Cancer Vaccines Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Technology (Preventive Cancer Vaccines, Therapeutic Cancer Vaccines), by Indication (Cervical Cancer, Prostate Cancer, Breast Cancer, Lung Cancer, Melanoma, Others), by Treatment Modality (Peptide Based Vaccines, Dendritic Cell Vaccines, Viral Vector Vaccines, DNA / RNA Vaccines, Whole Cell Vaccines), by End User (Hospitals, Specialty Cancer Clinics, Research Institutes / Academic Centers)

| Status : Published | Published On : Mar, 2026 | Report Code : VRHC1331 | Industry : Healthcare | Available Format :

|

Page : 179 |

Cancer Vaccines Market Overview

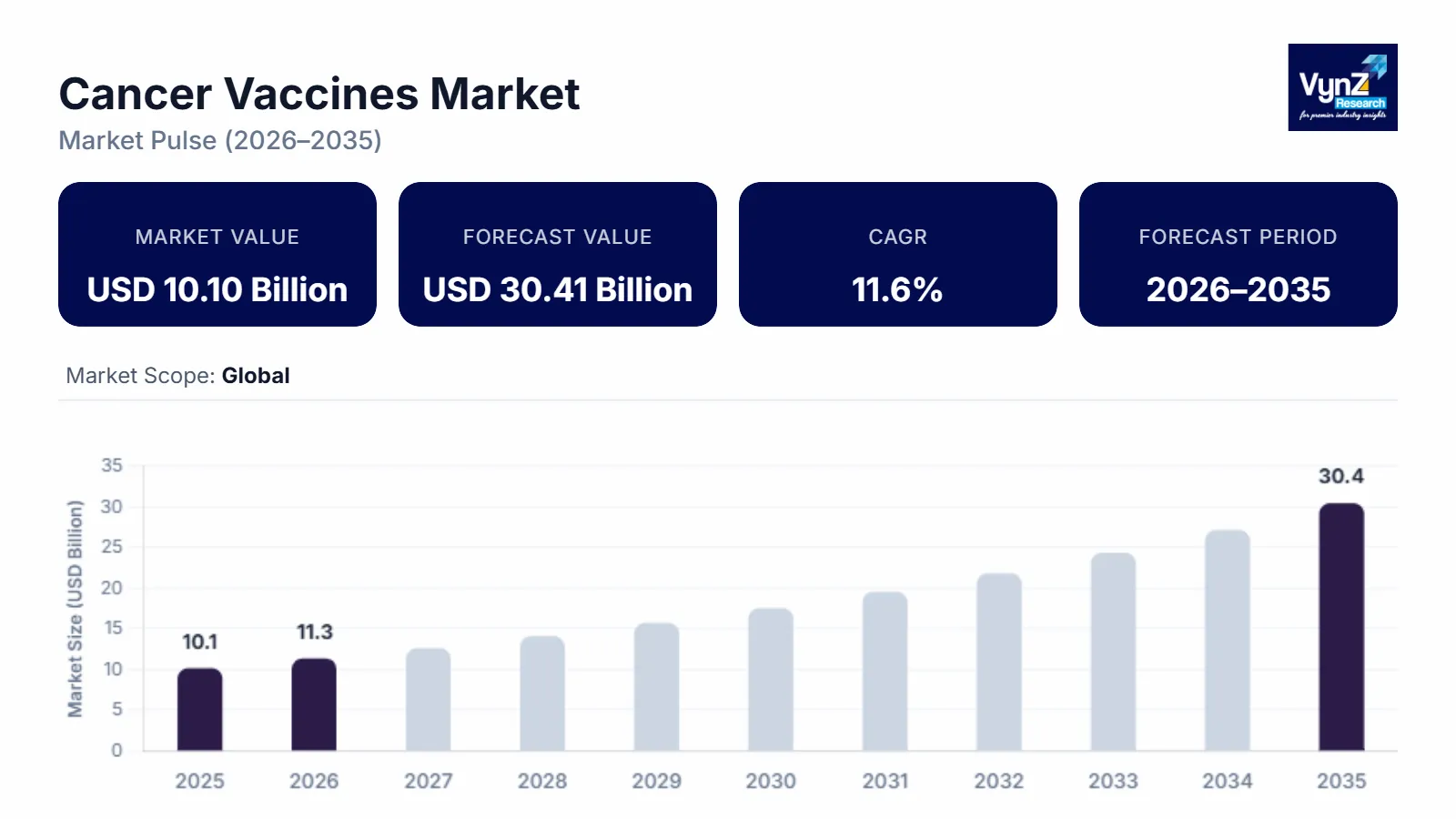

The Cancer Vaccines market which was valued at approximately USD 10.10 billion in 2025 and is estimated to rise further up to almost USD 11.32 billion in 2026, is projected to reach around USD 30.41 billion by 2035, expanding at a CAGR of about 11.6% during the forecast period 2026 to 2035.

Market expansion occurs because worldwide cancer rates increase and people conduct more research about immunotherapy treatments. Medical trials for customized treatment vaccines rise and the use of mRNA and peptide-based vaccine technologies becomes more common. Targeted oncology therapy demand and national cancer control program funding both drive market growth across New York, London, Beijing and other key markets.

Health authorities worldwide observe a steady growth in cancer cases which leads to stronger demands for vaccination methods that prevent and treat cancer. WHO reports that cancer stands as one of the top causes of death worldwide which leads governments to establish early disease prevention and vaccination programs as essential health priorities. Public funding for oncology research facilities, national vaccination programs and clinical development programs with National Cancer Institute and European health authority backing create a stronger pipeline for new cancer vaccine technologies which leads to global market growth for cancer vaccines.

Cancer Vaccines Market Dynamics

Market Trends

The medical field is moving toward immunotherapy supported precision oncology, which represents a treatment method shift that focuses on immunological treatments and extended disease protection. Vaccination programs which prevent cancer through virus vaccination methods targeting cervical and liver tumors are receiving increased acknowledgment from global health organizations. The World Health Organization promotes programs which boost vaccination rates and enhance screening programs while enabling countries to add preventive vaccines to their cancer control programs. Product development strategies now rely on mRNA technology advancements together with peptide vaccine and neoantigen personalized therapy developments. The biotechnology sector develops personalized therapeutic vaccine systems which create adaptive immune responses to enhance cancer treatment outcomes through these scientific breakthroughs.

Growth Drivers

The worldwide cancer epidemic and rising use of immunotherapy treatments drive market growth in this industry. The World Health Organization public health data shows that cancer remains one of the top global death causes, which creates an urgent requirement for vaccine research on preventive and therapeutic solutions. Oncology research programs, vaccine development initiatives, and clinical trial programs, which focus on early detection and improved patient outcomes, receive increased financial backing from government funding sources. The development of innovative cancer vaccine platforms accelerates through biotechnology research infrastructure investment and academic institution collaboration with pharmaceutical companies. The healthcare systems of developed markets together with emerging oncology markets display increasing demand for personalized medicine and targeted immune therapies, which healthcare providers now accept as standard practice.

Market Restraints / Challenges

The industry encounters difficulties because of its required clinical pathways and its need for lengthy clinical studies despite showing high potential for success. The development process for cancer vaccines necessitates formal safety evidence combined with effective testing results and national health authority approvals before they can be sold. Regulatory agencies together with government bodies present public health reports which show that oncology vaccine clinical trials need multiple study phases, which require many patients and extended monitoring time. The advanced biologics manufacturing and personalized vaccine development face production difficulties which lead to increased costs and manufacturing capacity restrictions. Healthcare systems in emerging economies and price sensitive markets will experience commercial challenges because of limited reimbursement systems and specialized oncology facilities.

Market Opportunities

The market needs preventive vaccination programs and next generation therapeutic vaccine platforms which target specific tumor antigens to create strong business opportunities. Government cancer prevention initiatives, which include large scale virus vaccination programs, promote vaccine based preventive methods for cancer. The health policy frameworks, which global health organizations support, create national oncology strategies through their requirements for vaccination, early screening, and immunotherapy to be combined into existing healthcare systems. Personalized cancer vaccine research will advance faster through genomic sequencing breakthroughs, mRNA vaccine development and artificial intelligence drug discovery methods. The companies which develop manufacturing processes, targeted immunotherapy systems and research partnerships will handle the rising demand for innovative oncology vaccines in developed healthcare markets and emerging healthcare markets.

Global Cancer Vaccines Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 10.10 Billion |

|

Revenue Forecast in 2035 |

USD 30.41 Billion |

|

Growth Rate |

11.6% |

|

Segments Covered in the Report |

Technology, Indication, Treatment Modality, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Amgen, Inc, Anixa Biosciences Inc, AstraZeneca PLC, BioNTech SE, BristolMyers Squibb Company, CSL Limited, Dendreon Pharmaceuticals LLC, Dynavax Technologies Corporation, Ferring B.V., Gritstone Bio, Inc. |

|

Customization |

Available upon request |

Cancer Vaccines Market Segmentation

By Technology

The market of 2025 included preventive cancer vaccines as its main revenue source, which generated approximately 57% of total market earnings. The high vaccination rates which protect against virus-related cancers demonstrate their effectiveness as public health programs. Vaccines against human papillomavirus and hepatitis infections receive widespread distribution through national immunization programs which international organizations and national health ministries endorse as essential healthcare standards. The preventive solutions demonstrate effectiveness in decreasing future cancer cases, while proving their value to public health organizations and vaccination initiatives in both developed and developing nations.

Therapeutic cancer vaccines are expected to become the fastest developing treatment option, with an anticipated growth rate of 12.8% during the upcoming period from 2026 to 2035. The clinical development process moves forward because researchers study personalized immunotherapies, the specific antigens of tumors and the combination methods which use immune checkpoint inhibitors. National oncology institutes coordinate government cancer research programs which provide funding to assist biotechnology companies and research organizations in developing therapeutic vaccine technologies. The upcoming developments will lead to improved treatment results which will enhance immunotherapy use in cancer treatment.

By Indication

Cervical cancer vaccines accounted for the largest segment share in 2025, contributing approximately 34% of total market revenue. The main position of this organization exists because it implements vaccination programs which focus on preventing human papillomavirus infection, the primary cause of cervical cancer. The World Health Organization promotes public health programs which advocate for adolescent vaccination to achieve universal vaccination status, which will decrease future cancer cases. Immunization programs which governments support along with public education campaigns, which active in North America, Europe and Asia Pacific, show positive results through school-based vaccination programs and national health initiatives.

Prostate cancer and lung cancer vaccine studies will increase their development rate during the upcoming period because they will achieve a compound annual growth rate of 12.2%. The ongoing clinical trials which target specific tumor antigens and develop immune response control techniques will create new therapeutic options for oncology specialists. Government health agencies fund national cancer control programs to prioritize research on innovative immunotherapies that enhance patient survival rates and minimize treatment side effects. The growth of segment-level market share achieves success through the establishment of precision medicine frameworks along with rising investments in cancer research infrastructure.

By Treatment Modality

Peptide based and dendritic cell vaccine platforms made up the largest segment of the market in 2025, which earned approximately 43% of total segment revenue. The platforms continue to receive research attention because they enable scientists to create immune responses which specifically target cancer antigens. The national research institutes and oncology centers use their extensive clinical research programs and biotechnology innovation initiatives to establish their development. Public financing of immunotherapy research leads to stronger research pipelines which help advanced vaccine technologies reach global healthcare markets through commercial sales.

DNA, RNA, and viral vector vaccine platforms are projected to grow at the fastest rate with an estimated compound annual growth rate of 13.1% throughout the forecast period. The development of next generation cancer immunotherapies advanced because scientists made progress in genetic engineering, mRNA delivery systems and viral vector design. Government-supported biomedical innovation programs create better research capacities through pandemic vaccine technology advancements which enhanced manufacturing capabilities. The platforms achieve rapid development times while they boost immune defense, which enables personalized cancer vaccine methods to develop in upcoming years.

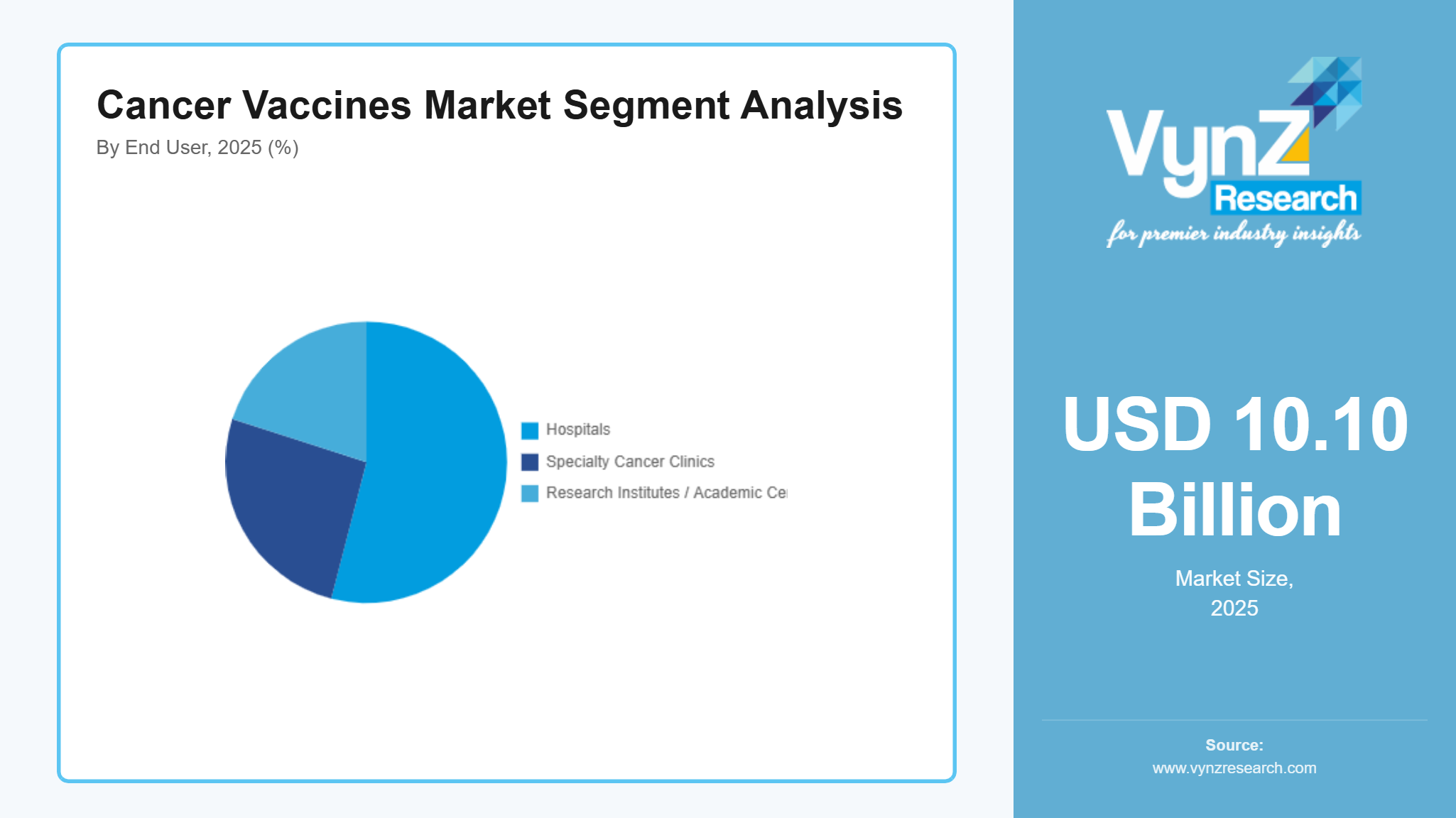

By End User

The market in 2025 identified hospitals as its major revenue driver which generated approximately 54% of market income. The healthcare system achieves its dominant market position because it has established oncology treatment centers with trained medical staff and access to advanced immunotherapy solutions. Hospitals serve as the main testing sites for cancer identification, treatment delivery and clinical research activities. The government health authorities fund national cancer treatment frameworks, which lead to better hospital networks throughout the main healthcare systems.

Specialty cancer clinics and research institutes are expected to grow at the fastest pace, registering an estimated CAGR of 11.9% between 2026 and 2035. The specialized treatment centers which adopt new cancer vaccine technologies receive funding through clinical trials, personalized medicine programs and advanced immunotherapy research initiatives. Government funding of oncology research projects, which academic institutions and biotechnology companies exchange through their collaborative programs, leads to innovation progress that maintains growth for the entire segment.

Regional Insights

North America

The North American market reached a 2025 market share of 33%. The region experiences growth because of its modern oncology research facilities, successful biotechnology sector development, and substantial healthcare funding. Boston, San Francisco, and Toronto serve as major research hubs that lead clinical development and commercialization efforts for cancer immunotherapies. The U.S. Food and Drug Administration together with its regulatory process enables hospitals, research centers, and biotechnology firms to implement cancer vaccines which protect against and treat cancer.

The region experiences growth because government funding supports cancer research and national immunization programs. The U.S. National Cancer Institute leads public health programs which focus on preventing early cancer through vaccination combined with advanced immunotherapy research. The region witnesses increased development of next generation cancer vaccines because of rising clinical trials and biotechnology investments.

Europe

The European market provided a 2025 share of 25%. The region experiences growth because public healthcare systems operate effectively while cancer research activities occur through extensive research programs and European Medicines Agency regulatory frameworks. Germany, the United Kingdom, France and Italy continue to enhance their research capabilities through clinical trials and immunotherapy research programs that develop cancer vaccines.

The European Union promotes preventive vaccine adoption for virus-related cancers through its governmental immunization initiatives and cancer control strategies which receive government support. The regional demand for advanced immunotherapy solutions increases because biotechnology companies invest in research partnerships with academia and oncology treatment facilities develop their infrastructure.

Asia Pacific

The Asia Pacific region holds a market share of 20% for cancer vaccines in 2025 because of rising healthcare spending and increasing cancer cases and growing biotechnology research capabilities. Countries including China, Japan, India and South Korea are building better systems for oncology research while they improve their vaccine production capabilities. Major metropolitan centers of Beijing, Tokyo and Mumbai experience growing use of immunotherapy treatments and preventive vaccination programs.

Government-supported national cancer control programs and vaccination campaigns are making preventive cancer vaccines more common in the region. Core public health strategies match global cancer prevention frameworks which help development of early screening and vaccination and immunotherapy technologies that create better cancer vaccine systems.

Rest of the World

The Rest of the World market reaches 18% in 2025, which includes Latin America, the Middle East, and Africa. The healthcare infrastructure expansion and cancer prevention education programs and virus-related cancer vaccination programs lead to market growth through their gradual implementation.

International healthcare organizations and development agencies continue to support cancer prevention initiatives and vaccination campaigns across emerging economies. Health sector modernization and oncology treatment infrastructure investment lead to increased cancer vaccine adoption while the remaining market demand is represented by the developing healthcare markets that will experience future growth.

Competitive Landscape / Company Insights

The market is moderately to highly competitive, with global biotechnology and pharmaceutical companies focusing on product innovation, strategic collaborations, and geographic expansion. Key vendors are investing in advanced immunotherapy platforms, mRNA-based vaccine technologies, and personalized oncology vaccines to improve treatment effectiveness. Adoption is supported by government initiatives such as funding programs from the U.S. National Cancer Institute, cancer prevention strategies led by the European Commission, and public health vaccination programs supported by global health agencies. These frameworks encourage companies to strengthen research capabilities and expand clinical development pipelines.

Mini Profiles

Amgen, Inc. focuses on therapeutic cancer vaccines and immuno-oncology solutions, supported by strong global distribution networks, robust clinical trial programs, and cost-effective manufacturing strategies that enhance presence across oncology treatment segments.

BioNTech SE operates in premium and specialized cancer vaccine segments, emphasizing mRNA-based immunotherapies, rapid vaccine development, and clinical efficacy, supported by strategic collaborations with global pharmaceutical companies and integrated research pipelines.

CSL Limited leverages local manufacturing and strategic partnerships to expand market presence, offering recombinant and viral vector-based vaccine solutions with streamlined supply chains and extensive regional distribution in high-demand markets.

Dynavax Technologies Corporation focuses on adjuvant-based oncology vaccines and immune-stimulating platforms, supported by innovative delivery systems, strong R&D investments, and collaborations with global biopharma to enhance clinical adoption and commercial reach.

Gritstone Bio, Inc. operates in premium personalized cancer vaccine segments, emphasizing neoantigen-targeted immunotherapies, digital genomic profiling, and adaptive clinical programs, supported by strategic alliances and advanced manufacturing capabilities.

Key Players

- Amgen, Inc.

- Anixa Biosciences Inc.

- AstraZeneca PLC

- BioNTech SE

- Bristol Myers Squibb Company

- CSL Limited

- Dendreon Pharmaceuticals LLC

- Dynavax Technologies Corporation

- Ferring B.V.

- Gritstone Bio, Inc.

Recent Developments

In February 2026, CSL Limited entered into a licensing agreement with Eli Lilly and Company which grants Lilly certain rights to develop and commercialize clazakizumab, an anti-interleukin-6 (IL-6) monoclonal antibody. This collaboration shall leverage Lilly’s global infrastructure to accelerate the development of clazakizumab for addressing inflammation-driven cardiovascular conditions.

In January 2026, AstraZeneca has announced USD 15 billion investment in China through 2030 to expand medicines manufacturing and R&D. This investment will leverage the country’s scientific excellence, advanced manufacturing, and China-UK healthcare ecosystem collaborations to deliver cutting-edge treatments to patients across China and globally. These investments span the value chain, from drug discovery and clinical development to manufacturing, and bring Chinese innovation to the world through the partnerships with leading biotechs including AbelZeta, CSPC, Harbour BioMed, Jacobio and Syneron Bio. The Company will also develop its existing manufacturing facilities in Wuxi, Taizhou, Qingdao, and Beijing, which provide high-quality medicines to patients in China and 70 markets worldwide, together with the establishment of new sites to be announced.

In January 2026, Amgen Inc. acquired UK-based biotechnology company Dark Blue Therapeutics in a deal valued at up to USD 840 million to strengthen its oncology pipeline. This shall aim on the advancement therapies for acute myeloid leukemia to improve cancer treatment outcomes. The acquisition adds to Amgen's portfolio an investigational small molecule that targets and degrades two proteins (MLLT1/3) that drive specific types of acute myeloid leukemia (AML), a fast-growing blood cancer. Amgen expects to integrate Dark Blue Therapeutics into its existing research organization, further strengthening the company's early oncology discovery efforts.

Global Cancer Vaccines Market Coverage

Technology Insight and Forecast 2026 - 2035

- Preventive Cancer Vaccines

- Therapeutic Cancer Vaccines

Indication Insight and Forecast 2026 - 2035

- Cervical Cancer

- Prostate Cancer

- Breast Cancer

- Lung Cancer

- Melanoma

- Others

Treatment Modality Insight and Forecast 2026 - 2035

- Peptide Based Vaccines

- Dendritic Cell Vaccines

- Viral Vector Vaccines

- DNA / RNA Vaccines

- Whole Cell Vaccines

End User Insight and Forecast 2026 - 2035

- Hospitals

- Specialty Cancer Clinics

- Research Institutes / Academic Centers

Global Cancer Vaccines Market by Region

- North America

- By Technology

- By Indication

- By Treatment Modality

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Technology

- By Indication

- By Treatment Modality

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Technology

- By Indication

- By Treatment Modality

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Technology

- By Indication

- By Treatment Modality

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Cancer Vaccines Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Technology

1.2.2. By

Indication

1.2.3. By

Treatment Modality

1.2.4. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Technology

5.1.1. Preventive Cancer Vaccines

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Therapeutic Cancer Vaccines

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.2. By Indication

5.2.1. Cervical Cancer

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Prostate Cancer

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Breast Cancer

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Lung Cancer

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. Melanoma

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.2.6. Others

5.2.6.1. Market Definition

5.2.6.2. Market Estimation and Forecast to 2035

5.3. By Treatment Modality

5.3.1. Peptide Based Vaccines

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Dendritic Cell Vaccines

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Viral Vector Vaccines

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. DNA / RNA Vaccines

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Whole Cell Vaccines

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.4. By End User

5.4.1. Hospitals

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Specialty Cancer Clinics

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Research Institutes / Academic Centers

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Technology

6.2. By

Indication

6.3. By

Treatment Modality

6.4. By

End User

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Technology

7.2. By

Indication

7.3. By

Treatment Modality

7.4. By

End User

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Technology

8.2. By

Indication

8.3. By

Treatment Modality

8.4. By

End User

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Technology

9.2. By

Indication

9.3. By

Treatment Modality

9.4. By

End User

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Amgen, Inc.

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Anixa Biosciences Inc.

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

AstraZeneca PLC

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

BioNTech SE

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Bristol Myers Squibb Company

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

CSL Limited

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Dendreon Pharmaceuticals LLC

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Dynavax Technologies Corporation

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Ferring B.V.

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Gritstone Bio, Inc.

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Cancer Vaccines Market