Electric Deluge Valve Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Type (Electrically Actuated Deluge Valves, Hydraulic, Foam-Water Deluge Systems, Corrosion-Resistant, Others), by Actuation Technology (Solenoid-Operated, Manual Release Station Integration, Releasing Control Panel Compatibility, Supervisory Monitoring, Others), by End Use Industry (Oil & Gas and Petrochemicals, Power Generation and Utilities, Chemical & Industrial Manufacturing), by Application (Industrial Process Areas, Tank Farms, Loading Racks and Terminals, Transformer and Substation Protection, Warehousing, Others), by Distribution Channel (Direct Sales, Authorized Distributors)

| Status : Published | Published On : Apr, 2026 | Report Code : VRSME9206 | Industry : Semiconductor & Electronics | Available Format :

|

Page : 190 |

Electric Deluge Valve Market Overview

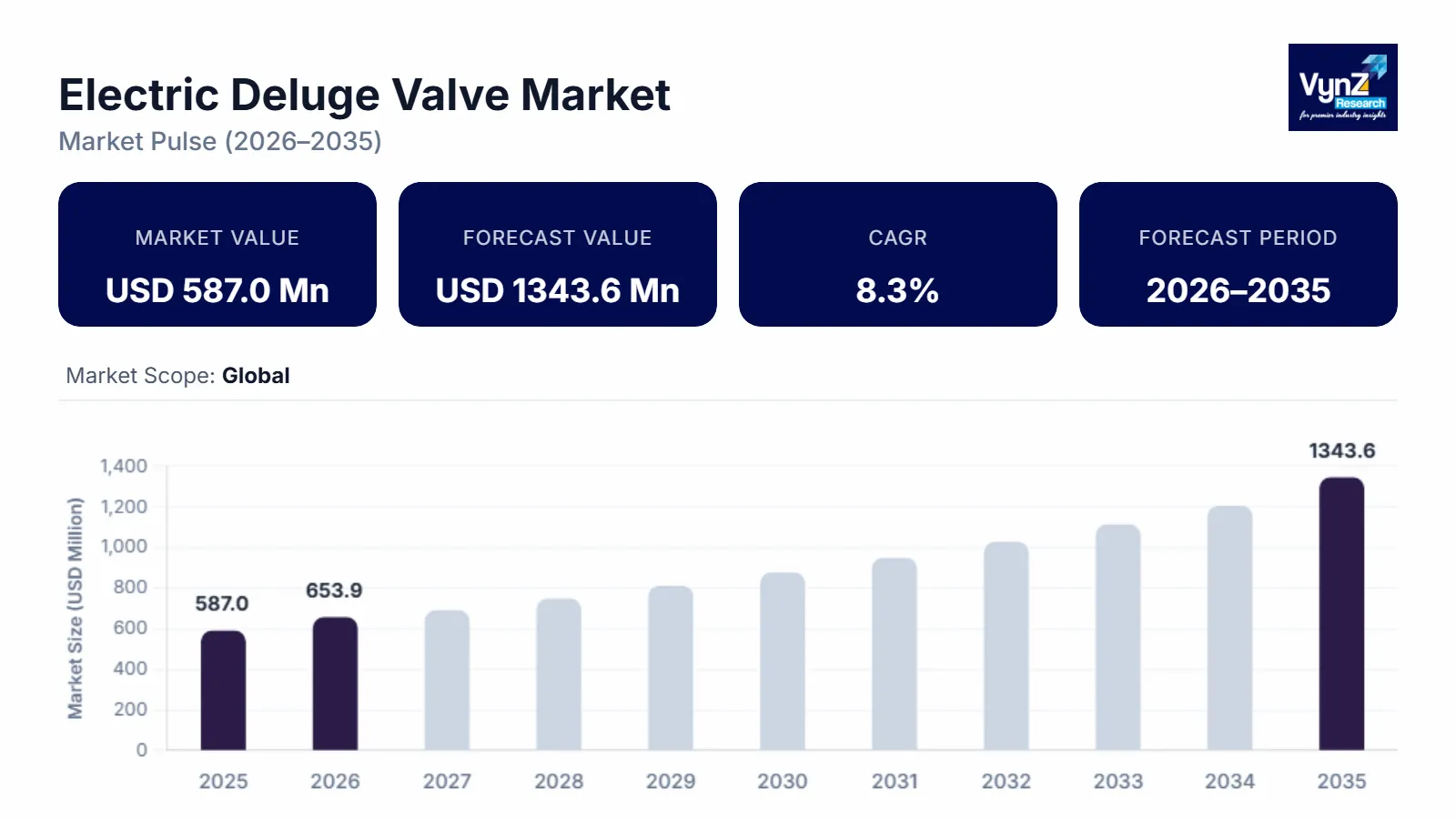

The electric deluge valve market which was valued at approximately USD 587.0 million in 2025 and is estimated to reach around USD 653.9 million in 2026, is projected to reach close to USD 1343.6 million by 2035, expanding at a CAGR of about 8.3% during the forecast period from 2026 to 2035.

The market is driven by rising investments in fire protection systems for high-hazard facilities such as oil & gas, chemical and petrochemical plants, power generation, warehousing and logistics, and large-scale manufacturing. Electric deluge valves are critical components in deluge sprinkler systems, enabling rapid water discharge across a protected area when triggered by fire detection and control panels. Stricter fire safety regulations, insurance compliance requirements, and increasing awareness of life and asset protection are accelerating adoption across industrial and commercial end users. Growth is further supported by the expansion of critical infrastructure projects, including airports, data centers, refineries, and renewable energy facilities, where fast-acting, reliable suppression systems are required. In parallel, government-funded resilience and infrastructure programs are supporting upgrades to safety-critical systems.

FEMA’s Building Resilient Infrastructure and Communities (BRIC) program published a funding opportunity making USD 1 billion available (covering FY 2024/2025) for hazard mitigation and resilient infrastructure projects, while the U.S. Infrastructure Investment and Jobs Act (IIJA) authorized about USD 1.2 trillion in infrastructure spending, including USD 550 billion in new investments. At the asset level, U.S. airport modernization funding has also included fire protection upgrades (e.g., FAA grants totaling USD 17 million awarded for fire alarm and fire sprinkler system improvements at a major airport), reinforcing demand for code-compliant, monitored deluge and sprinkler assemblies. The market also benefits from modernization of legacy fire water networks and retrofits that replace manual or pneumatic actuation with electrically actuated valves integrated with automated detection systems. Additionally, demand for remote monitoring, faster response times, and improved system diagnostics is encouraging deployment of electrically controlled deluge solutions, particularly in facilities pursuing digitalized safety management and centralized fire control.

Electric Deluge Valve Market Dynamics

Market Trends

Integration of electrically actuated deluge valves with intelligent fire detection and building/industrial automation systems is a key trend shaping the market. End users are increasingly deploying addressable fire alarm panels, heat/flame/smoke detectors, and supervisory control that can trigger deluge release quickly while enabling event logging, remote status indication, and diagnostics. As facilities adopt centralized safety control rooms and connected operations, electric actuation is preferred for its fast response, simplified interfacing with control logic, and compatibility with condition monitoring of valve position, solenoids, and power supply health. Another notable trend is the growing use of packaged skid-mounted deluge systems for modular construction projects, as well as increased demand for corrosion-resistant materials and coatings for harsh environments such as offshore platforms, coastal installations, and chemical processing plants.

Growth Drivers

Increasing deployment of deluge fire suppression systems in high-risk industrial environments is a major driver of the electric deluge valve market. Facilities handling flammable liquids, pressurized gases, and high heat loads require rapid, high-volume water discharge to control fire spread, cool equipment, and protect structural integrity. Electric deluge valves support fast and reliable system actuation through integration with detection and release panels, which is particularly important in large footprint sites where manual intervention may be delayed. Expansion of oil & gas exploration and processing, petrochemical capacity additions, and growth in power generation and heavy manufacturing are increasing installed base demand. In parallel, new construction of data centers, logistics warehouses, and large commercial complexes is driving adoption of engineered fire protection solutions, including electrically supervised deluge systems. Replacement demand also remains strong as aging fire water networks are upgraded to meet current codes, improve reliability, and enable remote monitoring and testing.

Market Restraints / Challenges

Complex installation, commissioning, and maintenance requirements can restrain the adoption of electric deluge valve systems, particularly in facilities with limited fire protection engineering resources. Electric deluge valves must be properly sized for hydraulic demand and pressure losses, coordinated with trim components, and integrated with detection and releasing control panels to ensure correct actuation logic and supervision. In corrosive or hazardous locations, additional requirements such as suitable enclosures, cable routing, grounding, and compliance with area classification can increase overall project cost. Reliability concerns related to power supply continuity, wiring integrity, solenoid performance, and environmental exposure also necessitate routine inspection and testing, which adds lifecycle cost. Furthermore, retrofitting existing deluge systems may require downtime, revalidation, and coordination with authorities having jurisdiction (AHJs) and insurers, which can extend project timelines.

Market Opportunities

Growing investment in smart fire protection and remote asset monitoring is creating significant opportunities for the electric deluge valve market. Industrial operators and building owners are increasingly adopting digitally enabled safety systems that provide real-time status, alarm analytics, and predictive maintenance insights to reduce unplanned downtime and improve compliance. Electric deluge valves that support supervisory feedback (valve position, solenoid status, low voltage alerts) can be integrated into SCADA, DCS, or building management systems to enhance situational awareness. Opportunities are also emerging from infrastructure buildout in data centers, battery manufacturing, and energy transition projects, where high-value assets require robust suppression. Government-led initiatives to accelerate digital and critical infrastructure are indirectly expanding the addressable base for advanced fire protection: in the United States, many states offer data-center-focused tax incentives, and Virginia’s Joint Legislative Audit and Review Commission reported about USD 928 million in sales and use tax relief for data centers in fiscal year 2023, underscoring the scale of policy support behind new build-outs that must be protected and supervised. In addition, public workforce programs linked to such projects (e.g., state job training allocations for large data center developments) can strengthen local installation and maintenance capacity over time. In addition, demand for corrosion-resistant designs, low-maintenance trim, and pre-engineered packaged deluge skids is increasing in offshore, marine, and chemical processing applications, supporting premium product differentiation for manufacturers.

Global Electric Deluge Valve Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 587 Million |

|

Revenue Forecast in 2035 |

USD 1343.6 Million |

|

Growth Rate |

8.3% |

|

Segments Covered in the Report |

Type, Actuation Technology, End Use Industry, Distribution Channel |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia-Pacific, Rest of the World |

|

Key Companies |

Johnson Controls, Honeywell International Inc., Tyco Fire Products, Victaulic, Viking Group, Inc., Cla-Val, Rapidrop Global Ltd., AVK International, Bermad, Bray International |

|

Customization |

Available upon request |

Electric Deluge Valve Market Segmentation

By Type

Electrically actuated deluge valves are the largest category with a market share of about 40% in 2025, owing to their widespread use in industrial and commercial deluge systems where rapid, automated water discharge is required. These valves integrate seamlessly with fire detection and release panels, enabling fast actuation, supervisory monitoring, and centralized control. Their adoption is strong in refineries, chemical plants, power facilities, large warehouses, and infrastructure projects where fire risk is high, and response time is critical. The increasing preference for automated safety systems and code-compliant supervised valve assemblies continues to support demand in this segment.

Corrosion-resistant is the fastest-growing category with a CAGR of 8.5% during the forecast period, driven by rising investments in offshore oil & gas, marine terminals, coastal industrial zones, and chemical processing plants where exposure to salt spray, humidity, and aggressive chemicals accelerates wear. Demand is increasing for valves with robust coatings, stainless steel trim, and enhanced supervision features that improve reliability and reduce maintenance frequency. In addition, growth in modular packaged deluge skids for harsh environments is accelerating the adoption of high-specification electric deluge valve solutions.

By Actuation Technology

Solenoid-operated is the largest category with a market share of about 45% in 2025, as it is the standard approach for electrically actuating deluge valves in supervised deluge systems. Solenoid release enables rapid opening upon signal from a fire alarm/releasing control panel, supporting automated response and improved repeatability compared to manual actuation. This configuration is widely specified in industrial facilities and large commercial projects due to its compatibility with detection logic, alarms, and monitoring requirements.

Supervisory monitoring is the fastest-growing category with a CAGR of 8.7% during the forecast period, due to the increasing need for remote monitoring, event diagnostics, and compliance reporting. End users are adopting releasing control panels and valve supervision modules that provide status feedback and integrate with SCADA, BMS, or plant safety systems. This trend is particularly strong in data centers, energy facilities, and large industrial sites seeking improved reliability and faster incident response.

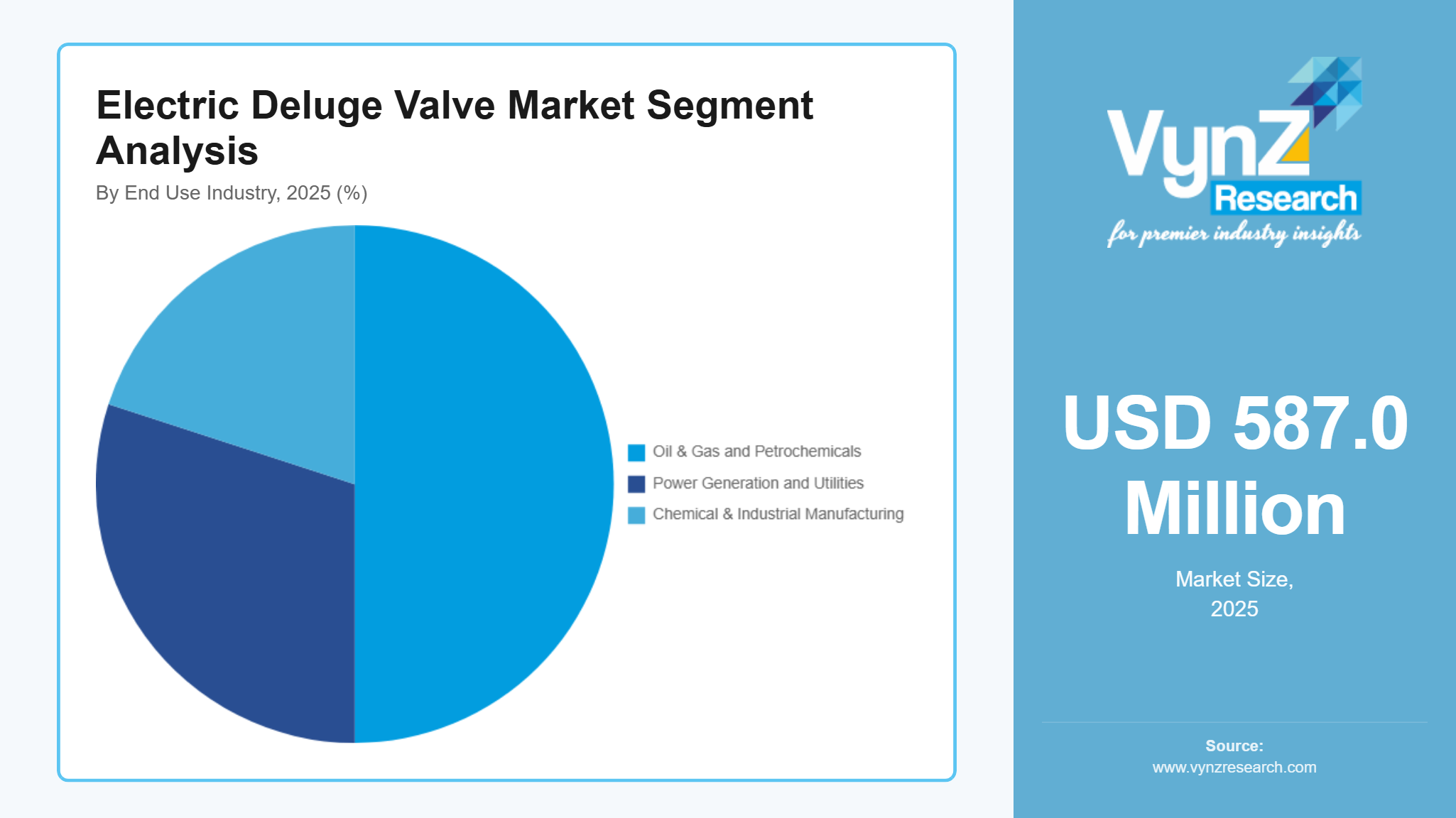

By End Use Industry

Oil & gas and petrochemicals is the largest category with a market share of about 50% in 2025, as deluge systems are widely deployed to protect process units, storage tanks, loading racks, compressor stations, and offshore modules where flammable hazards are significant. Electric deluge valves are favored for integration with flame and heat detection, emergency shutdown logic, and centralized fire control, enabling rapid water application for cooling and exposure protection. Continuous investment in safety upgrades, regulatory compliance, and insurance requirements support sustained demand in this end-use segment.

Chemical & industrial manufacturing is the fastest-growing category with a CAGR of 8.8% during the forecast period, driven by rapid expansion of digital infrastructure and high-value storage facilities. While these sites commonly use multiple fire protection approaches, deluge or open sprinkler systems are increasingly considered for specific high-challenge areas, equipment rooms, or exposure protection needs where fast water application is required. The focus on uptime, compliance, and remote monitoring is also increasing preference for electrically supervised deluge valve assemblies that can be tested and monitored through centralized facility management systems.

By Application

Industrial process areas are the largest category with a market share of about 35% in 2025, as these zones require rapid water discharge for exposure protection and fire control around critical equipment. Electric deluge valves are commonly specified to deliver immediate water application upon detection, helping reduce escalation risk in facilities with high heat and flammable inventories. Their ability to interface with detection systems and emergency response logic makes them a preferred choice for engineered fire protection in process industries.

Tank farms, loading racks, and terminals are the fastest-growing category during the forecast period, supported by expanding fuel storage capacity, chemical logistics networks, and terminal modernization. These applications often require fast-acting deluge for spill fires and exposure protection, with electric actuation enabling tight integration with flame detection, emergency shutdown systems, and remote activation from control rooms. Increased emphasis on risk mitigation and compliance is driving new installations and retrofits in this segment.

By Distribution Channel

Direct sales is the largest category with a market share of about 60% in 2025, because deluge valve systems are often engineered-to-order and specified as part of larger fire protection projects. Engineering, procurement, and construction (EPC) firms and specialized fire protection contractors typically procure complete valve assemblies, trim, and releasing panels directly from manufacturers to meet project specifications, approvals, and commissioning timelines. This channel is especially prominent in industrial projects such as refineries, chemical plants, terminals, and large infrastructure developments.

Authorized distributors are the fastest-growing category during the forecast period, driven by increasing replacement of legacy actuation mechanisms, expansion of service networks, and rising demand for spare parts and supervised trim kits. Many facilities upgrade existing deluge systems to electric actuation and monitoring without full system replacement, which supports demand through distributor-led retrofit and service channels. Faster availability of standardized valve assemblies and localized inventory is also improving adoption in emerging markets.

Regional Insights

North America

North America accounted for approximately 32% of the market in 2025, driven by stringent fire safety regulations, strong presence of oil & gas and chemical industries, and high adoption of automated fire suppression systems across industrial and commercial facilities. Strong demand from the United States and Canada continues to support market growth, particularly across refineries, terminals, data centers, manufacturing plants, and logistics infrastructure. According to the U.S. Infrastructure Investment and Jobs Act (IIJA), nearly USD 1.2 trillion has been allocated for infrastructure modernization, while FEMA’s BRIC program announced USD 1 billion in funding for resilient infrastructure and hazard mitigation projects.

Government investments, combined with increasing compliance requirements and modernization of fire protection infrastructure, are encouraging adoption of electrically actuated and supervised deluge valve systems across safety-critical facilities.

Asia-Pacific

Asia Pacific accounted for approximately 28% of the market in 2025, supported by rapid industrialization, expansion of petrochemical and refining capacity, and rising infrastructure construction across China, India, Southeast Asia, and Australia. Increasing adoption across manufacturing facilities, logistics parks, airports, power generation plants, and industrial corridors is driving consistent demand for electric deluge valve systems. According to the Government of India’s National Infrastructure Pipeline, planned investments of nearly USD 1.4 trillion are focused on transportation, energy, and urban infrastructure development, supporting installation of advanced fire protection systems.

Government initiatives focused on industrial safety, urban modernization, and stricter building code enforcement are further accelerating adoption of electrically monitored fire suppression solutions across the region.

Europe

Europe accounted for approximately 19% of the market in 2025, supported by strict industrial safety regulations, modernization of aging infrastructure, and strong demand from chemical processing, energy, transportation, and logistics sectors. Demand remains strong across Germany, France, the United Kingdom, and other major industrial economies. According to the European Commission, approximately €392 billion has been allocated under the Cohesion Policy (2021–2027) to support infrastructure, industrial development, and energy modernization projects across the region.

Growth in Europe is supported by increasing adoption of automated fire protection systems, upgrades to supervised deluge networks, and rising investments in data centers, transportation hubs, and industrial safety modernization projects.

Rest of the World

The rest of the world, including the Middle East, Africa, and Latin America, accounted for approximately 8% of the market in 2025, driven by investments in oil & gas, petrochemicals, mining, and infrastructure projects. Saudi Arabia’s Vision 2030 program, supported by planned investments exceeding USD 1 trillion, continues to drive development of industrial cities, energy facilities, and large-scale infrastructure projects requiring advanced fire suppression systems. In Latin America, industrial modernization and mining sector expansion are supporting steady market growth.

Increasing focus on industrial safety compliance, insurer requirements, and modernization of legacy fire protection systems is expected to support long-term market opportunities across these regions. Collectively, the above-mentioned regional markets account for nearly 87% of the global electric deluge valve market, while the remaining share is distributed among smaller developing markets worldwide.

Competitive Landscape / Company Insights

The electric deluge valve market is moderately consolidated, characterized by established fire protection OEMs and valve specialists offering deluge valve assemblies, trim packages, releasing control compatibility, and supervisory accessories. Leading companies compete on certification compliance, reliability in harsh environments, breadth of valve sizes and pressure ratings, and the ability to deliver complete engineered solutions for industrial hazards. Many players strengthen their positions through partnerships with fire protection contractors and EPC firms, product approvals for global codes and standards, and expansion of service and distribution networks to support installation, testing, and maintenance.

Companies also differentiate through corrosion-resistant designs, pre-assembled and factory-tested valve skids, and enhanced supervision features that enable remote monitoring and faster troubleshooting. Product innovation is increasingly focused on reducing false trips, simplifying commissioning, improving trim maintainability, and supporting integration with modern releasing panels and automation systems. Regional manufacturers compete by offering cost-effective solutions and localized support, while global brands leverage certifications, installed base, and broad channel reach.

Mini Profiles

Johnson Controls offers a broad portfolio of fire suppression and control solutions, including deluge valve assemblies and system integration capabilities for industrial and commercial fire protection applications.

Honeywell International Inc. provides fire detection, releasing control, and building safety technologies that support electrically actuated deluge system deployment and monitoring across critical facilities.

Viking Group, Inc. manufactures fire protection equipment including deluge and sprinkler system valves, offering engineered solutions and components used across industrial, commercial, and special hazard applications.

Victaulic Company offers fire protection system components and valves, supporting deluge and sprinkler system installations through integrated mechanical piping solutions and engineered fire protection products.

Cla-Val Company supplies automatic control valves used in fire protection and waterworks applications, including deluge and related valve solutions designed for reliable performance and code compliance.

Key Players

- Johnson Controls International plc

- Honeywell International Inc.

- Victaulic Company

- Viking Group, Inc.

- Cla-Val Company

- Bermad CS Ltd.

- AVK Holding A/S

- Rapidrop Global Ltd.

- Bray International, Inc.

- NIBCO Inc.

- Potter Electric Signal Company, LLC

Recent Developments

In January 2026, Johnson Controls expanded capacity for deluge valve production and testing to meet rising demand for electrically supervised deluge systems across industrial and critical infrastructure projects.

In December 2025, Honeywell International Inc. introduced an updated deluge releasing control panel configuration aimed at improving integration with electric deluge valve actuation and supervisory monitoring.

In October 2025, Victaulic Company expanded availability of its deluge valve and electric release trim options to support faster installation and serviceability for large-scale fire protection projects.

In August 2025, Bermad secured new deployments for electrically controlled deluge valves in high-hazard facilities, supporting remote actuation and valve position feedback for fire & gas monitoring.

In March 2026, HD Fire Protect Limited received UL Listing for advanced deluge valves with integrated pressure-reducing mechanisms designed for industrial and critical infrastructure fire protection applications.

Global Electric Deluge Valve Market Coverage

Type Insight and Forecast 2026 - 2035

- Electrically Actuated Deluge Valves

- Hydraulic

- Foam-Water Deluge Systems

- Corrosion-Resistant

- Others

Actuation Technology Insight and Forecast 2026 - 2035

- Solenoid-Operated

- Manual Release Station Integration

- Releasing Control Panel Compatibility

- Supervisory Monitoring

- Others

End Use Industry Insight and Forecast 2026 - 2035

- Oil & Gas and Petrochemicals

- Power Generation and Utilities

- Chemical & Industrial Manufacturing

Application Insight and Forecast 2026 - 2035

- Industrial Process Areas

- Tank Farms

- Loading Racks and Terminals

- Transformer and Substation Protection

- Warehousing

- Others

Distribution Channel Insight and Forecast 2026 - 2035

- Direct Sales

- Authorized Distributors

Global Electric Deluge Valve Market by Region

- North America

- By Type

- By Actuation Technology

- By End Use Industry

- By Application

- By Distribution Channel

- By Country - U.S., Canada, Mexico

- Europe

- By Type

- By Actuation Technology

- By End Use Industry

- By Application

- By Distribution Channel

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Type

- By Actuation Technology

- By End Use Industry

- By Application

- By Distribution Channel

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Type

- By Actuation Technology

- By End Use Industry

- By Application

- By Distribution Channel

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Electric Deluge Valve Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Type

1.2.2. By

Actuation Technology

1.2.3. By

End Use Industry

1.2.4. By

Application

1.2.5. By

Distribution Channel

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Type

5.1.1. Electrically Actuated Deluge Valves

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Hydraulic

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Foam-Water Deluge Systems

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Corrosion-Resistant

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Others

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.2. By Actuation Technology

5.2.1. Solenoid-Operated

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Manual Release Station Integration

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Releasing Control Panel Compatibility

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Supervisory Monitoring

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. Others

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.3. By End Use Industry

5.3.1. Oil & Gas and Petrochemicals

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Power Generation and Utilities

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Chemical & Industrial Manufacturing

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.4. By Application

5.4.1. Industrial Process Areas

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Tank Farms

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Loading Racks and Terminals

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Transformer and Substation Protection

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Warehousing

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

5.4.6. Others

5.4.6.1. Market Definition

5.4.6.2. Market Estimation and Forecast to 2035

5.5. By Distribution Channel

5.5.1. Direct Sales

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Authorized Distributors

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Type

6.2. By

Actuation Technology

6.3. By

End Use Industry

6.4. By

Application

6.5. By

Distribution Channel

6.5.1.

U.S. Market Estimate and Forecast

6.5.2.

Canada Market Estimate and Forecast

6.5.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Type

7.2. By

Actuation Technology

7.3. By

End Use Industry

7.4. By

Application

7.5. By

Distribution Channel

7.5.1.

Germany Market Estimate and Forecast

7.5.2.

France Market Estimate and Forecast

7.5.3.

U.K. Market Estimate and Forecast

7.5.4.

Italy Market Estimate and Forecast

7.5.5.

Spain Market Estimate and Forecast

7.5.6.

Russia Market Estimate and Forecast

7.5.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Type

8.2. By

Actuation Technology

8.3. By

End Use Industry

8.4. By

Application

8.5. By

Distribution Channel

8.5.1.

China Market Estimate and Forecast

8.5.2.

Japan Market Estimate and Forecast

8.5.3.

India Market Estimate and Forecast

8.5.4.

South Korea Market Estimate and Forecast

8.5.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Type

9.2. By

Actuation Technology

9.3. By

End Use Industry

9.4. By

Application

9.5. By

Distribution Channel

9.5.1.

Brazil Market Estimate and Forecast

9.5.2.

Saudi Arabia Market Estimate and Forecast

9.5.3.

South Africa Market Estimate and Forecast

9.5.4.

U.A.E. Market Estimate and Forecast

9.5.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Johnson Controls International plc

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Honeywell International Inc.

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Victaulic Company

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Viking Group, Inc.

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Cla-Val Company

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Bermad CS Ltd.

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

AVK Holding A/S

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Rapidrop Global Ltd.

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Bray International, Inc.

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

NIBCO Inc.

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

Potter Electric Signal Company, LLC

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Electric Deluge Valve Market