions gain wider adoption across major markets because government initiatives support telehealth, electronic health records and digital health interoperability.

The health care facilities which require tailored system connection and system security for their internal data and need to follow regional law requirements will drive the on-premise coding system market to grow at 11.7% from 2026 until 2035. Public health agency support for clinical documentation together with modernization of existing infrastructure will help expand this segment of the market.

By Application

The largest share of specialty applications market in 2025 went to radiology coding which generated about 38% of segment revenue. The procedure volumes lead to this situation because code requirements need verification from both insurance companies and government health programs to meet their documentation needs. The growth of this segment comes from national health authorities who require diagnostic imaging procedures to achieve correct coding.

The market for oncology coding will experience its highest growth rate between 2026 and 2035 because the field will see a 12.5% increase in market size. The rising cancer cases together with precision medicine becoming more popular and ai-assisted coding platforms being implemented have led to operational expansion. Reimbursement policies from the government which support cancer registries and specialized treatment coding create extra demand from hospitals and specialty centers across North America, Europe and Asia Pacific.

By Function

The code assignment and validation process became the primary workflow activity which generated approximately 50% of all revenues in 2025. Public health programs promote standardized coding practices and audit-ready documentation which help the segment gain popularity throughout healthcare networks across the country.

The analytics and reporting workflows show projected growth of 12% from 2026 until 2035. Government programs which promote data-driven decision-making and quality measurement lead to market growth which occurs through organizations using predictive analytics and performance monitoring and reimbursement optimization. The segment shows growth because organizations must follow regulations about value-based care and governmental reporting requirements.

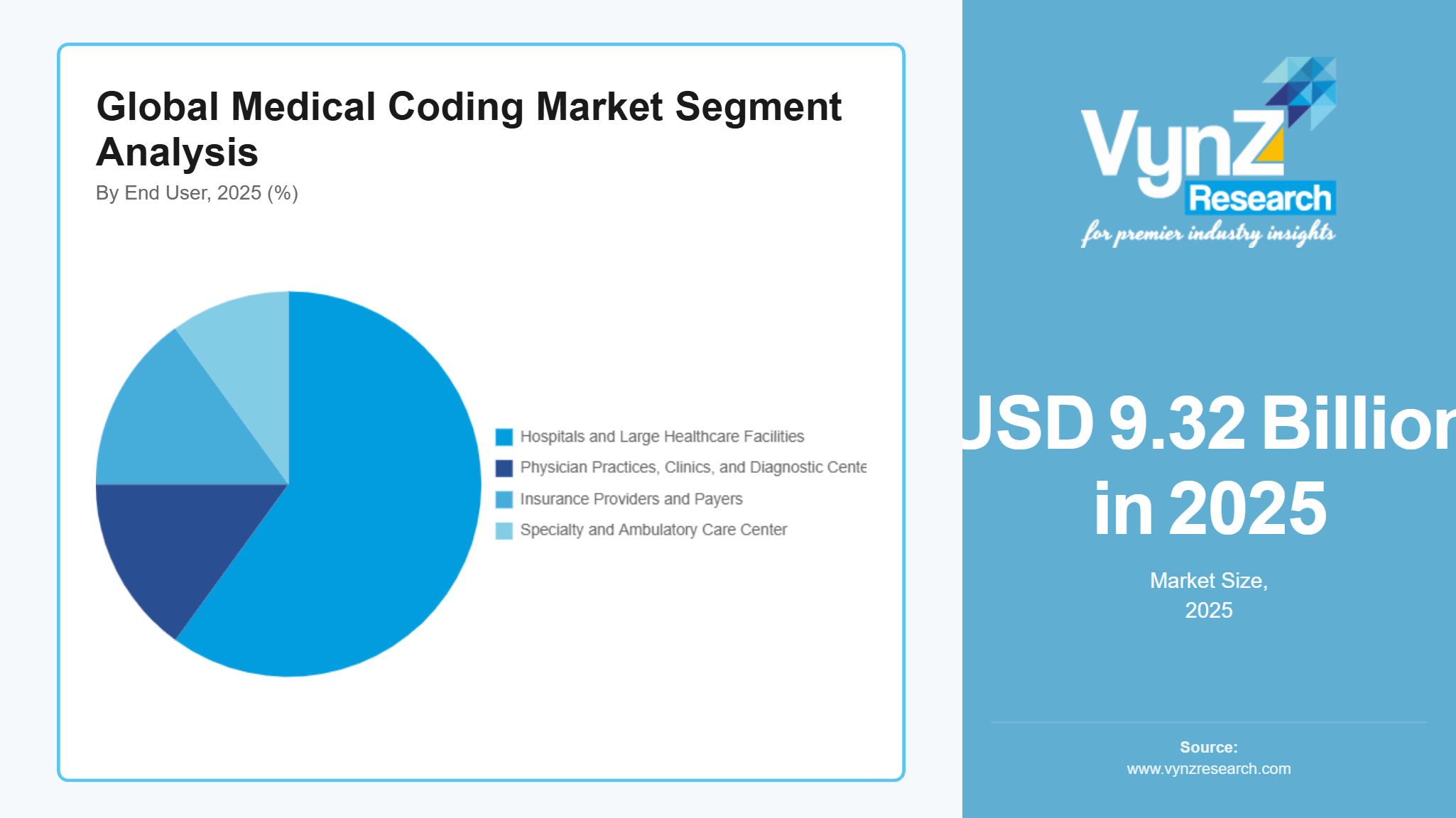

By End User

The largest segment of end-users in 2025 consisted of hospitals and large healthcare facilities which generated approximately 60% of the total market revenue. Their market share exceeds that of competitors because they attract many patients who need complex coding services which must meet both governmental health authority requirements and insurance company standards.

The field of physician practices clinics and diagnostic centers will expand the fastest according to projections which estimate a growth rate of 11.9% between 2026 and 2035. The need for precise billing and operational improvements and cloud-based systems together with AI-enabled coding solutions creates demand for growth from this market segment. Certified coders receive training through government training programs which together with reimbursement reforms and public health initiatives to improve documentation quality help smaller and mid-sized healthcare facilities adopt practices across the globe.

Regional Insights

North America

The market in North America reached a 30% share during 2025 because of high healthcare spending and advanced health IT systems and strict CMS and U.S. Department of Health & Human Services regulations. The hospitals and clinics and insurance providers in New York, Los Angeles and Chicago continue to adopt automated and AI-enabled coding solutions. Government-backed initiatives which promote EHR adoption and quality reporting and interoperability standards create additional reasons for organizations to invest in medical coding solutions.

Europe

The European market had a 23% market share during 2025 because its developed healthcare systems and European Medicines Agency (EMA) regulatory compliance and widespread use of standardized coding systems. The countries of Germany and the UK and France and Italy are implementing automated coding platforms across their hospitals and private clinics. Public health policies which focus on health information management and reimbursement optimization and digital health adoption create ongoing demand for their services.

Asia Pacific

The Asia Pacific market registered 18% share of the total market in 2025. The region experiences growth because Japan, China and India increase their healthcare spending, digital health adoption, and hospital infrastructure development. The hospitals and multispecialty clinics of Tokyo, Beijing and Mumbai serve as central locations for hospitals which provide advanced coding solutions. Government-backed digital health initiatives which include national EHR programs, interoperability standards and coder certification programs enable healthcare organizations to adopt modern coding technologies.

Rest of the World

The Rest of the World which includes Latin America, the Middle East and Africa accounted for 12% of the market in 2025. The healthcare infrastructure investments and urbanization and clinical documentation quality awareness create growth opportunities in these regions. Countries such as Brazil, South Africa and Saudi Arabia are progressively adopting digital and automated coding platforms while their market penetration stays below North America, Europe and Asia Pacific levels. Government health programs and national digital health strategies and training initiatives for clinical coders enable organizations to gradually implement digital health technology. T

The remaining demand which North America and Europe and Asia Pacific do not cover, is covered by the emerging markets with underserved regions that show potential for future growth.

Competitive Landscape / Company Insights

The market operates with moderate to high competition because international and regional companies focus on developing technological innovations and implementing workflow automation and expanding their business operations to new regions. The main companies of the market create AI-based coding systems together with their cloud solutions and their training programs for coders to improve their operational performance and their precision in work. The adoption of these programs receives support from government initiatives which include the EHR incentives from the U.S. Centers for Medicare & Medicaid Services (CMS), the national digital health strategies implemented in Europe and the health IT modernization initiatives that multiple Asian Pacific countries carry out to help companies build their market presence while they enhance their service capabilities.

Mini Profiles

AGS Health focuses on revenue cycle management and medical coding solutions, supported by advanced analytics platforms, strong client relationships, and global delivery centers, ensuring accurate coding and optimized reimbursement.

Cognizant leverages digital transformation, healthcare consulting, and strategic partnerships to expand market presence, offering integrated coding solutions, automation services, and scalable platforms across hospitals, insurers, and clinical providers globally.

eClinicalWorks operates in mass healthcare segments, emphasizing cloud-based EHR integration, automated coding accuracy, and patient management solutions, enabling clinics and hospitals to streamline operations and improve compliance efficiency.

GeBBS Healthcare Solutions focuses on coding, auditing, and RCM services, supported by multi-site

operations, skilled workforce, and AI-assisted platforms, enhancing coding accuracy and operational

efficiency for global healthcare clients.

Nuance Communications provides AI-powered speech recognition and medical coding solutions, leveraging cloud platforms, digital reach, and strategic partnerships to enhance clinician workflow efficiency and compliance across healthcare organizations worldwide.

Key Players

- 3M Health Information Systems

- AGS Health

- Access Healthcare

- Athenahealth

- Cognizant

- eClinicalWorks

- GeBBS Healthcare Solutions

- iMedX, Inc.

- Nuance Communications (Microsoft)

- Optum360

Recent Developments

In March 2026, the leading enterprise electronic health record (EHR) platform, Epic, and athenahealth's athenaOne, an AI-powered all-in-one EHR and practice management solution for ambulatory care, are now compatible with DarcyIQ, the AI revenue acceleration platform created by AWS Premier Tier Partner Innovative Solutions. Through natural language conversations within DarcyIQ, the new integrations enable clinical and administrative users to engage with their Epic and athenaOne environments, providing immediate access to patient records, clinical documentation, scheduling workflows, and revenue cycle data without having to switch between platforms. Healthcare institutions have seen notable operational advantages as a result of the integrations, including a 55% decrease in time spent on administrative documentation duties and a 40% quicker settlement of billing and claims. questions.

In March 2026, to increase the capabilities of Optum260, US Bank has partnered with Optum360's healthcare-focused technology. Hospitals and providers can better manage their revenue cycle and receivables demands with the use of this package. The solutions will aid in the digital management of receivables, offering workflow functionalities for denial management as well as support to providers in determining the underlying causes and speeding up revenue recovery.

In October 2025, to help meet the challenges like rising claim denials, staffing shortages, and mounting margin pressures, AGS Health, a leading provider of tech-enabled RCM solutions and a strategic growth partner to healthcare providers across the U.S., has introduced a new suite of agentic digital workforce solutions powered by AI agents and intelligent automation. This next-generation, AI-infused workforce solutions shall bring speed, agility, accuracy, and human-like decision-making to critical RCM functions such as eligibility verification, prior authorizations, denials management, and appeals.

Global Global Medical Coding Market Coverage

Classification System Insight and Forecast 2026 - 2035

- International Classification of Diseases (ICD)

- Current Procedural Terminology (CPT)

- Healthcare Common Procedure Coding System (HCPCS)

- Systematized Nomenclature of Medicine – Clinical Terms (SNOMED CT)

Offering Insight and Forecast 2026 - 2035

- Outsourced Medical Coding Services

- In-house Medical Coding Services

- Software Solutions

- AI / Automation Tools

Delivery Mode Insight and Forecast 2026 - 2035

- Cloud-based Solutions

- On-premise Coding Systems

- Hybrid / Managed Services

Application Insight and Forecast 2026 - 2035

- Radiology Coding

- Oncology Coding

- Cardiology Coding

- Pathology Coding

- Surgery / Procedure Coding

Function Insight and Forecast 2026 - 2035

- Code Assignment and Validation

- Analytics and Reporting

- Compliance and Audit Management

- Revenue Cycle Optimization

- Data Quality Management

End User Insight and Forecast 2026 - 2035

- Hospitals and Large Healthcare Facilities

- Physician Practices

- Clinics

- and Diagnostic Centers

- Insurance Providers and Payers

- Specialty and Ambulatory Care Center

Global Global Medical Coding Market by Region

- North America

- By Classification System

- By Offering

- By Delivery Mode

- By Application

- By Function

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Classification System

- By Offering

- By Delivery Mode

- By Application

- By Function

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Classification System

- By Offering

- By Delivery Mode

- By Application

- By Function

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Classification System

- By Offering

- By Delivery Mode

- By Application

- By Function

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Global Medical Coding Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Classification System

1.2.2. By

Offering

1.2.3. By

Delivery Mode

1.2.4. By

Application

1.2.5. By

Function

1.2.6. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Classification System

5.1.1. International Classification of Diseases (ICD)

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Current Procedural Terminology (CPT)

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Healthcare Common Procedure Coding System (HCPCS)

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Systematized Nomenclature of Medicine – Clinical Terms (SNOMED CT)

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.2. By Offering

5.2.1. Outsourced Medical Coding Services

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. In-house Medical Coding Services

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Software Solutions

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. AI / Automation Tools

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.3. By Delivery Mode

5.3.1. Cloud-based Solutions

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. On-premise Coding Systems

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Hybrid / Managed Services

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.4. By Application

5.4.1. Radiology Coding

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Oncology Coding

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Cardiology Coding

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Pathology Coding

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Surgery / Procedure Coding

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

5.5. By Function

5.5.1. Code Assignment and Validation

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Analytics and Reporting

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Compliance and Audit Management

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Revenue Cycle Optimization

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

5.5.5. Data Quality Management

5.5.5.1. Market Definition

5.5.5.2. Market Estimation and Forecast to 2035

5.6. By End User

5.6.1. Hospitals and Large Healthcare Facilities

5.6.1.1. Market Definition

5.6.1.2. Market Estimation and Forecast to 2035

5.6.2. Physician Practices

5.6.2.1. Market Definition

5.6.2.2. Market Estimation and Forecast to 2035

5.6.3. Clinics

5.6.3.1. Market Definition

5.6.3.2. Market Estimation and Forecast to 2035

5.6.4. and Diagnostic Centers

5.6.4.1. Market Definition

5.6.4.2. Market Estimation and Forecast to 2035

5.6.5. Insurance Providers and Payers

5.6.5.1. Market Definition

5.6.5.2. Market Estimation and Forecast to 2035

5.6.6. Specialty and Ambulatory Care Center

5.6.6.1. Market Definition

5.6.6.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Classification System

6.2. By

Offering

6.3. By

Delivery Mode

6.4. By

Application

6.5. By

Function

6.6. By

End User

6.6.1.

U.S. Market Estimate and Forecast

6.6.2.

Canada Market Estimate and Forecast

6.6.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Classification System

7.2. By

Offering

7.3. By

Delivery Mode

7.4. By

Application

7.5. By

Function

7.6. By

End User

7.6.1.

Germany Market Estimate and Forecast

7.6.2.

France Market Estimate and Forecast

7.6.3.

U.K. Market Estimate and Forecast

7.6.4.

Italy Market Estimate and Forecast

7.6.5.

Spain Market Estimate and Forecast

7.6.6.

Russia Market Estimate and Forecast

7.6.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Classification System

8.2. By

Offering

8.3. By

Delivery Mode

8.4. By

Application

8.5. By

Function

8.6. By

End User

8.6.1.

China Market Estimate and Forecast

8.6.2.

Japan Market Estimate and Forecast

8.6.3.

India Market Estimate and Forecast

8.6.4.

South Korea Market Estimate and Forecast

8.6.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Classification System

9.2. By

Offering

9.3. By

Delivery Mode

9.4. By

Application

9.5. By

Function

9.6. By

End User

9.6.1.

Brazil Market Estimate and Forecast

9.6.2.

Saudi Arabia Market Estimate and Forecast

9.6.3.

South Africa Market Estimate and Forecast

9.6.4.

U.A.E. Market Estimate and Forecast

9.6.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

3M Health Information Systems

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

AGS Health

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Access Healthcare

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Athenahealth

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Cognizant

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

eClinicalWorks

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

GeBBS Healthcare Solutions

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

iMedX, Inc.

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Nuance Communications (Microsoft)

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Optum360 / UnitedHealth Group

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Global Medical Coding Market