Deepfake AI Market Size & Share Growth Forecast Report (2026-2035)

Industry Insight by Component (Software, Services), by Type (Image Deepfake, Video Deepfake, Voice Deepfake), by Technology (Generative Adversarial Networks, Autoencoders, Transformer Models, Recurrent Neural Networks, Natural Language Processing, Diffusion Models, Convolutional Neural Networks), by End User (Media and Entertainment, BFSI, Government and Defense, Healthcare and Life Sciences, Retail and E Commerce, IT and Telecommunications, Legal, Education)

| Status : Published | Published On : May, 2026 | Report Code : VRICT5235 | Industry : ICT & Media | Available Format :

|

Page : 143 |

Deepfake AI Market Overview

The worldwide deepfake AI market, which is said to be worth around USD 1.08 billion in 2025 and expected to climb again to nearly USD 1.58 billion by 2026, is also projected to hit roughly USD 34.02 billion come 2035. It’s expanding fast, with a CAGR of about 41.2% across the period from 2026 to 2035.

The momentum is mostly pushed by quick improvements in generative AI systems and the stronger adoption of synthetic media solutions. There is this steady rise in demand for AI-generated digital content across media, entertainment, advertising and enterprise communication. Added momentum comes from investments in AI governance and cybersecurity monitoring and digital content authenticity frameworks. These efforts help the market grow across North America, Europe, and Asia Pacific. There are also government supported initiatives that encourage responsible AI rollouts, and misinformation curbing and enterprises are spending more on AI infrastructure and detection technologies, promoting market growth.

Deepfake AI Market Dynamics

Market Trends

The industry is seeing some notable shifts in synthetic media creation, AI based voice cloning, and real-time video manipulation tech. One big trend is the rising adoption of AI generated personalized content due to the demand for automation, content scale, and digital engagement. Generative AI tool integration across media, entertainment, and marketing platforms is speeding up commercial buy-in. Another trend is the ongoing rollout of deepfake detection and authentication solutions as there is a stricter regulation on misinformation control and responsible AI use. Government backed digital security programs and international AI governance frameworks are pushing organizations to put more attention on content checks, watermarking technologies and advanced cybersecurity offerings.

Growth Drivers

Growth in the market is due to fast developments in generative artificial intelligence and machine learning. These improvements keep feeding adoption across media production, enterprise communication and digital advertising uses. Growing investment in cloud computing infrastructure, AI research programs and digital transformation efforts also promotes market expansion. There is also rising desire for personalized virtual experiences and AI created content boosting adoption. When enterprises focus on automation, better customer engagement, and scalable output, synthetic media solutions keep looking attractive. Government supported investments in AI innovation and digital infrastructure are another factor for long term market growth.

Market Restraints / Challenges

Even with all the positive outlook, the market still has some obstacles that could slow expansion. Regulatory uncertainty, cybersecurity threats and the ongoing worry around misinformation are already affecting adoption, especially in sensitive areas like government, finance, and public communication. Protocols on ethical AI deployment is increasing compliance obligations for technology providers. Dependence on high performance computing infrastructure and the need for advanced AI expertise makes operations harder for developers and enterprises. Costs rise, content authentication demands get heavy and legal frameworks keep shifting affecting scalability and delaying deployments.

Market Opportunities

There are opportunities in AI based content authentication and synthetic media security, mainly because digital misinformation and identity fraud concerns are increasing. Businesses that can deliver scalable verification capabilities, watermarking systems, and enterprise grade AI monitoring platforms are positioned well to capture new demand from both corporate groups and public sector organizations. Another strong opportunity is virtual content creation and immersive digital communication. More investment in AI enabled media platforms and interactive experiences create long-term commercial potential, improvements in automation, cloud-based AI tools and multilingual synthetic media generation strengthen customer interaction which improves operating efficiency.

Global Deepfake AI Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 1.08 Billion |

|

Revenue Forecast in 2035 |

USD 34.02 Billion |

|

Growth Rate |

41.2% |

|

Segments Covered in the Report |

Component, Type, Technology, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Amazon Web Services, Attestiv Inc., BioID, D-ID, Datambit, Google LLC, Intel Corporation, Microsoft, Pindrop, Synthesia |

|

Customization |

Available upon request |

Deepfake AI Market Segmentation

By Component

In 2025 software accounted for the biggest share of the market, about 68% of total revenue because a lot of teams keep rolling out synthetic media generation platforms, facial mapping tools, and AI driven content creation systems across media, advertising and enterprise comms. More money is going into generative AI infrastructure and cloud-based machine learning ecosystems, pushing software adoption forward internationally. Also, government supported digital transformation programs and AI innovation initiatives across North America and Asia Pacific are helping this segment stay steady and grow.

Services are expected to grow the quickest during the forecast window, with an estimated CAGR of 43.6% from 2026 to 2035. Enterprise demand for AI integration, cybersecurity consulting, and deepfake detection services is basically speeding up expansion across both commercial and public sector orgs. Regulators are paying more attention to synthetic media authentication and responsible AI deployment pushing companies to choose managed service models and long-term platform support solutions.

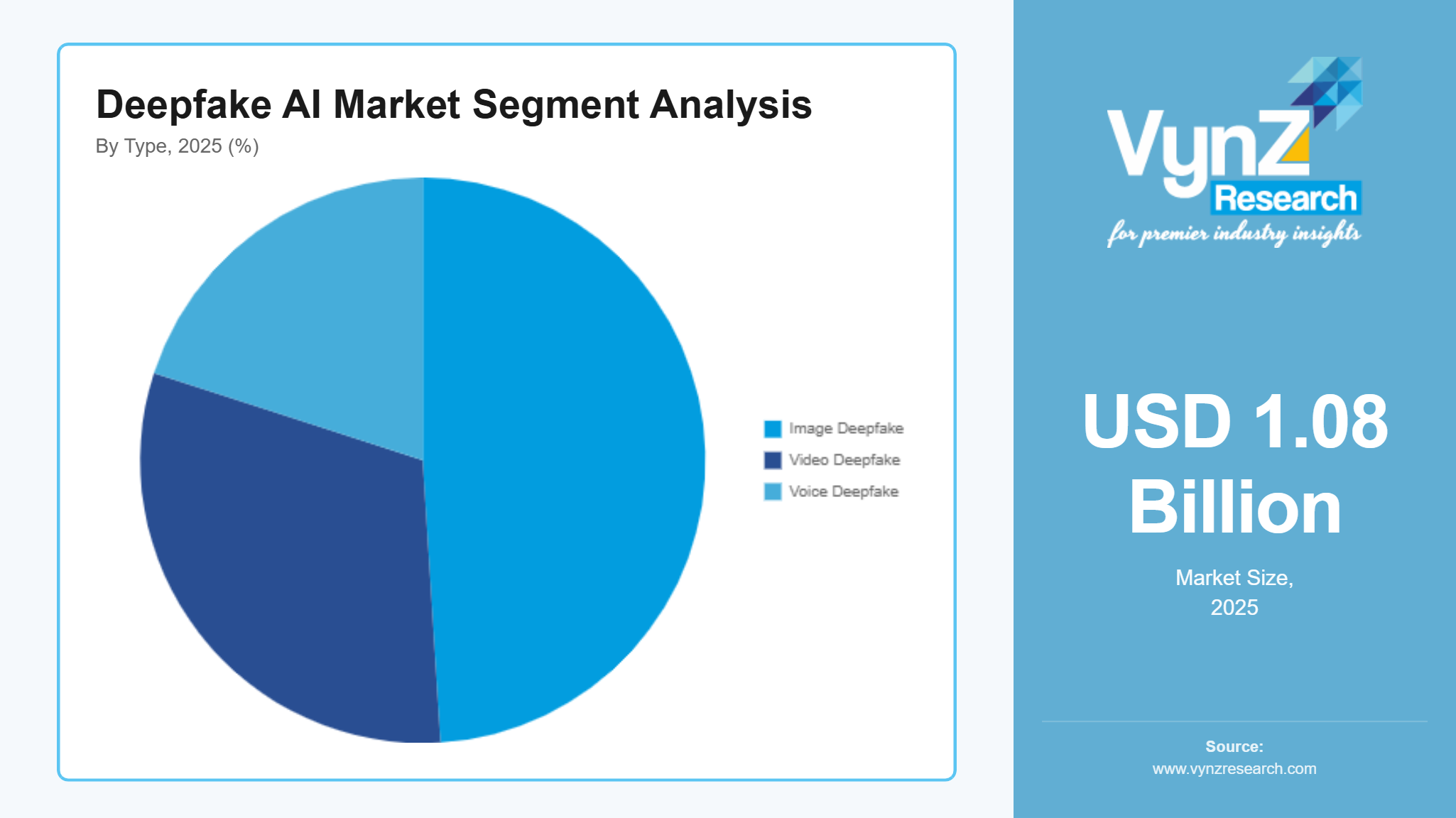

By Type

In 2025, video deepfake solutions took the largest market share, contributing nearly 49% of total segment revenue because they’re being used more in entertainment production, digital marketing campaigns, gaming content, and virtual influencer kinds of use cases. The quick expansion of short form video platforms along with AI powered editing tools has also made adoption easier across commercial content ecosystems. Discussions around misinformation monitoring and digital identity verification are pushing deployment including advanced video analysis and synthetic content management systems.

Voice deepfake technologies are anticipated to grow faster than the rest, with an estimated CAGR of 44.1% during 2026 to 2035 as multilingual voice synthesis is becoming more popular along with virtual assistants, automated customer engagement platforms and AI powered dubbing applications. Expanding investments in conversational AI and speech generation tech across enterprise communication and customer service industries are sustaining long term demand.

By Technology

Generative adversarial networks accounted for the largest share of the market in 2025, representing about 41% of segment revenue, supported by stronger image synthesis abilities, high quality facial reconstruction performance and broad use in synthetic media development platforms. Ongoing investments in advanced neural network architectures and AI training infrastructure are continuing to back that dominance.

Diffusion models are projected to grow at the fastest pace in the forecast period, with an estimated CAGR of 45.2% from 2026 to 2035. Demand is rising for more lifelike image generation, better rendering precision, and scalable content creation tools, so commercial adoption is accelerating.

By End User

Media and entertainment accounted for the largest share of the market in 2025, contributing approximately 36% of total revenue due to strong adoption of AI generated visual effects, virtual influencers, synthetic voice production, and personalized digital content. Streaming platforms, advertising agencies, gaming studios, and digital production companies are increasingly deploying deepfake technologies to improve production efficiency and audience engagement. Government backed initiatives that support digital innovation and creative technology ecosystems are also helping the industry expand.

Government and defense along with BFSI are expected to register the fastest growth during the forecast period, with estimated CAGR levels around 43.8% and 42.9% respectively from 2026 to 2035. Rising worries about misinformation, cyber fraud, biometric spoofing and digital identity manipulation are leading to more investment in deepfake detection and AI security solutions. Public sector cybersecurity programs and regulatory frameworks that promote responsible AI governance are further strengthening adoption across high security operational environments.

Regional Insights

North America

North America held roughly 34% of the AI market in 2025 because of their advanced artificial intelligence infrastructure, solid enterprise adoption and more funding for synthetic media technologies. Big demand from key technology hubs like California, New York and Toronto keeps feeding regional growth across media, cybersecurity, and cloud computing. Regulatory moves and AI governance frameworks are nudging deployment of content authentication and deepfake detection solutions.

Europe

In Europe, the market share sat around 25% in 2025. The regional demand comes from more attention to artificial intelligence transparency, data security and misinformation control. Germany, the UK and France in particular are seeing faster adoption of AI generated media tools across marketing, entertainment and workplace communication uses.

Asia Pacific

Asia Pacific represented about 22% of the market in 2025. This is fueled by fast digitalization, higher AI spending and the continued expansion of content creation industries in China, India, Japan, and South Korea. Tech hotspots such as Beijing, Tokyo, Seoul, and Bengaluru keep showing strong uptake of synthetic media platforms and AI driven communication solutions.

Rest of the World

The Rest of the World, including Latin America, the Middle East and Africa, made up nearly 19% in 2025. Growth here is supported by greater internet penetration, rising digital media consumption and steady investments in AI infrastructure and cybersecurity capabilities, which in turn helps create longer term chances for market participants.

Competitive Landscape / Company Insights

The market is highly competitive with the presence of global technology providers, AI platform developers, and cybersecurity firms focusing on innovation, strategic collaborations, and expansion of synthetic media capabilities. Companies are increasingly investing in generative AI research, cloud-based machine learning infrastructure, and deepfake detection technologies to strengthen their market position. Regulatory frameworks and responsible AI initiatives introduced by government backed digital authorities are further encouraging enterprises to enhance content authentication, cybersecurity compliance and ethical AI deployment strategies across commercial applications.

Mini Profiles

Amazon Web Services focuses on cloud based artificial intelligence infrastructure and generative AI solutions, supported by strong global distribution capabilities, scalable computing networks, and extensive enterprise partnerships across digital transformation industries.

BioID operates in niche biometric authentication and identity verification segments, emphasizing facial recognition accuracy, cybersecurity compliance, and AI driven fraud prevention solutions for enterprise and public sector applications.

D-ID focuses on AI generated video creation and synthetic media solutions, supported by strong digital capabilities, enterprise partnerships, and increasing adoption across marketing, communication, and content production applications.

Datambit focuses on AI powered media analytics and synthetic content technologies, supported by growing digital reach, enterprise integration capabilities, and increasing adoption across communication and cybersecurity related applications.

Google LLC operates in premium artificial intelligence and cloud technology segments, emphasizing large scale AI innovation, advanced generative models, and integrated digital ecosystems supporting enterprise and consumer applications globally.

Key Players

- Amazon Web Services

- Attestiv

- Inc.

- BioID

- D-ID

- Datambit

- Google LLC

- Intel Corporation

- Microsoft

- Pindrop

- Synthesia

Recent Developments

In February 2025, Attestiv Inc. expanded its AI powered media authentication capabilities for enterprise document and digital identity verification applications. The development strengthened the company’s position in synthetic content validation and fraud prevention solutions across regulated industries.

In April 2025, Intel Corporation introduced enhanced AI acceleration capabilities within its latest enterprise computing platforms to support real time deepfake detection and generative AI workloads. The initiative focused on improving synthetic media analysis and enterprise cybersecurity performance.

In June 2025, Microsoft expanded responsible AI and cybersecurity initiatives through advanced synthetic media monitoring and AI governance solutions. The company increased investments in enterprise AI protection tools supporting secure deployment of generative artificial intelligence systems.

In July 2025, Pindrop strengthened its deepfake detection capabilities following rising cases of AI generated identity fraud and synthetic voice attacks. The company expanded deployment of real time audio and video verification technologies for enterprise communication security.

In September 2025, Synthesia launched advanced full body AI avatar technologies designed to improve realism, multilingual communication, and enterprise video engagement. The innovation expanded the company’s synthetic media capabilities for training, marketing, and digital communication applications globally.

Global Deepfake AI Market Coverage

Component Insight and Forecast 2026 - 2035

- Software

- Services

Type Insight and Forecast 2026 - 2035

- Image Deepfake

- Video Deepfake

- Voice Deepfake

Technology Insight and Forecast 2026 - 2035

- Generative Adversarial Networks

- Autoencoders

- Transformer Models

- Recurrent Neural Networks

- Natural Language Processing

- Diffusion Models

- Convolutional Neural Networks

End User Insight and Forecast 2026 - 2035

- Media and Entertainment

- BFSI

- Government and Defense

- Healthcare and Life Sciences

- Retail and E Commerce

- IT and Telecommunications

- Legal

- Education

Global Deepfake AI Market by Region

- North America

- By Component

- By Type

- By Technology

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Component

- By Type

- By Technology

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Component

- By Type

- By Technology

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Component

- By Type

- By Technology

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Deepfake AI Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Component

1.2.2. By

Type

1.2.3. By

Technology

1.2.4. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Component

5.1.1. Software

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Services

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.2. By Type

5.2.1. Image Deepfake

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Video Deepfake

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Voice Deepfake

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By Technology

5.3.1. Generative Adversarial Networks

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Autoencoders

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Transformer Models

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Recurrent Neural Networks

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Natural Language Processing

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.3.6. Diffusion Models

5.3.6.1. Market Definition

5.3.6.2. Market Estimation and Forecast to 2035

5.3.7. Convolutional Neural Networks

5.3.7.1. Market Definition

5.3.7.2. Market Estimation and Forecast to 2035

5.4. By End User

5.4.1. Media and Entertainment

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. BFSI

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Government and Defense

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Healthcare and Life Sciences

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Retail and E Commerce

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

5.4.6. IT and Telecommunications

5.4.6.1. Market Definition

5.4.6.2. Market Estimation and Forecast to 2035

5.4.7. Legal

5.4.7.1. Market Definition

5.4.7.2. Market Estimation and Forecast to 2035

5.4.8. Education

5.4.8.1. Market Definition

5.4.8.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Component

6.2. By

Type

6.3. By

Technology

6.4. By

End User

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Component

7.2. By

Type

7.3. By

Technology

7.4. By

End User

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Component

8.2. By

Type

8.3. By

Technology

8.4. By

End User

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Component

9.2. By

Type

9.3. By

Technology

9.4. By

End User

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Amazon Web Services

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Attestiv Inc.

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

BioID

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

D-ID

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Datambit

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Google LLC

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Intel Corporation

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Microsoft

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Pindrop

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Synthesia

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Deepfake AI Market