Cloud OSS BSS Market - Size & Share Growth Forecast Report (2026-2035)

Industry Insight by Component (Solutions, Services), by Deployment (Public Cloud, Private Cloud, Hybrid Cloud), by Application (Customer Management, Revenue Management, Service Fulfillment, Service Assurance, Network Management), by End User (Telecom Service Providers, Enterprises)

| Status : Published | Published On : Jul, 2026 | Report Code : VRICT5239 | Industry : ICT & Media | Available Format :

|

Page : 146 |

Cloud OSS BSS Market Overview

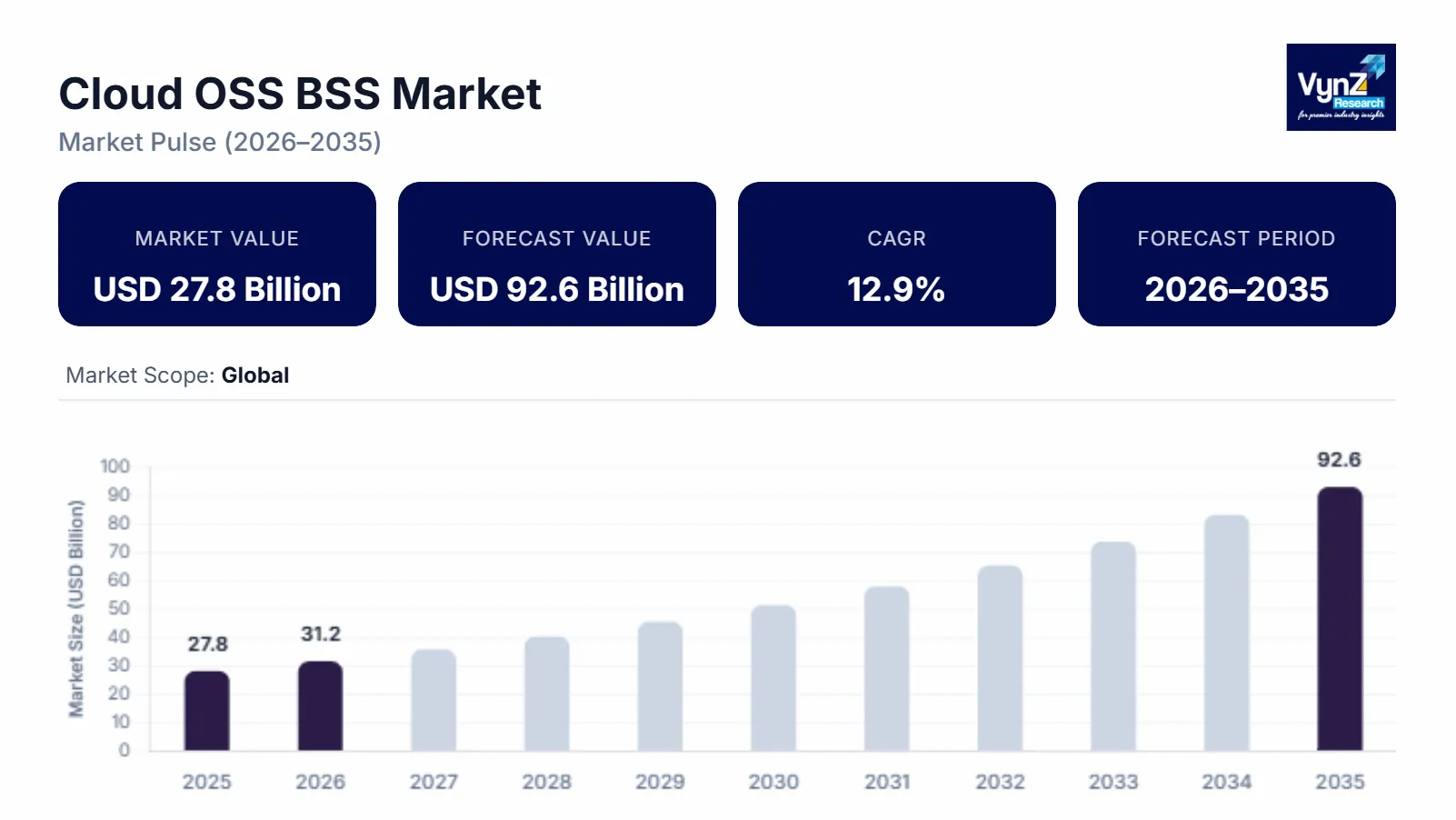

The cloud OSS BSS market size was estimated at about USD 27.8 billion in 2025 and is expected to reach around USD 31.2 billion in 2026, rising up to roughly USD 92.6 billion by 2035, growing at approximately 12.9% CAGR from 2026 to 2035.

Research Highlights

- Solutions held 67.4% share in 2025 driven by accelerating cloud native telecom transformation.

- In 2025, public cloud captured 58.1% share supported by scalable infrastructure and cost efficiency.

- Customer management generated 38.6% revenue owing to rising digital customer engagement.

- The enterprise segment is expected to grow at approximately 14.5% CAGR due to higher adoption.

- In 2025, North America held 36.8% share, driven by advanced cloud and telecom infrastructure.

Market growth is supported by accelerating 5G network deployment, increasing telecom cloud transformation and increasing network automation requirements, along with growing adoption of AI enabled OSS BSS platforms. Growing demand for real time billing, digital customer experience and service orchestration and ongoing investments in digital connectivity programs by the International Telecommunication Union (ITU), U.S. Federal Communications Commission (FCC) and the European Commission Digital Decade Program are further supporting market expansion across major regions including North America, Europe, and Asia Pacific.

Cloud OSS BSS Market Dynamics

Market Trends

The industry is witnessing notable shifts in cloud native network management, AI driven service orchestration and automated customer lifecycle management. One of the key trends shaping the market is the adoption of AI enabled OSS BSS platforms, reflecting increasing demand for operational efficiency, real time analytics and service agility. Another emerging trend is the integration of 5G and edge computing supported by the International Telecommunication Union (ITU) which continues to promote global digital connectivity while the GSMA reports expanding deployment of standalone 5G networks encouraging providers to deliver integrated digital service management solutions.

Growth Drivers

The growth of the market is largely supported by expanding 5G network deployments and accelerating telecom cloud transformation, generating sustained demand across communication service providers and enterprises. Increasing investments in digital infrastructure and broadband modernization are further strengthening market expansion. The U.S. Federal Communications Commission (FCC) continues to support broadband infrastructure through national connectivity initiatives while the European Commission's Digital Decade Program promotes secure digital networks encouraging telecom operators to modernize OSS and BSS platforms for improved operational efficiency.

Market Restraints / Challenges

Despite favorable growth prospects, the market faces challenges associated with complex legacy system integration and increasing cybersecurity risks which continue to affect deployment efficiency particularly among small and mid-sized telecom operators. Furthermore, dependence on highly specialized cloud technologies and skilled professionals creates implementation and operational challenges. The European Union Agency for Cybersecurity (ENISA) continues to emphasize stronger cybersecurity requirements for digital infrastructure increasing compliance obligations and implementation costs for network service providers.

Market Opportunities

The market presents significant opportunities in AI powered network automation and cloud based digital service management driven by expanding 5G adoption and increasing enterprise digital transformation. Vendors offering scalable and modular OSS BSS platforms are well positioned to capture demand from telecom operators and emerging digital service providers. Another opportunity lies in edge computing and network slicing supported by the International Telecommunication Union (ITU) and the Organization for Economic Cooperation and Development (OECD) both of which recognize advanced digital infrastructure as a key enabler of future economic growth and innovation.

Global Cloud OSS BSS Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 27.8 Billion |

|

Revenue Forecast in 2035 |

USD 92.6 Billion |

|

Growth Rate |

12.9% |

|

Segments Covered in the Report |

By Component, By Deployment, By Application, By End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Accenture, Amdocs, Cisco Systems, Comarch, CSG International, Ericsson, Huawei Technologies, Netcracker Technology, Nokia, Oracle |

|

Customization |

Available upon request |

Cloud OSS BSS Market Segmentation

By Component

The solutions segment accounted for approximately 67.4% of the market in 2025 supported by increasing investments in cloud native network management, real time billing, service orchestration, and customer experience platforms across telecom operators. The International Telecommunication Union (ITU) continues to emphasize advanced digital infrastructure and intelligent network management as essential for supporting next generation connectivity and expanding broadband services.

The services segment is expected to register the fastest growth advancing at approximately 14.2% CAGR through 2035 driven by growing demand for consulting, system integration, migration and managed support services. Telecom operators are increasingly relying on external expertise to modernize legacy environments and deploy cloud based operational platforms with minimal service disruption.

By Deployment

The public cloud segment held nearly 58.1% market share in 2025 supported by scalable computing resources, flexible subscription models and lower infrastructure ownership costs. Telecom operators are increasingly adopting public cloud environments to accelerate service launches, optimize resource utilization and improve operational agility. The U.S. Federal Communications Commission (FCC) continues to support broadband expansion and advanced communications infrastructure, encouraging service providers to invest in cloud enabled operational ecosystems capable of supporting growing digital traffic.

The hybrid cloud segment is projected to witness the fastest expansion recording an estimated 13.8% CAGR during the forecast period as operators balance security, regulatory compliance and operational flexibility. Growing emphasis on resilient communications infrastructure and secure data management, reinforced by recommendations from the European Union Agency for Cybersecurity (ENISA) continues to strengthen adoption across both developed and emerging telecom markets.

By Application

The customer management and billing segment contributed approximately 38.6% of total market revenue in 2025 supported by increasing demand for real time billing, digital customer engagement, subscription management and personalized service offerings. Telecom operators continue to modernize customer facing systems to improve retention, enhance revenue visibility and support diversified digital services. The ITU continues to promote digital inclusion and advanced communications services, reinforcing investments in customer centric operational platforms.

The service assurance segment is anticipated to register one of the strongest growth rates expanding at approximately 13.6% CAGR through 2035. Increasing network complexity associated with standalone 5G, edge computing and virtualized network functions is driving demand for predictive monitoring, automated fault detection, and AI enabled performance management.

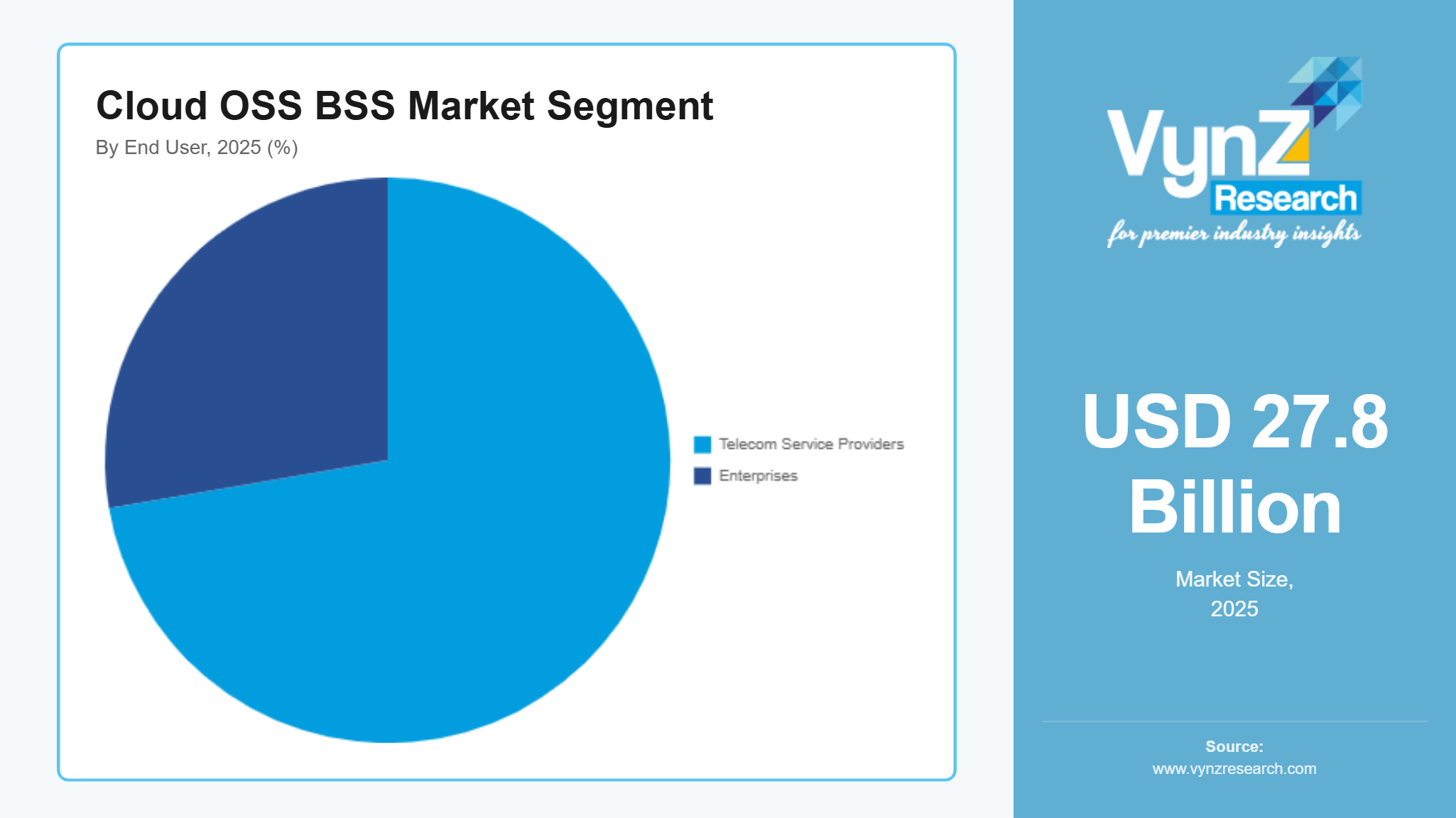

By End User

The telecom service providers segment accounted for nearly 72.3% of market revenue in 2025 due to continuous investments in network modernization, digital service monetization and cloud based operational transformation. The Federal Communications Commission (FCC) and the European Commission continue to promote next generation broadband deployment, supporting long term investments across the telecommunications ecosystem.

The enterprise segment is expected to record the fastest growth progressing at approximately 14.5% CAGR over the forecast period. Enterprises across manufacturing, financial services, healthcare and information technology are increasingly adopting cloud based operational support platforms to improve connectivity management, automate digital workflows, and enhance service delivery.

Regional Insights

North America

North America accounted for approximately 37% of the market in 2025 driven by large scale 5G deployment, rapid cloud transformation and strong investments by leading telecom operators across the United States and Canada. Demand from major technology hubs continues to accelerate adoption of cloud native OSS BSS platforms for network automation and digital customer management. The U.S. Federal Communications Commission (FCC) continues to support broadband expansion and advanced communications infrastructure, strengthening long term investment across cloud enabled telecom ecosystems.

Europe

Europe represented approximately 22% of the market in 2025 supported by expanding digital transformation initiatives, increasing cloud adoption and modernization of communication networks across major economies. The European Commission continues to advance its Digital Decade Program promoting secure digital infrastructure and next generation connectivity across member states, supporting sustained demand for cloud OSS BSS solutions.

Asia Pacific

Asia Pacific accounted for nearly 19% of the market in 2025 driven by expanding mobile subscriber bases, accelerating 5G rollouts and growing investments in cloud infrastructure across China, India, Japan, and South Korea. Rapid digitalization, increasing telecom network capacity and growing adoption of cloud-based business support platforms continue to create long term opportunities.

Rest of the World

The Rest of the World accounted for the remaining 22% of the market in 2025 comprising Latin America, the Middle East and Africa. Market expansion across these regions is supported by ongoing telecom modernization, increasing broadband penetration and growing investments in cloud enabled communications infrastructure. Government backed digital transformation programs and expanding mobile connectivity initiatives continue to encourage telecom operators to adopt advanced OSS BSS platforms creating sustained growth opportunities throughout the forecast period.

Competitive Landscape / Company Insights

The market is highly competitive with global and regional companies focusing on cloud native platform development, AI driven network automation, strategic partnerships and geographic expansion to strengthen their market positions. Vendors are increasing investments in research and development, cybersecurity capabilities and scalable digital service platforms to address evolving telecom requirements. The International Telecommunication Union (ITU) continues to support global digital connectivity initiatives while the European Commission promotes secure digital infrastructure encouraging continuous innovation and investment across the cloud OSS BSS ecosystem.

Mini Profiles

Accenture focuses on cloud transformation, OSS BSS integration, and digital consulting, supported by extensive global delivery capabilities, strategic telecom partnerships, and strong expertise in enterprise modernization and managed services.

Cisco Systems operates in enterprise and telecom infrastructure segments, emphasizing cloud networking, software defined solutions, cybersecurity, and automated network management to improve operational performance and service reliability.

Comarch leverages advanced OSS BSS platforms, long term telecom partnerships, and continuous product innovation to expand its market presence, delivering integrated billing, customer management, and network management solutions.

Ericsson specializes in cloud native OSS BSS platforms, 5G network management, and service orchestration, supported by a strong global customer base and significant investments in telecommunications research and development.

Huawei Technologies provides integrated cloud OSS BSS solutions, AI enabled network automation, and intelligent operations platforms, supported by extensive international deployment experience and comprehensive digital infrastructure capabilities.

Key Players

- Accenture

- Amdocs

- Cisco Systems

- Comarch

- CSG International

- Ericsson

- Huawei Technologies

- Netcracker Technology

- Nokia

- Oracle

Recent Developments

In March 2025, Amdocs announced a multiyear agreement with Vodafone to modernize its cloud native OSS BSS environment using AI driven orchestration and microservices. The collaboration is intended to accelerate digital service delivery and improve operational efficiency for next generation telecom networks.

In June 2025, Ericsson introduced its evolved OSS BSS portfolio featuring AI enabled charging, billing, service orchestration, and Telco DataOps capabilities. The expanded portfolio is designed to support autonomous network transformation and cloud native operations for communication service providers.

In July 2025, Oracle partnered with Verizon to deploy a cloud native converged charging and policy platform on Oracle Cloud Infrastructure. The initiative supports 5G standalone network slicing monetization and strengthens real time telecom service management capabilities.

In March 2025, Nokia announced a strategic collaboration with Capgemini to deliver cloud native OSS BSS modernization and network automation solutions. The partnership focuses on accelerating digital transformation and improving operational agility for telecom operators.

In November 2025, Netcracker Technology was recognized as a Leader in the IDC MarketScape 2025 Vendor Assessment for Worldwide Customer Experience Platforms in the telecommunications sector. The recognition highlights the company's continued innovation in cloud native OSS BSS and customer experience management solutions.

Global Cloud OSS BSS Market Coverage

Component Insight and Forecast 2026 - 2035

- Solutions

- Services

Deployment Insight and Forecast 2026 - 2035

- Public Cloud

- Private Cloud

- Hybrid Cloud

Application Insight and Forecast 2026 - 2035

- Customer Management

- Revenue Management

- Service Fulfillment

- Service Assurance

- Network Management

End User Insight and Forecast 2026 - 2035

- Telecom Service Providers

- Enterprises

Global Cloud OSS BSS Market by Region

- North America

- By Component

- By Deployment

- By Application

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Component

- By Deployment

- By Application

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Component

- By Deployment

- By Application

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Component

- By Deployment

- By Application

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Cloud OSS BSS Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Component

1.2.2. By

Deployment

1.2.3. By

Application

1.2.4. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Component

5.1.1. Solutions

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Services

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.2. By Deployment

5.2.1. Public Cloud

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Private Cloud

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Hybrid Cloud

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By Application

5.3.1. Customer Management

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Revenue Management

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Service Fulfillment

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Service Assurance

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Network Management

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.4. By End User

5.4.1. Telecom Service Providers

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Enterprises

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Component

6.2. By

Deployment

6.3. By

Application

6.4. By

End User

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Component

7.2. By

Deployment

7.3. By

Application

7.4. By

End User

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Component

8.2. By

Deployment

8.3. By

Application

8.4. By

End User

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Component

9.2. By

Deployment

9.3. By

Application

9.4. By

End User

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Accenture

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Amdocs

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Cisco Systems

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Comarch

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

CSG International

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Ericsson

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Huawei Technologies

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Netcracker Technology

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Nokia

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Oracle

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Cloud OSS BSS Market