APAC Commercial Refrigeration Equipment Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Product Type (Transportation Refrigeration Equipment, Refrigerators & Freezers, Beverage Refrigeration, Walk-in Coolers, Ice-making Machinery), by Application (Food Service, Food & Beverage Retail, Food & Beverage Distribution, Food & Beverage Production), by End User (Hotels, Restaurants, and Catering (HoReCa), Supermarkets and Hypermarkets, Convenience Stores, Food Processing Industry)

| Status : Published | Published On : Apr, 2026 | Report Code : VRSME9205 | Industry : Semiconductor & Electronics | Available Format :

|

Page : 132 |

APAC Commercial Refrigeration Equipment Market Overview

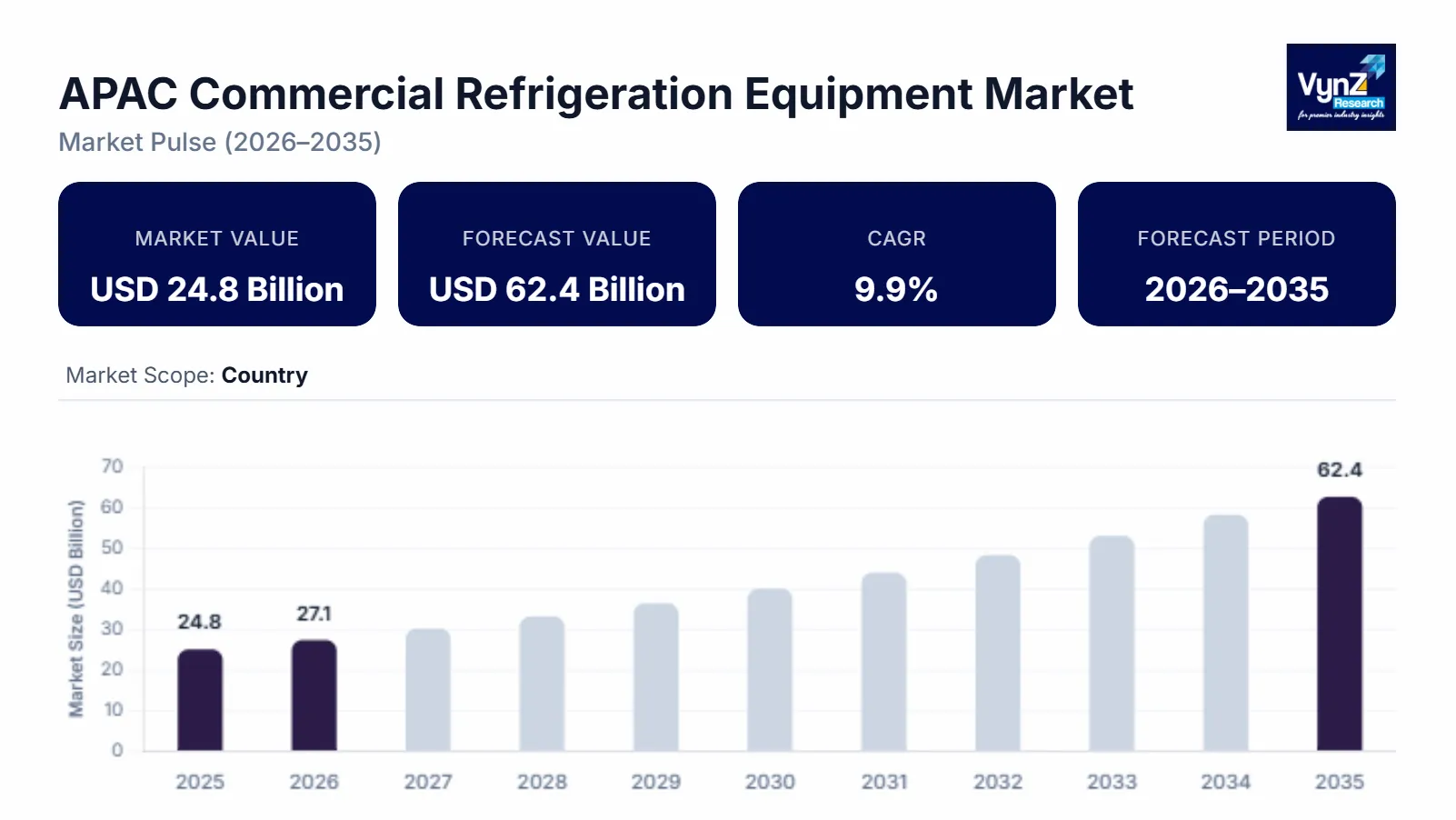

The APAC commercial refrigeration equipment market which was valued at approximately USD 24.8 billion in 2025 and is estimated to rise further up to almost USD 27.1 billion by 2026, is projected to reach around USD 62.4 billion in 2035, expanding at a CAGR of about 9.9% during the forecast period from 2026 to 2035.

The food service sector is expanding rapidly which drives market growth together with increasing urban populations, the need for cold chain systems, the growing demand for energy efficient refrigeration technologies, the rising use of environmentally friendly refrigerants and advanced cooling solutions. The market is expanding across major regions because of increasing processed, packaged food consumption, continuous investments in food safety infrastructure and cold storage development in China, India and Japan.

The region experiences industry growth because government initiatives and regulatory frameworks provide backing for development. Safe food storage practices must be implemented to decrease foodborne diseases according to World Health Organization guidelines which create a demand for dependable refrigeration systems. Sustainable cooling systems and low emission refrigerants need to be adopted according to national food safety authorities and energy efficiency initiatives that operate throughout Asia Pacific. The public sector invests in cold chain logistics which benefits both emerging economies and the implementation of policies that reduce food waste while improving supply chain efficiency to support the growth of commercial refrigeration systems used in retail and hospitality and food processing industries.

APAC Commercial Refrigeration Equipment Market Dynamics

Market Trends

The sector in APAC region is experiencing substantial changes because of new technology adoptions and different equipment purchasing methods. The market trend that drives market development requires businesses to adopt energy efficient systems which produce minimal emissions because customers now prefer environmentally responsible solutions and compliance with sustainability regulations. Commercial facilities should adopt natural refrigerants and modern cooling technologies because regional policy frameworks support climate commitments through their guidance. Businesses now use smart and connected refrigeration systems which have emerged as a new trend because food service and retail operations implement digital and automated systems. The new market developments create product offering changes which drive companies to develop intelligent monitoring and energy optimization systems and complete cold chain solutions, which transform the competitive landscape of the market.

Growth Drivers

The demand for products derives from the increasing needs of food service and retail businesses, which experience rapid growth in urban and developing markets. Market growth accelerates because businesses increase their investments in cold chain systems and food processing plants. The rising importance of food safety and storage requirements drives higher adoption rates in different industries. International health organizations state that temperature-controlled storage systems reduce foodborne hazards, which has led to higher demand in both hospitality and retail sectors. The demand for advanced refrigeration solutions will sustain strong growth during the entire forecast period because enterprises focus on improving operational efficiency while meeting their regulatory obligations.

Market Restraints / Challenges

The market encounters specific obstacles, which restrict its ability to achieve sustainable market growth. Small and medium enterprises face market entry difficulties because of two factors namely high initial investment costs and cost sensitivity issues which particularly affect developing economies. Manufacturers and suppliers confront operational difficulties because regulatory authorities have established complex rules for refrigerant transitions and environmental compliance requirements. The environmental standards which keep changing together with the need for imported parts result in increased expenses and product redesign needs. Economic downturns will cause market demand fluctuations because infrastructure problems in some areas will affect market performance.

Market Opportunities

The market presents substantial opportunities for sustainable refrigeration technologies because regulatory authorities now prioritize emissions reduction and energy efficiency improvements. Companies that provide ecofriendly energy optimized solutions will successfully attract extra customers from food retail businesses and hospitality providers. The development of organized retailing and cold chain logistics creates an important opportunity because new investments in contemporary infrastructure will drive business growth throughout the upcoming years. Government supported initiatives aimed at reducing food wastage and improving supply chain efficiency are further strengthening this outlook. Smart monitoring systems together with automated cooling technology make commercial systems easier to operate while driving higher usage rates in business environments.

APAC Commercial Refrigeration Equipment Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 24.8 Billion |

|

Revenue Forecast in 2035 |

USD 62.4 Billion |

|

Growth Rate |

9.9% |

|

Segments Covered in the Report |

Product Type, Application, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

China, India, Japan, South Korea, Rest of Asia Pacific |

|

Key Companies |

Blue Star Limited, Carrier Global Corporation, Daikin Industries Ltd., Dover Corporation, Electrolux AB, Haier Smart Home Co. Ltd., Hussmann Corporation, Panasonic Corporation, The Middleby Corporation, Whirlpool Corporation |

|

Customization |

Available upon request |

APAC Commercial Refrigeration Equipment Market Segmentation

By Product Type

The refrigerator and freezer market reached its highest point in 2025 when these products generated about 34% of total sales through their widespread use in both retail, food service and storage spaces. The ongoing need for temperature-controlled storage together with constant replacement schedules in areas of high usage enables them to maintain market control. The increasing regulatory pressure which mandates food preservation and safety standards through public health agencies in Asia Pacific, leads to higher commercial adoption rates.

The market for walk-in cooling systems and advanced refrigeration units will experience the most significant growth which will reach a compound annual growth rate of 10.6% between 2026 and 2035. The organized retail sector, large-scale food storage facilities and cold chain logistics investments drive this growth. The global food security initiatives which aim to reduce food waste create demand for high-capacity refrigeration systems in emerging markets.

By Application

The food service segment held the largest share in 2025 because it created approximately 38% of total demand through restaurant, quick service outlet and hospitality infrastructure expansion in urban centers. Chinese consumers increasingly prefer dining out and consuming ready-to-eat food which fuels market expansion. The commercial refrigeration systems of this segment receive ongoing installation through regulatory food hygiene and storage guidelines which protect food safety.

The food and beverage distribution industry will experience its strongest growth period because it will achieve a compound annual growth rate of 10.2% during the entire forecast period. The cold chain networks in operation today expand because government infrastructure programs and logistics modernization initiatives support their development. The growing demand for temperature-controlled transportation and the increasing cross-border food trade will expand the market within regional segments.

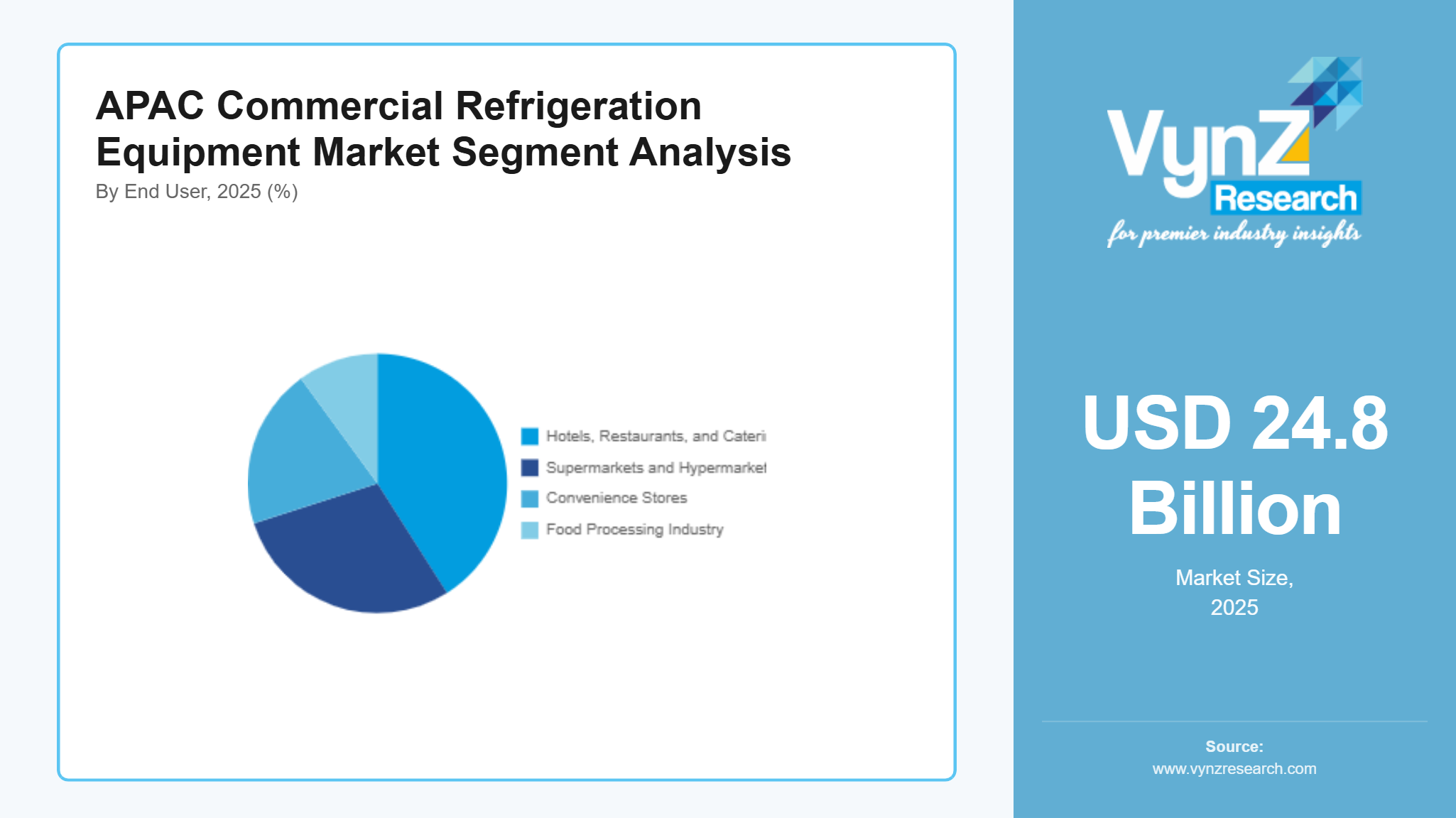

By End User

The hospitality sector generated the most revenue for the market during 2025 when it produced approximately 41% of total earnings which resulted from tourism growth, urban infrastructure development and hotel and restaurant expansion. The regulatory standards which health authorities set for food safety and storage requirements encourage all commercial kitchens and service facilities to install equipment according to established protocols.

The food processing sector expands fastest because it will reach a compound annual growth rate of 10.4% from 2026 until 2035. The food manufacturing sector, export-oriented production activities and value-added processing operations create demand for advanced refrigeration solutions. The government initiatives which aim to create stronger food supply chains and decrease post-harvest losses will drive food supply chain adoption which will lead to long-term sector growth.

Regional Insights

China

China held a 34% share of the APAC commercial refrigeration equipment market in 2025 through food processing industry growth and organized retail system development. The market experiences growth because urban areas like Shanghai, Beijing and Guangzhou drive demand for packaged and frozen food items. The government programs which aim to enhance cold chain systems and food safety control lead to increased funding for modern refrigeration technology. The national programs which focus on reducing food waste while enhancing supply chain operations drive businesses to implement food waste recycling practices across their commercial and industrial facilities.

India

India held an 18% share of the APAC commercial refrigeration equipment market in 2025 due to urbanization growth and increased investment in food retail and storage facilities. The market experiences growth because organized retail and food service industries continue to expand their operations. The public health framework needs food safety regulations which government backed cold chain development programs will establish to create operational standards for all end use industries. The urban market for milk and processed food storage solutions is growing which drives sector growth across both metropolitan areas and tier two cities.

Japan

Japan maintained a 14% share of the APAC commercial refrigeration equipment market in 2025 because commercial buildings adopted new technology and modernized their infrastructure. The market growth correlates with the high demand for systems which use less energy combined with refrigeration technologies that follow environmental regulations. The government regulations which promote low emission refrigerants and sustainable energy usage lead to product adoption in both retail and hospitality sectors. The market maintains its stability because consumers demand high quality food storage solutions which help them meet regulatory requirements.

South Korea

South Korea held a 10% share of the APAC commercial refrigeration equipment market in 2025 because retail expansion and food processing industry funding increased during that time. The market growth stems from supermarkets and convenience store chains adopting new refrigeration technology at an increasing rate. Market performance improves because government programs which support energy efficiency and smart infrastructure development create better business conditions. The rising public understanding of food safety requirements has prompted more restaurants and businesses to buy refrigeration systems.

Rest of Asia Pacific

Rest of Asia Pacific region held an 8% share of the APAC commercial refrigeration equipment market in 2025 because developing countries were making capital investments in food logistics and cold storage systems. The regions experience growth because supply chains are becoming better while more businesses require temperature-controlled storage systems. The government-backed programs which aim to decrease food waste while boosting agricultural value chains help the market to expand further. The remaining share of the market distribution is held by smaller regional markets which are not present in the previous list thus maintaining a complete market distribution of 100%.

Competitive Landscape / Company Insights

The market operates with moderate to high competition because global and regional companies compete through their product development and their market entry into new regions. Companies are increasingly investing in energy efficient technologies, smart cooling systems, and sustainable refrigerants to strengthen their market position. Government initiatives which promote food safety standards, energy efficiency regulations and cold chain infrastructure development in Asia Pacific regions serve as adoption support for the program. The frameworks established by these organizations drive manufacturers to develop new technological abilities while extending their operational reach throughout retail and hospitality and food processing industries.

Mini Profiles

Carrier Global Corporation focuses on commercial refrigeration and HVAC solutions, supported by strong global distribution networks and established brand recognition across retail, food service, and industrial applications.

Daikin Industries Ltd. operates in premium segments, emphasizing energy efficient technologies, advanced cooling systems, and environmentally compliant refrigerants to meet evolving regulatory and sustainability requirements.

Electrolux AB leverages strong product innovation and consumer focused design to expand market presence, supported by a wide portfolio catering to both commercial kitchens and food retail environments.

Haier Smart Home Co. Ltd. focuses on smart refrigeration and connected appliance solutions, supported by cost efficient manufacturing and expanding digital ecosystem integration across commercial and retail sectors.

Panasonic Corporation operates in advanced and niche segments, emphasizing performance reliability, energy efficiency, and integrated cooling technologies tailored for commercial and industrial applications.

Key Players

- Blue Star Limited

- Carrier Global Corporation

- Daikin Industries Ltd.

- Dover Corporation

- Electrolux AB

- Haier Smart Home Co. Ltd.

- Hussmann Corporation

- Panasonic Corporation

- The Middleby Corporation

- Whirlpool Corporation

Recent Developments

In April, 2025, Daikin Industries Ltd. expanded its next generation commercial refrigeration lineup focusing on low global warming refrigerants and high efficiency cooling systems. The company strengthened its Asia Pacific supply capabilities to meet rising demand from retail and food service infrastructure.

In June, 2025, Haier Smart Home Co. Ltd. introduced upgraded smart commercial refrigeration systems integrated with IoT based monitoring and predictive maintenance features. The development supports growing demand from supermarkets and cold chain operators across emerging Asian economies.

In March, 2026, Panasonic Corporation enhanced its commercial cooling portfolio with advanced inverter driven refrigeration systems aimed at reducing energy consumption in hospitality and retail applications. The company continues to focus on sustainability driven innovation aligned with global energy efficiency standards.

In October, 2025, Hussmann Corporation expanded its commercial refrigeration solutions portfolio with energy optimized display cases for food retail environments. The initiative supports increasing demand for sustainable refrigeration systems in supermarkets and convenience store chains.

In January, 2026, Blue Star Limited announced expansion of its commercial refrigeration manufacturing capacity in India to support rising demand from food service and organized retail sectors. The company is focusing on energy efficient and cost optimized cooling systems for domestic and export markets.

APAC Commercial Refrigeration Equipment Market Coverage

Product Type Insight and Forecast 2026 - 2035

- Transportation Refrigeration Equipment

- Refrigerators & Freezers

- Beverage Refrigeration

- Walk-in Coolers

- Ice-making Machinery

Application Insight and Forecast 2026 - 2035

- Food Service

- Food & Beverage Retail

- Food & Beverage Distribution

- Food & Beverage Production

End User Insight and Forecast 2026 - 2035

- Hotels

- Restaurants

- and Catering (HoReCa)

- Supermarkets and Hypermarkets

- Convenience Stores

- Food Processing Industry

APAC Commercial Refrigeration Equipment Market by Region

- China

- By Product Type

- By Application

- By End User

- Japan

- By Product Type

- By Application

- By End User

- India

- By Product Type

- By Application

- By End User

- South Korea

- By Product Type

- By Application

- By End User

- Vietnam

- By Product Type

- By Application

- By End User

- Thailand

- By Product Type

- By Application

- By End User

- Malaysia

- By Product Type

- By Application

- By End User

- Rest of Asia-Pacific

- By Product Type

- By Application

- By End User

Table of Contents for APAC Commercial Refrigeration Equipment Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Product Type

1.2.2. By

Application

1.2.3. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. APAC Market Estimate and Forecast

4.1. APAC Market Overview

4.2. APAC Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Product Type

5.1.1. Transportation Refrigeration Equipment

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Refrigerators & Freezers

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Beverage Refrigeration

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Walk-in Coolers

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Ice-making Machinery

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.2. By Application

5.2.1. Food Service

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Food & Beverage Retail

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Food & Beverage Distribution

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Food & Beverage Production

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.3. By End User

5.3.1. Hotels

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Restaurants

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. and Catering (HoReCa)

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Supermarkets and Hypermarkets

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Convenience Stores

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.3.6. Food Processing Industry

5.3.6.1. Market Definition

5.3.6.2. Market Estimation and Forecast to 2035

6. China Market Estimate and Forecast

6.1. By

Product Type

6.2. By

Application

6.3. By

End User

7. Japan Market Estimate and Forecast

7.1. By

Product Type

7.2. By

Application

7.3. By

End User

8. India Market Estimate and Forecast

8.1. By

Product Type

8.2. By

Application

8.3. By

End User

9. South Korea Market Estimate and Forecast

9.1. By

Product Type

9.2. By

Application

9.3. By

End User

10. Vietnam Market Estimate and Forecast

10.1. By

Product Type

10.2. By

Application

10.3. By

End User

11. Thailand Market Estimate and Forecast

11.1. By

Product Type

11.2. By

Application

11.3. By

End User

12. Malaysia Market Estimate and Forecast

12.1. By

Product Type

12.2. By

Application

12.3. By

End User

13. Rest of Asia-Pacific Market Estimate and Forecast

13.1. By

Product Type

13.2. By

Application

13.3. By

End User

14. Company Profiles

14.1.

Blue Star Limited

14.1.1.

Snapshot

14.1.2.

Overview

14.1.3.

Offerings

14.1.4.

Financial

Insight

14.1.5.

Recent

Developments

14.2.

Carrier Global Corporation

14.2.1.

Snapshot

14.2.2.

Overview

14.2.3.

Offerings

14.2.4.

Financial

Insight

14.2.5.

Recent

Developments

14.3.

Daikin Industries Ltd.

14.3.1.

Snapshot

14.3.2.

Overview

14.3.3.

Offerings

14.3.4.

Financial

Insight

14.3.5.

Recent

Developments

14.4.

Dover Corporation

14.4.1.

Snapshot

14.4.2.

Overview

14.4.3.

Offerings

14.4.4.

Financial

Insight

14.4.5.

Recent

Developments

14.5.

Electrolux AB

14.5.1.

Snapshot

14.5.2.

Overview

14.5.3.

Offerings

14.5.4.

Financial

Insight

14.5.5.

Recent

Developments

14.6.

Haier Smart Home Co. Ltd.

14.6.1.

Snapshot

14.6.2.

Overview

14.6.3.

Offerings

14.6.4.

Financial

Insight

14.6.5.

Recent

Developments

14.7.

Hussmann Corporation

14.7.1.

Snapshot

14.7.2.

Overview

14.7.3.

Offerings

14.7.4.

Financial

Insight

14.7.5.

Recent

Developments

14.8.

Panasonic Corporation

14.8.1.

Snapshot

14.8.2.

Overview

14.8.3.

Offerings

14.8.4.

Financial

Insight

14.8.5.

Recent

Developments

14.9.

The Middleby Corporation

14.9.1.

Snapshot

14.9.2.

Overview

14.9.3.

Offerings

14.9.4.

Financial

Insight

14.9.5.

Recent

Developments

14.10.

Whirlpool Corporation

14.10.1.

Snapshot

14.10.2.

Overview

14.10.3.

Offerings

14.10.4.

Financial

Insight

14.10.5.

Recent

Developments

15. Appendix

15.1. Exchange Rates

15.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

APAC Commercial Refrigeration Equipment Market