U.S. TIC Market for Medical Devices Industry Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Sourcing Type (In-house, Outsourced), by Service Type (Testing, Inspection, Certification), by Industry Vertical (In-vitro diagnostics, Diagnostic equipment, Patient monitoring, Orthopaedic, Cardiovascular, Home healthcare, Others)

| Status : Published | Published On : Apr, 2026 | Report Code : VRHC1333 | Industry : Healthcare | Available Format :

|

Page : 128 |

U.S. TIC Market for Medical Devices Industry Overview

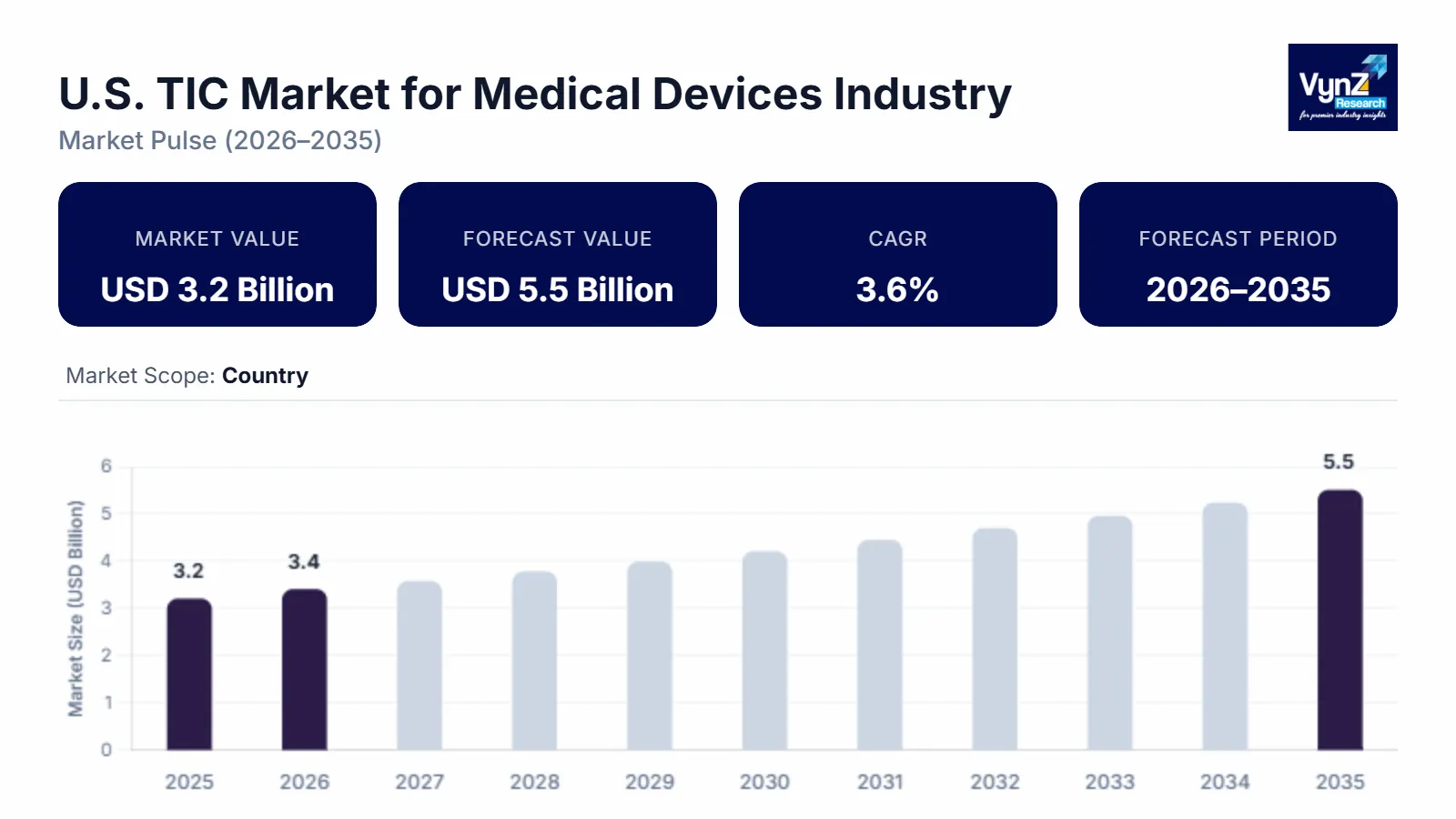

The U.S. TIC market for medical devices which was valued at approximately USD 3.2 billion in 2025 and is estimated to rise further up to almost USD 3.4 billion by 2026, is projected to reach around USD 5.5 billion in 2035, expanding at a CAGR of about 3.6% during the forecast period from 2026 to 2035.

Market growth results from three forces which include increasing regulatory compliance needs, the rising difficulty of medical device technology and the growing demand for product safety testing and quality control which combined with the increasing use of third-party testing and certification services. Advanced diagnostic and monitoring devices experience rising demand from healthcare facilities which receive ongoing funding to build healthcare quality infrastructure according to regulatory authorities like the World Health Organization and the U.S. Food and Drug Administration. This development leads to market growth across all major regions which include the United States, and Canada and Mexico.

U.S. TIC Market for Medical Devices Industry Dynamics

Market Trends

The market has established its contemporary technological framework through dual systems that empower organizations to establish standardized testing procedures while executing digital monitoring of their quality control processes. The increasing implementation of cybersecurity and software validation solutions represents the market's primary development because it shows the industry's movement toward safer products that can work with other systems while managing risks throughout their operational life. WHO and FDA publish their regulations to create digital health safety protocols, post market surveillance standards and testing methods for digital health technologies. The market requires companies to develop integrated solutions which will allow them to deliver advanced testing infrastructure together with compliance driven differentiation solutions because regulatory bodies demand TIC services while businesses need solutions to handle their growing technology requirements.

Growth Drivers

The market experiences growth acceleration through increasing regulatory scrutiny and compliance requirements which create ongoing demand across all device categories, including diagnostic, monitoring and therapeutic devices. The market expansion receives further acceleration from rising investments made into healthcare infrastructure which includes quality assurance systems and advanced manufacturing environments. The increased use of software-based medical devices that connect to other devices has created greater demand for testing and certification services specialized in these areas. The demand for third-party TIC services will stay strong because manufacturers are focusing their efforts on performance and patient safety and regulatory compliance. The WHO and FDA regulatory bodies support public health frameworks and device safety initiatives which enhance market growth through standard compliance practices.

Market Restraints / Challenges

The market faces specific growth impediments even though it shows strong potential for future expansion. Small and mid-sized manufacturers with constrained compliance budgets experience market entry challenges because of two factors, which are complex regulations and high certification expenses. The U.S. Food and Drug Administration reports together with their regulatory framework requirements show that companies must complete extensive validation, documentation and auditing processes to obtain medical device approvals, which creates operational challenges for their organizations. Service providers experience operational difficulties because they need skilled professionals and advanced testing infrastructure to deliver testing services. Organizations have to spend more money on testing technology that needs specialized expertise; this makes it hard for them to grow their business during times when regulatory changes and technological changes happen.

Market Opportunities

Digital health and remote monitoring validation services create valuable market opportunities that major technology advancements and rising need for connected healthcare solutions have established. Medical device manufacturers and healthcare providers will buy more security testing solutions from the marketplace because vendors provide technology testing solutions that maintain high performance standards while running tests at various scales. The market opportunity for integrated TIC platform expansion presents business prospects because organizations that invest in digital enabled compliance solutions will experience better operational efficiency and customer relationships. The service delivery process will become more efficient through automation and artificial intelligence testing and real-time monitoring systems will enable faster regulatory processing times. The World Health Organization and other organizations spend money on digital health programs and strategic initiatives, which will enable them to create new innovations while achieving their long-term growth targets.

U.S. TIC Market for Medical Devices Industry Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 3.2 Billion |

|

Revenue Forecast in 2035 |

USD 5.5 Billion |

|

Growth Rate |

5.6% |

|

Segments Covered in the Report |

Sourcing Type, Service Type, Industry Vertical |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

Northeast, Midwest, Southern, Western |

|

Key Companies |

Bureau Veritas, DEKRA SE, Element Materials Technology, Eurofins Scientific, Intertek Group plc., SGS SA, The British Standards Institution, TUV Rheinland, TUV SUD, UL LLC |

|

Customization |

Available upon request |

U.S. TIC Market for Medical Devices Industry Segmentation

By Sourcing Type

The outsourced segment accounted for the largest market share in 2025, estimated at nearly 62%, supported by increasing reliance on specialized third-party service providers offering regulatory expertise, advanced testing infrastructure, and faster certification timelines. Medical device manufacturers are increasingly shifting toward external partners to manage compliance complexities and reduce operational overheads, particularly in highly regulated product categories. The market will experience a growth rate of 3.9% between 2026 and 2035 because companies need complete TIC solutions that operate throughout all product lifecycle stages.

The in-house segment will experience steady growth at 3.1% in the forecast period because manufacturers need to keep their quality assurance systems for essential testing and validation work. Organizations are now adopting hybrid sourcing methods because they face rising costs for both physical infrastructure enhancements and the need for qualified staff. Businesses need to develop both internal capabilities and outsourcing partnerships to handle the increasing number of regulations and changing compliance standards which results in segment growth.

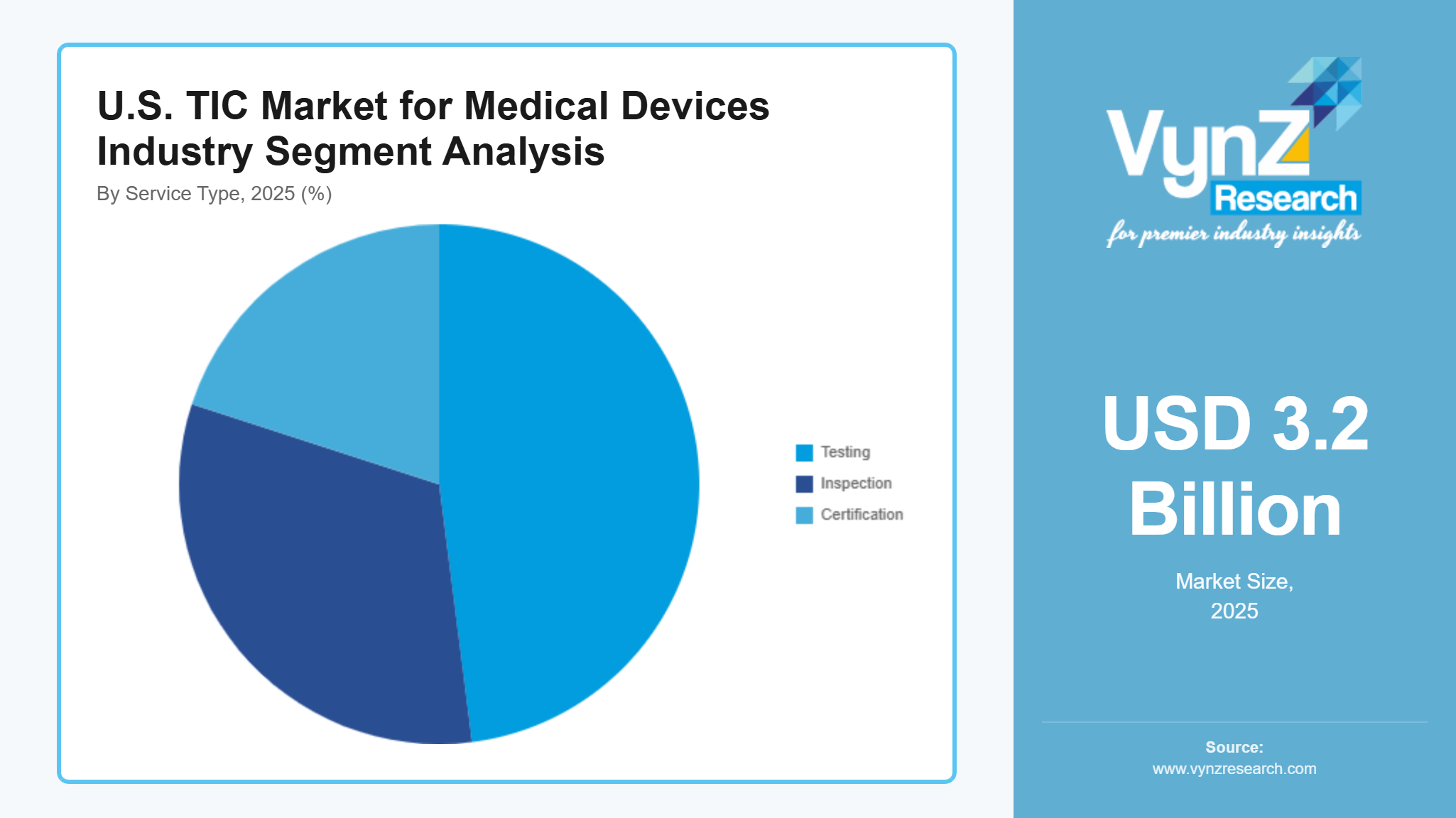

By Service Type

The testing segment dominated the market in 2025 with an estimated share of around 48%, supported by extensive demand for performance validation, safety testing, and compliance verification across a wide range of medical devices. The growing number of software-driven devices which require complex testing services that include electromagnetic compatibility and cybersecurity validation testing. The medical technologies market will grow at a rate of 3.8% because the industry develops new products while regulators introduce more demanding compliance measures.

The certification segment is anticipated to witness the fastest growth, expanding at a CAGR of about 4.1%, supported by rising demand for regulatory approvals and global market access. The increasing need for international quality standards compliance has led manufacturers to allocate more funds towards certification service development. The inspection service maintains its vital function of manufacturing process control and product quality assurance while achieving a 3.3% growth rate through existing production monitoring and audit practices.

By Industry Vertical

The diagnostic systems segment accounted for the largest market share in 2025, estimated at approximately 29%, supported by high utilization rates and continuous demand for accurate and reliable diagnostic solutions. The market for testing and certification services will expand at a rate of 3.7% because healthcare facilities need these services to meet current requirements for advanced imaging and in vitro diagnostic technologies.

The monitoring devices segment will experience the highest growth rate with a 4.2% compound annual growth rate because of increasing needs for tools that allow medical professionals to monitor patients from a distance and use wearable health devices. Increasing digital health solution usage together with connected device systems will drive major shifts in TIC needs for this particular area. Therapeutic equipment maintains its steady development at 3.4% growth rate because treatment technology research generates new medical procedures that People who receive treatment for medical issues. Other application areas also contribute steadily, driven by niche innovations and evolving clinical requirements.

Regional Insights

Northeast

The market in 2025 saw the Northeast United States region contribute about 21% of the total market share because Massachusetts and New York had many research bodies and advanced medical systems and major medical device manufacturers. The Boston and New Jersey innovation centers maintain market expansion by producing new products and carrying out regulatory filings. The U.S. Food and Drug Administration testing and certification requirements maintain a continuous need for testing and certification work throughout the year. The continuous validation process along with quality assurance standards for all device categories exists because of the strong academic and clinical research ecosystems which help create new validation requirements.

Midwest

The Midwest United States maintained an 18% market share in 2025 because manufacturing clusters already existed and businesses required economical production and regulatory compliance solutions across Illinois Indiana and Minnesota. The area possesses strong industrial capabilities combined with rising investments in medical device manufacturing facilities. The increasing need for diagnostic and therapeutic devices among elderly people in this area drives organizations to use TIC services. The expansion of manufacturing standards and federal healthcare regulations drives demand for inspection and certification services in production facilities.

Southern

The Southern United States market share reached approximately 20% in 2025 because Texas and Florida experienced fast healthcare infrastructure growth and increased medical manufacturing investment and rising healthcare service demands. The region expands through rising usage of connected medical devices and hospital network growth which needs ongoing compliance verification and safety evaluation. The growth of insurance coverage and government healthcare programs leads to higher advanced medical technology adoption which creates greater demand for TIC services. The rising number of contract manufacturing organizations in the area boosts local demand for their services.

Western

The Western United States held the largest market share in 2025 with 19% due to California and Washington showing strong technological developments and having major medical technology companies and their quick transition to digital health technologies. The region attracts funding to research and develop AI-enabled medical devices and connected healthcare technologies. The U.S. Food and Drug Administration cybersecurity software validation and device interoperability frameworks lead to rising demand for advanced TIC services. The active venture capital market together with the startup ecosystem in this region drives both innovation and compliance needs.

The total market share for these regions is 78% while the rest of the market share comes from smaller states and new clusters which this analysis does not include.

Competitive Landscape / Company Insights

The market shows moderate competition because international certification authorities and local companies who provide specialized services to their customers with technology, regulatory compliance and market access. Companies are building their market strength through investments in advanced testing technologies and cybersecurity validation and integrated compliance platforms. The U.S. Food and Drug Administration's regulatory frameworks and safety standards together with World Health Organization global guidance drive all market participants to develop innovative products and maintain quality standards and find unique ways to differentiate their products.

Mini Profiles

Bureau Veritas focuses on testing, inspection, and certification services for medical devices, supported by strong global presence, regulatory expertise, and advanced laboratory infrastructure ensuring compliance and quality assurance across healthcare markets.

DEKRA SE operates in specialized and safety critical segments, emphasizing performance validation, risk assessment, and certification services, with strong focus on compliance standards and industrial safety across medical and healthcare applications.

Element Materials Technology leverages advanced testing laboratories, strategic partnerships, and technical expertise to expand market presence, offering comprehensive materials testing and certification solutions tailored to medical device manufacturers and suppliers.

Intertek Group plc. focuses on quality assurance, testing, and certification services, supported by extensive global network, strong brand recognition, and integrated compliance solutions across medical device and healthcare sectors.

SGS SA operates in premium and compliance driven segments, emphasizing accuracy, reliability, and global standardization, with strong capabilities in inspection, verification, testing, and certification services for regulated medical industries.

Key Players

- Bureau Veritas

- DEKRA SE

- Element Materials Technology

- Eurofins Scientific

- Intertek Group plc.

- SGS SA

- The British Standards Institution

- TUV Rheinland

- TUV SUD

- UL LLC

Recent Developments

In December 2025, Eurofins Scientific expanded its capabilities in life sciences and medical device testing by strengthening laboratory infrastructure and analytical services. The company focused on enhancing specialized testing solutions to support increasing regulatory and quality requirements across healthcare sectors.

In December 2025, TÜV SÜD invested in expanding electric and medical device testing infrastructure, aligning with evolving safety and compliance standards. The company emphasized digital certification platforms and advanced testing protocols to improve efficiency and accuracy.

In January 2026, TÜV Rheinland enhanced its digital inspection and certification services by integrating AI-based validation systems for complex technologies. The initiative focused on improving compliance processes and reducing testing timelines across regulated industries including medical devices.

In January 2026, UL LLC expanded its advanced safety testing and certification services, particularly in connected and software-driven medical devices. The company focused on strengthening cybersecurity validation and global compliance capabilities to address evolving regulatory requirements.

In November 2025, The British Standards Institution introduced updated standards and guidance frameworks to support safety, compliance, and risk management across industries. These developments emphasized structured certification processes and improved quality assurance practices aligned with global regulatory expectations.

U.S. TIC Market for Medical Devices Industry Coverage

Sourcing Type Insight and Forecast 2026 - 2035

- In-house

- Outsourced

Service Type Insight and Forecast 2026 - 2035

- Testing

- Inspection

- Certification

Industry Vertical Insight and Forecast 2026 - 2035

- In-vitro diagnostics

- Diagnostic equipment

- Patient monitoring

- Orthopaedic

- Cardiovascular

- Home healthcare

- Others

U.S. TIC Market for Medical Devices Industry by Region

- Northeast

- By Sourcing Type

- By Service Type

- By Industry Vertical

- Midwest

- By Sourcing Type

- By Service Type

- By Industry Vertical

- Southern

- By Sourcing Type

- By Service Type

- By Industry Vertical

- Western

- By Sourcing Type

- By Service Type

- By Industry Vertical

Table of Contents for U.S. TIC Market for Medical Devices Industry Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Sourcing Type

1.2.2. By

Service Type

1.2.3. By

Industry Vertical

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. U.S. Market Estimate and Forecast

4.1. U.S. Market Overview

4.2. U.S. Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Sourcing Type

5.1.1. In-house

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Outsourced

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.2. By Service Type

5.2.1. Testing

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Inspection

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Certification

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By Industry Vertical

5.3.1. In-vitro diagnostics

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Diagnostic equipment

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Patient monitoring

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Orthopaedic

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Cardiovascular

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.3.6. Home healthcare

5.3.6.1. Market Definition

5.3.6.2. Market Estimation and Forecast to 2035

5.3.7. Others

5.3.7.1. Market Definition

5.3.7.2. Market Estimation and Forecast to 2035

6. Northeast Market Estimate and Forecast

6.1. By

Sourcing Type

6.2. By

Service Type

6.3. By

Industry Vertical

7. Midwest Market Estimate and Forecast

7.1. By

Sourcing Type

7.2. By

Service Type

7.3. By

Industry Vertical

8. Southern Market Estimate and Forecast

8.1. By

Sourcing Type

8.2. By

Service Type

8.3. By

Industry Vertical

9. Western Market Estimate and Forecast

9.1. By

Sourcing Type

9.2. By

Service Type

9.3. By

Industry Vertical

10. Company Profiles

10.1.

Bureau Veritas

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

DEKRA SE

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Element Materials Technology

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Eurofins Scientific

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Intertek Group plc.

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

SGS SA

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

The British Standards Institution

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

TUV Rheinland

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

TUV SUD

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

UL LLC

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

U.S. TIC Market for Medical Devices Industry