Infusion System Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Product Type (Large Volume Infusion Systems (Volumetric Pumps), Syringe Infusion Systems, Insulin Infusion Systems, Elastomeric Infusion Pumps, Enteral Feeding Pumps, Implantable Infusion Pumps, Ambulatory Infusion Pumps, Patient-Controlled Analgesia (PCA) Pumps), by Technology (Traditional Infusion Systems, Smart / Specialty Infusion Systems), by Mode of Administration (Intravenous (IV) Infusion, Subcutaneous Infusion, Enteral Infusion, Epidural Infusion, Others), by Application (Oncology / Chemotherapy, Diabetes Management, Pain Management (Analgesia), Nutrition (Parenteral & Enteral), Gastroenterology, Pediatrics & Neonatology, Hematology, Others), by Usage (Stationary Infusion Systems, Ambulatory / Portable Infusion Systems), by End User (Hospitals, Ambulatory Surgical Centers (ASCs), Home Healthcare Settings, Clinics, Nursing Homes / Long-Term Care Facilities)

| Status : Published | Published On : Apr, 2026 | Report Code : VRHC1334 | Industry : Healthcare | Available Format :

|

Page : 195 |

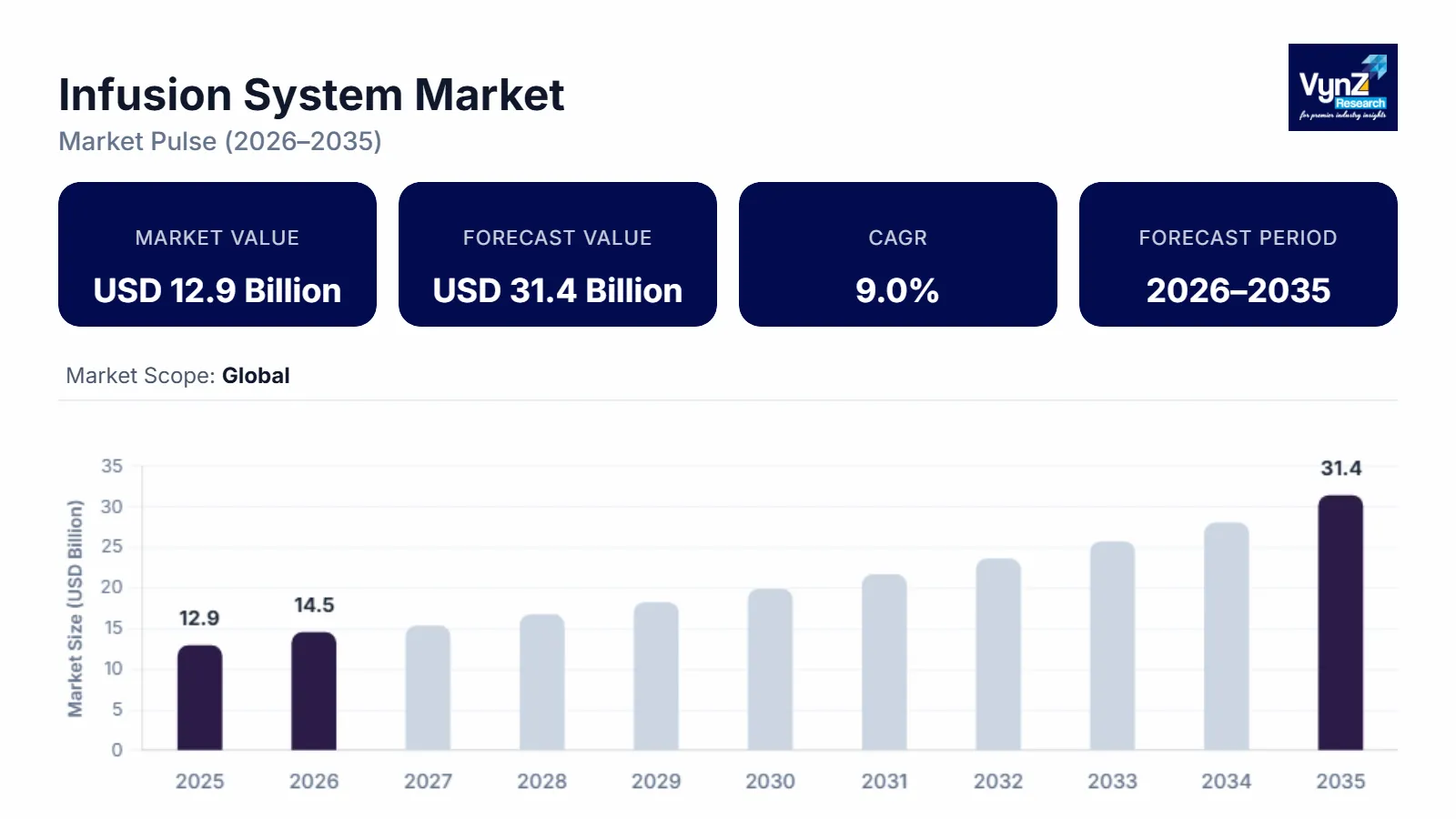

Infusion System Market Overview

The Infusion System Market which was valued at approximately USD 12.9 billion in 2025 and is estimated to reach around USD 14.5 billion in 2026, is projected to reach close to USD 31.4 billion by 2035, expanding at a CAGR of about 9.0% during the forecast period from 2026 to 2035.

The main reason for an increase in demand of infusion pump systems, and therefore the overall infusion system market, is the growing global prevalence of chronic disease such as cancer, diabetes and cardiovascular disease. Due to this, there will be more people in hospital undergoing surgical procedures, resulting in an increase in demand for infusion pump systems. There has been an increase in the ability to accurately treat patients while ensuring their safety through technology innovation such as smart infusion pumps, dose error mitigation systems and wireless connectivity, and this type of technology should be utilised more often in healthcare organisations.

An additional factor leading to a long-term requirement for infusion therapies is the ageing population of the world. This demographic is at a higher risk of developing chronic disease, and therefore will have an ongoing requirement for infusion therapy. Furthermore, the rapid increase in demand for infusion pump systems and other products within the infusion system market can be attributed to the trends toward home health care and ambulatory care services. This is because portable and user-friendly infusion systems allow treatments to take place outside of the hospital setting. Additionally, improvements in government programmes, investment into healthcare infrastructure, and the general availability of high-quality medical equipment in developing economies is improving access to the same. Finally, there is an increased emphasis placed upon patient safety and medication administration on behalf of healthcare professionals. As a result, they are utilising new infusion technologies.

Infusion System Market Dynamics

Market Trends

Home healthcare and ambulatory infusion are two trends which have made it possible for people to receive their treatment at home instead of staying in hospitals. Home-based treatments are less expensive and allow people to continue their normal routines. Because these devices are portable, safe, easy-to-use and can provide medication in many different locations outside of a hospital, they help support the shift from hospital to home-based therapies. To improve local production in the medical device industry, the Indian government has established a USD 400+ million PLI scheme specifically for the medical devices sector and will be providing financial incentives to producers of critical medical devices such as infusion pumps and associated systems. Healthcare providers are trying to promote outpatient care models so that there is an increase in efficiency and a reduction in pressure placed on hospitals. As well as being able to reduce the number of visits by patients to hospitals, clinicians are now able to monitor the progress of patients through the use of new remote monitoring technologies and compact pump designs. The trend toward home-based care is growing rapidly because of the increased awareness of infections related to hospital stays. Insurance providers and healthcare systems are also encouraged to do so because of the economic benefits of ambulatory infusion services..

Growth Drivers

The growing number of chronic disease cases has become a major factor for the increased utilisation of the infusion system across many countries' health systems. Many of the chronic disease cases, including diabetes, cancer, cardiovascular disease and autoimmune diseases, require long-term treatment using infusion equipment. These long-term treatments typically involve finely controlling the amount of medication administered over time, and thus infusion pumps are an important piece of medical equipment to provide effective patient treatment. Chronic illness cases are placing long-term pressures on hospitals, clinics and home care service providers to develop effective drug delivery systems. Due to lifestyle changes and increasing urban populations, there is no indication that the rate of increase of chronic disease cases will slow down globally. As a result, many people are having to rely on portable infusion devices at their homes instead of making repeated trips to the hospital for their ongoing treatment needs. Healthcare providers are increasingly relying on infusion technology to effectively manage complex treatment protocols. It appears that the trend toward more chronic disease cases will continue and, as such, the demand for infusion systems will continue to grow in coming years.

Market Restraints / Challenges

The high expense of advanced infusion systems continues to represent an obstacle for this technology to develop further in terms of market potential. The cost of implementing smart infusion pump systems that utilise contemporary technology, including smart features, communication capabilities and safety features, is typically very high and represents a financial burden to hospitals. This is one reason why smaller healthcare organisations and private practices do not purchase or implement smart infusion pump systems because they simply cannot afford them. In addition to being expensive to purchase, the ongoing expenses associated with maintenance, upgrading software and training employees should not be overlooked. Advanced infusion technologies are frequently unable to be implemented in developing countries due to budgetary constraints, resulting in lower-quality patient treatments. Additionally, using advanced medical devices such as infusion pump systems to treat patients in private healthcare settings may increase the total cost of treatment. Because of limited budgets, government-funded healthcare facilities will delay replacing older infusion systems with newer versions; this delay will result in decreased efficiency and safety. Manufacturers of infusion pump systems are experiencing an increasing demand to find a way to provide innovative products while keeping prices affordable so as to expand their customer base.

Market Opportunities

Emerging markets present an incredible opportunity for companies operating in the global infusion system market as there is a growing demand for healthcare services. With the development of infrastructure in many countries, including China, and increased access to healthcare services, there is a large potential for increased demand for infusion systems. In addition to this, several countries in Asia Pacific, such as India, Latin America and the Middle East are building new hospitals and clinics. Moreover, governments in these countries are spending billions of dollars on modernising their healthcare infrastructures through the construction of new hospitals and other medical facilities. In addition to this, increases in per capita incomes in many developing economies are allowing an increasing number of people to pay for expensive treatments that require the use of infusion systems. There has been an increase in the number of cases of chronic and infectious diseases in recent years in various parts of the world, including Asia Pacific, Latin America and the Middle East. As a result, it is becoming increasingly important for these countries to develop reliable methods for delivering drugs. Government policies are supporting the modernisation of healthcare through new regulations and additional funding for medical equipment, creating strong growth opportunities for infusion system manufacturers.

Global Infusion System Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 12.9 Billion |

|

Revenue Forecast in 2035 |

USD 31.4 Billion |

|

Growth Rate |

9.0% |

|

Segments Covered in the Report |

Product Type, Technology, Mode of Administration, Application, Usage, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia-Pacific, Latin America, Middle East & Africa |

|

Key Companies |

Becton, Dickinson and Company, Baxter International Inc., B. Braun Melsungen AG, Fresenius SE & Co. KGaA, ICU Medical, Inc., Medtronic plc, Smiths Group plc, Terumo Corporation, Nipro Corporation, Moog Inc., Micrel Medical Devices S.A., Insulet Corporation |

|

Customization |

Available upon request |

Infusion System Market Segmentation

By Product Type

Large Volume Infusion Systems (Volumetric Pumps) are the largest segment with a market share of about 30% in 2025, as they have been widely used in hospitals to provide continuous and large volume fluid delivery for many different treatments such as hydration, antibiotics and other critical care treatments. Because volumetric pumps can be used continuously to provide a very steady flow rate, they are often seen as an important device within the in-patient setting. They continue to maintain this strong position due to their ability to provide a consistent infusion rate throughout long treatment periods.

Ambulatory Infusion Pumps is the fastest growing segment with a CAGR of 9.3% during the forecast period, as hospitals continue to adopt "home care" and "outpatient care" treatment models; patients are able to be treated for their therapy such as chemo, pain control and insulin delivery outside of a hospital setting through the use of an ambulatory device which will increase patient satisfaction and reduce healthcare costs.

By Technology

Traditional Infusion Systems are the largest segment with a market share of about 60% in 2025, this can be attributed to the fact that these systems have been used for many years and are widely used throughout various types of healthcare institutions worldwide. In addition, the reliance on traditional infusion systems in low-cost environments has increased their utilisation in hospitals. Also, this type of system provides a lower-cost alternative compared to newer advanced infusion technologies. Additionally, healthcare providers continue to prefer these systems because of their familiarity with them. The continued growth of developing countries also contributes to the demand for these traditional infusion systems.

Smart / Specialty Infusion Systems are the fastest growing segment with a CAGR of 9.5% during the forecast period, as the need for advanced safety features (i.e., dose error reduction systems) and real-time infusion data tracking, along with interfacing with hospital information systems, continues to grow. These systems offer many improvements over traditional IV pumps regarding both patient safety and operational efficiency, which will encourage hospitals to invest in these products. In addition, the increased focus on minimising medication errors via the use of digital technology and regulation will also foster their development.

By Mode of Administration

Intravenous (IV) Infusion is the largest segment with a market share of about 55% in 2025, due to the fact that this method of administering fluids, medications or nutrients directly into the bloodstream provides an instantaneous therapeutic effect. This method of treatment is also widely utilised in hospital settings and emergency situations, as well as in many other healthcare applications due to its reliability and efficiency. As a result, IV infusion will continue to be one of the most commonly used methods of treatment.

Subcutaneous Infusion is the fastest growing segment with a CAGR of 9.6% during the forecast period, due to increasing use in long-term treatments for various chronic conditions (e.g. biologics; insulin) which provide ease and comfort for patients when used at home. Its accelerated growth is backed by the increasing popularity of minimally invasive and self-administered procedures.

By Application

Oncology / Chemotherapy is the largest segment with a market share of about 25% in 2025, the growing incidence of cancer worldwide has led to an increased need for continuous delivery of chemotherapeutic agents; however, accurate and constant delivery of these agents can be difficult without proper use of infusion systems. The increasing population of treatment centres and targeted therapies have kept the demand in this segment growing.

Diabetes Management is the fastest growing segment during the forecast period, because of the increasing number of people diagnosed with diabetes and an increase in the number of patients using insulin infusion pumps as part of their long-term continuous blood sugar level management. Continuous delivery of insulin through these pumps provides an improved outcome for patients by providing a controlled and precise delivery of insulin. The growing awareness levels and use of wearable insulin pumps, along with the growing use of the devices, make the segment grow rapidly.

By Usage

Stationary Infusion Systems are the largest segment with a market share of about 65% in 2025, due to the fact that these systems provide the ability for continuous or periodic monitoring; therefore, they can be used in hospitals, intensive care units and/or in surgical areas where high volume infusion may be necessary. Because of its reliability and capabilities of administering multiple treatments over long periods of time, this type of infusion system has become preferred in many medical facilities. Their leading role is due to their established presence in the healthcare infrastructure.

Ambulatory / Portable Infusion Systems are the fastest growing segment during the forecast period, due to increasing demand for outpatient care and home-based interventions. The convenience and flexibility provided by these types of systems allows the patient to complete therapy while at home. The growth is triggered by the rising pressure on healthcare costs and higher mobility of patients.

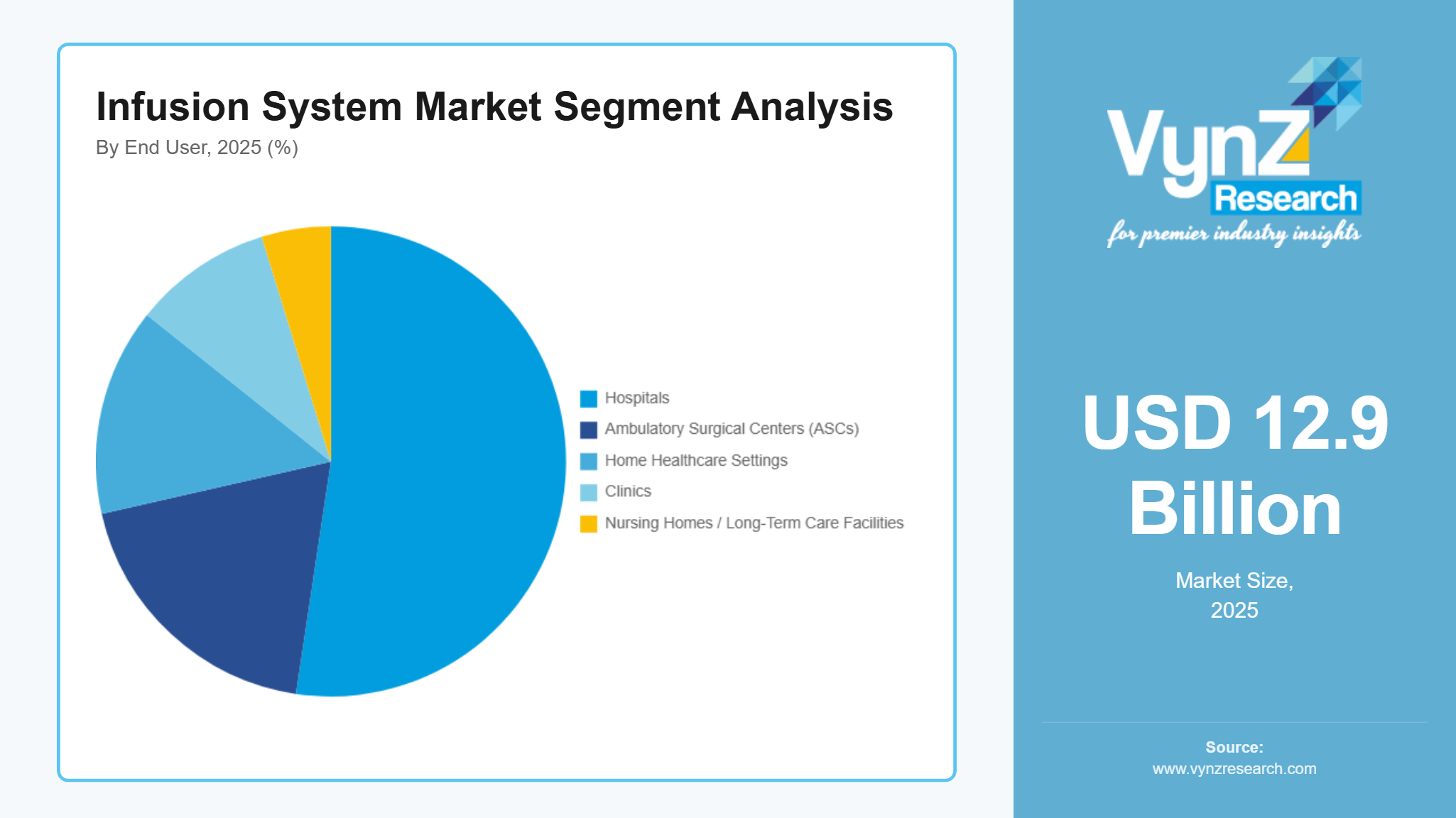

By End User

Hospitals are the largest segment with a market share of about 55% in 2025, due to their high volume of patient populations for in-patient treatments, surgeries and critical care patients who require IV (intravenous) infusions. These institutions have both the physical resources and skilled professionals needed to provide complex infusion therapy services. They are the key players in the provision of healthcare, and this makes the infusion systems demand to be sustained.

Home Healthcare Settings are the fastest growing segment during the forecast period, as there will be an increasing amount of long-term disease management and decentralised care at home. Hospital visits by patients will occur less frequently while they enjoy a better level of comfort, and as a result, the burden on the health system for operations is decreased. The development of portable infusion devices and remote monitoring technologies also contribute to this trend.

Regional Insights

North America

North America accounted for approximately 38% of the market in 2025, driven by advanced healthcare infrastructure, high healthcare expenditure, and strong adoption of smart and connected infusion technologies across the United States and Canada. Strong demand from major hospital networks, ICUs, and home healthcare providers continues to support market growth. According to the U.S. Agency for Healthcare Research and Quality (AHRQ), ongoing investments in patient safety and medication management systems are accelerating adoption of advanced infusion solutions.

Government initiatives, combined with rising chronic disease burden and ageing population, are encouraging investments in smart infusion pumps and integrated digital healthcare systems, while expansion of outpatient and home care services is further strengthening regional performance.

Asia-Pacific

Asia Pacific accounted for approximately 28% of the market in 2025, driven by rapid expansion of healthcare infrastructure, rising surgical volumes, and increasing government investment in hospital and ICU development across China, India, Japan, and Southeast Asia. Increasing adoption across public hospitals, private healthcare networks, and specialty care centers is driving consistent demand for infusion systems. According to China’s National Health Commission, public healthcare expenditure has exceeded CNY 2 trillion annually, supporting large-scale hospital expansion and medical equipment upgrades. Growth in Asia Pacific is supported by strong hospital construction activity, rising medical tourism, and increasing focus on patient safety and treatment accuracy, along with growing adoption of portable and home-based infusion devices.

Europe

Europe accounted for approximately 22% of the market in 2025, supported by strong healthcare systems, strict regulatory standards, and high adoption of advanced medical technologies across Germany, France, and the United Kingdom. Increasing prevalence of chronic diseases and ageing population continues to drive steady demand for infusion therapies in hospitals and outpatient care settings. According to the European Commission, ongoing funding for medical device innovation and digital health integration is strengthening healthcare modernization across the region.

Growth in Europe is supported by rising adoption of connected infusion systems, increasing focus on patient safety and compliance, and expansion of home healthcare and ambulatory services, creating stable long-term demand.

Rest of the World

The Rest of the World (Latin America, Middle East, and Africa) accounted for approximately 12% of the market in 2025, driven by improving healthcare infrastructure, rising chronic disease burden, and gradual modernization of hospital systems. Countries such as Brazil, Mexico, Saudi Arabia, and the UAE are investing in hospital expansion, ICU capacity, and advanced medical technologies. According to the World Health Organization (WHO), strengthening access to essential healthcare services in developing regions remains a key priority supporting medical device adoption. Growth in these regions is supported by government healthcare investments, expansion of private hospitals, and increasing medical tourism.

Competitive Landscape / Company Insights

Infusion system manufacturers include a wide array of both domestic and international competitors across multiple product lines, technology platforms and end-user segments. This results from the vast range of infusion device types (volumetric pumps; syringe pumps; insulin pumps; ambulatory systems) as well as the need for specific medical training for safe operation and proper design. While many large infusion equipment producers (e.g. Becton Dickinson & Co.; Baxter International Inc.; B. Braun Melsungen AG) dominate certain areas of the market, the presence of numerous mid-sized and smaller manufacturers, particularly in emerging markets, adds complexity. Due to many players offering similar products at varying prices, market concentration remains limited. Regulatory requirements, price sensitivities and healthcare infrastructure create opportunities for regional providers to meet specific clinical needs.

Manufacturers are developing smart infusion technologies, wearable and portable devices, and connected digital health systems to compete. Companies continue to enhance patient safety through dose error reduction, connectivity and user-friendly interfaces in clinical and homecare settings. Strategic initiatives include partnerships, acquisitions and product launches, along with expansion into emerging markets. Innovation, regulatory compliance and cost-effective solutions define the competitive environment.

Mini Profiles

Becton, Dickinson and Company is an international developer and producer of medical technology, including various types of infusion systems, such as smart pumps and medication management systems applied in hospitals and clinical practices.

Baxter International Inc. is a medical organization dealing with infusion pumps, IV solutions, and integrated delivery systems that aid in critical care, nutrition, and medication delivery.

B. Braun Melsungen AG is a medical devices company offering advanced infusion therapy systems, including volumetric and syringe pumps, along with comprehensive hospital solutions.

Fresenius SE & Co. KGaA is a multinational health care company that provides infusion therapy products, clinical nutrition, and medical devices via the several operating divisions.

ICU Medical, Inc. is a medical technology firm that deals with infusion therapy, IV systems and critical care products that aim at improving patient safety and efficiency of treatment.

Medtronic plc is a pioneering medical equipment company that provides insulin pumps and innovative infusion methods that are aimed at the management of diabetes and patient-centered care.

Key Players

- Becton, Dickinson and Company

- Baxter International Inc.

- B. Braun Melsungen AG

- Fresenius SE & Co. KGaA

- ICU Medical, Inc.

- Medtronic plc

- Smiths Group plc

- Terumo Corporation

- Nipro Corporation

- Moog Inc.

- Micrel Medical Devices S.A.

- Insulet Corporation

Recent Developments

In March 2026, Becton, Dickinson and Company announced enhancements to its smart infusion pump platform, focusing on improved interoperability with hospital information systems and advanced dose error reduction features to strengthen patient safety.

In February 2026, ICU Medical, Inc. has enhanced its infusion therapy offering with new product releases to enhance the safety of IVs and workflow in acute care facilities.

In November 2025, Medtronic plc reported developments on its insulin pump technologies with the emphasis to be on the automated insulin delivery system to enhance diabetes managing results.

In October 2025, B. Braun Melsungen AG announced an upgrade to its infusion pump systems with improved safety software and user interface to minimize medication errors.

Global Infusion System Market Coverage

Product Type Insight and Forecast 2026 - 2035

- Large Volume Infusion Systems (Volumetric Pumps)

- Syringe Infusion Systems

- Insulin Infusion Systems

- Elastomeric Infusion Pumps

- Enteral Feeding Pumps

- Implantable Infusion Pumps

- Ambulatory Infusion Pumps

- Patient-Controlled Analgesia (PCA) Pumps

Technology Insight and Forecast 2026 - 2035

- Traditional Infusion Systems

- Smart / Specialty Infusion Systems

Mode of Administration Insight and Forecast 2026 - 2035

- Intravenous (IV) Infusion

- Subcutaneous Infusion

- Enteral Infusion

- Epidural Infusion

- Others

Application Insight and Forecast 2026 - 2035

- Oncology / Chemotherapy

- Diabetes Management

- Pain Management (Analgesia)

- Nutrition (Parenteral & Enteral)

- Gastroenterology

- Pediatrics & Neonatology

- Hematology

- Others

Usage Insight and Forecast 2026 - 2035

- Stationary Infusion Systems

- Ambulatory / Portable Infusion Systems

End User Insight and Forecast 2026 - 2035

- Hospitals

- Ambulatory Surgical Centers (ASCs)

- Home Healthcare Settings

- Clinics

- Nursing Homes / Long-Term Care Facilities

Global Infusion System Market by Region

- North America

- By Product Type

- By Technology

- By Mode of Administration

- By Application

- By Usage

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Product Type

- By Technology

- By Mode of Administration

- By Application

- By Usage

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Product Type

- By Technology

- By Mode of Administration

- By Application

- By Usage

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Product Type

- By Technology

- By Mode of Administration

- By Application

- By Usage

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Infusion System Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Product Type

1.2.2. By

Technology

1.2.3. By

Mode of Administration

1.2.4. By

Application

1.2.5. By

Usage

1.2.6. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Product Type

5.1.1. Large Volume Infusion Systems (Volumetric Pumps)

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Syringe Infusion Systems

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Insulin Infusion Systems

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Elastomeric Infusion Pumps

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Enteral Feeding Pumps

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.1.6. Implantable Infusion Pumps

5.1.6.1. Market Definition

5.1.6.2. Market Estimation and Forecast to 2035

5.1.7. Ambulatory Infusion Pumps

5.1.7.1. Market Definition

5.1.7.2. Market Estimation and Forecast to 2035

5.1.8. Patient-Controlled Analgesia (PCA) Pumps

5.1.8.1. Market Definition

5.1.8.2. Market Estimation and Forecast to 2035

5.2. By Technology

5.2.1. Traditional Infusion Systems

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Smart / Specialty Infusion Systems

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Mode of Administration

5.3.1. Intravenous (IV) Infusion

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Subcutaneous Infusion

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Enteral Infusion

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Epidural Infusion

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Others

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.4. By Application

5.4.1. Oncology / Chemotherapy

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Diabetes Management

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Pain Management (Analgesia)

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Nutrition (Parenteral & Enteral)

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Gastroenterology

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

5.4.6. Pediatrics & Neonatology

5.4.6.1. Market Definition

5.4.6.2. Market Estimation and Forecast to 2035

5.4.7. Hematology

5.4.7.1. Market Definition

5.4.7.2. Market Estimation and Forecast to 2035

5.4.8. Others

5.4.8.1. Market Definition

5.4.8.2. Market Estimation and Forecast to 2035

5.5. By Usage

5.5.1. Stationary Infusion Systems

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Ambulatory / Portable Infusion Systems

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.6. By End User

5.6.1. Hospitals

5.6.1.1. Market Definition

5.6.1.2. Market Estimation and Forecast to 2035

5.6.2. Ambulatory Surgical Centers (ASCs)

5.6.2.1. Market Definition

5.6.2.2. Market Estimation and Forecast to 2035

5.6.3. Home Healthcare Settings

5.6.3.1. Market Definition

5.6.3.2. Market Estimation and Forecast to 2035

5.6.4. Clinics

5.6.4.1. Market Definition

5.6.4.2. Market Estimation and Forecast to 2035

5.6.5. Nursing Homes / Long-Term Care Facilities

5.6.5.1. Market Definition

5.6.5.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Product Type

6.2. By

Technology

6.3. By

Mode of Administration

6.4. By

Application

6.5. By

Usage

6.6. By

End User

6.6.1.

U.S. Market Estimate and Forecast

6.6.2.

Canada Market Estimate and Forecast

6.6.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Product Type

7.2. By

Technology

7.3. By

Mode of Administration

7.4. By

Application

7.5. By

Usage

7.6. By

End User

7.6.1.

Germany Market Estimate and Forecast

7.6.2.

France Market Estimate and Forecast

7.6.3.

U.K. Market Estimate and Forecast

7.6.4.

Italy Market Estimate and Forecast

7.6.5.

Spain Market Estimate and Forecast

7.6.6.

Russia Market Estimate and Forecast

7.6.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Product Type

8.2. By

Technology

8.3. By

Mode of Administration

8.4. By

Application

8.5. By

Usage

8.6. By

End User

8.6.1.

China Market Estimate and Forecast

8.6.2.

Japan Market Estimate and Forecast

8.6.3.

India Market Estimate and Forecast

8.6.4.

South Korea Market Estimate and Forecast

8.6.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Product Type

9.2. By

Technology

9.3. By

Mode of Administration

9.4. By

Application

9.5. By

Usage

9.6. By

End User

9.6.1.

Brazil Market Estimate and Forecast

9.6.2.

Saudi Arabia Market Estimate and Forecast

9.6.3.

South Africa Market Estimate and Forecast

9.6.4.

U.A.E. Market Estimate and Forecast

9.6.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Becton, Dickinson and Company

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Baxter International Inc.

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

B. Braun Melsungen AG

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Fresenius SE & Co. KGaA

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

ICU Medical, Inc.

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Medtronic plc

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Smiths Group plc

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Terumo Corporation

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Nipro Corporation

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Moog Inc.

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

Micrel Medical Devices S.A.

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

10.12.

Insulet Corporation

10.12.1.

Snapshot

10.12.2.

Overview

10.12.3.

Offerings

10.12.4.

Financial

Insight

10.12.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Infusion System Market