Healthcare Analytical Testing Services Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Type (Pharmaceutical Analytical Testing Services, Medical Device Analytical Testing Services), by Service Type (Bioanalytical Testing, Stability Testing, Microbial Testing, Method Development & Validation, Raw Material Testing, Environmental Monitoring), by End User (Pharmaceutical & Biopharmaceutical Companies, Medical Device Companies, Contract Research Organisations (CROs), Contract Development & Manufacturing Organisations (CDMOs), Academic & Research Institutes), by Development Stage (Preclinical Testing, Clinical Testing, Commercial / Post-Market Testing), by Application (Oncology, Neurology, Cardiology, Infectious Diseases, Others)

| Status : Published | Published On : Apr, 2026 | Report Code : VRHC1331 | Industry : Healthcare | Available Format :

|

Page : 195 |

Healthcare Analytical Testing Services Market Overview

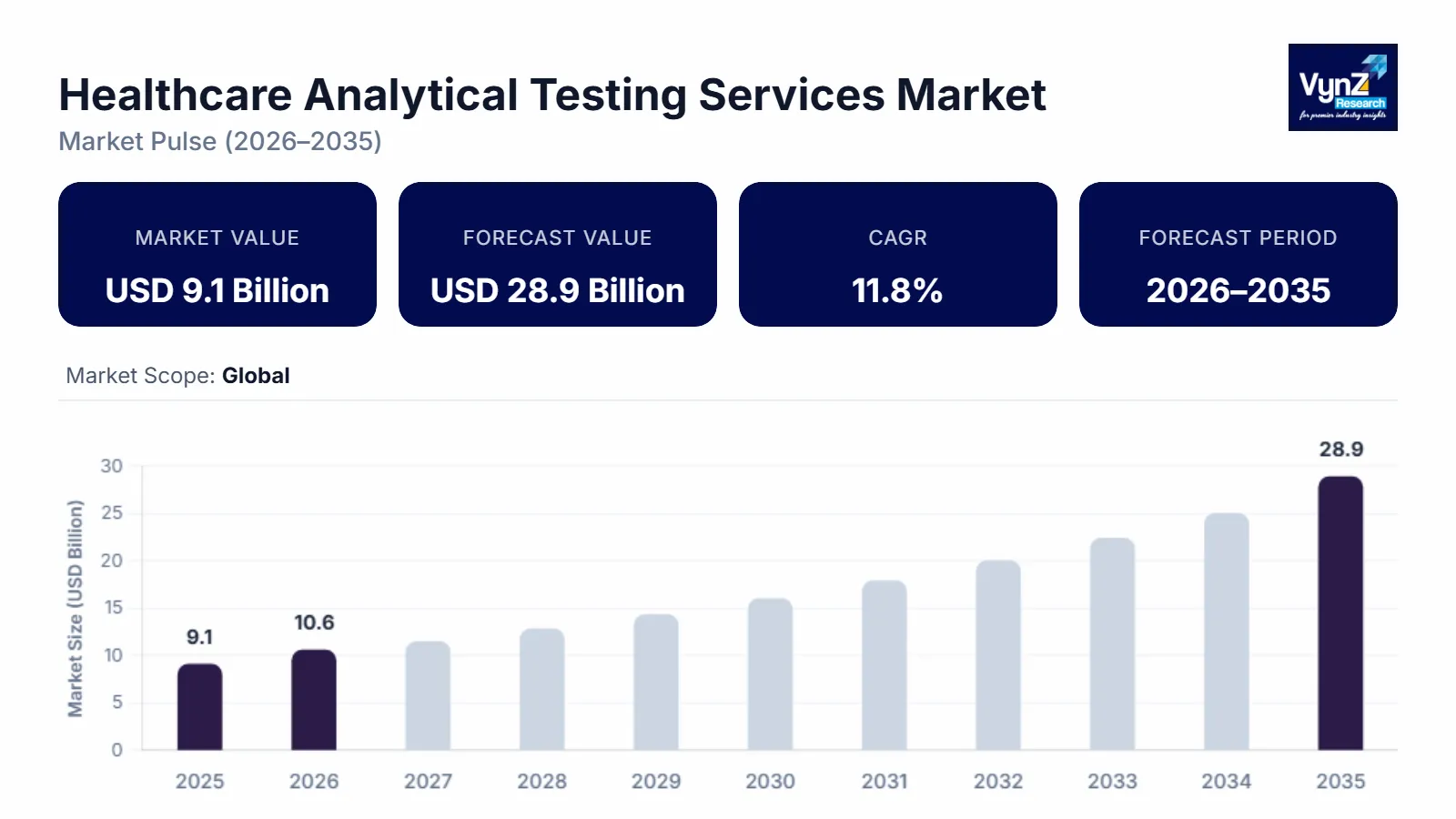

The healthcare analytical testing services market, which was valued at approximately USD 9.1 billion in 2025 and is estimated to reach around USD 10.6 billion in 2026, is projected to reach close to USD 28.9 billion by 2035, expanding at a CAGR of about 11.8% during the forecast period from 2026 to 2035.

The primary driver of this growth in the contract laboratory market is the increased complexity in the development of new pharmaceuticals and medical devices, as well as the increasing pressure to meet tight regulatory requirements regarding the quality and safety of products that are being developed. Additionally, a major factor driving this trend is the continuing movement towards outsourcing complex analytical services. Biologics, biosimilars, and advanced technologies often need more detailed characterisation, more extensive method development and validation, larger stability programmes, and additional microbiological testing throughout their development. At the same time, there has been an ongoing increase in the number of clinical trials and manufacturing scale-up operations, which creates an increasing demand for batch-release testing, raw material testing, and comparative studies. Contract service laboratories are also seeing an advantage due to the industry's desire to shorten timelines and improve data integrity with the use of automated instruments, digital Laboratory Information Management Systems (LIMS), and standardised quality systems.

Additionally, the rise of combination products and connected medical technologies increases the breadth of testing requirements spanning chemical, biological, and performance attributes. Overall, the market is supported by the need for compliant, high-throughput, and technically advanced analytical testing that enables faster approvals and reliable product supply.

Healthcare Analytical Testing Services Market Dynamics

Market Trends

The most significant trend affecting the overall healthcare analytical testing services market is the growing use of sophisticated analytical platforms and data-based approaches to enhance throughput, provide greater traceability, and ensure compliance with regulations. As service providers expand their high-sensitivity analytical methods (such as mass spectrometry, chromatography, and bio-analytical assays) to address the complexity of biologic molecules and impurities in drug substances and intermediates, they also develop and validate new methods on a global basis through expanded method transfer and validation programmes. The second largest trend has been an expansion in end-to-end offerings. Service providers have developed integrated solutions that combine early phase support (such as method development/characterisation) with later stage quality control/batch release testing to help clients reduce the number of vendors required. Finally, many laboratory operations have invested in automation and digital quality management systems (LIMS included) to eliminate manual errors, create stronger audit trails, and reduce the time it takes to complete studies.

Growth Drivers

The increase in reliance on outsourced analytical testing by pharmaceutical, biopharmaceutical, and medical device manufacturers has created the largest driving force in the healthcare analytical testing services market. Sponsors face growing pipelines and increased regulatory compliance requirements while, at the same time, trying to control their fixed cost base as it relates to laboratory infrastructure, and thereby create long-term demand for their testing partners from the perspective of development and commercialisation. Analytical testing will continue to be an increasingly important part of the development process of biologic drugs and biosimilar drugs due to the fact that they must have extensive comparative physical and chemical characterisation and functional comparison, as well as robust stability studies to assure consistency of product quality. Regulatory compliance and reimbursement models within major markets further underscore the requirement for sponsors to provide compliant clinical diagnostic laboratory testing protocols. For example, in the United States, payment for clinical diagnostic laboratory tests is made to laboratories by Medicare through the Clinical Laboratory Fee Schedule (CLFS). The CLFS fee schedule is reviewed and amended periodically pursuant to previously promulgated federal regulations, illustrating the formalised, regulated nature of laboratory testing services and the continued need for standardisation of laboratory practice.

Market Restraints / Challenges

The most important issues with the healthcare analytical testing services market are: the high costs required to support a laboratory environment that is compliant with regulations, the requirement to continually invest in technology (specialised instrumentation), and an ongoing lack of skilled workers who are able to conduct work in laboratories. Testing service providers have strict quality system requirements and regulatory expectations, which make it difficult to be efficient in operations and limit their ability to grow rapidly without substantial capital investment or process improvements. Additionally, talent availability can be particularly limited for advanced testing such as advanced bioanalytical assays and complex chromatography/mass spectrometry workflows. As of 2024, the Bureau of Labour Statistics reported there were approximately 351,200 Clinical Laboratory Technologist/Clinical Laboratory Technician positions available in the United States. This number illustrates the magnitude of the labour force that supports all types of testing conducted by laboratories. The BLS also stated that, due to the ongoing replacement needs in this field, along with the modest amount of expected growth, competition for qualified staff will continue.

Market Opportunities

Therapeutic drug expansion (biologics, biosimilars) with an increase in complexity of formulation is generating opportunities for analytical lab service providers to establish differentiation based on their ability to perform high-sensitivity impurity profiling, advanced characterisation, and comprehensive release and stability testing. As research and development accelerate with shorter time frames to launch products, labs are able to take advantage of a larger share of outsourced budget dollars by providing a full range of analytical testing services from early-stage method development/qualification through late-stage quality control. Additionally, there is growth in the scale-up of digital laboratory operational processes and technologies; these include automated equipment, electronic workflow standardisation, and enhanced data integrity features that will provide increased efficiency in turnaround time and audit compliance. Finally, growth is being generated across diagnostics/laboratory ecosystems.

Global Healthcare Analytical Testing Services Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 9.1 Billion |

|

Revenue Forecast in 2035 |

USD 28.9 Billion |

|

Growth Rate |

11.8% |

|

Segments Covered in the Report |

Type, Service Type, End User, Region |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia-Pacific, Latin America, Middle East & Africa |

|

Key Companies |

Eurofins Scientific SE, SGS SA, Intertek Group plc, Charles River Laboratories International, Inc., Laboratory Corporation of America Holdings, IQVIA Holdings Inc., Thermo Fisher Scientific Inc., Pace® Analytical Services, LLC, WuXi AppTec Co., Ltd., ALS Limited |

|

Customization |

Available upon request |

Healthcare Analytical Testing Services Market Segmentation

By Type

Pharmaceutical analytical testing services are the larger category, with a market share of about 60% in 2025, as pharmaceutical and biopharmaceutical product development is supported extensively throughout the entire process (discovery, formulation, preclinical, clinical, and commercial) with analytical services. The services included in this category include method development/verification, stability testing, impurity profiling, and release testing to ensure that products meet both regulatory compliance standards and are of high quality. Due to an increase in the number of biological/biosimilar drug products being developed, there has been an increase in the level of analytical service required, with an emphasis on physicochemical characterisation and comparability studies. Increased outsourcing from sponsors will continue to support the strong position of this category due to the acceleration of time to completion and access to specialised instrumentation.

Medical device analytical testing services are the faster-growing category, with a CAGR of 11.9% during the forecast period, due to increased complexity in all types of medical devices, the growing number of "combination" type products that contain both drug and non-drug components, as well as greater emphasis on demonstrating biocompatibility, extractable/leachable, and material characterisation for various product designs. Manufacturers have created new implant technologies, diagnostic products, and "connected" products that require specialised testing to demonstrate their performance, safety, and conformance with regulations. The expansion of this testing market is being driven by expanded regulatory oversight and requirements from national authorities around the world that impose unique conformity assessments (regulatory standards). Therefore, there is a growing requirement for laboratories that have demonstrated quality management systems and can perform testing according to multiple standards.

By Service Type

Method Development & Validation Services are the larger category, with a market share of about 25% in 2025, due to the role that validated analytical procedures play in ensuring that quality data can be generated throughout product development, manufacturing, and regulatory submissions. In order to generate quality data, sponsors require robust analytical methods for determining potency, quantifying impurities, and confirming identity, while maintaining batch-to-batch comparability among all raw materials, intermediates, and final products. The necessity for robust methods is further driven by the frequency at which these methods are transferred from one site to another or partner to partner; the requirement for stability indicating methods, and ongoing lifecycle method maintenance post-approval.

Bioanalytical testing services are the fastest-growing category, with a CAGR of 12.3% during the forecast period, due to an increase in the number of biological drug candidates, as well as an increase in analytical needs in PK/PD, immunogenicity testing, and biomarkers for use in clinical trials. The majority of these will require a variety of customised assays that have specific requirements, including but not limited to: strict sample management and sensitive detection systems.

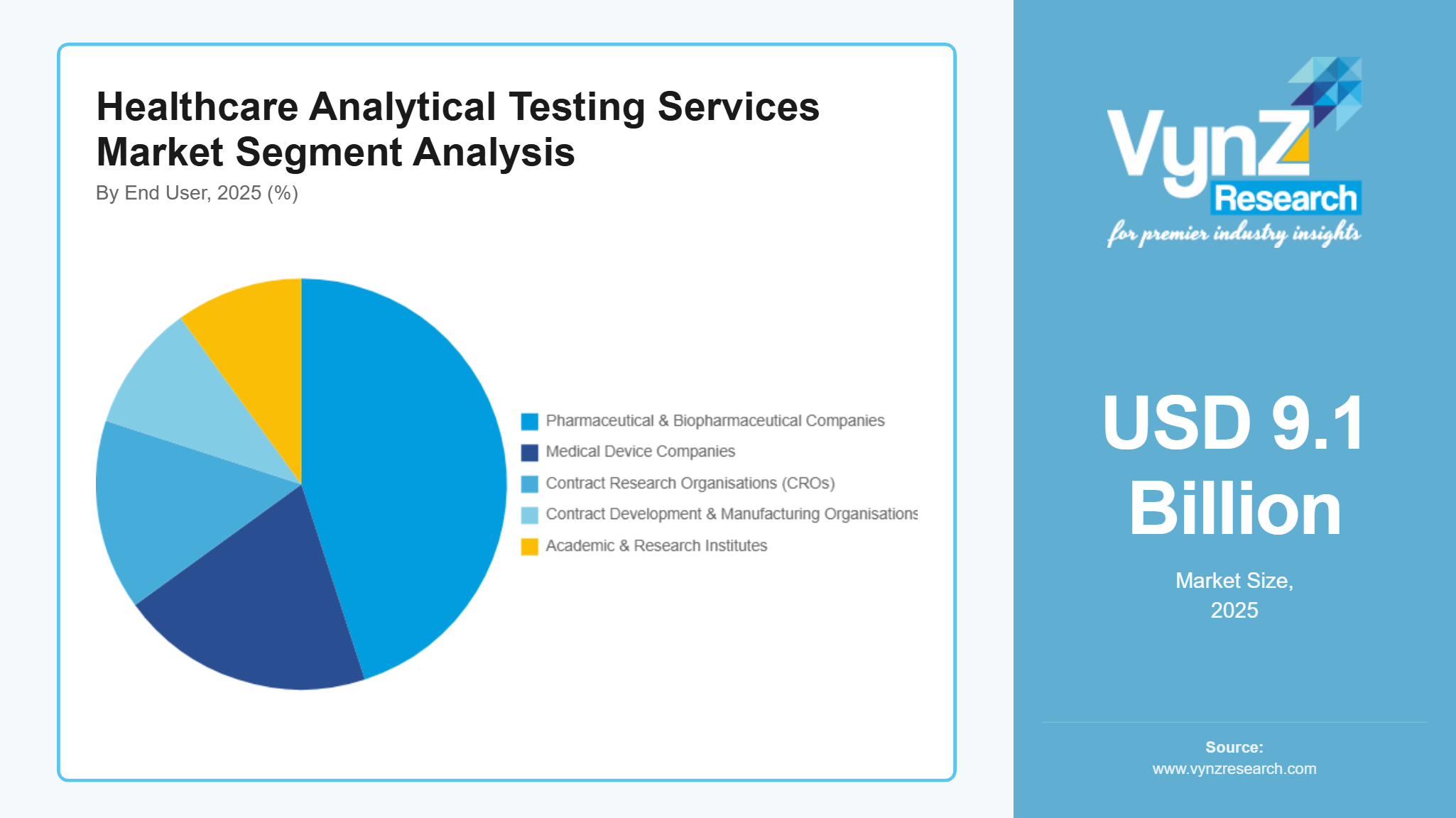

By End User

Pharmaceutical & Biopharmaceutical Companies are the largest category, with a market share of about 45% in 2025, because pharmaceutical and biopharmaceutical organisations need constant analytical support during their entire drug development life cycle (from early research stages to commercialisation). Due to this, they utilise outside laboratories for development and validation of methods, for stability programmes, release testing, and impurities, in order to comply with regulations and provide consistent products. A large number of pipeline projects, a large increase in the amount of biologic drugs/biosimilar drugs being developed, and the ongoing changes that occur after approval create continued demand for high-throughput analytical services that are compliant.

Medical device companies are the fastest-growing category, with a CAGR of 12.5% during the forecast period, due to increasing device innovation and an increase in the scope of analytical requirements associated with materials, biocompatibility, and chemical characterisation, including extractables & leachable analysis. Manufacturers developing increasingly sophisticated implantable medical devices, diagnostic systems, and combination product systems have required special testing by third parties to document their safety and performance for emerging regulations.

By Development Stage

Commercial or post-market is the largest category, with a market share of about 45% in 2025, since there will always be a requirement for quality assurance, regulatory compliance, and lifecycle management of approved drugs and medical devices. After launching a drug or device, a company's products are required to have an ongoing programme of stability testing; batch release testing; pharmacovigilance (to provide continued safety data), etc., to demonstrate that their product continues to perform safely and consistently across all regulated countries. The FDA and EMA, etc., require companies to continue to monitor their products and obtain re-approval for these products through the use of continuous re-validation programmes, which have created significant growth opportunities for analytical testing service providers.

Clinical testing is the fastest-growing category during the forecast period, due to the rising number of drugs and biologics entering clinical trials, especially in areas such as oncology and rare diseases. This phase requires extensive bioanalytical and biomarker testing to evaluate safety, efficacy, and dosage accuracy in human subjects. The increasing outsourcing of clinical trial support to specialised service providers and the expansion of global clinical pipelines are accelerating demand.

By Application

Oncology is the largest category, with a market share of about 25% in 2024, mainly due to the very high global incidence of cancers, as well as the large development pipelines of oncology drugs and biologics. In addition to assessing drug safety and efficacy, analytical testing provides key information regarding drug stability necessary to support the approval and post-approval use of cancer treatments, including targeted therapies and immunotherapies. Increasingly large investments are being made into cancer research. The growing number of clinical trials in this field also contributes to an increased need for analytical testing services.

Infectious diseases are the fastest-growing category during the forecast period, due to increased emphasis being placed upon emerging or re-emerging infectious agents (COVID-19) and the emergence of antibiotic-resistant organisms. This has resulted in a significant increase in demand for analytical testing services, which include bio-analytical and microbiological testing with respect to the development of vaccines and drugs for infectious diseases. As a result, governments and health care institutions have invested large sums into researching infectious diseases, resulting in an increase in the number of active clinical trials.

Regional Insights

North America

North America accounted for approximately 38% of the market in 2025, driven by strong biopharmaceutical R&D activity, a well-established outsourcing ecosystem, and the large presence of GMP manufacturing and regulated medical device production facilities. Strong demand from major biotechnology and pharmaceutical hubs across the United States and Canada continues to support market growth. According to the National Institutes of Health (NIH), the U.S. invests nearly USD 48 billion annually in biomedical research, supporting drug development, clinical trials, and laboratory testing infrastructure.

Government initiatives, combined with increasing outsourcing of analytical testing, regulatory compliance requirements, and demand for validated laboratory services, are encouraging investments in advanced analytical testing capabilities and laboratory infrastructure across the region.

Asia-Pacific

Asia Pacific accounted for approximately 27% of the market in 2025, supported by rapid growth in biopharmaceutical manufacturing, increasing clinical trial activity, and rising adoption of outsourced testing services across China, India, Japan, and South Korea. Increasing demand from pharmaceutical, biotechnology, and medical device companies is driving consistent market growth. Governments across the region are investing heavily in healthcare infrastructure, diagnostics, and life sciences manufacturing, while India and China continue expanding their pharmaceutical production and research capabilities.

Government support, rising clinical research activity, and expansion of CRO and CDMO service networks are accelerating demand for bioanalytical testing, stability testing, and method validation services across the region.

Europe

Europe accounted for approximately 18% of the market in 2025, driven by the strong presence of pharmaceutical and biotechnology manufacturers, stringent regulatory standards, and an active clinical research environment. Demand remains strong across Germany, France, the United Kingdom, and other major pharmaceutical markets. According to the European Union, the EU4Health program includes investments of approximately €5.1 billion during 2021–2027 to strengthen healthcare systems, diagnostics, and advanced therapeutic development.

Growth in Europe is supported by increasing investments in biologics, advanced therapeutics, and digital laboratory technologies, along with rising demand for third-party analytical testing and regulatory compliance services.

Rest of the World

The rest of the world, including Latin America and the Middle East & Africa, accounted for approximately 7% of the market in 2025, supported by improving healthcare infrastructure, increasing pharmaceutical production, and strengthening regulatory frameworks. Countries such as Brazil, Mexico, Saudi Arabia, and South Africa are witnessing rising investments in diagnostics, healthcare modernization, and laboratory quality standards.

Government healthcare initiatives, growing adoption of Good Laboratory Practices (GLP), and expansion of pharmaceutical manufacturing capabilities are expected to create long-term opportunities for analytical testing service providers across these regions. Collectively, the above-mentioned regional markets account for nearly 90% of the global healthcare analytical testing services market, while the remaining share is distributed among smaller developing markets worldwide.

Competitive Landscape / Company Insights

The health care analytical testing services industry is moderately fragmented; it has the major players being contract testing service providers and larger laboratory networks providing both multi-technical test capabilities (method development/validation, stability testing, microbiology, chemical characterisation) and broader global reach. Key players are Eurofins Scientific SE, SGS SA, and Intertek Group plc. Each company provides an array of services related to its individual areas of technical expertise, and each maintains established quality systems and audit-ready documentation for all activities. A scale advantage may exist in addition to geographic reach, especially when a sponsor wants to have consistent test execution at various locations or globally.

Charles River Laboratories International, Inc., Laboratory Corp. of America Holdings, and IQVIA Holdings Inc., along with several other specialised CRO/CDMO laboratories that offer bioanalytical, biomarker, and central laboratory services supporting clinical development, are among the many additional prominent participants in this field. As the competition shifts towards high-value tests (complex biologic characterisation, sensitive bioanalytical assays for PK/PD and immunogenicity, extractables & leachables for devices and packaging), etc., some of these providers will need to invest in automation, digital workflow tools, and standardised laboratory information management systems to increase data integrity and throughput. In order to better serve the needs of global sponsors, strategic partnerships, capacity expansions, and acquisitions continue to be common methods for expanding the capabilities of these companies.

Mini Profiles

Eurofins Scientific SE operates a large global laboratory network providing analytical testing services for pharmaceuticals, biopharmaceuticals, and medical devices, including method development and validation, stability testing, microbiology, and specialised characterisation.

SGS SA provides testing, inspection, and certification services with a significant life-sciences testing footprint, supporting pharmaceutical quality control, stability and release testing, and compliance-focused analytical services across multiple regions.

Charles River Laboratories International, Inc. supports drug development with a portfolio that includes analytical and bioanalytical services used in preclinical and clinical programs, helping sponsors generate regulatory-grade data for complex therapeutics.

Intertek Group plc offers analytical testing and assurance services across industries, including regulated healthcare testing that supports pharmaceutical quality programs, materials characterisation, and compliance-driven laboratory services.

Laboratory Corporation of America Holdings provides laboratory services across clinical and drug development domains, including analytical and bioanalytical testing capabilities that support clinical trials, central lab services, and regulated testing needs for life-sciences sponsors.

Key Players

- Eurofins Scientific SE

- SGS SA

- Intertek Group plc

- Charles River Laboratories International, Inc.

- Laboratory Corporation of America Holdings

- IQVIA Holdings Inc.

- Thermo Fisher Scientific Inc.

- Pace Analytical Services, LLC

- WuXi AppTec Co., Ltd.

- ALS Limited

- PPD, Inc.

- LGC Limited

Recent Developments

In March 2026, Laboratory Corporation of America Holdings completed the acquisition of select assets of Crouse Health’s Laboratory Alliance of Central New York laboratory business and entered into an agreement to manage Crouse’s inpatient laboratory operations, expanding its laboratory services footprint.

In December 2025, Intertek Group plc announced the acquisition of an additional GMP pharmaceutical services facility in Melbourn near Cambridge, United Kingdom, to expand its development and laboratory capacity for next-generation inhaled medicines, including enhanced analytical testing and characterization capabilities.

In September 2025, Eurofins Scientific SE announced the completion of its planned purchase of related-party-owned sites, supporting long-term optimization of its laboratory network and infrastructure footprint.

In February 2026, Laboratory Corporation of America Holdings expanded its collaboration with PathAI to deploy an FDA-cleared digital pathology platform more broadly, strengthening capabilities that support advanced pathology workflows and laboratory modernization.

In January 2026, SGS SA expanded its pharmaceutical and bioanalytical testing capabilities through investments in advanced laboratory technologies and capacity upgrades to support growing demand for biologics, clinical testing, and regulatory compliance services.

Global Healthcare Analytical Testing Services Market Coverage

Type Insight and Forecast 2026 - 2035

- Pharmaceutical Analytical Testing Services

- Medical Device Analytical Testing Services

Service Type Insight and Forecast 2026 - 2035

- Bioanalytical Testing

- Stability Testing

- Microbial Testing

- Method Development & Validation

- Raw Material Testing

- Environmental Monitoring

End User Insight and Forecast 2026 - 2035

- Pharmaceutical & Biopharmaceutical Companies

- Medical Device Companies

- Contract Research Organisations (CROs)

- Contract Development & Manufacturing Organisations (CDMOs)

- Academic & Research Institutes

Development Stage Insight and Forecast 2026 - 2035

- Preclinical Testing

- Clinical Testing

- Commercial / Post-Market Testing

Application Insight and Forecast 2026 - 2035

- Oncology

- Neurology

- Cardiology

- Infectious Diseases

- Others

Global Healthcare Analytical Testing Services Market by Region

- North America

- By Type

- By Service Type

- By End User

- By Development Stage

- By Application

- By Country - U.S., Canada, Mexico

- Europe

- By Type

- By Service Type

- By End User

- By Development Stage

- By Application

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Type

- By Service Type

- By End User

- By Development Stage

- By Application

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Type

- By Service Type

- By End User

- By Development Stage

- By Application

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Healthcare Analytical Testing Services Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Type

1.2.2. By

Service Type

1.2.3. By

End User

1.2.4. By

Development Stage

1.2.5. By

Application

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Type

5.1.1. Pharmaceutical Analytical Testing Services

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Medical Device Analytical Testing Services

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.2. By Service Type

5.2.1. Bioanalytical Testing

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Stability Testing

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Microbial Testing

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Method Development & Validation

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. Raw Material Testing

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.2.6. Environmental Monitoring

5.2.6.1. Market Definition

5.2.6.2. Market Estimation and Forecast to 2035

5.3. By End User

5.3.1. Pharmaceutical & Biopharmaceutical Companies

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Medical Device Companies

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Contract Research Organisations (CROs)

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Contract Development & Manufacturing Organisations (CDMOs)

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Academic & Research Institutes

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.4. By Development Stage

5.4.1. Preclinical Testing

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Clinical Testing

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Commercial / Post-Market Testing

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.5. By Application

5.5.1. Oncology

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Neurology

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Cardiology

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Infectious Diseases

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

5.5.5. Others

5.5.5.1. Market Definition

5.5.5.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Type

6.2. By

Service Type

6.3. By

End User

6.4. By

Development Stage

6.5. By

Application

6.5.1.

U.S. Market Estimate and Forecast

6.5.2.

Canada Market Estimate and Forecast

6.5.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Type

7.2. By

Service Type

7.3. By

End User

7.4. By

Development Stage

7.5. By

Application

7.5.1.

Germany Market Estimate and Forecast

7.5.2.

France Market Estimate and Forecast

7.5.3.

U.K. Market Estimate and Forecast

7.5.4.

Italy Market Estimate and Forecast

7.5.5.

Spain Market Estimate and Forecast

7.5.6.

Russia Market Estimate and Forecast

7.5.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Type

8.2. By

Service Type

8.3. By

End User

8.4. By

Development Stage

8.5. By

Application

8.5.1.

China Market Estimate and Forecast

8.5.2.

Japan Market Estimate and Forecast

8.5.3.

India Market Estimate and Forecast

8.5.4.

South Korea Market Estimate and Forecast

8.5.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Type

9.2. By

Service Type

9.3. By

End User

9.4. By

Development Stage

9.5. By

Application

9.5.1.

Brazil Market Estimate and Forecast

9.5.2.

Saudi Arabia Market Estimate and Forecast

9.5.3.

South Africa Market Estimate and Forecast

9.5.4.

U.A.E. Market Estimate and Forecast

9.5.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Eurofins Scientific SE

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

SGS SA

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Intertek Group plc

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Charles River Laboratories International, Inc.

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Laboratory Corporation of America Holdings

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

IQVIA Holdings Inc.

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Thermo Fisher Scientific Inc.

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Pace Analytical Services, LLC

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

WuXi AppTec Co., Ltd.

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

ALS Limited

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

PPD, Inc.

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

10.12.

LGC Limited

10.12.1.

Snapshot

10.12.2.

Overview

10.12.3.

Offerings

10.12.4.

Financial

Insight

10.12.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Healthcare Analytical Testing Services Market