UAE Data Center Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Data Center Type (Hyperscale Data Centers, Colocation Data Centers, Enterprise Data Centers, Edge Data Centers), by Data Center Size (Small Data Centers, Medium Data Centers, Large Data Centers, Massive Data Centers, Mega Data Centers), by Tier Standard (Tier 1 and Tier 2, Tier 3, Tier 4), by End User (IT and ITES, BFSI, Government, E commerce, Manufacturing, Media and Entertainment, Telecom, Healthcare, Other End Users), by Region (Dubai, Abu Dhabi, Sharjah, Rest of United Arab Emirates)

| Status : Published | Published On : May, 2026 | Report Code : VRSME9217 | Industry : Semiconductor & Electronics | Available Format :

|

Page : 126 |

UAE Data Center Market Overview

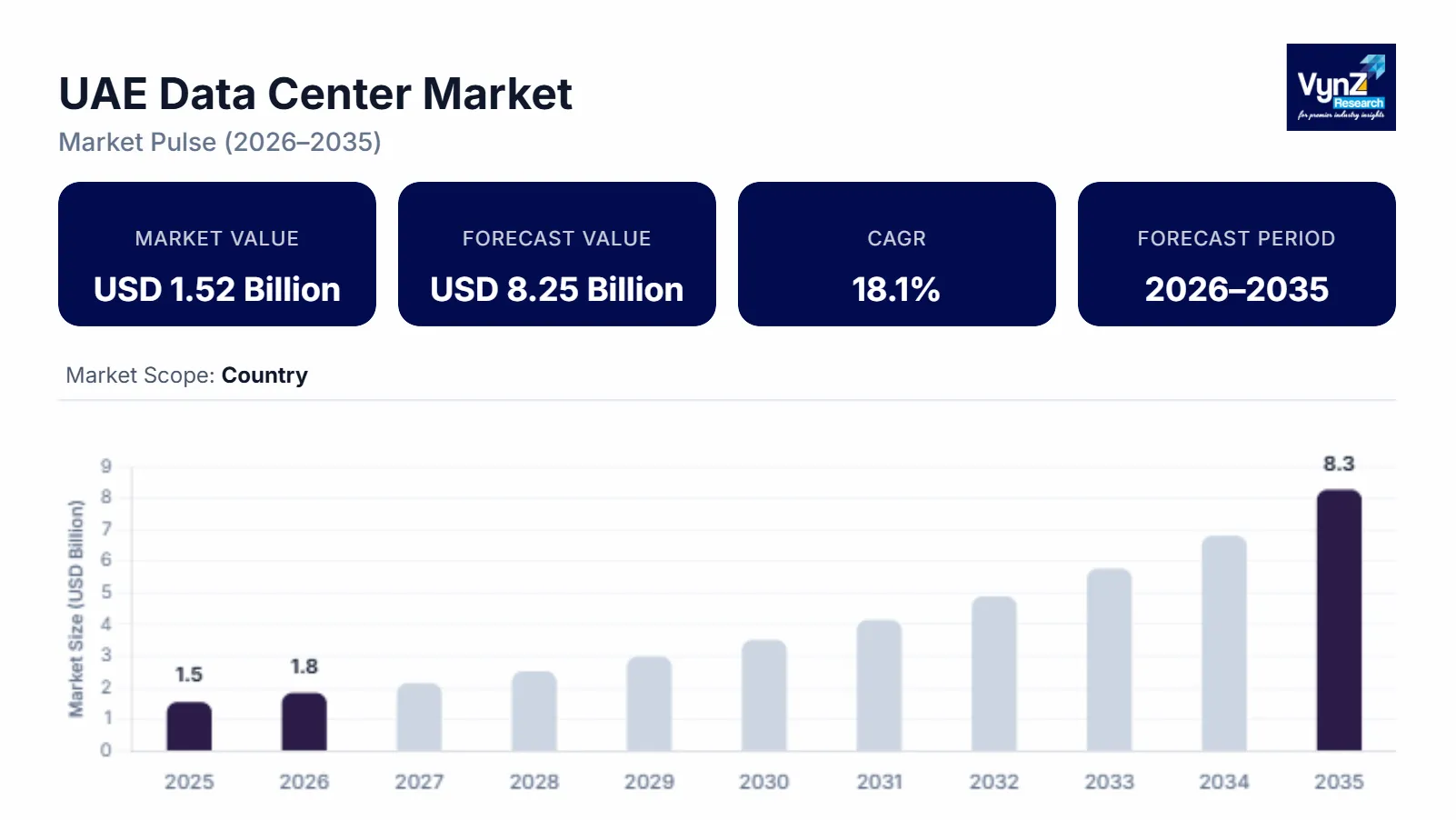

The UAE data center market which was valued at approximately USD 1.52 billion in 2025 and is estimated to rise further up to almost USD 1.81 billion by 2026, is projected to reach around USD 8.25 billion by 2035, expanding at a CAGR of about 18.1% during the forecast period from 2026 to 2035.

The market is seeing a strong expansion due to fast hyperscale cloud deployments and artificial intelligence workloads increasing quickly. There is the growing enterprise push for digital transformation across banking, telecom, and government. People are also paying more attention to sovereign cloud frameworks and safer data infrastructure and that is quietly but steadily making capacity additions grow in the major hubs like Dubai, Abu Dhabi, and the Northern Emirates.

Market growth is also fueled by national digital economy strategies and the spread of smart government ecosystems. There are also major investments in ICT infrastructure backed by telecom regulatory and digital authorities, alongside global standardization moves supported through international digital governance frameworks. Demand keeps increasing for low latency computing, data localization needs, and more advanced colocation services. With continued investments in AI ready infrastructure and cloud-first policies, long term adoption is getting reinforced across both enterprise and public sector ecosystems.

UAE Data Center Market Dynamics

Market Trends

In the market industry, there are some pretty noticeable shifts, especially with how hyperscale deployments are being planned and expansion of the whole edge infrastructure. Also, enterprise migration depends more on cloud native architectures. One of the bigger drivers behind it is the rapid acceptance of hyperscale and colocation driven infrastructure, more energy efficiency, better scale, and a capital expenditure structure. It is more optimized, less complicated and lines up well with national digital transformation programs and sovereign cloud adoption frameworks backed by government led digital economy initiatives in the United Arab Emirates. Another trend is around AI ready data center architectures along with accelerated digital penetration and the regulatory spotlight on data localization and cybersecurity compliance. All of this is affecting service offerings and it is making businesses adopt modular design, high density computing environments, and even integrated cooling and power optimization systems.

Growth Drivers

The market growth is largely backed by the rapid expansion of the digital economy, which keeps pulling in steady demand across cloud services, telecom infrastructure, and enterprise IT workloads. Investments in smart city development, 5G deployment, and national AI strategies are also adding fuel, supported by government led digital infrastructure programs and longer-term ICT investment frameworks in the United Arab Emirates. Enterprise demand for secure data storage and low latency computing is becoming more dominant. When enterprises and government entities start emphasizing data sovereignty, operational resilience, and performance optimization, it creates stronger adoption pressure for hyperscale and colocation services.

Market Restraints / Challenges

The market has challenges related to high capital expenditure requirements for hyperscale infrastructure development, including advanced cooling systems and energy efficient technologies. This continues to influence investment intensity, particularly for smaller operators and newer colocation providers, where budgets are not exactly flexible. High energy consumption plus the need for uninterrupted power supply creates real problems for developers and operators. Reliance on advanced imported semiconductor components, networking equipment, and specialized cooling technologies creates operational issues, cost pressures and expose operators to supply chain vulnerabilities.

Market Opportunities

The market has real opportunities especially in hyperscale expansion and AI optimized infrastructure development. This is mainly due to rising demand for high performance computing and cloud-based enterprise solutions. Firms that can deliver modular, scalable, and energy efficient data center solutions are in a strong position to grab additional demand from hyperscale cloud providers, telecom operators, and government digital platforms. Another opportunity is green data center development. With rising investments in energy efficient and sustainable infrastructure, and ties to national carbon neutrality plus environmental efficiency programs, the sector opens up pathways for long term cost optimization. Regulatory compliance, advancements in automation, smart monitoring systems, and liquid cooling technologies should further improve operational efficiency and help overall service reliability across the entire sector.

UAE Data Center Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 1.52 Billion |

|

Revenue Forecast in 2035 |

USD 8.25 Billion |

|

Growth Rate |

18.1% |

|

Segments Covered in the Report |

Data Center Type, Data Center Size, Tier Standard, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

Dubai, Abu Dhabi, Sharjah, Rest of United Arab Emirates |

|

Key Companies |

Amazon Web Services, China Mobile International, Damac Data Center, Equinix, Etisalat (e&), Khazna Data Centers, Microsoft, NTT Global Data Centers, Oracle, ST Telemedia Global Data Centers |

|

Customization |

Available upon request |

UAE Data Center Market Segmentation

By Data Center Type

Colocation data centers held the biggest share in 2025, roughly 41% of the total market revenue mostly because enterprises are outsourcing more, chasing cost optimization, and hybrid cloud architectures are being used extensively. It gets boost from telecom operators, BFSI organizations, and public sector bodies pushing for infrastructure that can grow, without turning everything into a full rebuild every time demand jumps.

Hyperscale data centers are also forecasted to move the quickest, about 19.2% growth, in the forecast window due to cloud service rollouts, artificial intelligence workloads, and big investments from global tech vendors. Government-led digital economy programs and sovereign cloud blueprints in the United Arab Emirates are helping hyperscale adoption feel more solid, and less experimental. Meanwhile edge and enterprise data centers keep growing for distributed computing needs. Edge infrastructure is expected to grow by around 16.5% because low latency applications are becoming more common and real time data processing is getting demanded across smart city environments, promoting connected use cases.

By Data Center Size

In 2025, large facilities held the leading share, close to 38% of the total market revenue due to widespread use by enterprise and colocation operators who want better capacity and operational efficiency. It is backed up further by the growing need for scalable infrastructure that supports cloud migration and enterprise digital transformation across core industries like banking, telecom, and government services.

Mega data centers are projected to grow the fastest, about 20.1% during the forecast period, driven by hyperscale cloud expansion, artificial intelligence computing needs, and a trend toward consolidating workloads into fewer but bigger plants. Massive data centers are witnessing steady growth due to ongoing investment in high-capacity infrastructure across Abu Dhabi and Dubai. Small and medium data centers still cover more localized enterprise requirements, especially where edge computing fits best.

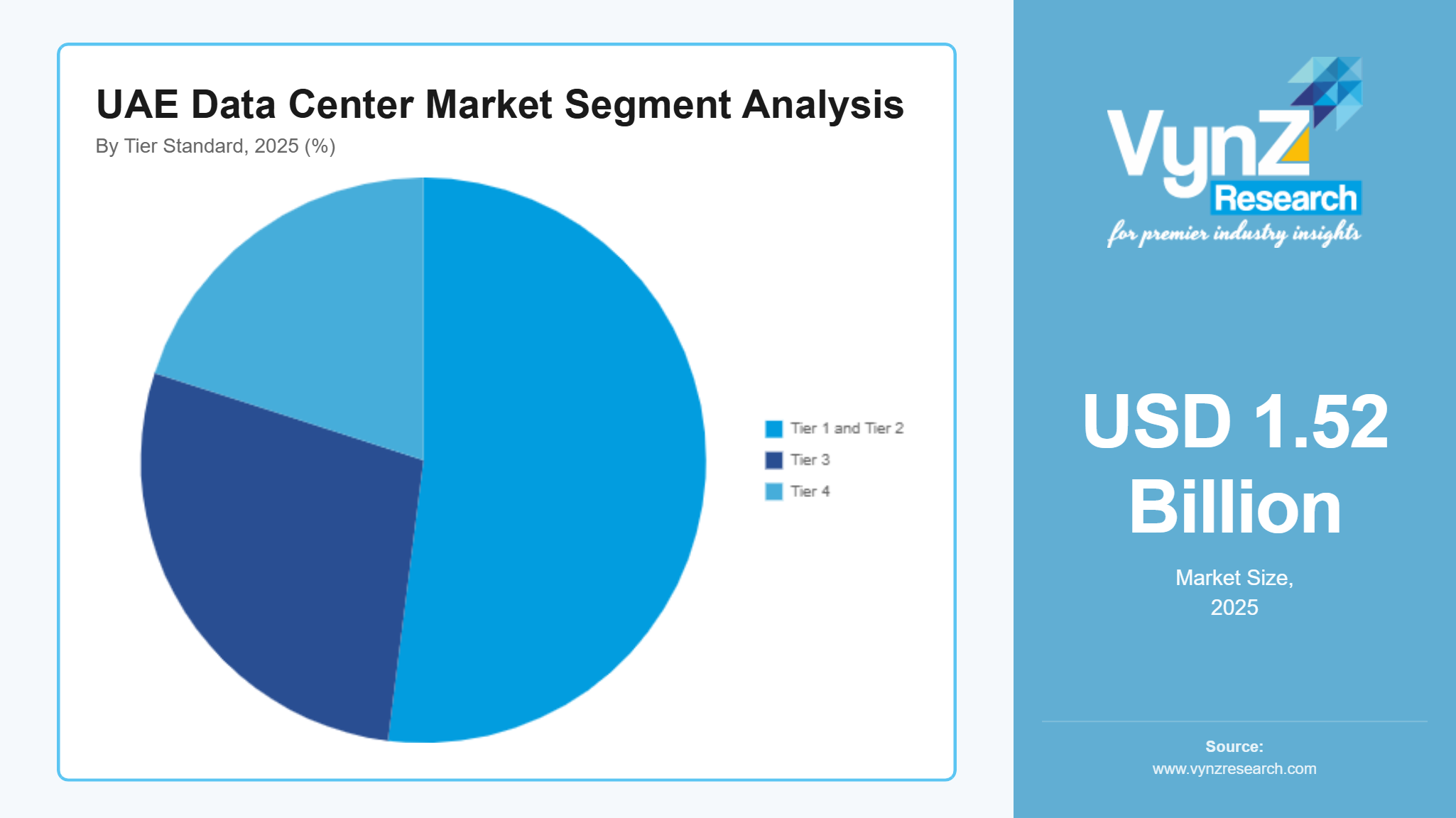

By Tier Standard

Tier 3 data centers dominated in 2025, representing around 52% of the total revenue share due to a practical balance of redundancy, cost efficiency, and high availability performance. They are widely used because BFSI, telecom, and government sectors often need dependable uptime.

Tier 4 data centers are expected to record the fastest growth rate, roughly 18.6% during the forecast period due to stronger needs for fault tolerant setups, mission critical workloads, and growing regulatory attention on data security and service continuity. Government digital transformation initiatives and sovereign cloud programs are also speeding up Tier 4 rollouts in strategic regions. Tier 1 and Tier 2 facilities, in contrast, are predicted to lose relative share because redundancy levels are limited and they don’t fit well with modern high availability requirements.

By End User

IT and ITES accounted for the largest market share in 2025, around 26% of total revenue. This was supported by strong cloud adoption, software service growth, and increasing outsourcing activities. The segment also benefits from ongoing digital transformation initiatives and a high dependency on scalable computing resources across broad enterprise ecosystems.

BFSI is expected to grow the fastest, approximately 19.4% during the forecast period due to rapid digital banking expansion, fintech integration, and rising regulatory requirements tied to secure data storage and processing. Government stays a major contributor too, fueled by large smart city initiatives, digital governance frameworks, and sovereign data localization rules. Telecom remains a crucial demand driver because 5G expansion keeps rolling, and network virtualization is scaling up. Media, healthcare, and ecommerce collectively support steady growth through higher data consumption.

Regional Insights

Dubai

Dubai accounted for approximately 42% of the market in 2025, driven by its position as the primary digital and commercial hub of the country. Strong concentration of hyperscale and colocation facilities across zones such as Dubai Internet City and Jebel Ali Free Zone continues to support large scale infrastructure deployment. Demand from financial services, ecommerce platforms, and multinational enterprises is reinforcing capacity expansion, particularly for cloud integrated and high availability environments. Government led digital economy initiatives, combined with strong enterprise digitization trends, are further strengthening investments in advanced data center infrastructure, while carrier neutral ecosystem expansion is enhancing connectivity driven growth across the region.

Abu Dhabi

Abu Dhabi accounted for approximately 29% of the market in 2025, supported by sovereign cloud programs, large scale government digital transformation initiatives, and strong investment capacity from energy backed institutions. The region is witnessing steady expansion of Tier 3 and Tier 4 facilities, driven by increasing demand for secure and resilient infrastructure across public sector, defense, and financial services. National artificial intelligence strategies and data localization policies are further accelerating adoption of high-performance computing environments, positioning Abu Dhabi as a key long term growth hub for hyperscale and government led digital infrastructure development.

Sharjah

Sharjah accounted for approximately 17% of the market in 2025, driven by gradual industrial digitization and growing demand for cost efficient colocation services. Increasing adoption of cloud-based applications among SMEs and educational institutions is contributing to steady infrastructure expansion. The region is also benefiting from improving telecom connectivity and business park development initiatives, which are encouraging localized data hosting and edge computing deployment.

Rest of United Arab Emirates

The rest of United Arab Emirates accounted for approximately 12% of the market in 2025, supported by expanding digital infrastructure development in Northern Emirates such as Ajman, Ras Al Khaimah, and Fujairah. Growth is driven by increasing edge computing requirements, telecom network expansion, and small-scale enterprise data hosting demand. Government supported digital connectivity initiatives and industrial diversification programs are encouraging gradual investment in localized data center facilities. Although the region remains relatively fragmented, ongoing infrastructure modernization and distributed workload adoption are expected to support steady long-term growth in edge and colocation capacity.

Competitive Landscape / Company Insights

The market is moderately to highly competitive with global hyperscale operators, regional colocation providers, and telecom backed infrastructure firms focusing on capacity expansion, digital transformation, and strategic partnerships. Companies are increasingly investing in advanced cooling technologies, high density computing infrastructure, and AI ready data center architectures to strengthen their market position. Government led digital economy initiatives, sovereign cloud frameworks, and data localization policies supported by national ICT and cybersecurity authorities are further shaping competitive intensity. Increasing participation from telecom operators and international cloud providers is intensifying infrastructure consolidation and long-term investment strategies across the UAE data center ecosystem.

Mini Profiles

Amazon Web Services focuses on hyperscale cloud and data center services, supported by strong global infrastructure reach, advanced scalability, and dominant presence in enterprise cloud computing and digital transformation ecosystems.

China Mobile International operates in global connectivity and telecom infrastructure segments, emphasizing high-capacity network services, international data transmission efficiency, and strong enterprise connectivity solutions across cross border digital ecosystems.

Damac Data Center focuses on large scale data center development and colocation infrastructure, supported by integrated real estate capabilities, rapid capacity expansion strategy, and strong regional digital infrastructure positioning.

Equinix operates in premium colocation and interconnection services, emphasizing carrier neutral ecosystems, high performance data exchange, and strong global enterprise connectivity across multi cloud and hybrid environments.

Etisalat (e&) focuses on telecom driven digital infrastructure and cloud services, supported by strong national network dominance, government aligned digital transformation initiatives, and expanding enterprise connectivity solutions.

Key Players

- Amazon Web Services

- China Mobile International

- Damac Data Center

- Equinix

- Etisalat (e&)

- Khazna Data Centers

- Microsoft

- NTT Global Data Centers

- Oracle

- ST Telemedia Global Data Centers

Recent Developments

In November 2025, Khazna Data Centers expanded its UAE footprint through a 200 MW capacity addition delivered in partnership with Microsoft and G42. The expansion, supported by AI-optimized infrastructure including liquid cooling systems, is scheduled to come online by the end of 2026, reinforcing Khazna’s leadership in hyperscale and sovereign cloud infrastructure development in the UAE.

In November 2025, Microsoft announced a major expansion of its UAE data center capacity through a $15.2 billion investment commitment in partnership with G42. The initiative includes a 200 MW infrastructure build delivered via Khazna Data Centers, aimed at strengthening Azure’s sovereign cloud and AI computing capabilities across the UAE digital ecosystem.

In January 2026, NTT Global Data Centers announced progress on expanding its Middle East hyperscale footprint, focusing on scaling AI-ready infrastructure and energy-efficient colocation facilities. The company emphasized increasing demand for enterprise cloud migration and low-latency interconnection services, aligning its regional strategy with accelerating digital transformation in GCC markets.

In December 2025, Oracle expanded its cloud infrastructure investment program across the Middle East, enhancing OCI availability zones to support sovereign cloud adoption and enterprise workload migration. The initiative focuses on strengthening regulated industry adoption, particularly within finance and government sectors requiring high compliance and secure data residency frameworks.

In October 2025, ST Telemedia Global Data Centers advanced its regional expansion strategy by increasing hyperscale capacity investments across Asia and the Middle East. The company highlighted growing demand for AI-ready infrastructure and scalable colocation services, reinforcing its long-term strategy of building high-density, sustainable data center ecosystems for enterprise and cloud clients.

UAE Data Center Market Coverage

Data Center Type Insight and Forecast 2026 - 2035

- Hyperscale Data Centers

- Colocation Data Centers

- Enterprise Data Centers

- Edge Data Centers

Data Center Size Insight and Forecast 2026 - 2035

- Small Data Centers

- Medium Data Centers

- Large Data Centers

- Massive Data Centers

- Mega Data Centers

Tier Standard Insight and Forecast 2026 - 2035

- Tier 1 and Tier 2

- Tier 3

- Tier 4

End User Insight and Forecast 2026 - 2035

- IT and ITES

- BFSI

- Government

- E commerce

- Manufacturing

- Media and Entertainment

- Telecom

- Healthcare

- Other End Users

Region Insight and Forecast 2026 - 2035

- Dubai

- Abu Dhabi

- Sharjah

- Rest of United Arab Emirates

UAE Data Center Market by Region

- Dubai

- By Data Center Type

- By Data Center Size

- By Tier Standard

- By End User

- By Region

- Abu Dhabi

- By Data Center Type

- By Data Center Size

- By Tier Standard

- By End User

- By Region

- Sharjah

- By Data Center Type

- By Data Center Size

- By Tier Standard

- By End User

- By Region

- Rest of United Arab Emirates

- By Data Center Type

- By Data Center Size

- By Tier Standard

- By End User

- By Region

Table of Contents for UAE Data Center Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Data Center Type

1.2.2. By

Data Center Size

1.2.3. By

Tier Standard

1.2.4. By

End User

1.2.5. By

Region

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. UAE Market Estimate and Forecast

4.1. UAE Market Overview

4.2. UAE Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Data Center Type

5.1.1. Hyperscale Data Centers

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Colocation Data Centers

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Enterprise Data Centers

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Edge Data Centers

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.2. By Data Center Size

5.2.1. Small Data Centers

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Medium Data Centers

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Large Data Centers

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Massive Data Centers

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. Mega Data Centers

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.3. By Tier Standard

5.3.1. Tier 1 and Tier 2

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Tier 3

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Tier 4

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.4. By End User

5.4.1. IT and ITES

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. BFSI

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Government

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. E commerce

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Manufacturing

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

5.4.6. Media and Entertainment

5.4.6.1. Market Definition

5.4.6.2. Market Estimation and Forecast to 2035

5.4.7. Telecom

5.4.7.1. Market Definition

5.4.7.2. Market Estimation and Forecast to 2035

5.4.8. Healthcare

5.4.8.1. Market Definition

5.4.8.2. Market Estimation and Forecast to 2035

5.4.9. Other End Users

5.4.9.1. Market Definition

5.4.9.2. Market Estimation and Forecast to 2035

5.5. By Region

5.5.1. Dubai

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Abu Dhabi

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Sharjah

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Rest of United Arab Emirates

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

6. Dubai Market Estimate and Forecast

6.1. By

Data Center Type

6.2. By

Data Center Size

6.3. By

Tier Standard

6.4. By

End User

6.5. By

Region

7. Abu Dhabi Market Estimate and Forecast

7.1. By

Data Center Type

7.2. By

Data Center Size

7.3. By

Tier Standard

7.4. By

End User

7.5. By

Region

8. Sharjah Market Estimate and Forecast

8.1. By

Data Center Type

8.2. By

Data Center Size

8.3. By

Tier Standard

8.4. By

End User

8.5. By

Region

9. Rest of United Arab Emirates Market Estimate and Forecast

9.1. By

Data Center Type

9.2. By

Data Center Size

9.3. By

Tier Standard

9.4. By

End User

9.5. By

Region

10. Company Profiles

10.1.

Amazon Web Services

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

China Mobile International

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Damac Data Centers

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Equinix

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Etisalat (e&)

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Khazna Data Centers

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Microsoft

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

NTT Global Data Centers

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Oracle

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

ST Telemedia Global Data Centres

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

UAE Data Center Market