UAE Liquid Cooling Data Center Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Cooling Type (Air Cooling, Liquid Cooling, Hybrid Cooling Systems), by Cooling Technology (Direct-to-Chip Cooling, Immersion Cooling, Rear Door Heat Exchanger, In-Row Cooling, Evaporative Cooling, Chilled Water Cooling), by Component (Cooling Units, Chillers, Pumps, Heat Exchangers, CDU Systems, Air Handling Units, Monitoring and Control Systems), by Data Center Type (Hyperscale Data Centers, Colocation Data Centers, Enterprise Data Centers, Edge Data Centers), by End User (Cloud Sere Providers, Colocation Providers, BFSI, IT and Telecom, Govervicnment, Healthcare, Manufacturing, Energy and Utilities), by Region (Dubai, Abu Dhabi, Sharjah, Rest of UAE)

| Status : Published | Published On : May, 2026 | Report Code : VRSME9219 | Industry : Semiconductor & Electronics | Available Format :

|

Page : 121 |

UAE Liquid Cooling Data Center Market Overview

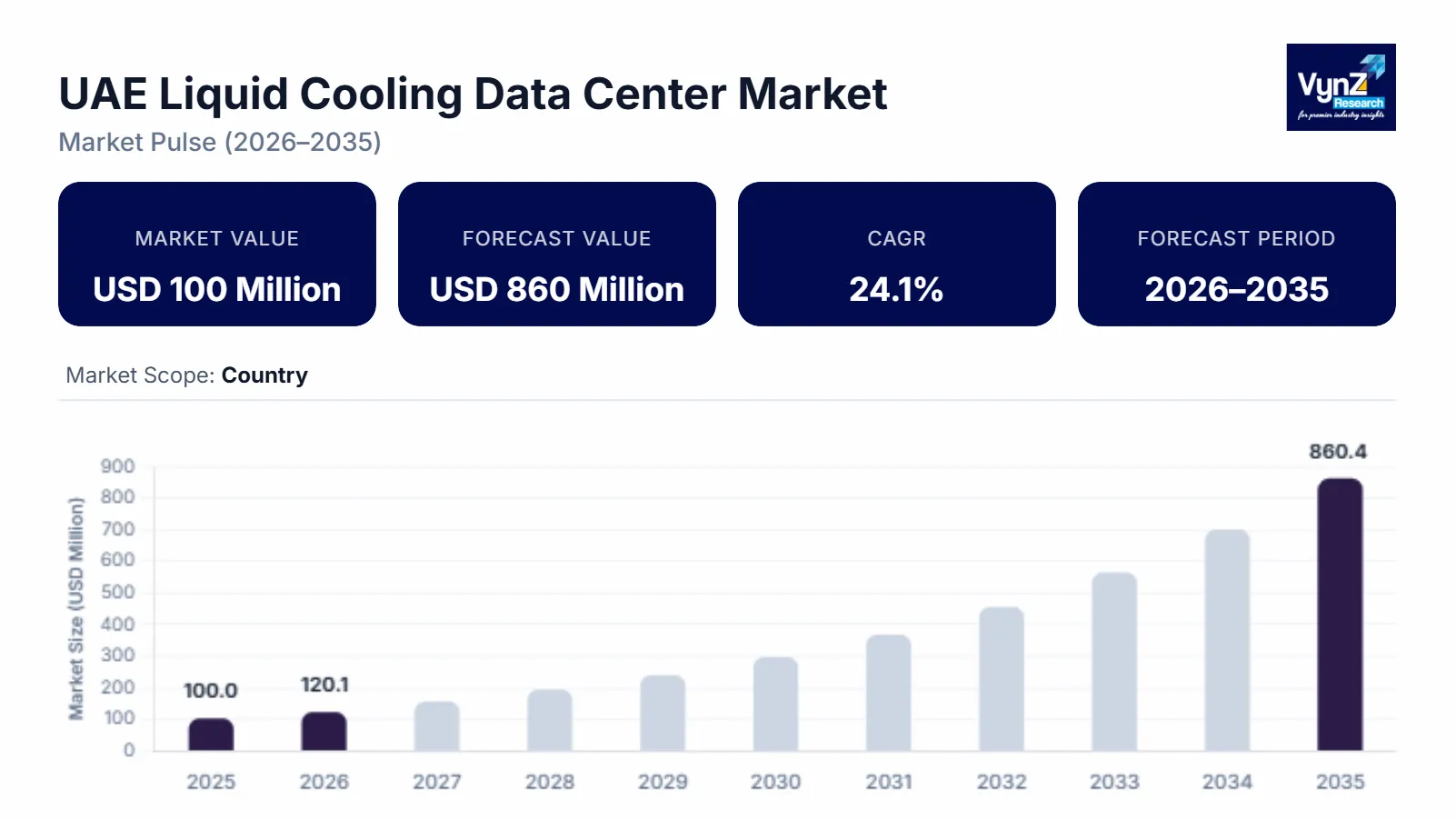

The UAE liquid cooling data center market which was valued at approximately USD 100 million in 2025 and is estimated to reach around USD 120 million in 2026, is projected to reach approximately USD 860 million by 2035, expanding at a CAGR of about 24.1% during the forecast period from 2026 to 2035.

Market growth is mostly driven by the rising deployment of hyperscale facilities where more artificial intelligence and high-performance computing workloads are showing up and a growing demand for energy efficient thermal control solutions across today’s data center setup. Adoption of immersion cooling and direct to chip cooling technologies is also getting faster and that is helping the whole market expand, especially across Dubai, Abu Dhabi, and Sharjah.

Government-backed digital transformation drives along with steady investments into advanced ICT infrastructure are giving the industry extra momentum across the UAE. National efforts related to artificial intelligence adoption smart city development and cloud ecosystem improvements are helping boost demand for high density computing spaces which then pushes operators toward advanced liquid cooling systems. Sustainability strategies that focus on energy efficiency and lower carbon emissions are encouraging data center teams to use the next wave cooling technologies with lower power consumption and better operational efficiency.

UAE Liquid Cooling Data Center Market Dynamics

Market Trends

In the industry, cooling technology adoption is moving toward more energy optimizing approaches and high-density computing setups. A main trend is the bigger acceptance of immersion cooling and direct to chip liquid cooling systems which shows a stronger interest toward energy efficient thermal management and lower latency for AI work and hyperscale workloads. There is more attention on power usage effectiveness and backing more sustainable digital infrastructure. There’s also an emerging move toward AI ready data center architecture partly because cloud deployment keeps expanding and national digital transformation initiatives keep rolling forward. Government supported smart infrastructure programs and sustainability frameworks are pushing operators to put money into advanced cooling ecosystems, with better efficiency and lower carbon emissions.

Growth Drivers

The growth of the market is mostly supported by new and continued investments in hyperscale data center infrastructure. This keeps feeding demand across cloud computing, colocation, and enterprise applications. AI workloads keep expanding, data traffic is rising, and high-performance computing systems are being rolled out. All those factors together are driving demand for advanced liquid cooling technologies in big commercial hubs, like Dubai and Abu Dhabi. Government backed digital economy initiatives matter a lot for industry expansion. National strategies that focus on artificial intelligence adoption, smart city infrastructure, and cloud ecosystem development are encouraging enterprises to build energy efficient data center environments with higher density capabilities. Since operators are increasingly prioritizing energy efficiency, operational steadiness, and longer-term sustainability compliance, the demand for advanced liquid cooling systems should stay strong during the forecast window.

Market Restraints / Challenges

Even with good growth signs, the market has obstacles that can slow wider rollout. First, high initial installation costs and the complexity of changing existing setups still slow adoption, especially for small to mid-sized operators that have limited capital to invest. Also, bringing liquid cooling systems into facilities that were originally air cooled requires meaningful redesign and operational tuning, which adds more financial pressure for site owners. Additionally, there is a reliance on imported cooling technologies and specialized engineering know how. This can become an operational pain point for infrastructure developers and service providers.

Market Opportunities

The market has real chances for growth mainly in AI oriented infrastructure development. This is being encouraged by expanding deployments of generative AI platforms, machine learning applications, and high-density server environments. Vendors that provide scalable immersion cooling plus direct liquid cooling options are in a solid position to benefit as hyperscale operators, colocation providers, and government backed digital infrastructure projects increase spending. Another opportunity comes from sustainable data center modernization. With more investments going toward energy-efficient, environmentally optimized infrastructure, there are pathways for ongoing revenue growth. National sustainability targets and green building initiatives are motivating operators to adopt cooling solutions that use less energy and reduce water usage. Progress in automated monitoring systems, intelligent thermal optimization, and modular cooling architecture is expected to lift operational performance and make customers more comfortable adopting these systems across the UAE market.

UAE Liquid Cooling Data Center Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 100 Million |

|

Revenue Forecast in 2035 |

USD 860 Million |

|

Growth Rate |

24.1% |

|

Segments Covered in the Report |

Cooling Type, Cooling Technology, Component, Data Center Type, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

Dubai, Abu Dhabi, Sharjah, Rest of UAE |

|

Key Companies |

Alfa Laval, Asetek, CoolIT Systems, Dell Technologies, Fujitsu, Hitachi, Iceotope, Schneider Electric, STULZ, Vertiv |

|

Customization |

Available upon request |

UAE Liquid Cooling Data Center Market Segmentation

By Cooling Type

Air cooling held the biggest share of the market in 2025, roughly 46% of total segment revenue as it is used widely across classic enterprise and colocation setups. It fits into the existing infrastructure and the whole installation is generally not too complicated. Many data center operators depend on air based thermal management systems for moderate density workloads and there is a comfort factor since teams already know how to run them.

Liquid cooling systems are expected to post the fastest expansion over the forecast window with an estimated CAGR of 25.8% between 2026 and 2035 as AI infrastructure keeps being deployed more, hyperscale computing keeps growing, and high-density server racks are becoming common due to better thermal efficiency. There is also a stronger push toward energy optimization, lower PUE, and sustainable infrastructure deployment, so direct liquid cooling and immersion approaches are gaining traction in next generation facilities. Hybrid cooling systems are staying on a steady upward path with demand growth around 19.6%, supported by gradual modernization of older data center environments.

By Cooling Technology

Direct to chip cooling held the largest share of the market in 2025, contributing about 34% of total technology revenue because more operators are deploying it in AI centered computing clusters and also in hyperscale server environments where heat has to be handled with accuracy. Adoption of high-performance processors and graphics processing units is pushing operators to move toward advanced direct cooling because it tends to support better energy efficiency and stronger operational reliability. National sustainability frameworks that emphasize energy optimized infrastructure are giving additional support for wider segment growth across more advanced commercial data centers.

Immersion cooling is projected to deliver the fastest growth during the forecast period with an estimated CAGR of 27.3% from 2026 to 2035. The growth story is tied to demand for ultra-high density computing infrastructure and increasing investments in AI driven data processing facilities. Operators are also selecting immersion systems more often to reduce cooling energy consumption and boost overall server efficiency, especially in places where space is tight and constraints are real.

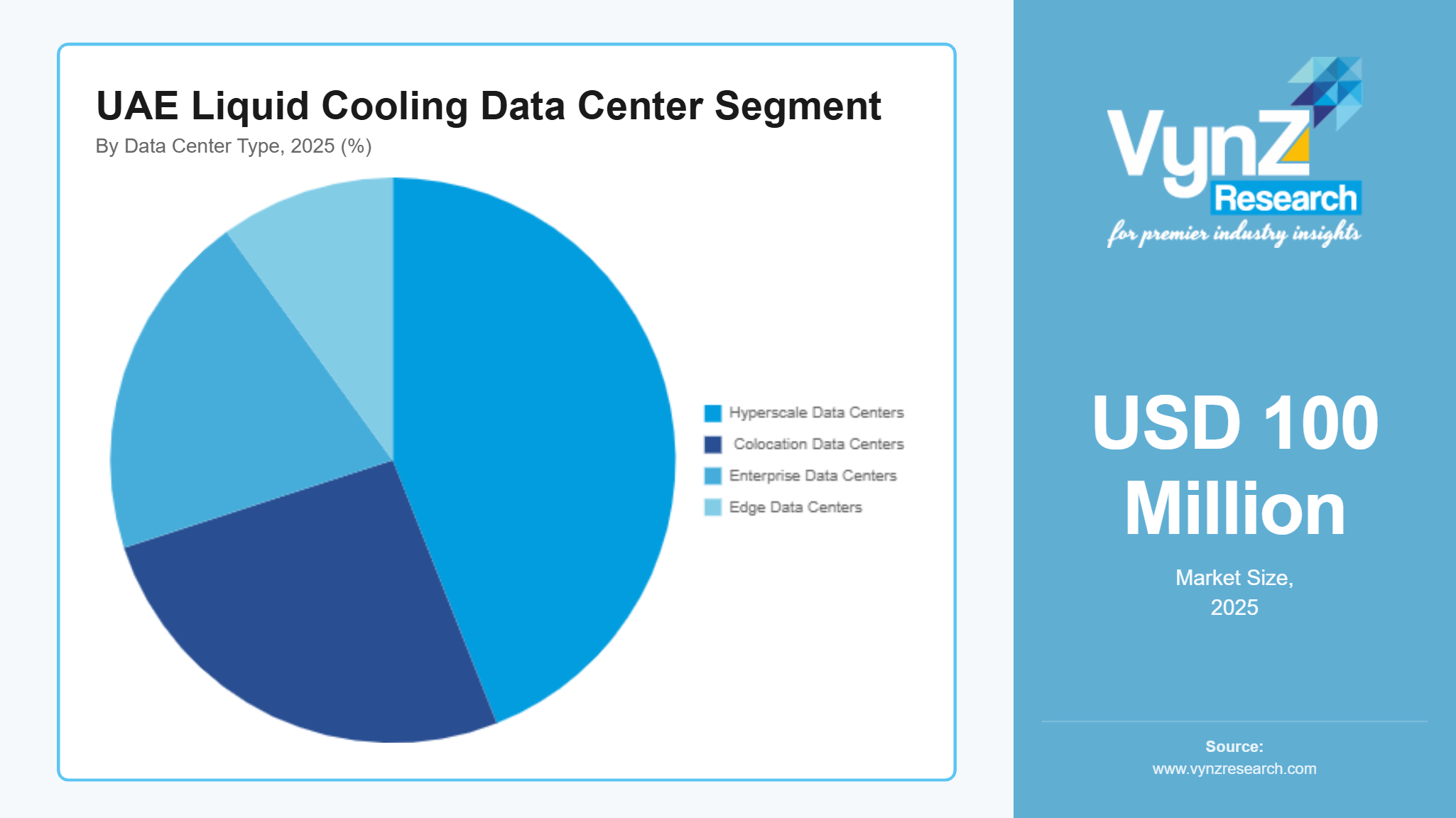

By Data Center Type

Hyperscale data centers accounted for the largest share of the market in 2025, representing approximately 44% of total segment revenue. Their leadership is supported by bigger investments from cloud service providers, more deployment of AI computing infrastructure, and the continuing expansion of regional digital ecosystems. Since large scale facilities need advanced cooling systems that can manage high rack density and continuous performance, liquid based thermal management technologies are being rolled out faster. Government supported digital transformation and smart city programs are also reinforcing demand for hyperscale infrastructure in Dubai and Abu Dhabi.

Edge data centers are expected to grow the fastest during the forecast period with an estimated CAGR of 26.1% from 2026 to 2035 due to increasing rollout of low latency applications, IoT ecosystems, and real time analytics infrastructure, which is pushing localized processing facilities to expand more quickly. Colocation data centers are also growing strongly, around 23.4%, mainly because enterprises are outsourcing more and want scalable, energy efficient infrastructure.

By End User

Cloud service providers accounted for the largest share of the UAE liquid cooling data center market in 2025, contributing approximately 39% of total market revenue. Ongoing demand for cloud storage, AI computing platforms, and digital enterprise applications continues to support infrastructure expansion, particularly across hyperscale facilities. Big investments in regional cloud zones and smart infrastructure development are encouraging deployment of advanced liquid cooling technologies that can handle high density workloads while maintaining optimized energy performance. Government initiatives promoting cloud first strategies and digital economy development are further strengthening demand across large scale commercial environments, without slowing down.

IT and telecom operators are expected to witness the fastest growth during the forecast period with an estimated CAGR of 25.5% from 2026 to 2035. Expansion of 5G infrastructure, rising data traffic, and more edge computing deployments are all accelerating the need for efficient thermal management systems. Colocation providers are seeing notable growth of about 24.2%, supported by increasing enterprise outsourcing and additional regional connectivity investments. Government, healthcare, manufacturing, BFSI, and energy sectors continue to adopt advanced cooling infrastructure as they need secure data processing, operational continuity, and compliance with national digital transformation goals.

Regional Insights

Dubai

Dubai accounted for approximately 36% of the market in 2025 driven by strong hyperscale investments, expanding cloud infrastructure, and rapid deployment of AI enabled computing facilities. The emirate continues to serve as the primary digital infrastructure hub within the UAE, supported by large scale commercial developments and increasing enterprise demand for high density data processing environments. Major technology corridors and free economic zones are further encouraging adoption of advanced liquid cooling systems across colocation and cloud facilities.

Abu Dhabi

Abu Dhabi contributed approximately 26% of the market in 2025. The regional market is witnessing steady growth due to increasing government backed digital transformation initiatives, rising enterprise cloud adoption, and expanding investments in sovereign digital infrastructure projects. Growing deployment of AI platforms and advanced analytics solutions across government and energy sectors continues to generate demand for high performance cooling systems.

Sharjah

Sharjah represented approximately 18% of the market in 2025, supported by increasing industrial digitization, infrastructure modernization, and growing investments in enterprise connectivity solutions. Expansion of manufacturing and logistics operations across the emirate is creating rising demand for localized data processing and efficient cooling infrastructure. Educational and research institutions are also contributing to increasing adoption of high-performance computing systems requiring advanced thermal management capabilities.

Rest of UAE

The remaining regions including Ajman, Ras Al Khaimah, Fujairah, and Umm Al Quwain collectively accounted for approximately 20% of the market in 2025. Growth across these regions is supported by gradual expansion of enterprise infrastructure, increasing cloud service penetration, and rising adoption of digital government platforms. Emerging investments in edge computing and localized data storage facilities are further supporting demand for compact and energy efficient cooling technologies.

Competitive Landscape / Company Insights

The market is moderately competitive with the presence of international cooling technology providers, infrastructure specialists, and regional data center operators focusing on energy efficient thermal management solutions. Companies are increasingly investing in advanced liquid cooling technologies, AI ready infrastructure capabilities, and sustainable cooling innovation to strengthen market positioning. Strategic partnerships with hyperscale cloud providers and colocation operators are further supporting competitive expansion. Government backed digital transformation initiatives and sustainability programs are also encouraging technology modernization and infrastructure investments across the UAE data center ecosystem.

Mini Profiles

Alfa Laval focuses on advanced thermal management and liquid cooling solutions, supported by strong industrial expertise, energy efficient technologies, and extensive global infrastructure deployment capabilities across high performance computing environments.

CoolIT Systems operates in specialized liquid cooling segments, emphasizing high density server cooling, advanced direct liquid cooling technologies, and customized thermal management systems for hyperscale and AI driven facilities.

Dell Technologies leverages enterprise infrastructure expertise, strategic cloud partnerships, and integrated digital capabilities to strengthen its presence in advanced data center and high-performance computing ecosystems globally.

Fujitsu focuses on energy efficient data center infrastructure and cooling optimization technologies, supported by strong research capabilities, sustainable digital transformation initiatives, and long-standing enterprise technology partnerships.

Hitachi operates across industrial and digital infrastructure segments, emphasizing advanced cooling innovation, operational reliability, and scalable thermal management solutions for enterprise and hyperscale computing facilities.

Key Players

- Alfa Laval

- Asetek

- CoolIT Systems

- Dell Technologies

- Fujitsu

- Hitachi

- Iceotope

- Schneider Electric

- STULZ

- Vertiv

Recent Developments

In February 2025, Vertiv launched its global liquid cooling services portfolio designed for AI and high-density computing environments. The company further expanded its CoolChip CDU portfolio in June 2025 to support scalable liquid cooling deployment across hyperscale data centers.

In March 2025, Schneider Electric expanded its AI focused data center infrastructure initiatives with increased emphasis on sustainable liquid cooling integration. The company continued strengthening partnerships for energy efficient cooling and high-density computing solutions across hyperscale environments.

In May 2026, Iceotope secured USD 26 million in Series B funding to accelerate precision liquid cooling technology expansion for AI infrastructure applications. The company also expanded its patent portfolio and ecosystem partnerships supporting next generation thermal management innovation.

In May 2024, STULZ introduced its CyberCool CMU coolant distribution unit designed to maximize heat exchange efficiency within liquid cooling environments. The launch focused on supporting growing AI and machine learning workloads requiring higher rack density cooling capabilities.

In 2025, Asetek continued expanding its liquid cooling technology portfolio for high performance computing and AI server applications. The company increased focus on energy efficient cooling architectures and advanced thermal optimization solutions for modern data center environments.

UAE Liquid Cooling Data Center Market Coverage

Cooling Type Insight and Forecast 2026 - 2035

- Air Cooling

- Liquid Cooling

- Hybrid Cooling Systems

Cooling Technology Insight and Forecast 2026 - 2035

- Direct-to-Chip Cooling

- Immersion Cooling

- Rear Door Heat Exchanger

- In-Row Cooling

- Evaporative Cooling

- Chilled Water Cooling

Component Insight and Forecast 2026 - 2035

- Cooling Units

- Chillers

- Pumps

- Heat Exchangers

- CDU Systems

- Air Handling Units

- Monitoring and Control Systems

Data Center Type Insight and Forecast 2026 - 2035

- Hyperscale Data Centers

- Colocation Data Centers

- Enterprise Data Centers

- Edge Data Centers

End User Insight and Forecast 2026 - 2035

- Cloud Service Providers

- Colocation Providers

- BFSI

- IT and Telecom

- Government

- Healthcare

- Manufacturing

- Energy and Utilities

Region Insight and Forecast 2026 - 2035

- Dubai

- Abu Dhabi

- Sharjah

- Rest of UAE

UAE Liquid Cooling Data Center Market by Region

- Dubai

- By Cooling Type

- By Cooling Technology

- By Component

- By Data Center Type

- By End User

- By Region

- Abu Dhabi

- By Cooling Type

- By Cooling Technology

- By Component

- By Data Center Type

- By End User

- By Region

- Sharjah

- By Cooling Type

- By Cooling Technology

- By Component

- By Data Center Type

- By End User

- By Region

- Rest of UAE

- By Cooling Type

- By Cooling Technology

- By Component

- By Data Center Type

- By End User

- By Region

Table of Contents for UAE Liquid Cooling Data Center Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Cooling Type

1.2.2. By

Cooling Technology

1.2.3. By

Component

1.2.4. By

Data Center Type

1.2.5. By

End User

1.2.6. By

Region

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. UAE Market Estimate and Forecast

4.1. UAE Market Overview

4.2. UAE Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Cooling Type

5.1.1. Air Cooling

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Liquid Cooling

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Hybrid Cooling Systems

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Cooling Technology

5.2.1. Direct-to-Chip Cooling

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Immersion Cooling

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Rear Door Heat Exchanger

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. In-Row Cooling

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. Evaporative Cooling

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.2.6. Chilled Water Cooling

5.2.6.1. Market Definition

5.2.6.2. Market Estimation and Forecast to 2035

5.3. By Component

5.3.1. Cooling Units

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Chillers

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Pumps

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Heat Exchangers

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. CDU Systems

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.3.6. Air Handling Units

5.3.6.1. Market Definition

5.3.6.2. Market Estimation and Forecast to 2035

5.3.7. Monitoring and Control Systems

5.3.7.1. Market Definition

5.3.7.2. Market Estimation and Forecast to 2035

5.4. By Data Center Type

5.4.1. Hyperscale Data Centers

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Colocation Data Centers

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Enterprise Data Centers

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Edge Data Centers

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.5. By End User

5.5.1. Cloud Service Providers

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Colocation Providers

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. BFSI

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. IT and Telecom

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

5.5.5. Government

5.5.5.1. Market Definition

5.5.5.2. Market Estimation and Forecast to 2035

5.5.6. Healthcare

5.5.6.1. Market Definition

5.5.6.2. Market Estimation and Forecast to 2035

5.5.7. Manufacturing

5.5.7.1. Market Definition

5.5.7.2. Market Estimation and Forecast to 2035

5.5.8. Energy and Utilities

5.5.8.1. Market Definition

5.5.8.2. Market Estimation and Forecast to 2035

5.6. By Region

5.6.1. Dubai

5.6.1.1. Market Definition

5.6.1.2. Market Estimation and Forecast to 2035

5.6.2. Abu Dhabi

5.6.2.1. Market Definition

5.6.2.2. Market Estimation and Forecast to 2035

5.6.3. Sharjah

5.6.3.1. Market Definition

5.6.3.2. Market Estimation and Forecast to 2035

5.6.4. Rest of UAE

5.6.4.1. Market Definition

5.6.4.2. Market Estimation and Forecast to 2035

6. Dubai Market Estimate and Forecast

6.1. By

Cooling Type

6.2. By

Cooling Technology

6.3. By

Component

6.4. By

Data Center Type

6.5. By

End User

6.6. By

Region

7. Abu Dhabi Market Estimate and Forecast

7.1. By

Cooling Type

7.2. By

Cooling Technology

7.3. By

Component

7.4. By

Data Center Type

7.5. By

End User

7.6. By

Region

8. Sharjah Market Estimate and Forecast

8.1. By

Cooling Type

8.2. By

Cooling Technology

8.3. By

Component

8.4. By

Data Center Type

8.5. By

End User

8.6. By

Region

9. Rest of UAE Market Estimate and Forecast

9.1. By

Cooling Type

9.2. By

Cooling Technology

9.3. By

Component

9.4. By

Data Center Type

9.5. By

End User

9.6. By

Region

10. Company Profiles

10.1.

Alfa Laval

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Asetek

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

CoolIT Systems

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Dell Technologies

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Fujitsu

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Hitachi

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Iceotope

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Schneider Electric

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

STULZ

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Vertiv

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

UAE Liquid Cooling Data Center Market