AI Cybersecurity Copilot Market Size & Share Growth Forecast Report (2026-2035)

Industry Insight by Solution Type (Threat Detection Copilots, Incident Response Copilots, Threat Intelligence Copilots, Security Orchestration Copilots), by Deployment Mode (Cloud Based, Hybrid, On Premise), by Organization Size (Large Enterprises, Small and Medium Enterprises), by End User (Banking and Financial Services, Government and Defense, IT and Telecom, Healthcare, Retail and E-commerce)

| Status : Published | Published On : May, 2026 | Report Code : VRICT5236 | Industry : ICT & Media | Available Format :

|

Page : 134 |

AI Cybersecurity Copilot Market Overview

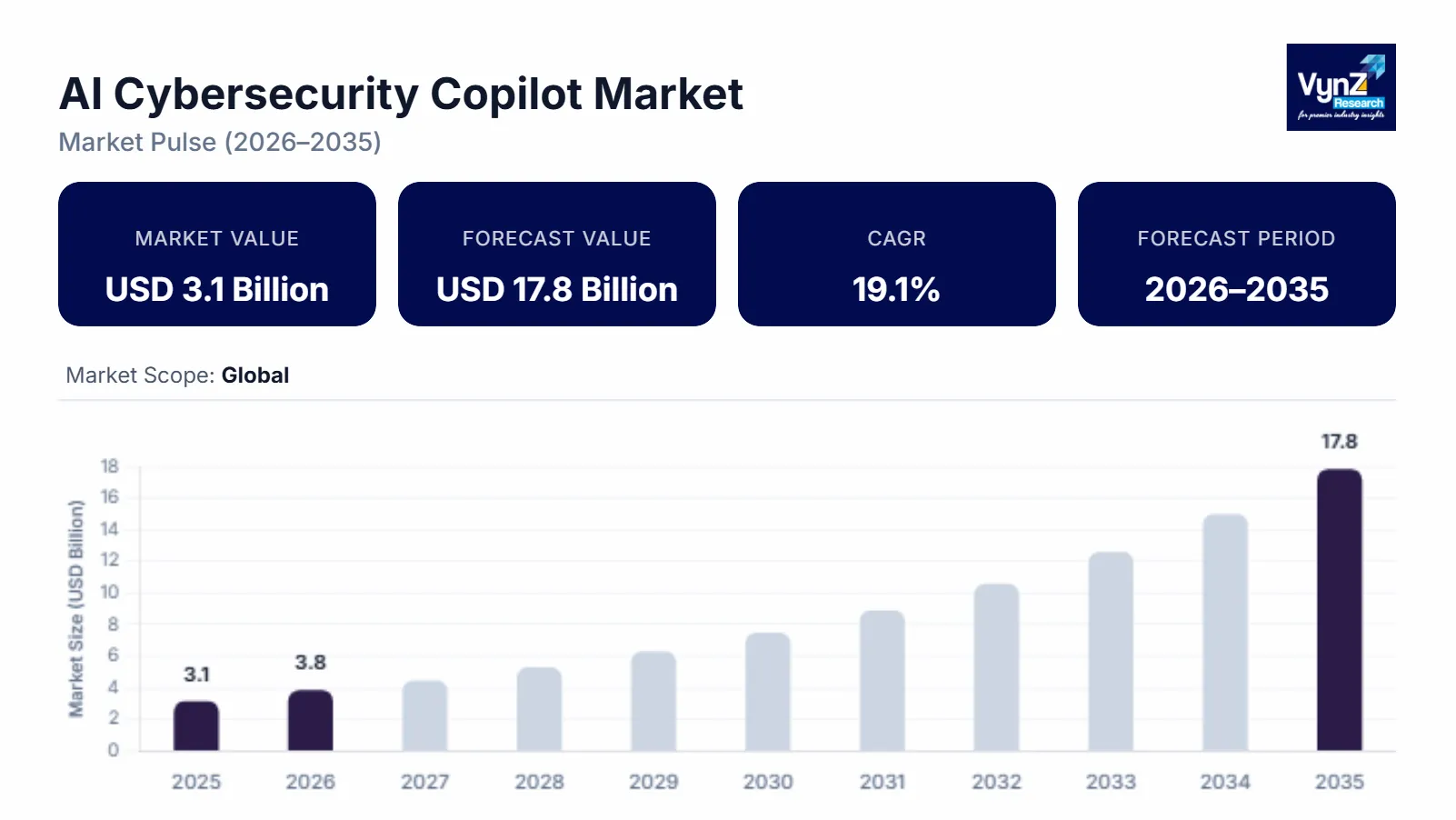

The AI Cybersecurity Copilot market which was valued at approximately USD 3.1 billion in 2025 and is estimated to rise further up to almost USD 3.8 billion by 2026, is projected to reach around USD 17.8 billion by 2035, expanding at a CAGR of about 19.1% during the forecast period from 2026 to 2035.

The market grows due to increasing cyberattack and its complexity, rising cloud adoption by enterprises and a bigger need for real-time security automation and because more teams are adopting AI powered threat detection and response copilots. The demand for autonomous security operations across enterprises is rising and investments are made in national cybersecurity modernization programs. These are helping the market expand across major regions like United States, United Kingdom, and India. Based on guidance from the Cybersecurity and Infrastructure Security Agency and the European Union Agency for Cybersecurity, organizations are pushing ahead with AI assisted cybersecurity frameworks to improve threat response and overall resilience.

AI Cybersecurity Copilot Market Dynamics

Market Trends

The industry is showing clear shifts in security operations and enterprise threat management procurement patterns. A big trend is the rising adoption of autonomous SOC copilots. It signals that buyers now ant faster threat detection, more operational efficiency and less human hand-holding in cybersecurity tasks. Another trend is the rising threat intelligence platforms due to faster digital penetration and refined cyber threats. As demanded by the Cybersecurity and Infrastructure Security Agency and the European Union Agency for Cybersecurity, organizations are increasingly taking on AI assisted security frameworks. As a result, vendors are being pushed to deliver unified security platforms and automated incident response systems.

Growth Drivers

The market is broadly supported by a higher frequency of cyberattacks and also by the growing need for real time threat detection across enterprise IT setups. At the same time, investments in cloud infrastructure and broader digital enterprise transformation are helping the market expand faster across financial services, healthcare, and government. Adoption of AI driven security automation is a key factor for deployment momentum. Enterprises are looking hard at cost efficiency, data protection and compliance readiness that increases the demand for AI based cybersecurity copilots through the forecast period. Government backed cybersecurity modernization programs are giving adoption extra momentum across regions.

Market Restraints / Challenges

Even with strong growth, the market still hits some friction points, especially around data privacy regulations and model reliability risks. Those hurdles can make deployment harder in highly regulated industries. In particular, enterprises in sensitive areas like finance and defense feel the pressure more. There is also a practical problem around needing high quality threat data and having enough skilled cybersecurity professionals. Vendors run into operational constraints and when integration touches legacy security infrastructure, complexity grows. This causes cost pressures and longer deployment cycles, especially during big scale digital transformation initiatives.

Market Opportunities

Opportunity lies around autonomous security operations centers and real time threat intelligence automation driven by rising enterprise cybersecurity complexity and the expansion of attack surfaces. Providers that can offer scalable, AI driven, and cost-efficient security copilots are in a good position to win business from large enterprises and government agencies. Another notable chance is within cloud native cybersecurity platforms. With rising investments in digital infrastructure, the demand for advanced AI security orchestration tools is strengthening and as machine learning based threat prediction keeps improving along with automated incident response systems, operational efficiency should get a boost, which may also improve adoption globally.

Global AI Cybersecurity Copilot Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 3.1 Billion |

|

Revenue Forecast in 2035 |

USD 17.8 Billion |

|

Growth Rate |

19.1% |

|

Segments Covered in the Report |

Solution Type, Deployment Mode, Organization Size, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

CrowdStrike, Darktrace, Fortinet, Google Cloud, IBM, Microsoft, Palo Alto Networks, SentinelOne, Splunk, Zscaler |

|

Customization |

Available upon request |

AI Cybersecurity Copilot Market Segmentation

By Solution Type

In 2025, threat detection copilots were basically the biggest chunk of the market, holding around 41% of overall revenue. This big share is due to the rising frequency of advanced cyberattacks and how much organizations depend on real time monitoring systems and also the broad rollout of these tools across security operations centers, especially in large enterprises. AI driven threat detection is combined into enterprise security frameworks and that momentum is pushed by modernization guidance from agencies such as the Cybersecurity and Infrastructure Security Agency.

Incident response copilots are expected to grow the quickest, with a projected CAGR of 20.8% from 2026 to 2035 because automated remediation workflows are in demand, AI assisted forensic analysis is becoming more practical and teams want faster containment for complex threats. The ongoing shortage of experienced cybersecurity professionals and the fact that attack surfaces keep getting bigger pushes adoption. Government supported cybersecurity resilience programs, along with enterprise goals around lowering mean time to respond are promoting adoption through global security ecosystems.

By Deployment Mode

Cloud based deployment took the lead in 2025, at roughly 57% of the market due to fast enterprise cloud migration, the scalability upsides and the ability to centralize threat intelligence processing. Companies are increasingly using cloud native security platforms to handle the growing cyber risk across IT environments. When AI cybersecurity copilots plug into those cloud security ecosystems, detection accuracy and operational efficiency both tend to improve.

Hybrid deployment should see the fastest growth, at around a 21.3% CAGR over 2026 to 2035 due to stricter regulatory compliance needs, data sovereignty worries, and the push to connect older infrastructure with newer AI security systems. Banking, defense and critical infrastructure organizations are choosing hybrid models to balance security control with scalability.

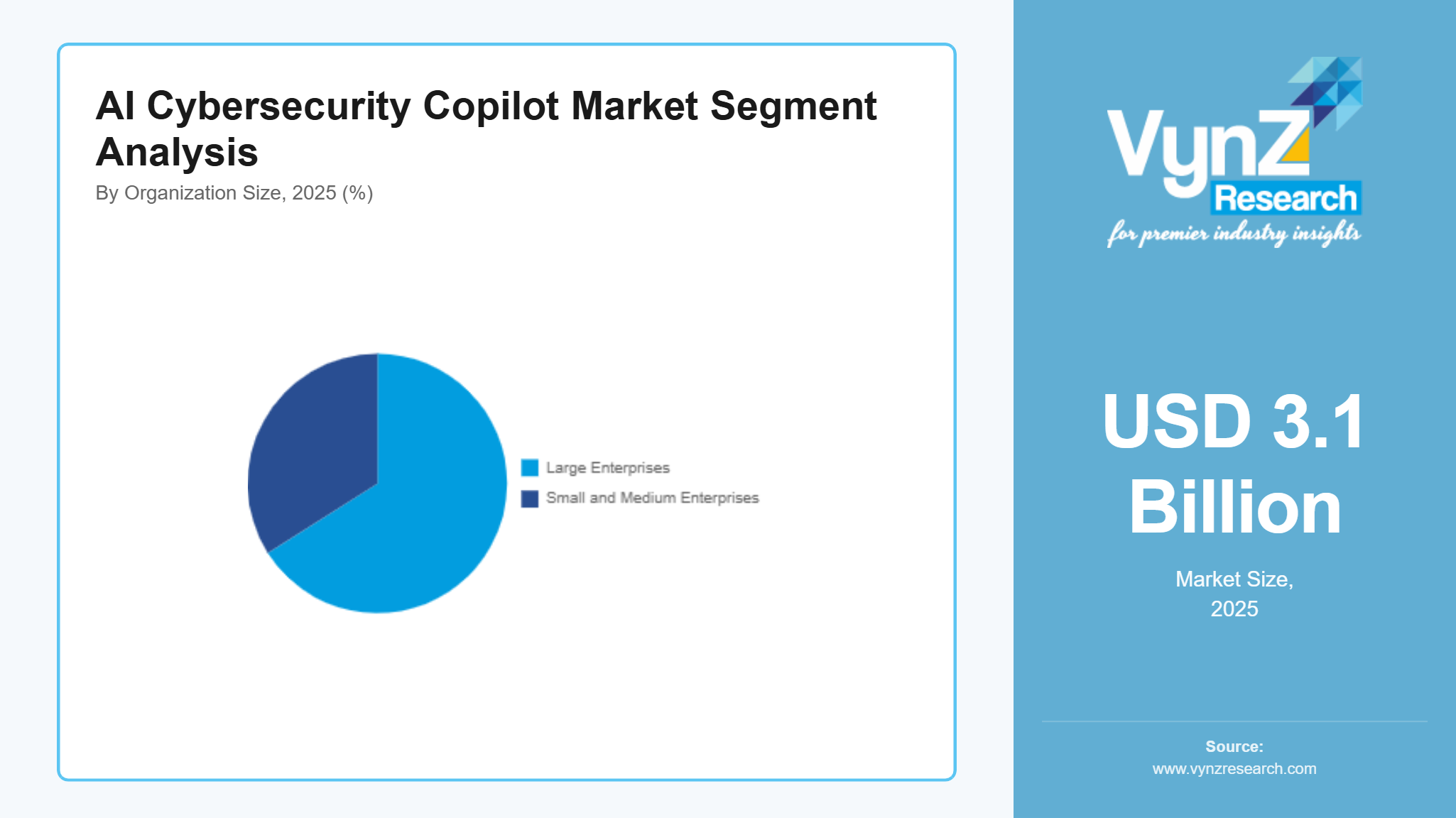

By Organization Size

Large enterprises held the largest portion, about 66% in 2025, largely because cybersecurity budgets are higher, IT ecosystems are more intricate and advanced persistent threats are more frequent. They also tend to be early adopters, using AI cybersecurity copilots for automated SOC operations, threat intelligence analysis, and risk visibility across the organization.

Small and medium enterprises are forecast to post the fastest CAGR, roughly 22.1% from 2026 to 2035, influenced by rising awareness of cyber risk exposure, easier access to affordable cloud-based cybersecurity copilots and the expansion of managed security service offerings. Many SMEs are adopting AI driven security solutions because in house expertise is limited and to strengthen defenses against ransomware campaigns and phishing attempts that keep evolving.

By End User

Banking and financial services accounted for the largest share, around 37% in 2025 because cyberattacks hit more often, compliance expectations are strict and digital banking infrastructure keeps deepening. Financial firms are investing heavily in AI driven cybersecurity copilots to support better fraud detection, transaction monitoring and real time threat response. Strong oversight across financial sectors continues to reinforce adoption in global markets.

Government and defense are expected to be the fastest growing segment, with a projected CAGR of about 21.6% during 2026 to 2035 due to increasing geopolitical cyber threats, a sharper focus on safeguarding critical infrastructure and large-scale national cybersecurity modernization initiatives. Government organizations are rolling out AI based threat intelligence systems to strengthen overall cyber resilience and to improve real time incident response. Policy structures and strategic cybersecurity spending are also speeding up adoption across defense networks worldwide.

Regional Insights

North America

North America accounted for approximately 42% of the market in 2025, driven by strong enterprise cybersecurity maturity, high cloud adoption, and advanced SOC automation across financial services, healthcare and government sectors. Strong presence of large technology providers and early adoption of AI driven security orchestration systems continues to support regional dominance. Major demand hubs across the United States and Canada are investing heavily in real time threat intelligence and automated incident response platforms. Government backed cybersecurity modernization initiatives led by agencies such as the Cybersecurity and Infrastructure Security Agency are further strengthening deployment of AI based security copilots across critical infrastructure and enterprise networks.

Asia Pacific

The Asia Pacific region held approximately 27% share in 2025 and is witnessing steady growth due to rapid digital transformation, expanding cloud infrastructure, and increasing cyber threat exposure across enterprises. Countries such as China, India and Japan are experiencing rising demand for AI driven cybersecurity solutions across banking, telecom, and government sectors. Increasing investments in national cybersecurity frameworks and digital economy programs are accelerating adoption of automated threat detection and response systems. Government backed digital infrastructure initiatives and growing enterprise awareness of cyber risk are further supporting market expansion across the region.

Europe

Europe accounted for approximately 19% of the market in 2025, supported by strict data protection regulations, growing cybersecurity compliance requirements and increasing adoption of AI driven security platforms across enterprises. Countries such as Germany, France and the United Kingdom are investing in advanced threat intelligence systems and SOC automation tools to enhance digital resilience. Regulatory frameworks and cybersecurity directives supported by the European Union Agency for Cybersecurity are encouraging standardized adoption of AI based cybersecurity copilots. Rising enterprise focus on data privacy and operational security is further strengthening regional demand.

Rest of the World

The rest of the world accounted for approximately 12% of the market in 2025, driven by gradual digital transformation, increasing cybersecurity awareness and growing adoption of cloud based security solutions across emerging economies in the Middle East, Latin America, and Africa. Rising investment in digital infrastructure and enterprise IT modernization is supporting adoption of AI enabled cybersecurity tools in both public and private sectors. Government led cybersecurity capacity building programs and international digital security collaborations are further contributing to market development.

Competitive Landscape / Company Insights

The market is moderately to highly competitive with the presence of global cybersecurity vendors and AI driven security platform providers focusing on product innovation, threat intelligence automation and enterprise scale deployment strategies. Companies are increasingly investing in AI research and development, advanced analytics capabilities and integrated security orchestration platforms to strengthen their market position. Growing cybersecurity modernization initiatives and evolving compliance frameworks supported by organizations such as the Cybersecurity and Infrastructure Security Agency and European Union Agency for Cybersecurity are further encouraging adoption of standardized AI driven security solutions across global enterprises.

Mini Profiles

CrowdStrike focuses on AI driven endpoint security and threat intelligence solutions, supported by strong cloud native architecture and global enterprise adoption across cybersecurity operations centers and digital infrastructure environments.

Darktrace operates in premium AI cybersecurity segments, emphasizing autonomous threat detection, self-learning AI models, and advanced network defense capabilities for enterprise and critical infrastructure protection systems.

Fortinet leverages integrated security platforms and strategic global partnerships to expand market presence, offering unified cybersecurity solutions across network security, cloud protection, and enterprise firewall systems.

Google Cloud focuses on cloud native cybersecurity and AI powered security analytics, supported by large scale digital infrastructure, global data centers, and strong enterprise cloud ecosystem integration capabilities.

IBM operates in enterprise cybersecurity and AI security intelligence segments, emphasizing hybrid cloud security, advanced threat detection, and strong consulting driven digital transformation capabilities across global industries.

Key Players

- CrowdStrike

- Darktrace

- Fortinet

- Google Cloud

- IBM

- Microsoft

- Palo Alto Networks

- SentinelOne

- Splunk

- Zscaler

Recent Developments

In February 2026, SentinelOne expanded its AI security platform with advanced agentic AI capabilities for real-time threat detection and autonomous response. The upgrade focused on improving AI-driven incident triage and reducing SOC workload across enterprise environments.

In January 2026, CrowdStrike enhanced its Falcon platform with improved AI-powered threat hunting and identity protection features. The update strengthened endpoint visibility and improved response speed against AI-generated cyber threats across global enterprise networks.

In March 2026, Palo Alto Networks upgraded its Cortex XSIAM platform with deeper AI automation for security operations centers. The development improved threat correlation and reduced detection-to-response time across cloud and hybrid environments.

In April 2026, Zscaler strengthened its AI-based zero-trust security architecture with enhanced cloud-native threat intelligence integration. The enhancement focused on securing distributed enterprise networks and improving real-time policy enforcement across remote users.

In March 2026, Fortinet addressed emerging AI-driven attack vectors by upgrading its FortiAI-powered security fabric. The update improved automated threat detection and reinforced firewall resilience against evolving zero-day vulnerabilities.

Global AI Cybersecurity Copilot Market Coverage

Solution Type Insight and Forecast 2026 - 2035

- Threat Detection Copilots

- Incident Response Copilots

- Threat Intelligence Copilots

- Security Orchestration Copilots

Deployment Mode Insight and Forecast 2026 - 2035

- Cloud Based

- Hybrid

- On Premise

Organization Size Insight and Forecast 2026 - 2035

- Large Enterprises

- Small and Medium Enterprises

End User Insight and Forecast 2026 - 2035

- Banking and Financial Services

- Government and Defense

- IT and Telecom

- Healthcare

- Retail and E-commerce

Global AI Cybersecurity Copilot Market by Region

- North America

- By Solution Type

- By Deployment Mode

- By Organization Size

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Solution Type

- By Deployment Mode

- By Organization Size

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Solution Type

- By Deployment Mode

- By Organization Size

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Solution Type

- By Deployment Mode

- By Organization Size

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for AI Cybersecurity Copilot Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Solution Type

1.2.2. By

Deployment Mode

1.2.3. By

Organization Size

1.2.4. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Solution Type

5.1.1. Threat Detection Copilots

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Incident Response Copilots

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Threat Intelligence Copilots

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Security Orchestration Copilots

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.2. By Deployment Mode

5.2.1. Cloud Based

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Hybrid

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. On Premise

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By Organization Size

5.3.1. Large Enterprises

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Small and Medium Enterprises

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By End User

5.4.1. Banking and Financial Services

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Government and Defense

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. IT and Telecom

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Healthcare

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Retail and E-commerce

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Solution Type

6.2. By

Deployment Mode

6.3. By

Organization Size

6.4. By

End User

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Solution Type

7.2. By

Deployment Mode

7.3. By

Organization Size

7.4. By

End User

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Solution Type

8.2. By

Deployment Mode

8.3. By

Organization Size

8.4. By

End User

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Solution Type

9.2. By

Deployment Mode

9.3. By

Organization Size

9.4. By

End User

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

CrowdStrike

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Darktrace

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Fortinet

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Google Cloud

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

IBM

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Microsoft

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Palo Alto Networks

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

SentinelOne

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Splunk

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Zscaler

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

AI Cybersecurity Copilot Market