Europe Skincare Devices Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Product / Device Type (Treatment Devices, Diagnostic Devices), by Application (Skin Rejuvenation, Acne Treatment, Hair Removal, Skin Cancer Diagnosis, Psoriasis Treatment, Tattoo Removal, Wrinkle Reduction, Pigmentation Treatment), by Distribution Channel (Direct Sales, Retail Pharmacies, E-commerce / Online Platforms, Specialty Stores), by End User (Hospitals, Dermatology Clinics, Homecare Settings, Medical Spas and Beauty Clinics)

| Status : Published | Published On : Apr, 2026 | Report Code : VRHC1330 | Industry : Healthcare | Available Format :

|

Page : 132 |

Europe Skincare Devices Market Overview

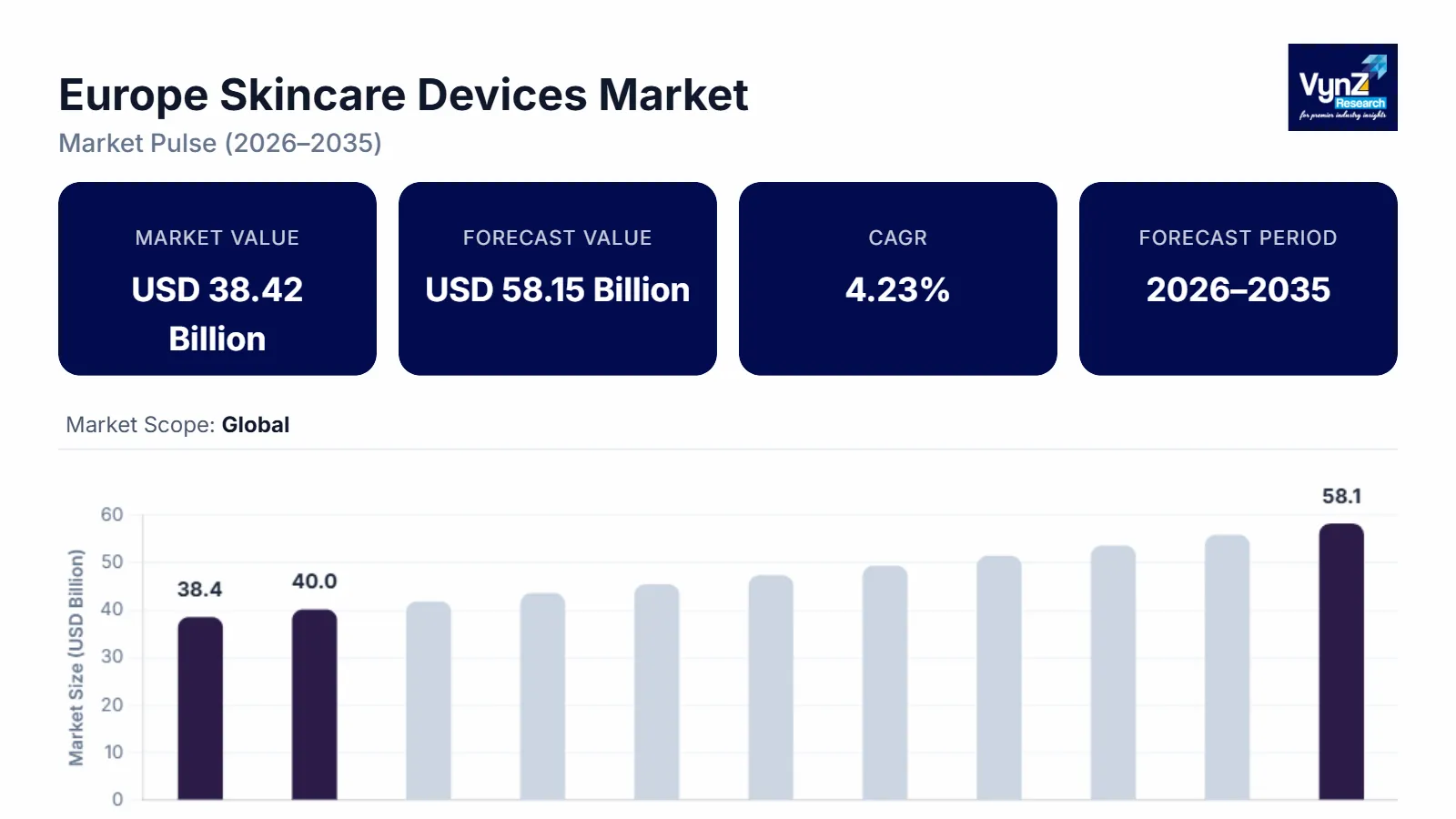

The Europe skincare devices market which was valued at approximately USD 38.42 billion in 2025 and is estimated to rise further up to almost USD 40.04 billion by 2026, is projected to reach around USD 58.14 billion in 2035, expanding at a CAGR of about 4.23% during the forecast period 2026 to 2035.

The market experiences growth because more people develop skin conditions which include acne, pigmentation disorders, photoaging and because noninvasive skincare treatment devices develop through ongoing technological progress. The World Health Organization reports that skin diseases represent one of the most frequently occurring health problems in the world which leads healthcare professionals to implement new diagnostic and treatment technologies that enhance their dermatological treatment capabilities.

The market development receives additional support from government health programs which promote early skin disorder detection and public education about the dangers of ultraviolet radiation. The European Commission and other institutions have established regional programs which seek to improve preventive healthcare and dermatology screening services. The growing demand from consumers for aesthetic skin treatments together with healthcare infrastructure investments boost adoption in major markets which include Germany, France and Italy.

Europe Skincare Devices Market Dynamics

Market Trends

The market is experiencing significant technological changes as customers now prefer non-invasive dermatological treatments and digital skin analysis systems. World Health Organization public health reports show that skin disorders are increasing and more early diagnostic technologies are needed to improve dermatological outcomes. Medical facilities now use laser treatment devices, radiofrequency systems and advanced skin imaging solutions to perform accurate clinical assessments and conduct their minimally invasive procedures. European healthcare systems see dermatology clinics and aesthetic centers using digital imaging, automated skin assessment systems and energy-based treatment methods to improve their clinical performance and achieve better patient outcomes.

Growth Drivers

The market experiences growth because more people develop skin conditions and there is higher interest in aesthetic dermatology treatments among the aging population. European Commission reports show that dermatology care services are expanding while preventive health services help people detect skin diseases at earlier stages. The combination of increased healthcare spending and dermatology clinic upgrades drives hospitals and specialty clinics and cosmetic treatment centers to adopt new medical devices. Energy-based treatment devices and diagnostic skin assessment technologies are now in higher demand throughout major European healthcare markets because consumers prefer advanced skin care treatments and minimally invasive cosmetic procedures.

Market Restraints / Challenges

The market exists in a challenging environment because regulatory requirements and expensive advanced dermatology equipment create obstacles for business growth. European Medicines Agency officials require medical device manufacturers to complete clinical validation and safety testing and obtain product approvals before they can sell their devices. Manufacturers face increased operational expenses because they must meet compliance requirements which extend the time needed to introduce new products. Smaller healthcare facilities and emerging aesthetic clinics face limitations in adopting advanced treatment devices because they need both skilled dermatology professionals and specialized clinical training.

Market Opportunities

The market provides substantial opportunities for digital dermatology technology growth and customized skincare treatment development which are backed by European healthcare innovation programs. European Commission policy frameworks promote digital health adoption which covers artificial intelligence enabled diagnostic systems and tele dermatology services that enhance access to dermatological treatment. The market for dermatology solutions will grow because companies are investing in smart diagnostic tools, automated skin imaging systems and personalized treatment technologies for their operations. The new technologies will enhance clinic results while making treatments more available and they will help hospitals and dermatology clinics adopt advanced skincare devices for an extended period of time.

Europe Skincare Devices Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 38.42 Billion |

|

Revenue Forecast in 2035 |

USD 58.14 Billion |

|

Growth Rate |

4.23% |

|

Segments Covered in the Report |

By Product Type, By Application, By Distribution Channel, By End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

Germany, U.K., France, Rest of Europe |

|

Key Companies |

Alma Lasers Ltd., Candela Medical, Classys Inc., Galderma SA, Hologic Inc., Koninklijke Philips N.V., L'Oréal SA, Lumenis Ltd., Merz Pharma GmbH & Co. KGaA, Panasonic Corporation, Procter & Gamble Company |

|

Customization |

Available upon request |

Europe Skincare Devices Market Segmentation

By Product Type

The market for treatment devices held the highest market share of 68% in 2025. The widespread clinical applications of laser systems, radiofrequency equipment and microdermabrasion technologies as cosmetic and therapeutic skin treatment tools, clinical dermatology and aesthetic treatment centers, maintain their dominance in the market. The segment expansion through major healthcare systems in Europe receives support from two factors, which include the growing popularity of minimally invasive methods and the ongoing development of energy-based dermatology technology.

Diagnostic devices will experience the highest growth rate between 2026 and 2035 with a CAGR of 8.6%. The market growth results from two factors which include clinicians, who want early identification of skin diseases and the rising usage of digital skin imaging systems in clinical settings. Dermatology specialists use dermatoscopes together with advanced imaging platforms to achieve better diagnostic results. The World Health Organization public health guidelines about skin disease early screening continue to boost technology adoption, through their recommendations.

By Application

Skin rejuvenation accounted for the largest segment share in 2025, representing approximately 30% of total application revenue. The segment benefits from rising demand for anti-aging procedures and noninvasive cosmetic treatments designed to improve skin tone and elasticity. European dermatology clinics and medical aesthetic centers keep expanding their treatment capacity through laser-based and energy-driven rejuvenation technologies.

Hair removal and acne treatment applications are expected to grow steadily, registering estimated CAGRs of 8.1% and 7.9% respectively during the forecast period. Urban areas have seen growing adoption of dermatological care between people who want access to cosmetic skin treatments because they are becoming more aware of skin health. Preventive healthcare initiatives that European Commission authorities support, promote early skin condition diagnosis, which increases demand for advanced skincare treatment devices.

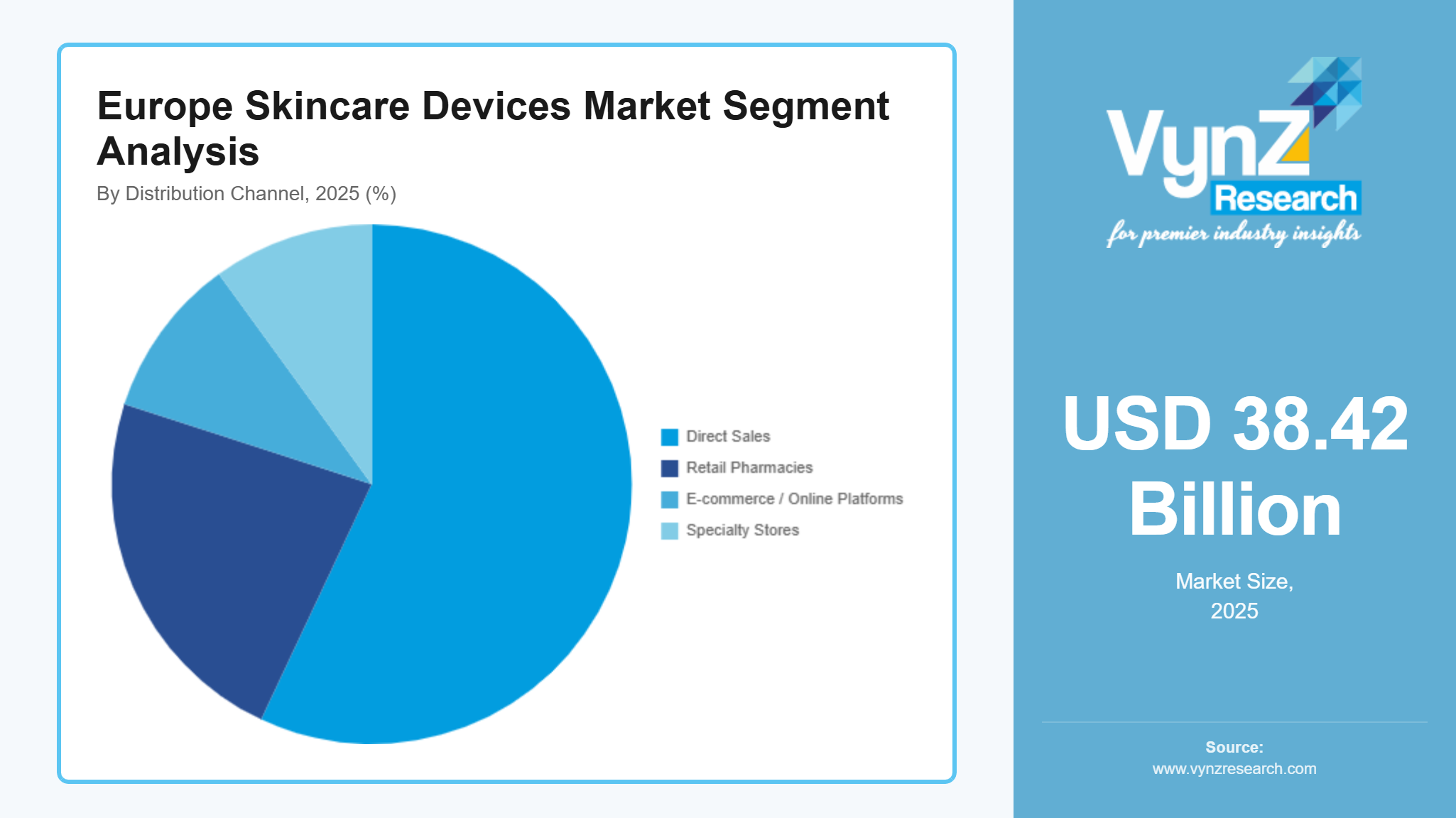

By Distribution Channel

Direct sales dominated the distribution landscape in 2025, accounting for approximately 57% of total market revenue. Hospitals and dermatology clinics and medical aesthetic centers purchase advanced skincare devices from manufacturers to deliver product authenticity, technical support and regulatory compliance, through their direct procurement model. Medical institutions such as the European Medicines Agency establish strict standards for medical devices, which compel professional dermatology equipment suppliers to use direct procurement channels.

Online platforms are expected to register the fastest growth, with an estimated CAGR of 9.2% during the forecast period. Digital procurement platforms and logistics systems expansion enable clinics and consumers to access a wider range of dermatology devices. The European skincare device distribution ecosystem improves product availability through distributor network integration, which connects online purchasing systems to distributors.

By End User

Dermatology clinics accounted for the largest share in 2025, representing approximately 42% of total market revenue. The organization leads through its specialized clinics and dermatology practices, which offer both clinical skin treatment and aesthetic skin treatment services. The expanding private dermatology centers and rising demand for advanced cosmetic procedures from consumers have made this segment the largest market sector in European healthcare.

Homecare settings are anticipated to witness the fastest growth, with an estimated CAGR of 9.5% during 2026 to 2035. The adoption of portable skincare devices has increased because of two factors, which include technological progress and consumer demand for lightweight skincare solutions. Public awareness initiatives, which organizations like the World Health Organization, promote about skin health, should lead to more people using safe home-based skincare products.

Regional Insights

Germany

The market in 2025 included Germany as its main market with 28% share because of its modern dermatology facilities and widespread use of cosmetic treatment technologies. Berlin, Munich and Frankfurt hospitals receive increasing patient traffic who request laser dermatology treatments together with digital dermatology diagnostic equipment. People spend more money on healthcare services while dermatology research centers exist which results in continuous demand from users for the latest skincare technology products.

The market development gets stronger through the government-funded healthcare systems and the European Medicines Agency medical device rules which assess their safety and effectiveness. Hospitals and dermatology clinics adopt advanced skin imaging and treatment technologies because public health agencies drive skin cancer screening program awareness through their dermatology research funding.

United Kingdom

The United Kingdom accounted for approximately 24% of the market in 2025. The region experiences growth because consumers want cosmetic dermatology procedures while private aesthetic clinics operate in multiple cities including London, Manchester and Birmingham. Consumers become more aware of advanced skin treatment technologies which leads them to adopt laser therapy and skin rejuvenation equipment and diagnostic dermatology systems.

The National Health Service leads public health initiatives which help people identify and treat skin health problems at an early stage. Hospitals and specialty clinics expand their skincare device demand because dermatology services increase and healthcare investments rise and skin cancer prevention programs become more widely known.

France

France holds about 22% of the regional skincare device market because consumers understand dermatological health and they want aesthetic treatments. Major urban centers including Paris, Lyon, and Marseille have experienced rising adoption of skin rejuvenation technologies and diagnostic dermatology devices in both clinical and cosmetic treatment facilities.

The World Health Organization together with dermatology awareness campaigns and healthcare modernization initiatives, promotes skin disease prevention through early detection of skin conditions. The growing investments in dermatology clinics and medical aesthetic centers lead to increased adoption of advanced skincare technologies throughout the entire country.

Rest of Europe

The remaining European countries control approximately 26% of the market which will operate in 2025. The region operates with expanding dermatology clinics and aesthetic skin treatment demand together with increasing knowledge about preventive skincare procedures. Digital skin diagnostic technologies together with laser-based treatment devices are being implemented across major metropolitan areas in both southern and northern Europe.

Competitive Landscape / Company Insights

The market is moderately to highly competitive, with global and regional manufacturers focusing on technological innovation, pricing strategies, and geographic expansion. Companies are increasingly investing in advanced laser technologies, digital skin diagnostic systems, and portable skincare devices to strengthen their market presence. Adoption is supported by dermatology awareness programs and preventive healthcare initiatives promoted by institutions such as the World Health Organization and healthcare modernization frameworks coordinated by the European Commission, encouraging wider deployment of advanced dermatology technologies across clinical settings.

Mini Profiles

Alma Lasers Ltd. focuses on advanced energy-based aesthetic and dermatology devices, supported by strong global distribution networks, continuous product innovation, and established clinical adoption across dermatology clinics and medical aesthetic centers.

Classys Inc. operates in premium dermatology and aesthetic device segments, emphasizing high performance laser and radiofrequency technologies that support skin tightening and rejuvenation treatments across specialized cosmetic clinics.

Galderma SA leverages strong dermatology expertise and strategic partnerships to expand market presence, offering integrated skincare solutions and aesthetic technologies supported by extensive clinical research and international dermatology networks.

Hologic Inc. focuses on medical imaging and energy-based treatment technologies, supported by strong healthcare partnerships, advanced research capabilities, and an established presence across hospitals and specialty clinical environments.

Panasonic Corporation operates in consumer and professional skincare device segments, emphasizing precision engineering, digital innovation, and strong global distribution channels that enhance accessibility of home use and clinical skincare technologies.

Key Players

- Alma Lasers Ltd.

- Candela Medical

- Classys Inc.

- Galderma SA

- Hologic Inc.

- Koninklijke

- Philips N.V.

- L'Oréal SA

- Lumenis Ltd.

- Merz Pharma GmbH & Co. KGaA

- Panasonic Corporation

- Procter & Gamble Company

Recent Developments

In April 2025, Candela launched the Vbeam Pro laser platform for vascular and dermatologic treatments, integrating dual wavelength technology to improve treatment precision, efficiency, and clinical outcomes across dermatology and aesthetic practices.

In September 2025, Classys expanded global commercialization of its Volnewmer radiofrequency skin tightening system, strengthening partnerships with dermatology clinics and aesthetic treatment centers to support minimally invasive cosmetic procedures.

In June 2025, Merz Aesthetics expanded distribution of advanced aesthetic treatment technologies across European dermatology clinics, strengthening clinical education programs and physician partnerships to accelerate adoption of minimally invasive skin therapies.

In February 2026, Hologic expanded its aesthetic and dermatology device portfolio through strategic investments in energy-based treatment technologies and digital health solutions aimed at improving minimally invasive skin treatment procedures.

In January 2026, Philips introduced upgraded AI-enabled dermatology imaging capabilities within its connected health technology platforms, supporting early skin condition detection and improving dermatological diagnostic accuracy.

Europe Skincare Devices Market Coverage

Product / Device Type Insight and Forecast 2026 - 2035

- Treatment Devices

- Diagnostic Devices

Application Insight and Forecast 2026 - 2035

- Skin Rejuvenation

- Acne Treatment

- Hair Removal

- Skin Cancer Diagnosis

- Psoriasis Treatment

- Tattoo Removal

- Wrinkle Reduction

- Pigmentation Treatment

Distribution Channel Insight and Forecast 2026 - 2035

- Direct Sales

- Retail Pharmacies

- E-commerce / Online Platforms

- Specialty Stores

End User Insight and Forecast 2026 - 2035

- Hospitals

- Dermatology Clinics

- Homecare Settings

- Medical Spas and Beauty Clinics

Europe Skincare Devices Market by Region

- Germany

- By Product / Device Type

- By Application

- By Distribution Channel

- By End User

- U.K.

- By Product / Device Type

- By Application

- By Distribution Channel

- By End User

- France

- By Product / Device Type

- By Application

- By Distribution Channel

- By End User

- Italy

- By Product / Device Type

- By Application

- By Distribution Channel

- By End User

- Spain

- By Product / Device Type

- By Application

- By Distribution Channel

- By End User

- Russia

- By Product / Device Type

- By Application

- By Distribution Channel

- By End User

- Rest of Europe

- By Product / Device Type

- By Application

- By Distribution Channel

- By End User

Table of Contents for Europe Skincare Devices Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Product / Device Type

1.2.2. By

Application

1.2.3. By

Distribution Channel

1.2.4. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Europe Market Estimate and Forecast

4.1. Europe Market Overview

4.2. Europe Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Product / Device Type

5.1.1. Treatment Devices

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Diagnostic Devices

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.2. By Application

5.2.1. Skin Rejuvenation

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Acne Treatment

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Hair Removal

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Skin Cancer Diagnosis

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. Psoriasis Treatment

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.2.6. Tattoo Removal

5.2.6.1. Market Definition

5.2.6.2. Market Estimation and Forecast to 2035

5.2.7. Wrinkle Reduction

5.2.7.1. Market Definition

5.2.7.2. Market Estimation and Forecast to 2035

5.2.8. Pigmentation Treatment

5.2.8.1. Market Definition

5.2.8.2. Market Estimation and Forecast to 2035

5.3. By Distribution Channel

5.3.1. Direct Sales

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Retail Pharmacies

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. E-commerce / Online Platforms

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Specialty Stores

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.4. By End User

5.4.1. Hospitals

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Dermatology Clinics

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Homecare Settings

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Medical Spas and Beauty Clinics

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

6. Germany Market Estimate and Forecast

6.1. By

Product / Device Type

6.2. By

Application

6.3. By

Distribution Channel

6.4. By

End User

7. U.K. Market Estimate and Forecast

7.1. By

Product / Device Type

7.2. By

Application

7.3. By

Distribution Channel

7.4. By

End User

8. France Market Estimate and Forecast

8.1. By

Product / Device Type

8.2. By

Application

8.3. By

Distribution Channel

8.4. By

End User

9. Italy Market Estimate and Forecast

9.1. By

Product / Device Type

9.2. By

Application

9.3. By

Distribution Channel

9.4. By

End User

10. Spain Market Estimate and Forecast

10.1. By

Product / Device Type

10.2. By

Application

10.3. By

Distribution Channel

10.4. By

End User

11. Russia Market Estimate and Forecast

11.1. By

Product / Device Type

11.2. By

Application

11.3. By

Distribution Channel

11.4. By

End User

12. Rest of Europe Market Estimate and Forecast

12.1. By

Product / Device Type

12.2. By

Application

12.3. By

Distribution Channel

12.4. By

End User

13. Company Profiles

13.1.

Alma Lasers Ltd.

13.1.1.

Snapshot

13.1.2.

Overview

13.1.3.

Offerings

13.1.4.

Financial

Insight

13.1.5.

Recent

Developments

13.2.

Candela Medical

13.2.1.

Snapshot

13.2.2.

Overview

13.2.3.

Offerings

13.2.4.

Financial

Insight

13.2.5.

Recent

Developments

13.3.

Classys Inc.

13.3.1.

Snapshot

13.3.2.

Overview

13.3.3.

Offerings

13.3.4.

Financial

Insight

13.3.5.

Recent

Developments

13.4.

Galderma SA

13.4.1.

Snapshot

13.4.2.

Overview

13.4.3.

Offerings

13.4.4.

Financial

Insight

13.4.5.

Recent

Developments

13.5.

Hologic Inc.

13.5.1.

Snapshot

13.5.2.

Overview

13.5.3.

Offerings

13.5.4.

Financial

Insight

13.5.5.

Recent

Developments

13.6.

Koninklijke Philips N.V.

13.6.1.

Snapshot

13.6.2.

Overview

13.6.3.

Offerings

13.6.4.

Financial

Insight

13.6.5.

Recent

Developments

13.7.

L'Oréal SA

13.7.1.

Snapshot

13.7.2.

Overview

13.7.3.

Offerings

13.7.4.

Financial

Insight

13.7.5.

Recent

Developments

13.8.

Lumenis Ltd.

13.8.1.

Snapshot

13.8.2.

Overview

13.8.3.

Offerings

13.8.4.

Financial

Insight

13.8.5.

Recent

Developments

13.9.

Merz Pharma GmbH & Co. KGaA

13.9.1.

Snapshot

13.9.2.

Overview

13.9.3.

Offerings

13.9.4.

Financial

Insight

13.9.5.

Recent

Developments

13.10.

Panasonic Corporation

13.10.1.

Snapshot

13.10.2.

Overview

13.10.3.

Offerings

13.10.4.

Financial

Insight

13.10.5.

Recent

Developments

13.11.

Procter & Gamble Company

13.11.1.

Snapshot

13.11.2.

Overview

13.11.3.

Offerings

13.11.4.

Financial

Insight

13.11.5.

Recent

Developments

14. Appendix

14.1. Exchange Rates

14.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Europe Skincare Devices Market