Asia Electric Two-Wheeler Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Product Type (E-scooters, E-bikes, E-motorcycles, Others), by Battery Type (Sealed lead acid, Lithium ion, Nickel metal hydride), by Battery Technology (Removable, Non removable), by Voltage (24V, 36V, 48V, 60V, 72V), by Region (China, India, Japan, South Korea, Southeast Asia, Rest of Asia)

| Status : Published | Published On : Apr, 2026 | Report Code : VRAT9668 | Industry : Automotive & Transportation | Available Format :

|

Page : 163 |

Asia Electric Two-Wheeler Market Overview

The Asia electric two-wheeler market which was valued at approximately USD 82.40 billion in 2025 and is estimated to rise further up to almost USD 94.10 billion by 2026, is projected to reach around USD 305.47 billion in 2035, expanding at a CAGR of about 14% during the forecast period from 2026 to 2035.

The market expands because urban air pollution increases and fuel prices rise while regulations demand vehicle electrification and people adopt lithium-ion battery and battery swapping systems. The need for affordable urban transportation solutions together with national electrification projects which receive ongoing funding creates market growth opportunities in China, India and Southeast Asia. The international energy and transport agencies report that electric two wheelers account for most electric vehicle usage in Asia because they have lower ownership expenses and match short distance travel needs.

The market development process receives strong support from government programs which aim to cut emissions while promoting the adoption of clean transportation solutions. The electric mobility programs in India and China provide vehicle adoption support through their national incentive programs and purchase subsidies and tax benefits. The data from the government shows that electric two-wheeler registrations experience continuous growth which happens because charging stations and local battery production facilities have increased. Manufacturers throughout the regional market expand their production capacity and invest in advanced energy storage technology because policy frameworks support both carbon neutrality and decreased fossil fuel usage.

Asia Electric Two-Wheeler Market Dynamics

Market Trends

The industry currently experiences major transformations through three technological developments which include new battery systems, alternate transportation methods for cities, and enhanced digital systems that operate inside vehicle networks. The market currently undergoes a transformation through the transition from conventional battery systems to lithium-ion battery systems, which reflect current customer needs for more efficient energy use and longer product lifespans and lower upkeep demands. The International Energy Agency together with government energy transition programs demonstrate a gradual movement away from traditional battery technologies toward modern energy storage systems which support sustainable transportation objectives.

Growth Drivers

The market experiences growth because its regulatory framework establishes emission reduction targets that drive persistent demand from urban transportation users. The market expands at a faster rate because companies invest more in building charging stations, battery production facilities and regional manufacturing networks. The electric mobility adoption programs, which receive government backing through financial incentives and infrastructure development support, create a demand pattern that will persist in important markets. The rising costs of fuel have increased sensitivity among consumers, which has driven more people to adopt the technology.

Market Restraints / Challenges

The market shows strong growth potential yet it encounters obstacles that will hinder its future development. The market remains inaccessible to price-sensitive consumers because high vehicle prices and battery replacement costs continue to exist as major barriers. The cost of electric mobility remains the main barrier to adoption according to governmental assessments, despite existing subsidy programs in multiple countries. The manufacturing and supply chain operations of battery component producers and raw material producers face operational challenges because they depend on battery shipments and raw material shipments from overseas.

Market Opportunities

The market provides major growth possibilities through battery swapping infrastructure development which urban areas need because they experience rising demand while charging stations face limited operational time. Companies that deliver flexible swapping systems, which combine cost efficiency with scalability, will attract additional customers from both delivery fleets and shared mobility services. The Indian government is launching standardized battery swapping networks through its pilot projects and regulatory frameworks which will help expedite battery swapping network establishment. The premium and high-performance electric two-wheeled market presents another important market opportunity through advanced battery technology and digital technology development, which enables businesses to create better profit margins, while they develop long-lasting customer relationships.

Asia Electric Two-Wheeler Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 82.40 Billion |

|

Revenue Forecast in 2035 |

USD 312.60 Billion |

|

Growth Rate |

14% |

|

Segments Covered in the Report |

By Product Type, By Battery Type, By Battery Technology, By Voltage |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

China, India, Japan, South Korea, Southeast Asia, Rest of Asia |

|

Key Companies |

AIMA Technology Group Co. Ltd., Ather Energy, Hero Electric Vehicles Pvt. Ltd., Honda Motor Co. Ltd., Jiangsu Kingbon Vehicle Co., Ltd., Jiangsu Xinri E-Vehicle Co. Ltd. (SUNRA), Lohia Auto Industries, Segway Inc., Terra Motors Corporation, Xiaomi Inc. |

|

Customization |

Available upon request |

Asia Electric Two-Wheeler Market Segmentation

By Product Type

E-scooters represented 56% of total revenue in 2025 within the market. Their widespread urban adoption and cost efficiency enable them to dominate in densely populated cities for short distance commuting purposes. Government programs which receive backing from authorities create demand for low emission urban transport systems and shared mobility solutions. Segment growth continues in China and India because vehicles require less maintenance and people use them more frequently than traditional vehicles.

The forecast period from 2026 to 2035 will see e-motorcycles achieve the strongest growth rate through their projected 15.2% CAGR. Consumers now prefer products which offer higher speed and longer runtime abilities. The development of advanced powertrain technologies and battery systems results in improved battery performance and longevity. The growth of commercial applications that include delivery and logistics services creates new opportunities for emerging urban centers.

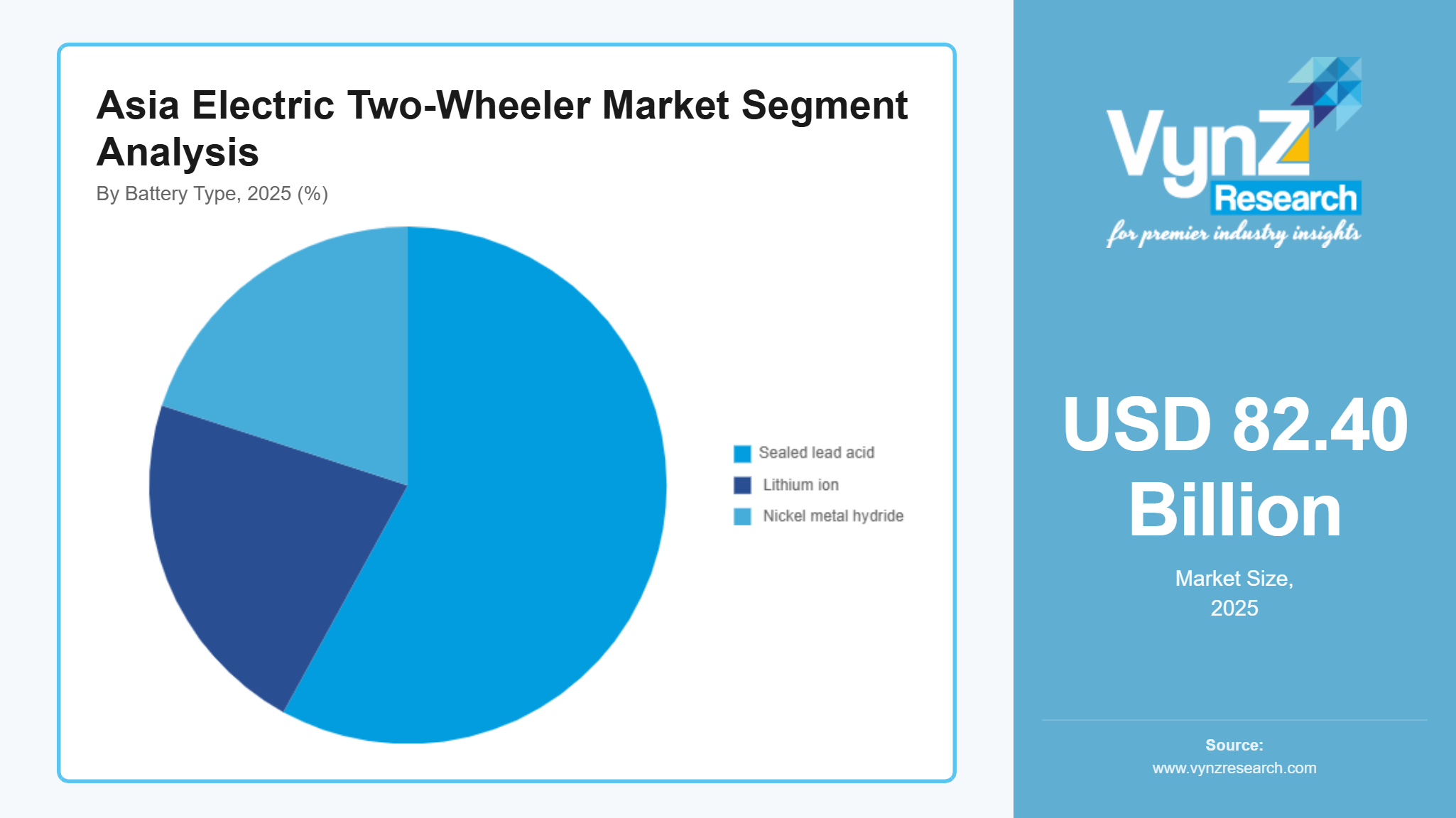

By Battery Type

Sealed lead acid batteries represented the largest market share in 2025 when they accounted for 48% of segment revenue. The market maintains its dominant position because of reverse supply chain costs which enable price sensitive markets to access their products. Electric mobility adoption government data shows that purchase patterns in developing economies depend mostly on product affordability. The modern world of advanced battery chemistries needs safer storage systems which these products provide.

Lithium-ion batteries will experience the fastest market growth because their estimated CAGR will reach 16.1% for the upcoming forecast period. The market for these products experiences growth because they provide better energy density which leads to greater battery life and shorter charging periods. Advanced energy storage technologies receive policy support which boosts domestic manufacturing efforts. The urban market appeal of lithium ion-based vehicles increases through the dual development of fast charging infrastructure and battery swapping networks.

By Battery Technology

Non removable battery systems held the largest share in 2025, accounting for approximately 58% of segment revenue. The vehicle design structure enables better safety through the integrated design system which prevents battery theft. Designers who create products continue to select fixed battery systems because they produce simpler design structures and lower manufacturing expenses. The adoption of integrated battery systems in mass market models gets reinforced through government safety standards and certification frameworks which require electric vehicles to follow established protocols.

The market for removable battery technology will experience the strongest growth because it will achieve a 15.6% CAGR between 2026 and 2035. The need for flexible charging solutions in urban areas with limited charging infrastructure drives market expansion. The adoption of battery swapping ecosystems grows through government pilot programs and regulatory frameworks which create new battery swapping ecosystems. The business model becomes especially attractive for fleet managers who need less downtime to improve their operations.

By Voltage

The 48V segment represented 44% of total revenue in 2025 to become the largest market segment. The e-scooter track system provides balanced performance which enables urban commuters to achieve their transportation needs. The process of standard voltage configuration enables segment adoption through its ability to match current battery systems. The development of budget-friendly electric mobility solutions through government initiatives allows this segment to expand into key Asian markets.

The higher voltage categories from 60V to 72V will experience stronger growth because their estimated CAGR will be 14.8% during the upcoming forecast period. The market experiences growth because there is rising consumer demand for products which deliver better speed performance and longer load capacity and extended range capabilities. The development of battery management systems together with power electronic systems enables users to fully utilize higher voltage platforms. The two key factors enable performance-oriented users and commercial applications to achieve their required operational efficiency level.

Regional Insights

China

The market in 2025 showed approximately 42% market share from China due to its strong manufacturing base, high urban population density and early electric mobility implementation. The three major urban centers of Beijing and Shanghai and Shenzhen permit extensive electric two-wheeler use for both personal and business purposes. Government policies that aim to reduce emissions and enhance urban air quality have created fast market growth opportunities.

Government backing for new energy vehicle programs through subsidies and production incentives and infrastructure development creates a system that drives ongoing electric mobility investments. The national energy and transport authorities report that regions achieve extensive market adoption through their existing supply chain systems and battery manufacturing facilities which serve as market development hubs.

India

India held about 18% market share in 2025 because rising fuel costs and growing urban traffic and strong policy support for electrification drive demand. The cities of Delhi, Bengaluru, and Mumbai show increasing numbers of people who use electric two wheelers for their daily travel and their last mile connection needs. The expanding middle class and cost sensitive customers drive the demand for products.

National electric mobility frameworks use incentive programs and tax benefits and infrastructure development to help the government bring electric vehicles into widespread use. The transport and energy department’s report that electric vehicle registrations are increasing as local manufacturers produce more vehicles and charging stations become more common in their area.

Japan and South Korea

Japan and South Korea together account for approximately 11% of the market in 2025 due to their technological progress and research potential and commitment to sustainable transportation methods. The cities of Tokyo and Seoul use electric two wheelers to achieve better urban transport and lower their emissions. The market maintains constant demand because customers understand advanced technologies and prefer to use them.

The government backing for clean energy transitions and smart mobility programs drives organizations to implement efficient electric transport solutions. The market in these developed economies becomes stronger through investments that enhance battery technology and safety standards and digital mobility solutions.

Rest of Asia

The rest of Asia, including Southeast Asian countries such as Indonesia, Vietnam, and Thailand, represents approximately 29% of the market in 2025. The regions experience growth because more people move to cities and more people buy two wheelers and more people learn about the advantages of electric mobility. The cities of Jakarta, Bangkok and Ho Chi Minh City experience more people who adopt electric two wheelers because they want to avoid traffic jams and high fuel expenses.

The government programs that support clean transportation together with the charging infrastructure investments and local assembly operations create an environment that supports business growth. All market share outside China, India, Japan and South Korea is distributed across this section of the market.

Competitive Landscape / Company Insights

The market features intense rivalry because both regional manufacturers and new market entrants compete through their innovative products, pricing methods and their efforts to establish operations in new regions. Companies are increasing their investment efforts into battery technology research and development and their production facilities and digital technology capabilities to improve their market competitiveness. The government-backed initiatives which support domestic manufacturing and environmentally friendly transportation systems and receive backing from national energy and transportation authorities create an environment that attracts new businesses to the market.

Mini Profiles

AIMA Technology Group Co. Ltd. focuses on electric scooters and motorcycles, supported by strong distribution networks and cost-efficient manufacturing across Asian markets, enabling wide consumer reach and consistent volume growth.

Hero Electric Vehicles Pvt. Ltd. operates in the mass segment, emphasizing affordability, energy efficiency, and urban mobility solutions, supported by strong domestic brand recognition and expanding dealer network across India.

Jiangsu Xinri E-Vehicle Co. Ltd. leverages advanced manufacturing capabilities and strategic partnerships to expand market presence, supported by continuous product innovation and growing export footprint across emerging Asian markets.

Segway Inc. focuses on smart electric mobility solutions, supported by strong global brand recognition and advanced digital integration capabilities, enabling differentiated offerings across urban mobility and personal transportation segments.

Xiaomi Inc. operates in the connected mobility segment, emphasizing design innovation and digital ecosystem integration, supported by strong consumer electronics presence and extensive online distribution channels across Asia.

Key Players

- AIMA Technology Group Co. Ltd.

- Ather Energy

- Hero Electric Vehicles Pvt. Ltd.

- Honda Motor Co. Ltd.

- Jiangsu Kingbon Vehicle Co., Ltd.

- Jiangsu Xinri E-Vehicle Co. Ltd. (SUNRA)

- Lohia Auto Industries

- Segway Inc.

- Terra Motors Corporation

- Xiaomi Inc.

Recent Developments

In March 2026, Ather Energy reported a significant rise in monthly sales, reaching over 33,000 units, driven by strong demand for its family focused scooter models. The company is also expanding its retail network and planning new product launches based on advanced platforms to strengthen market presence in 2026.

In October 2025, Hero Electric Vehicles Pvt. Ltd. strengthened its market position as legacy manufacturers increased their share of total electric two-wheeler registrations across India. The company is focusing on expanding its electric portfolio and leveraging strong dealer networks to capture rising demand in urban and semi urban regions.

In February 2026, AIMA Technology Group continued to expand production scale and product portfolio as part of broader industry shifts toward manufacturing readiness and execution focused growth.

The company is emphasizing large scale production capabilities and product diversification to strengthen competitiveness across Asian markets in 2026.

In February 2026, Honda Motor Co. Ltd. is actively focusing on electric two-wheeler product launches and expanding its electric mobility portfolio to align with regional electrification trends.

The company is increasing investments in product development and manufacturing scale to enhance its presence in the evolving electric mobility ecosystem.

Asia Electric Two-Wheeler Market Coverage

Product Type Insight and Forecast 2026 - 2035

- E-scooters

- E-bikes

- E-motorcycles

- Others

Battery Type Insight and Forecast 2026 - 2035

- Sealed lead acid

- Lithium ion

- Nickel metal hydride

Battery Technology Insight and Forecast 2026 - 2035

- Removable

- Non removable

Voltage Insight and Forecast 2026 - 2035

- 24V

- 36V

- 48V

- 60V

- 72V

Region Insight and Forecast 2026 - 2035

- China

- India

- Japan

- South Korea

- Southeast Asia

- Rest of Asia

Asia Electric Two-Wheeler Market by Region

- China

- By Product Type

- By Battery Type

- By Battery Technology

- By Voltage

- By Region

- Japan

- By Product Type

- By Battery Type

- By Battery Technology

- By Voltage

- By Region

- India

- By Product Type

- By Battery Type

- By Battery Technology

- By Voltage

- By Region

- South Korea

- By Product Type

- By Battery Type

- By Battery Technology

- By Voltage

- By Region

- Vietnam

- By Product Type

- By Battery Type

- By Battery Technology

- By Voltage

- By Region

- Thailand

- By Product Type

- By Battery Type

- By Battery Technology

- By Voltage

- By Region

- Malaysia

- By Product Type

- By Battery Type

- By Battery Technology

- By Voltage

- By Region

- Rest of Asia-Pacific

- By Product Type

- By Battery Type

- By Battery Technology

- By Voltage

- By Region

Table of Contents for Asia Electric Two-Wheeler Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Product Type

1.2.2. By

Battery Type

1.2.3. By

Battery Technology

1.2.4. By

Voltage

1.2.5. By

Region

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Asia Market Estimate and Forecast

4.1. Asia Market Overview

4.2. Asia Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Product Type

5.1.1. E-scooters

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. E-bikes

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. E-motorcycles

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Others

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.2. By Battery Type

5.2.1. Sealed lead acid

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Lithium ion

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Nickel metal hydride

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By Battery Technology

5.3.1. Removable

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Non removable

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By Voltage

5.4.1. 24V

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. 36V

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. 48V

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. 60V

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. 72V

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

5.5. By Region

5.5.1. China

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. India

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Japan

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. South Korea

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

5.5.5. Southeast Asia

5.5.5.1. Market Definition

5.5.5.2. Market Estimation and Forecast to 2035

5.5.6. Rest of Asia

5.5.6.1. Market Definition

5.5.6.2. Market Estimation and Forecast to 2035

6. China Market Estimate and Forecast

6.1. By

Product Type

6.2. By

Battery Type

6.3. By

Battery Technology

6.4. By

Voltage

6.5. By

Region

7. Japan Market Estimate and Forecast

7.1. By

Product Type

7.2. By

Battery Type

7.3. By

Battery Technology

7.4. By

Voltage

7.5. By

Region

8. India Market Estimate and Forecast

8.1. By

Product Type

8.2. By

Battery Type

8.3. By

Battery Technology

8.4. By

Voltage

8.5. By

Region

9. South Korea Market Estimate and Forecast

9.1. By

Product Type

9.2. By

Battery Type

9.3. By

Battery Technology

9.4. By

Voltage

9.5. By

Region

10. Vietnam Market Estimate and Forecast

10.1. By

Product Type

10.2. By

Battery Type

10.3. By

Battery Technology

10.4. By

Voltage

10.5. By

Region

11. Thailand Market Estimate and Forecast

11.1. By

Product Type

11.2. By

Battery Type

11.3. By

Battery Technology

11.4. By

Voltage

11.5. By

Region

12. Malaysia Market Estimate and Forecast

12.1. By

Product Type

12.2. By

Battery Type

12.3. By

Battery Technology

12.4. By

Voltage

12.5. By

Region

13. Rest of Asia-Pacific Market Estimate and Forecast

13.1. By

Product Type

13.2. By

Battery Type

13.3. By

Battery Technology

13.4. By

Voltage

13.5. By

Region

14. Company Profiles

14.1.

AIMA Technology Group Co. Ltd.

14.1.1.

Snapshot

14.1.2.

Overview

14.1.3.

Offerings

14.1.4.

Financial

Insight

14.1.5.

Recent

Developments

14.2.

Ather Energy

14.2.1.

Snapshot

14.2.2.

Overview

14.2.3.

Offerings

14.2.4.

Financial

Insight

14.2.5.

Recent

Developments

14.3.

Hero Electric Vehicles Pvt. Ltd.

14.3.1.

Snapshot

14.3.2.

Overview

14.3.3.

Offerings

14.3.4.

Financial

Insight

14.3.5.

Recent

Developments

14.4.

Honda Motor Co. Ltd.

14.4.1.

Snapshot

14.4.2.

Overview

14.4.3.

Offerings

14.4.4.

Financial

Insight

14.4.5.

Recent

Developments

14.5.

Jiangsu Kingbon Vehicle Co., Ltd.

14.5.1.

Snapshot

14.5.2.

Overview

14.5.3.

Offerings

14.5.4.

Financial

Insight

14.5.5.

Recent

Developments

14.6.

Jiangsu Xinri E-Vehicle Co. Ltd. (SUNRA)

14.6.1.

Snapshot

14.6.2.

Overview

14.6.3.

Offerings

14.6.4.

Financial

Insight

14.6.5.

Recent

Developments

14.7.

Lohia Auto Industries

14.7.1.

Snapshot

14.7.2.

Overview

14.7.3.

Offerings

14.7.4.

Financial

Insight

14.7.5.

Recent

Developments

14.8.

Segway Inc.

14.8.1.

Snapshot

14.8.2.

Overview

14.8.3.

Offerings

14.8.4.

Financial

Insight

14.8.5.

Recent

Developments

14.9.

Terra Motors Corporation

14.9.1.

Snapshot

14.9.2.

Overview

14.9.3.

Offerings

14.9.4.

Financial

Insight

14.9.5.

Recent

Developments

14.10.

Xiaomi Inc.

14.10.1.

Snapshot

14.10.2.

Overview

14.10.3.

Offerings

14.10.4.

Financial

Insight

14.10.5.

Recent

Developments

15. Appendix

15.1. Exchange Rates

15.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Asia Electric Two-Wheeler Market