U.S. TIC Market for Pharmaceuticals and Biotech Industry Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Service Type (Testing, Inspection, Certification), by Sourcing Type (In house, Outsourced), by Technology (Conventional Testing Methods, Rapid Microbiological Methods, Digital and Automated Validation Systems), by End User (Pharmaceutical Companies, Biotechnology Firms, Contract Research and Manufacturing Organizations)

| Status : Published | Published On : Apr, 2026 | Report Code : VRHC1334 | Industry : Healthcare | Available Format :

|

Page : 132 |

U.S. TIC Market for Pharmaceuticals and Biotech Industry Overview

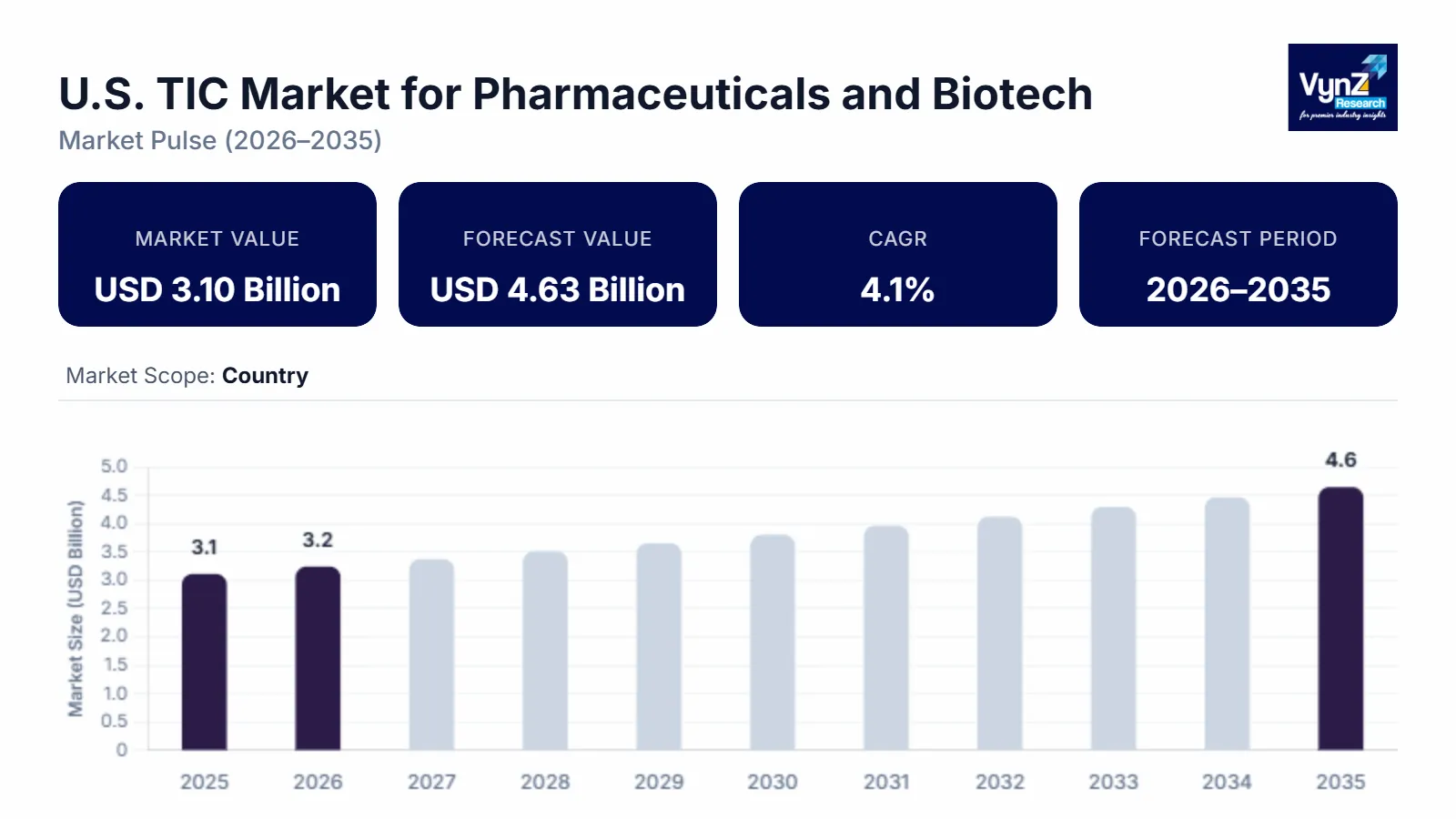

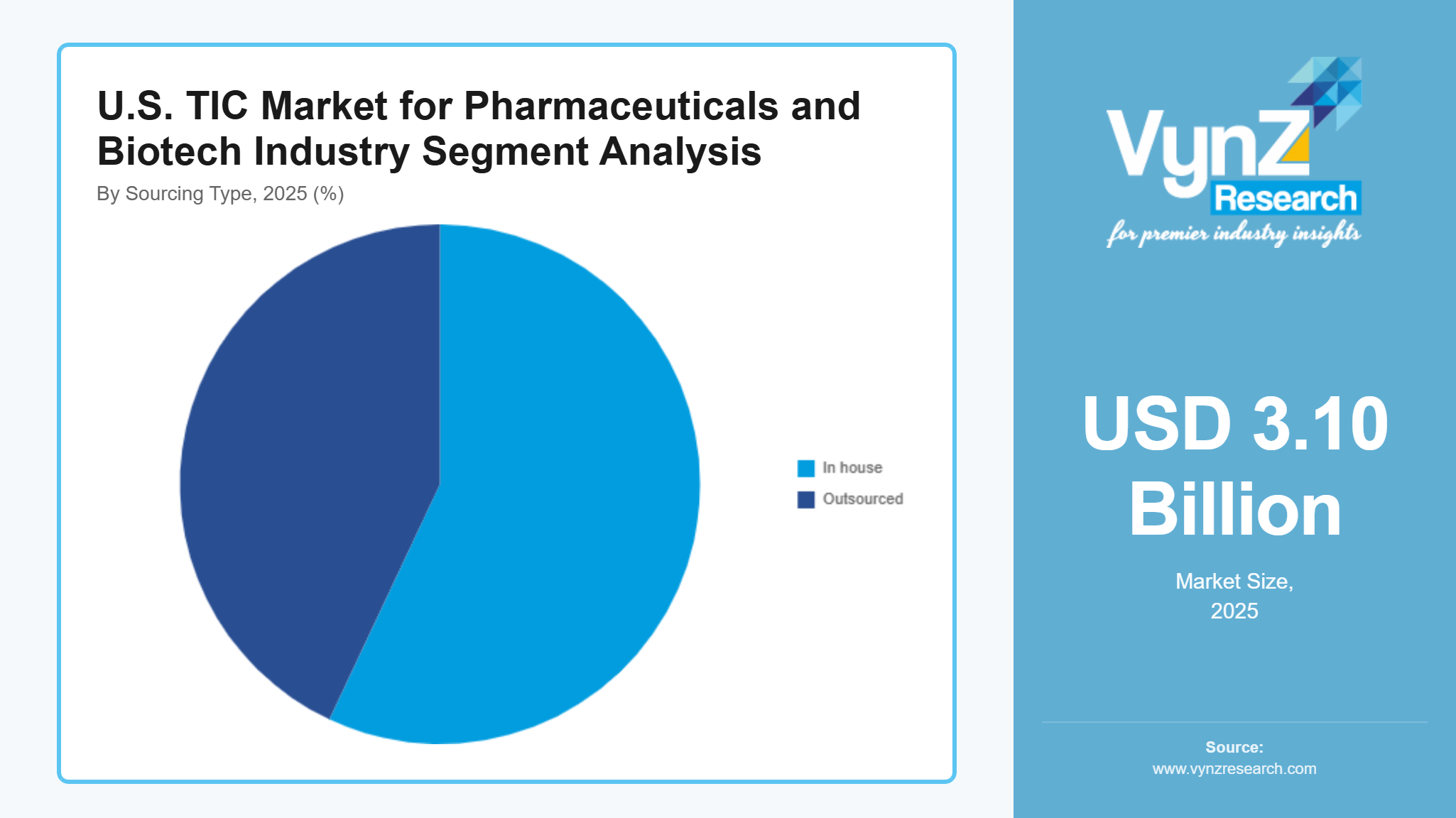

The U.S. TIC market for pharmaceuticals and biotech industry which was valued at approximately USD 3.10 billion in 2025 and is estimated to rise further up to almost USD 3.23 billion by 2026, is projected to reach around USD 4.63 billion in 2035, expanding at a CAGR of about 4.1% during the forecast period from 2026 to 2035.

The market expansion results from three main factors which include the rising need for regulatory compliance, the increasing complexity of pharmaceutical manufacturing processes, and the growing demand for quality assurance in both biologics and advanced therapies, along with the rising use of third-party testing and inspection and certification services. The market expansion in major regions including California, Massachusetts and New Jersey receives support from two factors which include the increasing need for safe drug production and the regulatory strengthening efforts by the U.S. Food and Drug Administration and World Health Organization.

U.S. TIC Market for Pharmaceuticals and Biotech Industry Dynamics

Market Trends

The market is currently experiencing substantial technological changes together with increased compliance requirements which particularly target advanced quality assurance frameworks and digital compliance systems. The market evolves through a growing trend of organizations implementing risk-based inspection and real time monitoring systems which enhance efficiency while providing complete traceability and maintaining regulatory transparency. The U.S. Food and Drug Administration and World Health Organization provide frameworks which enable organizations to adopt standardized quality systems, protect data integrity, and implement lifecycle-based compliance, thus driving manufacturers to utilize automated testing and digital validation tools throughout their production facilities.

Growth Drivers

The market grows because regulatory compliance requirements create ongoing demand which exists throughout pharmaceutical manufacturing and biologics production and clinical research environments. Market growth receives acceleration from the expanding drug development infrastructure and the construction of new biologics manufacturing facilities. Regulatory frameworks issued by authorities such as the U.S. Food and Drug Administration mandate rigorous testing, inspection, and certification protocols, which reinforce the need for third party compliance services throughout the entire value chain.

The adoption of biologics and advanced therapies through their fast growth pattern has become a vital factor which supports industry expansion. The demand for specialized testing and validation services will remain strong during the forecast period because pharmaceutical companies now prioritize product safety and quality consistency and global compliance with health guidelines and quality standards established by the World Health Organization.

Market Restraints / Challenges

The market shows strong growth potential but the industry faces multiple obstacles which will restrict its market expansion. Small and mid-sized manufacturers face operational efficiency and cost structure challenges because they must comply with multiple product category requirements which require their teams to handle regulatory compliance work. The U.S. Food and Drug Administration require organizations to update their validation methods and quality system documentation and validation procedures. The requirement for organizations to keep their validation documentation up to date and quality systems running creates extra compliance work for them. Service providers face operational difficulties because they need both highly skilled technical workers and advanced testing equipment to deliver their services. The market performance in times of economic uncertainty will suffer because specialized expertise becomes rare and laboratory technologies become expensive, which creates both cost pressures and scalability problems according to global capacity and workforce assessments conducted by the World Health Organization.

Market Opportunities

The market has major growth potential through expanding digital and automated compliance solutions which emerge from technological improvements and the rising complexity of pharmaceutical production processes. Integrated testing and certification services which provide high performance and scalability will enable companies to capture growing business from biologics manufacturers and contract research organizations and emerging biotech firms. Government initiatives which support pharmaceutical innovation and establish quality standards create an environment which enables new technologies to emerge throughout advanced manufacturing ecosystems.

The current market opportunity exists because advanced therapy testing services have gained popularity through precision medicine and biologics investments, which create demand for high value service offerings and long-term partnerships. The operational efficiency of organizations will improve through automation and data analytics and digital validation platforms, which also help organizations comply with regulations established by the U.S. Food and Drug Administration and international quality standards set by the World Health Organization.

U.S. TIC Market for Pharmaceuticals and Biotech Industry Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 3.10 Billion |

|

Revenue Forecast in 2035 |

USD 4.63 Billion |

|

Growth Rate |

4.1% |

|

Segments Covered in the Report |

Service Type, Sourcing Type, Technology, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

Northeast, West, Midwest, South, Other Regions |

|

Key Companies |

Applus+, Bureau Veritas, Element Materials Technology, Eurofins Scientific, Intertek Group plc, SGS SA, The Lloyd Register Group Limited, TUV Rheinland, TUV SUD, UL LLC |

|

Customization |

Available upon request |

U.S. TIC Market for Pharmaceuticals and Biotech Industry Segmentation

By Service Type

Testing services achieved the largest market share during 2025 when they generated approximately 48% of total revenue. Their dominance is maintained through their frequent use in drug development biologics validation and batch release processes which need to meet strict quality standards enforced by agencies like the U.S. Food and Drug Administration. The pharmaceutical and biotech manufacturing environments require laboratory-based analytical testing due to increasing regulatory requirements that focus on product safety and sterility assurance and data integrity between facilities.

Certification services will grow the most rapidly between 2026 and 2035 when the market will experience a CAGR increase that reaches 4.6%. Rising global compliance validation needs and standardization of quality systems and international trade participation growth combine to create this expansion. International trade participation and global compliance validation requirements and quality system standardization needs drive this growth.

Inspection services experience ongoing growth because manufacturing facilities require supervised production processes and regulatory audits that check their operations. The segment will expand at an estimated CAGR of 3.8% because high risk production environments need constant monitoring to ensure compliance particularly in biologics and sterile drug manufacturing operations.

By Sourcing Type

Pharmaceutical and biotech companies choose to use outsourced services because they want to achieve cost savings and operational flexibility while gaining access to specialized knowledge which led these services to capture 57% of the market in 2025. Companies depend on third-party service providers to handle their complete compliance and validation needs because drug formulations and regulatory requirements have become more challenging to manage.

The demand for scalable testing infrastructure drives outsourced services to experience their highest growth rate which will reach a CAGR of 4.4% between 2026 and 2035. The service accessibility and efficiency of contract manufacturing and research organizations receive improvements through advanced laboratory technology and global service network integration.

In-house services remain important for pharmaceutical companies who have existing internal capabilities. The segment will grow at an estimated CAGR of 3.5% which will enable organizations to achieve direct quality control and proprietary process management capabilities for high-value biologics and innovative drug pipelines.

By Technology

The testing market achieved its biggest revenue share during 2025 when conventional methods generated approximately 51% of total segment income. Established protocols and regulatory acceptance and the widespread deployment of pharmaceutical manufacturing facilities continue to sustain their market position. The U.S. Food and Drug Administration verification standards serve as a basis for sustaining product adoption throughout the industry.

Digital and automated validation systems will achieve their fastest growth between 2026 and 2035 when the market will experience a CAGR increase that reaches 4.8% annual growth. Modern data-driven compliance tools together with real-time monitoring systems and operational automation technologies now enable organizations to streamline their work through accurate results which reduce their operational work duration. Organizations now require data integrity frameworks that meet global quality standards from the World Health Organization to support their digital transformation initiatives according to regulatory mandates. Rapid microbiological methods are also gaining traction because sterile manufacturing environments require faster contamination detection and better process efficiency.

By End User

Pharmaceutical companies generated 54% of the market revenue during 2025 which made them the top revenue generator for the industry. Their market position comes from their ability to produce drugs at large scale while meeting extensive regulatory standards and making ongoing investments into both drug development and quality assurance systems. Government-backed regulatory frameworks and inspection protocols continue to reinforce demand within this segment.

Biotechnology firms are witnessing the fastest growth with an estimated CAGR of 4.7% because the industry now concentrates on developing biologics and gene therapies and advanced treatment technologies. The segment continues to grow because organizations need to operate their R&D activities while employing special testing and validation services.

Pharmaceutical value chain organizations use contract research and manufacturing services which lead to sustained market growth through their increasing outsourcing activities. The segment will grow at an estimated CAGR of 4.0% because organizations need to implement compliance solutions that cover their entire global supply chain.

Regional Insights

Northeast

In 2025, the United States Northeast region maintained a 27% share of the market, which developed from its strong research base in drug development and biologics production combined with its regulatory manufacturing practices. The testing, inspection, and certification service market continues to grow because Boston, New York City, and Philadelphia function as major service centers. The U.S. Food and Drug Administration established strict compliance requirements for the region, which creates ongoing demand for validation and quality assurance services.

The region is projected to grow at an estimated CAGR of 4.3%, driven by increasing biologics approvals, expansion of clinical research pipelines, and rising investments in precision medicine. Government funding research programs together with public health projects encourage organizations to implement modern testing and compliance methods.

West

The United States West held a market share of 22% during 2025 because of its strong biotechnology sector and ongoing development of new treatment methods and digital healthcare technologies. Key cities such as San Francisco, San Diego, and Seattle are major contributors to regional demand.

The region is expected to grow at a CAGR of 4.5%, supported by increasing adoption of automated testing platforms and digital compliance tools. Advanced validation system adoption is growing because governments and World Health Organization standards along with national agency standards create regulatory modernization requirements together with essential quality criteria.

Midwest

The United States Midwest held an estimated 18% market share during 2025 because of its developing pharmaceutical manufacturing sector and contract production business. Cities including Chicago, Indianapolis, and Columbus are emerging as key industrial hubs for compliance driven production.

The region is expected to grow at a 3.9% CAGR because of rising funding for big manufacturing plants and supply chain efficiency projects. The United States Food and Drug Administration-backed government manufacturing programs together with their regulatory inspection initiatives continue to drive TIC service requests from the entire region.

South

The United States South region obtained a 23% market share during 2025 because of its rapidly expanding pharmaceutical production system and supportive investment regulations. Major cities such as Houston, Raleigh, and Atlanta are witnessing increasing adoption of testing and certification services across manufacturing and research facilities.

The region is expected to grow at a CAGR of 4.2% because domestic drug production and biologics manufacturing capacity continue to increase. The demand for government supply chain resilience initiatives and quality compliance programs, which support the development of healthcare infrastructure, will continue throughout the region. The remaining demand which amounts to 10% is distributed among emerging clusters and smaller regions which have not been mentioned yet.

Competitive Landscape / Company Insights

The market operates with moderate competition because established global companies and specialized regional service providers use their innovation, compliance expertise and service integration capabilities to compete in this market. Companies are investing in laboratory infrastructure digital validation platforms and automation technologies to build their competitive position in the market. The U.S. Food and Drug Administration regulatory frameworks and quality standards together with World Health Organization global guidance define how companies develop their competitive strategies and their unique service offerings.

Mini Profiles

Applus+ focuses on inspection, testing, and certification services for pharmaceuticals and industrial sectors, supported by strong global presence, technical expertise, and diversified service portfolio across regulated and compliance driven markets.

Bureau Veritas operates in premium compliance and certification segments, emphasizing quality assurance, regulatory expertise, and performance driven inspection services across pharmaceutical manufacturing and biotechnology value chains.

Element Materials Technology leverages advanced laboratory capabilities and strategic partnerships to expand market presence, offering specialized testing and validation services for complex pharmaceutical and biotech applications.

Intertek Group plc focuses on integrated quality assurance solutions, supported by extensive global network, digital capabilities, and strong brand recognition across pharmaceutical testing and certification services.

SGS SA operates in mass and premium segments, emphasizing reliability, global accreditation, and comprehensive inspection and certification services tailored for pharmaceutical and biotechnology industries.

Key Players

- Applus+

- Bureau Veritas

- Element Materials Technology

- Eurofins Scientific

- Intertek Group plc

- SGS SA

- The Lloyd Register Group Limited

- TUV Rheinland

- TUV SUD

- UL LLC

Recent Developments

In February 2025, Bureau Veritas entered advanced negotiations with SGS SA for a potential merger valued at over USD 33 billion. This strategic move aims to strengthen combined capabilities across testing, inspection, and certification services in regulated industries.

In January 2026, SGS SA expanded its focus on AI driven inspection and digital quality assurance solutions aligned with evolving industry demand. This reflects increasing adoption of automated inspection technologies across pharmaceutical and life sciences sectors.

In December 2025, Applus+ was highlighted in industry reports emphasizing its growing role in global TIC market expansion and service diversification. The company continues to strengthen its position through integrated testing and certification solutions across regulated sectors.

In January 2025, Intertek Group plc expanded its presence in life sciences TIC services, focusing on advanced testing capabilities and compliance solutions. This development aligns with increasing regulatory requirements and demand for high quality assurance services.

In December 2025, UL LLC continued strengthening its certification and compliance portfolio within the TIC market through innovation in safety and performance standards. The company remains focused on expanding global certification capabilities for regulated industries.

U.S. TIC Market for Pharmaceuticals and Biotech Industry Coverage

Service Type Insight and Forecast 2026 - 2035

- Testing

- Inspection

- Certification

Sourcing Type Insight and Forecast 2026 - 2035

- In house

- Outsourced

Technology Insight and Forecast 2026 - 2035

- Conventional Testing Methods

- Rapid Microbiological Methods

- Digital and Automated Validation Systems

End User Insight and Forecast 2026 - 2035

- Pharmaceutical Companies

- Biotechnology Firms

- Contract Research and Manufacturing Organizations

U.S. TIC Market for Pharmaceuticals and Biotech Industry by Region

- Northeast

- By Service Type

- By Sourcing Type

- By Technology

- By End User

- West

- By Service Type

- By Sourcing Type

- By Technology

- By End User

- Midwest

- By Service Type

- By Sourcing Type

- By Technology

- By End User

- South

- By Service Type

- By Sourcing Type

- By Technology

- By End User

- Other Regions

- By Service Type

- By Sourcing Type

- By Technology

- By End User

Table of Contents for U.S. TIC Market for Pharmaceuticals and Biotech Industry Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Service Type

1.2.2. By

Sourcing Type

1.2.3. By

Technology

1.2.4. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. U.S. Market Estimate and Forecast

4.1. U.S. Market Overview

4.2. U.S. Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Service Type

5.1.1. Testing

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Inspection

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Certification

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Sourcing Type

5.2.1. In house

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Outsourced

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Technology

5.3.1. Conventional Testing Methods

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Rapid Microbiological Methods

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Digital and Automated Validation Systems

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.4. By End User

5.4.1. Pharmaceutical Companies

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Biotechnology Firms

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Contract Research and Manufacturing Organizations

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

6. Northeast Market Estimate and Forecast

6.1. By

Service Type

6.2. By

Sourcing Type

6.3. By

Technology

6.4. By

End User

7. West Market Estimate and Forecast

7.1. By

Service Type

7.2. By

Sourcing Type

7.3. By

Technology

7.4. By

End User

8. Midwest Market Estimate and Forecast

8.1. By

Service Type

8.2. By

Sourcing Type

8.3. By

Technology

8.4. By

End User

9. South Market Estimate and Forecast

9.1. By

Service Type

9.2. By

Sourcing Type

9.3. By

Technology

9.4. By

End User

10. Other Regions Market Estimate and Forecast

10.1. By

Service Type

10.2. By

Sourcing Type

10.3. By

Technology

10.4. By

End User

11. Company Profiles

11.1.

Applus+

11.1.1.

Snapshot

11.1.2.

Overview

11.1.3.

Offerings

11.1.4.

Financial

Insight

11.1.5.

Recent

Developments

11.2.

Bureau Veritas

11.2.1.

Snapshot

11.2.2.

Overview

11.2.3.

Offerings

11.2.4.

Financial

Insight

11.2.5.

Recent

Developments

11.3.

Element Materials Technology

11.3.1.

Snapshot

11.3.2.

Overview

11.3.3.

Offerings

11.3.4.

Financial

Insight

11.3.5.

Recent

Developments

11.4.

Eurofins Scientific

11.4.1.

Snapshot

11.4.2.

Overview

11.4.3.

Offerings

11.4.4.

Financial

Insight

11.4.5.

Recent

Developments

11.5.

Intertek Group plc

11.5.1.

Snapshot

11.5.2.

Overview

11.5.3.

Offerings

11.5.4.

Financial

Insight

11.5.5.

Recent

Developments

11.6.

SGS SA

11.6.1.

Snapshot

11.6.2.

Overview

11.6.3.

Offerings

11.6.4.

Financial

Insight

11.6.5.

Recent

Developments

11.7.

The Lloyd Register Group Limited

11.7.1.

Snapshot

11.7.2.

Overview

11.7.3.

Offerings

11.7.4.

Financial

Insight

11.7.5.

Recent

Developments

11.8.

TUV Rheinland

11.8.1.

Snapshot

11.8.2.

Overview

11.8.3.

Offerings

11.8.4.

Financial

Insight

11.8.5.

Recent

Developments

11.9.

TUV SUD

11.9.1.

Snapshot

11.9.2.

Overview

11.9.3.

Offerings

11.9.4.

Financial

Insight

11.9.5.

Recent

Developments

11.10.

UL LLC

11.10.1.

Snapshot

11.10.2.

Overview

11.10.3.

Offerings

11.10.4.

Financial

Insight

11.10.5.

Recent

Developments

12. Appendix

12.1. Exchange Rates

12.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

U.S. TIC Market for Pharmaceuticals and Biotech Industry