Patient Warming Device Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Device Type (Surface Warming Devices, Fluid Warming Devices, Intravascular Warming Devices, Radiant Warmers, Patient Warming Accessories, Others), by Technology (Conductive, Convective, Fluid-Based, Radiant, Others), by Application (Perioperative Care, Postoperative Care, Acute & Critical Care, Neonatal & Pediatric Care, Therapeutic), by End User (Hospitals, Ambulatory Surgical Centers, Home Care Settings, Specialty Clinics, Others)

| Status : Published | Published On : Apr, 2026 | Report Code : VRHC1333 | Industry : Healthcare | Available Format :

|

Page : 195 |

Patient Warming Device Market Overview

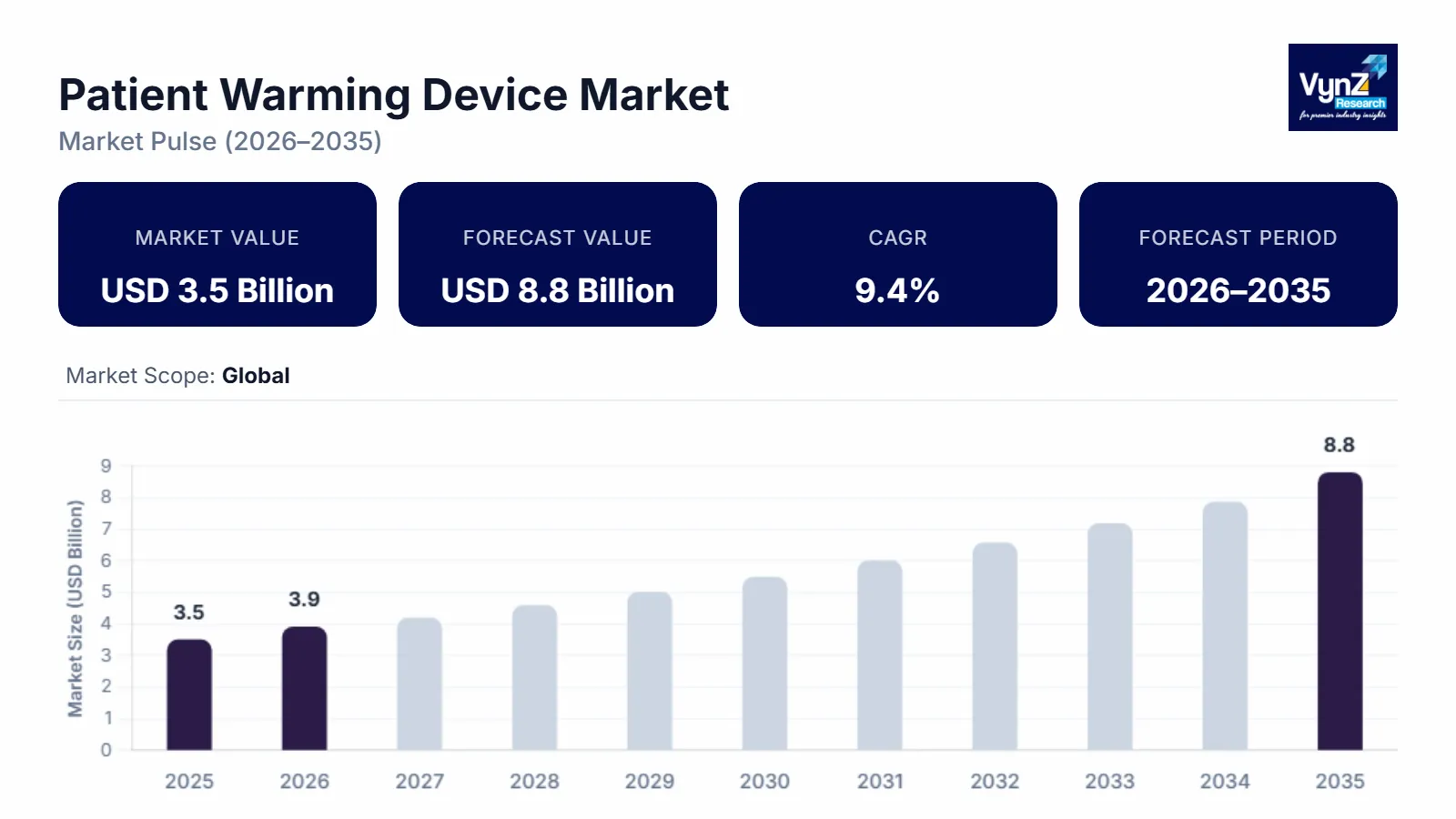

The patient warming device market which was valued at approximately USD 3.5 billion in 2025 and is estimated to reach around USD 3.9 billion in 2026, is projected to reach close to USD 8.8 billion by 2035, expanding at a CAGR of about 9.4% during the forecast period from 2026 to 2035.

The market is growing as a result of the clinical focus on maintaining normothermia and improved patient safety. Temperature management devices are no longer seen as supportive functions in hospitals or surgical centres; instead, they have become core clinical protocols that directly impact outcomes such as reduced post-surgical complications, faster recovery times, and shorter hospital stays. The increase in surgical volumes, particularly among ageing populations with chronic conditions, has increased demand for reliable and efficient warming solutions. Healthcare systems are also increasing pressure to improve operational efficiency, which will include reducing risks associated with patient warming devices and related costs. Innovation in this area has further accelerated adoption by creating more precise, portable, and real-time integrated monitoring systems that allow clinicians to provide targeted thermal care across multiple care settings, including operating rooms and home care environments.

In addition to these factors, the shift towards ambulatory and outpatient care is expanding the use of compact, easy-to-deploy warming technologies. Emerging markets are also contributing to growth due to investments in healthcare infrastructure and quality standards. Together, these factors position patient warming devices not just as supporting equipment but rather as strategic tools in improving clinical performance and patient-centred care.

Patient Warming Device Market Dynamics

Market Trends

The current Federal policy and regulatory environment with respect to CMS 2026 OPPS Final Rule has created an extraordinary opportunity to introduce a paradigm shift from stationary, convective systems to high efficiency, portable, conductive and fluid-based systems. The CMS has announced a 2.6% payment increase to all outpatient providers, as well as added hundreds of additional complex surgical procedures to the ASC Covered Procedure List. In response to the regulatory changes, there will be a significant transition of surgeons from using stationary, forced-air ("convective") systems to modular surface warming devices that utilise conduction or fluid-based technology. From a corporate perspective, the introduction of these systems enables greater operational flexibility. As surgeries are being increasingly performed outside of in-patient settings (e.g., in ambulatory surgery centres), the need for compact, battery operated surface warming devices is becoming rapidly increasing.

Growth Drivers

The main factor driving growth of the patient warming device market will be the increased inclusion of thermal management within the framework of value-based health care reimbursement. Healthcare systems are now judged on their ability to deliver treatments based on outcome and total costs of care rather than solely based on treatment delivery. As a result, programmes like bundled payment models for surgical procedures have created an accountability for hospitals' financial viability with regards to complications arising from or following treatment. Maintaining normothermia is therefore no longer discretionary; it will impact both clinical performance and financial viability. An example of this trend is demonstrated through the expanded funding for new and advanced medical technology. The New Technology Add-on Payment (NTAP) programme is anticipated to increase by $192 million in FY 2026, thereby creating additional incentive for adoption of new technologies which can help decrease complication and readmission rates. As reimbursement models increasingly penalise preventable complications, healthcare providers are adopting warming technologies not only to enhance patient outcomes but also to protect margins and align with evolving payment structures.

Market Restraints / Challenges

A major obstacle in the patient warming devices market is the rapidly escalating difficulty of maintaining reliable consistency in the function of these products across various health care environments. The need for continued operation in demanding areas like ORs and ICUs will have an impact on the ability of healthcare providers to operate effectively, because even slight variations in performance may create risk to patients or disrupt workflows. Another significant issue is the ability to maintain accurate temperatures at all times during extended use and to build equipment that is durable enough to withstand this type of use. Additionally, there are added layers of operational complexity due to recent advancements in product functionality (e.g., automated sensors), which also require additional time and money from healthcare providers to train their personnel, perform regular maintenance, and ensure compatibility with existing systems. Therefore, this could limit providers' willingness to adopt these types of products, especially those who do not possess the necessary technology resources.

Market Opportunities

One of the biggest opportunities exists as patients warm in alternative environments (i.e., outside hospitals). With the move from hospitals to out-of-hospital settings like at-home care or ambulatory surgery centres, the need for low-cost, portable, and simple-to-use warming devices has increased. These changes are aligned with international healthcare objectives centred around access and continuity of care. In addition, public health organisations are continually emphasising that safety standards should be maintained regardless of the environment in which a patient receives their care. As the World Health Organization states through its Surgical Safety Framework, temperature control needs to continue for patients, even after they leave an operating room. Thus, there is tremendous potential for companies to create innovative products based on small footprint, ease-of-use designs specifically targeted towards non-hospital locations. Additionally, several developing countries, such as those located in the Asian-Pacifica region, Latin America, and Africa, have made large investments in their healthcare infrastructures, creating many opportunities for growth for businesses who develop affordable and scalable technology.

Global Patient Warming Device Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 3.5 Billion |

|

Revenue Forecast in 2035 |

USD 8.8 Billion |

|

Growth Rate |

9.4% |

|

Segments Covered in the Report |

Device Type, Technology, Application, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

3M Company, Medtronic plc, Stryker Corporation ICU Medical, Inc., GE HealthCare Technologies Inc., Becton, Dickinson and Company (BD), Baxtr International Inc., Gentherm Incorporated, Koninklijke Philips N.V., Drägerwerk AG & Co. KGaA, ZOLL Medical Corporation, Inspiration Healthcare Group plc |

|

Customization |

Available upon request |

Patient Warming Device Market Segmentation

By Device Type

Surface warming devices represent the largest category, with a market share of about 40% in 2025, for two main reasons. First, they are used extensively throughout the world in both critical care and perioperative environments. Second, surface warming devices are most frequently chosen as a result of their low-cost, easy-to-use nature and ability to provide constant thermal control. With respect to the large number of surgeries that occur around the globe on an annual basis, it follows that there is a need for thermal control in surgery. The World Health Organization reports that over 300 million surgical procedures take place every year; thus, the extent to which temperature management is needed in clinical practice is substantial. Standardised surgical protocols also include the use of surface warming devices, specifically forced air and conduction-based systems, as a normal course of action. Additionally, surface warming systems are applicable to various settings within a hospital, including recovery areas, and this broad applicability enhances their usage.

Intravascular warming devices are emerging as the fastest-growing category, with a CAGR of 9.6% during the forecast period, due to an increase in the use of precision-based temperature management techniques within high acuity patient populations. These intravascular devices allow clinicians to have total control over patients' core body temperature, which makes them especially useful in cases such as complex surgical procedures, trauma care, and critical care medicine. The increased need for both the volume of surgical procedures and improved outcomes has significantly contributed to the rapid growth of this product area. According to the World Health Organization, there would be an estimated 143 million more surgical procedures per year needed globally to meet world health needs; therefore, there will continue to be a significant strain on the healthcare system to implement more cost-efficient and technologically advanced solutions. As hospitals begin transitioning to outcome-based patient care models, there is a growing interest in utilising intravascular systems due to potential improvements in reducing postoperative complications and improving patients' recovery times.

By Technology

Convective technology, primarily represented by forced-air systems, holds the largest share due to its proven clinical effectiveness and widespread acceptance. It offers rapid and uniform heat distribution, making it ideal for perioperative applications. Hospitals favour this technology because it integrates easily into surgical workflows and delivers reliable results across a wide range of procedures. Its long-standing clinical validation has made it a trusted standard in temperature management, ensuring its continued dominance.

Conductive technology is emerging as the fastest-growing category in the coming years, because there has been a growing emphasis to reduce infections and to improve the operational efficiency of hospitals. Because they have minimal air flow, conductive systems provide an advantage over convective systems when trying to prevent contamination in sterile areas. As hospitals continue to enhance their infection control protocols, this trend will continue. In addition to improved operational efficiencies, conductive systems are also being enhanced with better materials, which enable them to transfer heat more efficiently. These improvements make conductive systems a more viable option and more attractive to today's health care environment.

By Application

Perioperative care represents the largest application category; maintaining the appropriate body temperature in a patient undergoing a surgical procedure is crucial to their well-being. The primary reason that perioperative care has become the most important application category is to maintain the patients' normal or near-normal body temperature during all surgical procedures. Maintaining the patient's normal body temperature directly affects both the reduction of potential post-surgical complications and the length of time required to recover from surgery. Because of the vast number of surgical procedures performed on a global basis, heating/cooling products have been incorporated into routine use by surgeons through inclusion in many hospital-specific operating room (OR) standards.

Acute and critical care is the fastest-growing category as a result of an increased need to continuously monitor patients, stabilise them, and provide ongoing care in a variety of acute or critically ill settings. Maintaining body temperature is important in many of these areas (i.e., trauma, sepsis, etc.) and is therefore key in providing optimal care. As hospitals continue to build out their critical care infrastructures, there will be an increasing need for dependable and accurate products that are used to warm patients.

By End User

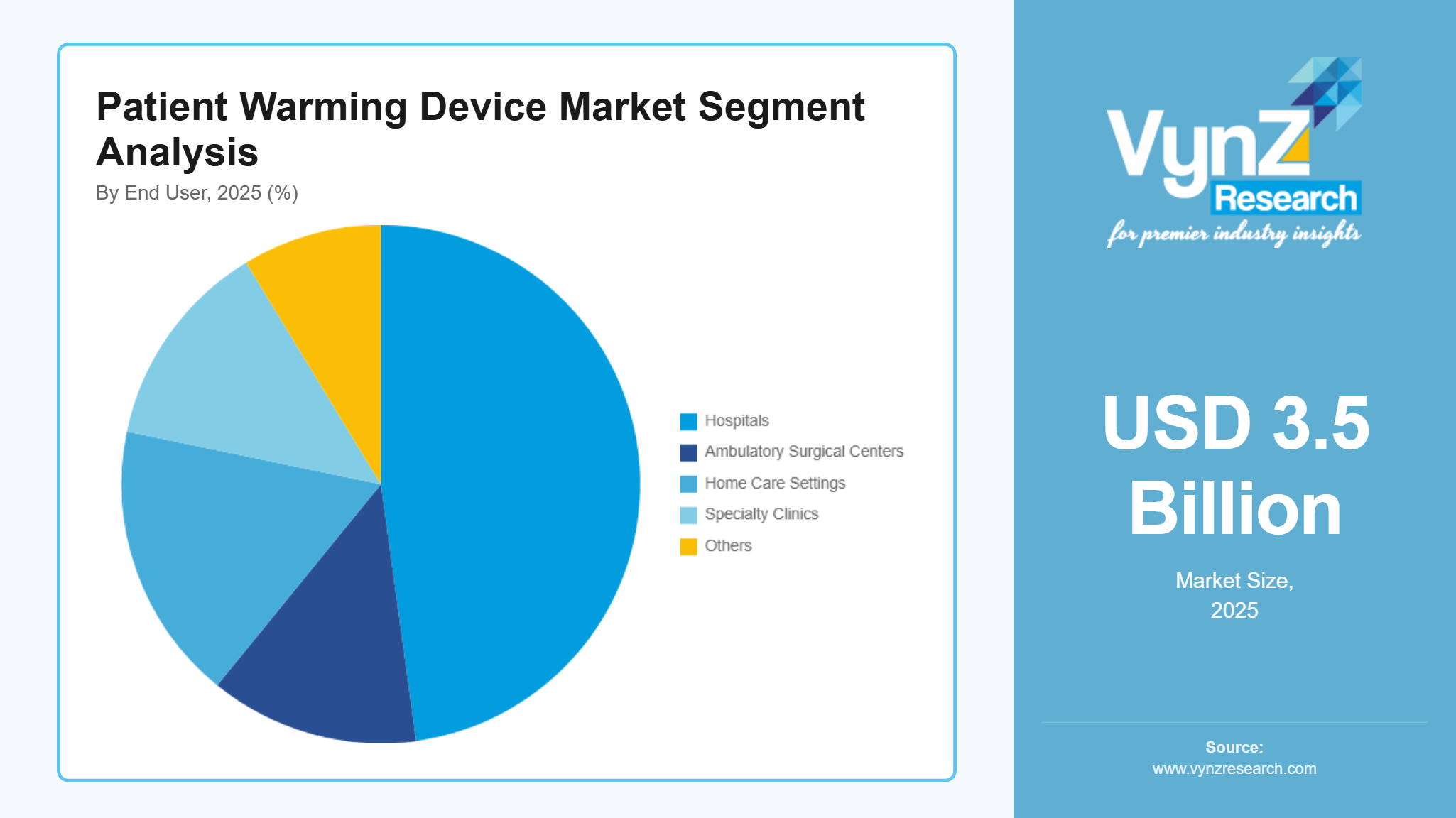

Hospitals continue to dominate the end-user landscape, with a market share of about 55% in 2025, because they are responsible for providing a wide variety of complex and high-volume care. All aspects of hospital care, from basic surgery to highly technical life sustaining intervention, are performed within hospital walls, and therefore, temperature regulation is both a supporting and clinically required function. Hospitals provide an environment that ensures consistency in how patient warming technologies can be integrated into departmental functions, utilising a structure that includes standardised protocols and ongoing monitoring capabilities. In addition to their organised environment, hospitals also have a large-scale presence in the global health care system. Consequently, this reflects their key role in the delivery of care. The combination of high volumes of patients and increased complexity of surgical procedures continues to generate a stable demand for clinical warming equipment.

Home care settings are rapidly emerging as the fastest-growing end-user category, with a CAGR of 9.9% during the forecast period, due to a trend toward patient centricity and decentralisation in healthcare delivery. The focus is shifting away from traditional hospital-based models toward enabling patients to recover and manage chronic conditions in their homes. Devices designed to provide patient warming have become increasingly important to this transition, particularly for elderly patients requiring stable thermal control for continued recovery and ongoing chronic care. There are demographic forces driving the shift toward greater use of home-based care. By 2030, it is projected that one in six individuals worldwide will be 60 years old or older, up from one billion in 2020 to 1.4 billion and eventually increasing to 2.1 billion by 2050. Additionally, the number of individuals aged 80 and above is expected to increase to 426 million and continue to create demand for innovative, non-clinical based care options.

Regional Insights

Asia Pacific

The Asia Pacific market is witnessing steady growth due to rapid expansion of healthcare infrastructure, rising surgical volumes, and increasing government investment in hospital modernization across China, India, Japan, and Southeast Asia. Increasing adoption across hospitals, surgical centers, and emerging medical tourism hubs is driving consistent demand for patient warming devices. According to India’s Ministry of Health and Family Welfare, continued investments under national healthcare strengthening programs are improving access to advanced surgical and critical care infrastructure.

Growth in Asia Pacific is supported by hospital expansion projects, increasing focus on patient safety standards, and rising awareness of perioperative hypothermia management, creating long-term opportunities for market participants.

Europe

Europe accounted for approximately 22% of the market in 2025, supported by strong regulatory frameworks, high patient safety standards, and well-established hospital infrastructure across Germany, France, the United Kingdom, Italy, and Nordic countries. Increasing adoption in surgical, ICU, and recovery care settings continues to support steady demand. According to the European Commission, healthcare modernization and quality-of-care initiatives under EU health programs are supporting upgrades in hospital infrastructure and clinical equipment.

Growth in Europe is supported by ongoing hospital modernization, strict infection control and safety regulations, and increasing adoption of standardized perioperative care protocols, creating stable long-term demand.

North America

North America accounted for approximately 38% of the market in 2025, driven by advanced healthcare infrastructure, high surgical volumes, and strong emphasis on perioperative patient safety across the United States and Canada. Strong demand from major hospital networks and surgical centers continues to support market growth. According to the U.S. Centers for Medicare & Medicaid Services (CMS), reimbursement frameworks for hospital-based procedures continue to encourage adoption of advanced perioperative care technologies, including temperature management systems.

Government initiatives, combined with rising focus on value-based healthcare and outcome improvement, are encouraging investments in advanced patient warming systems, while strong hospital networks and established procurement systems are further strengthening regional performance.

Rest of the World

The rest of the world, including Latin America, the Middle East, and Africa, accounted for approximately 15% of the market in 2025, driven by improving healthcare access, rising investments in hospital infrastructure, and expanding surgical capacity in emerging economies. Countries such as Brazil, Mexico, Saudi Arabia, and South Africa are increasing adoption of critical care and perioperative equipment. According to the World Health Organization (WHO), continued focus on strengthening surgical care systems in low- and middle-income countries is improving access to essential medical technologies.

Growth in these regions is supported by healthcare infrastructure development, expansion of private hospitals, and government-led health system upgrades, creating long-term opportunities for market participants. Collectively, the above regions account for nearly 75–80% of the global patient warming devices market, while the remaining share is distributed across smaller developing markets worldwide.

Competitive Landscape / Company Insights

The patient warming device industry has a relatively fragmented (moderately consolidated) level of competition. There will be large, well-established companies that compete globally across all areas of the product line, and there will also be many small, regionally focused companies developing specialised products at lower price points than those developed by larger competitors. These small and regionally based companies will have a distinct competitive advantage, as they can develop products specifically designed to meet the demands of localised markets.

These two different types of competitors will create a very competitive market in which product development, pricing, and regulatory issues will become major factors. To remain competitive, it appears that these companies will need to focus on creating unique products, integrating "smart" features into their existing products, and expanding their sales into new emerging countries. With an increased focus on patient safety and value-based health care delivery systems, this competition is likely to continue to grow, as both established and emerging competitors compete for position with respect to innovative technology, reliable performance, and a larger international footprint.

Mini Profiles

Medtronic plc is a global medical technology company offering device-based therapies across cardiovascular, neuroscience, and surgical care. It operates worldwide with a strong focus on improving patient outcomes through innovation.

Stryker Corporation develops and manufactures medical devices and surgical equipment used in hospitals. Its portfolio supports areas such as orthopedics, neurotechnology, and patient safety.

GE HealthCare Technologies Inc. provides medical imaging, monitoring, and diagnostic solutions. The company focuses on advancing precision care through digital and data-driven healthcare technologies.

Koninklijke Philips N.V. is a health technology company delivering diagnostic, treatment, and connected care solutions. It emphasizes integrated systems to improve patient care across clinical settings.

3M Company offers a range of healthcare solutions, including patient warming and infection prevention products. The company focuses on improving clinical outcomes through advanced material technologies.

Key Players

- 3M Company

- Medtronic plc

- Stryker Corporation

- ICU Medical, Inc.

- GE HealthCare Technologies Inc.

- Becton, Dickinson and Company (BD)

- Baxter International Inc.

- Gentherm Incorporated

- Koninklijke Philips N.V.

- Drägerwerk AG & Co. KGaA

- ZOLL Medical Corporation

- Inspiration Healthcare Group plc

Recent Developments

In March 2026, Medtronic plc announced its plan to acquire Scientia Vascular, strengthening its neurovascular portfolio and enhancing precision-based treatment capabilities in stroke care.

In March 2026, GE HealthCare Technologies Inc. expanded its multi-year strategic alliance with Medtronic plc, focusing on integrated monitoring solutions, wearable technologies, and perioperative care innovation.

In December 2025, Koninklijke Philips N.V. agreed to acquire SpectraWAVE Inc., strengthening its capabilities in advanced coronary intravascular imaging and AI-enabled physiological assessment technologies.

In November 2025, Siemens Healthineers AG announced the expansion of its AI-enabled imaging and diagnostics platform, enhancing workflow automation and precision imaging across hospital networks globally.

In January 2026, Baxter International Inc. introduced upgraded connected infusion systems with enhanced safety monitoring and interoperability features to improve critical care medication delivery in hospital settings.

Global Patient Warming Device Market Coverage

Device Type Insight and Forecast 2026 - 2035

- Surface Warming Devices

- Fluid Warming Devices

- Intravascular Warming Devices

- Radiant Warmers

- Patient Warming Accessories

- Others

Technology Insight and Forecast 2026 - 2035

- Conductive

- Convective

- Fluid-Based

- Radiant

- Others

Application Insight and Forecast 2026 - 2035

- Perioperative Care

- Postoperative Care

- Acute & Critical Care

- Neonatal & Pediatric Care

- Therapeutic

End User Insight and Forecast 2026 - 2035

- Hospitals

- Ambulatory Surgical Centers

- Home Care Settings

- Specialty Clinics

- Others

Global Patient Warming Device Market by Region

- North America

- By Device Type

- By Technology

- By Application

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Device Type

- By Technology

- By Application

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Device Type

- By Technology

- By Application

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Device Type

- By Technology

- By Application

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Patient Warming Device Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Device Type

1.2.2. By

Technology

1.2.3. By

Application

1.2.4. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Device Type

5.1.1. Surface Warming Devices

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Fluid Warming Devices

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Intravascular Warming Devices

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Radiant Warmers

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Patient Warming Accessories

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.1.6. Others

5.1.6.1. Market Definition

5.1.6.2. Market Estimation and Forecast to 2035

5.2. By Technology

5.2.1. Conductive

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Convective

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Fluid-Based

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Radiant

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. Others

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.3. By Application

5.3.1. Perioperative Care

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Postoperative Care

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Acute & Critical Care

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Neonatal & Pediatric Care

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Therapeutic

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.4. By End User

5.4.1. Hospitals

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Ambulatory Surgical Centers

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Home Care Settings

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Specialty Clinics

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Others

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Device Type

6.2. By

Technology

6.3. By

Application

6.4. By

End User

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Device Type

7.2. By

Technology

7.3. By

Application

7.4. By

End User

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Device Type

8.2. By

Technology

8.3. By

Application

8.4. By

End User

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Device Type

9.2. By

Technology

9.3. By

Application

9.4. By

End User

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

3M Company

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Medtronic plc

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Stryker Corporation

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

ICU Medical, Inc.

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

GE HealthCare Technologies Inc.

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Becton, Dickinson and Company (BD)

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Baxter International Inc.

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Gentherm Incorporated

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Koninklijke Philips N.V.

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Drägerwerk AG & Co. KGaA

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

ZOLL Medical Corporation

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

10.12.

Inspiration Healthcare Group plc

10.12.1.

Snapshot

10.12.2.

Overview

10.12.3.

Offerings

10.12.4.

Financial

Insight

10.12.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Patient Warming Device Market