Europe Electric Bus Charging Station Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Charging Type (Depot Charging, Opportunity Charging, Inductive Charging), Charger Category (Off-Board Chargers, On-Board Chargers), Power Output (<50 kW, 50–150 kW, 151–450 kW, 450 kW), End User (Public Transit, Private Fleets)

| Status : Published | Published On : Mar, 2026 | Report Code : VRSME9197 | Industry : Semiconductor & Electronics | Available Format :

|

Page : 145 |

Europe Electric Bus Charging Station Market Overview

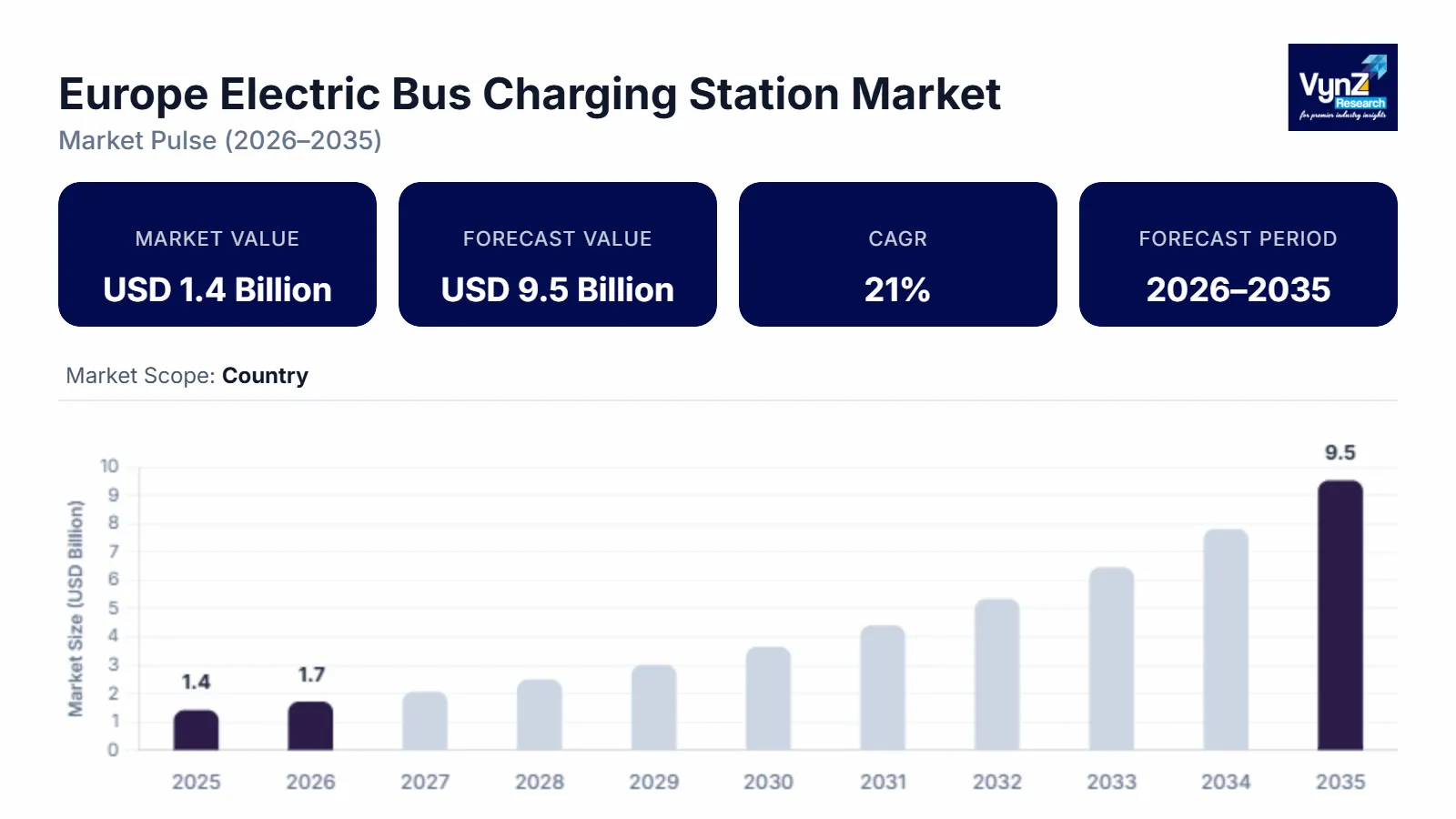

The Europe Electric Bus Charging Station market, which was valued at approximately USD 1.4 billion in 2025 and is estimated to rise further up to almost USD 1.7 billion by 2026, is projected to reach around USD 9.5 billion in 2035, expanding at a CAGR of about 21% during the forecast period 2026 to 2035.

The European Green Deal establishes strict decarbonization mandates which drive market expansion together with municipal transit systems switching to zero-emission vehicles and the development of high-power DC charging technologies which automated pantograph and megawatt charging systems. The market expansion in Germany, France and the United Kingdom benefits from rising needs for charging networks which can operate across different systems and from current European Union infrastructure funding initiatives which include the Alternative Fuels Infrastructure Regulation (AFIR) and the Connecting Europe Facility (CEF).

The European Alternative Fuels Observatory (EAFO) and the European Commission expects that there will be more than 1 million charging points installed across the region by 2025. The European Automobile Manufacturers' Association (ACEA) data indicates 10x charging capacity expansion in heavy-duty sector by 2030 in order to satisfy the restructured CO2 emission standards for heavy-duty vehicles.

Europe Electric Bus Charging Station Market Dynamics

Market Trends

The sector shows significant technological shifts which influence both its technology selection and purchasing processes. The market experiences its most significant change through the implementation of standardized high-power charging interfaces which enable better cost-efficient operation across various vendor fleets. The International Association of Public Transport (UITP) reports that municipal operators experience decreased proprietary "lock-in" risks through their transition to open-interface standards which include Opp Charge and CCS2 for pantographs and depots respectively.

The EU Digitalization of Energy Action Plan drives technological progress which leads to the adoption of AI-based energy management systems for organizations. Companies need to develop smart load balancing and predictive maintenance solutions because market changes from product offering developments. The European Alternative Fuels Observatory (EAFO) reports that all new infrastructure must adhere to the DATEX II standard by April 2026 which requires stations to provide real-time data about their operational status and power accessibility.

Growth Drivers

The market expands because municipal public transit networks require decarbonization mandates which create constant demand for charging stations. The Clean Vehicles Directive establishes public procurement targets which will increase to zero-emission buses between 33% and 66% between 2026 and 2030 thus requiring a twofold expansion of existing charging stations. The German government allocates €1.9 billion to its charging initiative while the UK provides £1.3 billion in funding which drives market growth through increased national infrastructure program investments.

Technological advancements in ultra-fast charging technology drive higher market acceptance. The demand for high-power DC chargers (above 150 kW) will continue strong because transit agencies and private fleet operators value performance and Alternative Fuels Infrastructure Regulation (AFIR) compliance. As the European Automobile Manufacturers' Association (ACEA) states, infrastructure deployment needs to multiply eight times by 2030 to match vehicle introduction rates which maintain investment continuity.

Market Restraints / Challenges

The market needs to address particular challenges which limit its growth despite available expansion opportunities. High initial capital expenditure (CAPEX) requirements which include grid upgrade expenses and land acquisition costs continue to diminish profitability for budget-constrained municipalities and smaller private operators. The costs to install a single high-power depot station range from USD 10,000 to USD 50,000 while excluding all hardware costs according to industry data.

Manufacturers and suppliers face operational difficulties because grid capacity restrictions. Local transformer upgrades and external energy grid readiness serve as two main factors which cause delivery delays and scalability problems that reduce market performance during fleet expansion. The European Environment Agency (EEA) has determined that various Eastern and Southern European regions need substantial electrical infrastructure upgrades to accommodate 100% electric bus depot high-load charging.

Market Opportunities

The market provides substantial prospects for bi-directional charging and Vehicle-to-Grid (V2G) integration because technological developments and grid stability requirements create demand. Companies which provide high-performance bidirectional solutions can obtain market share through operators who want to use bus batteries as mobile energy storage units. Smart flexibility from EV assets will help European grid operators save up to €4 billion each year through enhanced renewable energy optimization.

Charging-as-a-Service (CaaS) models present another key market opportunity because digital-enabled premium offerings attract business investments which develop enduring client partnerships. Customers will experience better service through ISO 15118-compliant "Plug and Charge" protocols and automated payment systems which will also help businesses increase their operational conversion rates. The EU believes that charging point needs along core corridors require a charging point every 60 km which creates a market demand for modular scalable multi-standard charging hubs that offer high-margin outcomes to market leaders.

Europe Electric Bus Charging Station Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 1.4 Billion |

|

Revenue Forecast in 2035 |

USD 9.5 Billion |

|

Growth Rate |

21% |

|

Segments Covered in the Report |

Charging Type, Charger Category, Power Output, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

Western Europe, Southern Europe, Eastern Europe, Northern & Central Europe |

|

Key Companies |

ABB Ltd., Alstom SA, BYD Motors Inc., ChargePoint Inc., Efacec Power Solutions SGPS S.A., Ekoenergetyka-Polska Sp. z o.o., JEMA Energy S.A., Kempower Oyj, Siemens AG, Solaris Bus & Coach sp. z o.o. |

|

Customization |

Available upon request |

Europe Electric Bus Charging Station Market Segmentation

By Charging Type

The market share of depot charging reached its peak in 2025 when the segment generated approximately 60% of total industry revenue. Municipalities have implemented overnight charging cycles with high frequency which enables them to use economical electricity rates during non-peak times thereby keeping their entire fleet available for the morning deployments. The 14.8% CAGR forecast for depot installations until 2035 supports this segment because cities now focus on establishing centralized infrastructure to replicate traditional fuel distribution systems.

Fixed depot stations serve as the preferred option for large fleet conversions because they offer dependable service at lower operational demands compared to high-power on-route systems. Report shows that dedicated bus depots currently house almost 62% of existing charging stations in Europe which establishes this segment as the foundation of the market.

By Power Output

The <50 kW category held the largest market share in 2025, accounting for approximately 48.5% of the industry revenue. The extensive deployment of this technology in overnight depot charging applications has made it the primary choice for municipal transit authorities who need to transition their systems to accommodate large-scale fleets.

The >450 kW segment represents the market segment which has reached its highest growth rate because it will attain a 15.5% CAGR until 2035. The increasing demand for "ultra-fast" opportunity charging at terminal layovers drives this growth because buses need substantial power within a 10-minute window to keep up their urban service frequency. The European Alternative Fuels Observatory (EAFO) reports that chargers with more than 350 kW capacity have seen their installation rate double because transportation agencies now need megawatt-ready systems to remove range anxiety from heavy-duty transit.

By Charger Category

The off-board charger segment dominated the market in 2025 when it achieved approximately 75% market share through its superiority in both volume and revenue generation. The technology needs to deliver high DC power directly to the bus battery system which creates a requirement for direct power delivery because vehicle-integrated converters limits both weight and space capacity. Off-board systems hold strategic value because they permit central locations to achieve better operational efficiency while enabling simple maintenance procedures for their power electronics systems.

The on-board segment will experience sustained growth because it finds most applications in smaller regional and school bus systems which lack the need for extensive infrastructure. The market value derives principally from the off-board category which will achieve a 14.3% CAGR through 2035. The segment capitalizes on the modular power cabinets trend which enables transit agencies to expand their charging capacity as they acquire additional electric buses, providing a non-risky approach to complete electrification of their operations.

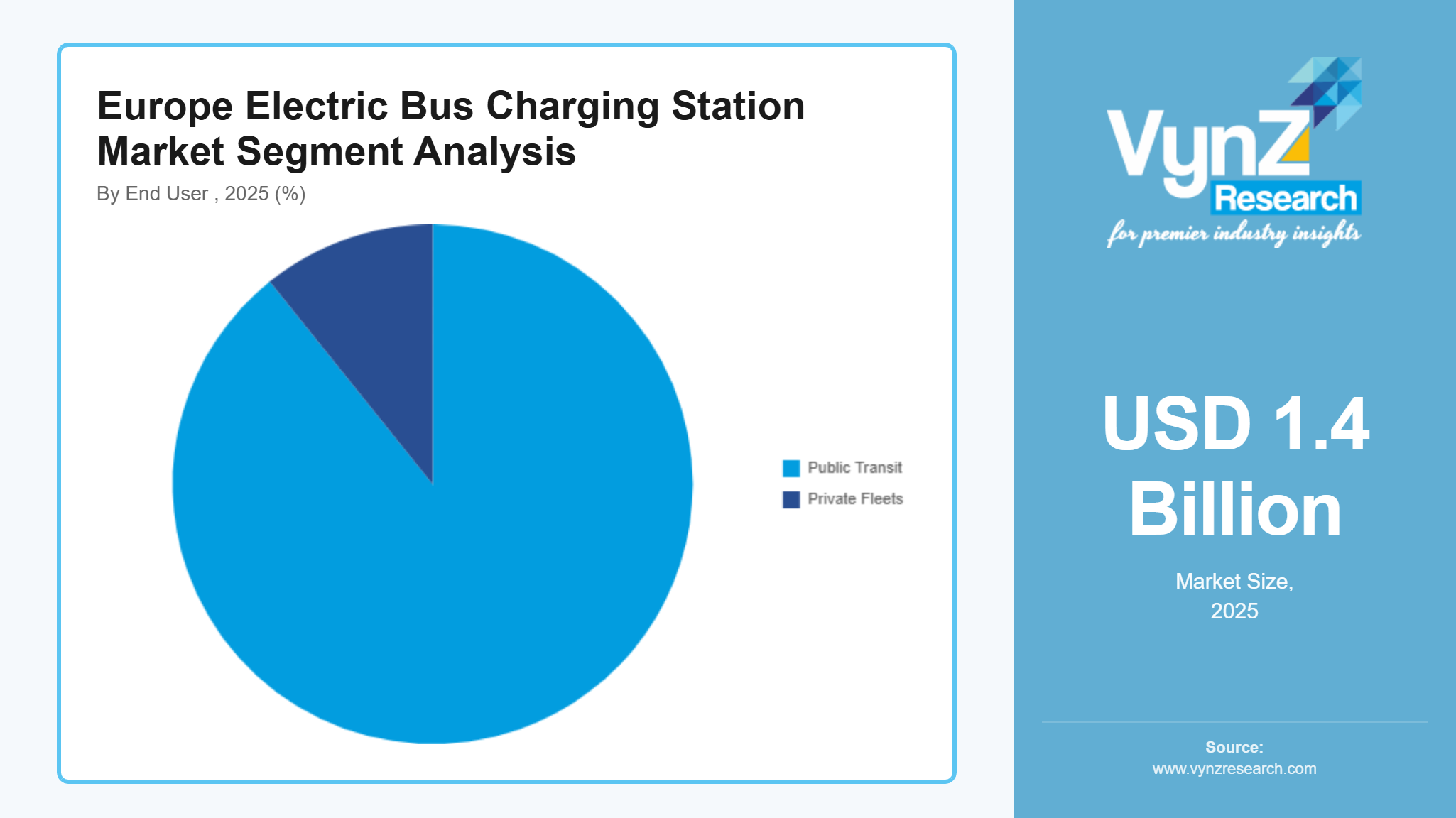

By End User

The Public Transit segment accounted for the largest market share in 2025, holding a commanding 81.2% of the revenue. The massive share exists because EU municipal city councils purchase aggressively while the EU Clean Vehicles Directive enforces mandatory zero-emission bus requirements for public tenders.

The Private Fleets segment is the fastest-growing category, expected to expand at a 19.4% CAGR during the forecast period. The acceleration occurs because companies need sustainable practices and schools need modernized transportation systems in Western European tourism fleets. The industry research shows that "Charging-as-a-Service" (CaaS) model availability has reduced private operators' entry costs by 15% which enables Italian and Spanish private tourism coaches to make quick transitions after they stayed away due to high infrastructure expenses.

Regional Insights

Western Europe

Western Europe made up about 46.5% of the Europe Electric Bus Charging Station market in 2025 because countries implemented strict decarbonization goals while cities developed zero-emission zones. Cities such as Berlin, Paris and London maintain their market development through strong demand which results in Germany becoming the top revenue generator for Europe with its 30% market share. Western European countries use high-power depot chargers to meet their 100% electric bus requirements under the European Commission's Alternative Fuels Infrastructure Regulation (AFIR) which states that the Netherlands and UK must achieve full electric bus operation by 2030.

Ultra-fast charging hardware investments receive support from government programs which respond to the strong municipal demand for clean air solutions because digital platform interoperability enables better market performance in the region. European Automobile Manufacturers' Association (ACEA) reports show that two-thirds of EU charging points are now found in three Western countries which include the Netherlands, Germany and France because these nations built their charging infrastructure early while having advanced electrical grid systems.

Southern Europe

The Southern Europe market held about 17.2% of the total market in 2025 because it grew steadily through major urban development projects and tourist destination development policies that supported Mediterranean tourism. Italian transit networks and Spanish transit networks use depot charging systems together with opportunity charging systems to meet their ongoing operational requirements. Italy needs to build 15% more high-capacity infrastructure every year across its cities because Italy plans to purchase thousands of electric buses through its National Recovery and Resilience Plan according to ACEA and the Italian Ministry of Infrastructure.

Public fleet operators and private fleet operators receive direct subsidies through policy frameworks which include the Moves Flotas program in Spain to accelerate charging point development. The regional shift now moves forward through increasing Electric Road projects and wireless charging pilot tests which include the Arena del Futuro project in Italy that plans to establish inductive charging along main highway routes. The region needs these developments because they support its goal of transitioning away from heavy-duty vehicles in both private coach and tourism operations.

Eastern Europe

Eastern Europe experienced a market increase which reached 14.8% during 2025 because fleet modernization efforts and urban air quality awareness grew among consumers. The fastest-growing geographical segment of the region now includes Poland and Romania which drive extensive state-funded initiatives. Poland's Act on Electromobility serves as the primary driver of charging installations because it provides legal incentives that have resulted in 29% growth for DC fast-charging installations throughout the past two years according to European Alternative Fuels Observatory (EAFO) data. Poland now operates one of the largest electric bus fleets in the European Union due to its electric bus fleet growth which has resulted from both the Act on Electromobility and increased charging installations.

Municipalities receive government support to replace their old diesel fleets because they can receive back up to €30,000 through government-backed programs which support charging stations that exceed 22 kW capacity in Romania.

Other Regions (Northern & Central Europe)

Northern and Central Europe account for 21.5% of the market while Norway Sweden and Denmark lead the market as top-performing nations. The countries have small total landmass but their residents achieve the highest charging density per person among all countries worldwide. Norway dominates the European market because 100% of new bus registrations now use electric power while the country has developed a comprehensive high-power depot charging infrastructure to support this. Western Europe, Southern Europe and Eastern Europe form three major regional blocks which together account for approximately 78.5% of total market revenue while Nordics and smaller Alpine states provide the remaining revenue from their efficient and full markets.

Competitive Landscape / Company Insights

Europe Electric Bus Charging Station market is moderately to highly competitive as both global and regional players are focusing on product innovation, pricing strategies, and geographic expansion. Besides, Companies are looking more and more into R&D and interoperability standards to reinforce their position in the market. ACEA and the European Commission have said that there is a race around high, power megawatt charging (MCS) and smart grid integration. Trusted sources say that players are focusing on turnkey depot solutions in order to fulfill the 2026 mandates of the Alternative Fuels Infrastructure Regulation (AFIR).

Mini Profiles

ABB focuses on innovative on-demand electric bus charging systems, supported by global distribution strength and robust connectivity via its Ability™ platform to ensure smarter, emission-free urban mobility.

BYD operates in the mass transit and heavy-duty segments, emphasizing cost efficiency and manufacturing scale to provide integrated energy solutions, including ultra-fast one-megawatt charging for rapid turnaround.

ChargePoint leverages its next-generation software platform and strategic partnerships to expand its market presence, offering scalable, future-ready DC fast charging solutions for municipal and commercial fleets.

Ekoenergetyka specializes in high-power charging for commercial public transport, emphasizing technical performance and modularity through custom-developed fixed and mobile terminals for logistics and heavy-duty vehicle environments.

Jema leverages its extensive engineering experience and local European presence to deliver interoperable depot chargers, emphasizing high-quality design and compliance with international standards for heavy-duty fleet electrification.

Key Players

- ABB Ltd.

- Alstom SA

- BYD Motors Inc.

- ChargePoint Inc.

- Efacec Power Solutions SGPS S.A.

- Ekoenergetyka-Polska Sp. z o.o.

- JEMA Energy S.A.

- Kempower Oyj

- Siemens AG

- Solaris Bus & Coach sp. z o.o.

Recent Developments

In January 2026, Titagarh Rail Systems Ltd. has given ABB a contract to provide modern propulsion systems and Train Control and Management System (TCMS) software for the Mumbai Metro Lines 5. ABB's position shall be strengthened as a partner in providing long-term solutions for India's expanding metro networks which shall increase connection between key geographic areas, reduce travel times, and ease daily commuter traffic.

In November 2025, Alstom which is a global leader in smart and sustainable mobility and Ukrainian Railways have announced an agreement to supply 55 Traxx locomotives. The contract will be financed primarily by the European Bank for Reconstruction and Development and the World Bank. The locomotives will be designed and manufactured at Alstom’s Belfort site, France. The delivery will begin in 2027.

In November 2025, A revamped software platform has been released by ChargePoint with the goal of managing EV charging operations at any size. The solution allows for the optimization of mixed hardware, including any OCPP-compliant charging stations, and serves fleets, CPOs, commercial locations, and OEMs.

Europe Electric Bus Charging Station Market Coverage

Charging Type Insight and Forecast 2026 - 2035

- Depot Charging

- Opportunity Charging

- Inductive Charging

Charger Category Insight and Forecast 2026 - 2035

- Off-Board Chargers

- On-Board Chargers

Power Output Insight and Forecast 2026 - 2035

- <50 kW

Europe Electric Bus Charging Station Market by Region

- Germany

- By Charging Type

- By Charger Category

- By Power Output

- U.K.

- By Charging Type

- By Charger Category

- By Power Output

- France

- By Charging Type

- By Charger Category

- By Power Output

- Italy

- By Charging Type

- By Charger Category

- By Power Output

- Spain

- By Charging Type

- By Charger Category

- By Power Output

- Russia

- By Charging Type

- By Charger Category

- By Power Output

- Rest of Europe

- By Charging Type

- By Charger Category

- By Power Output

Table of Contents for Europe Electric Bus Charging Station Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Charging Type

1.2.2. By

Charger Category

1.2.3. By

Power Output

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Europe Market Estimate and Forecast

4.1. Europe Market Overview

4.2. Europe Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Charging Type

5.1.1. Depot Charging

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Opportunity Charging

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Inductive Charging

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Charger Category

5.2.1. Off-Board Chargers

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. On-Board Chargers

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Power Output

5.3.1. <50 kW

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

6. Germany Market Estimate and Forecast

6.1. By

Charging Type

6.2. By

Charger Category

6.3. By

Power Output

7. U.K. Market Estimate and Forecast

7.1. By

Charging Type

7.2. By

Charger Category

7.3. By

Power Output

8. France Market Estimate and Forecast

8.1. By

Charging Type

8.2. By

Charger Category

8.3. By

Power Output

9. Italy Market Estimate and Forecast

9.1. By

Charging Type

9.2. By

Charger Category

9.3. By

Power Output

10. Spain Market Estimate and Forecast

10.1. By

Charging Type

10.2. By

Charger Category

10.3. By

Power Output

11. Russia Market Estimate and Forecast

11.1. By

Charging Type

11.2. By

Charger Category

11.3. By

Power Output

12. Rest of Europe Market Estimate and Forecast

12.1. By

Charging Type

12.2. By

Charger Category

12.3. By

Power Output

13. Company Profiles

13.1.

ABB Ltd.

13.1.1.

Snapshot

13.1.2.

Overview

13.1.3.

Offerings

13.1.4.

Financial

Insight

13.1.5.

Recent

Developments

13.2.

Alstom SA

13.2.1.

Snapshot

13.2.2.

Overview

13.2.3.

Offerings

13.2.4.

Financial

Insight

13.2.5.

Recent

Developments

13.3.

BYD Motors Inc.

13.3.1.

Snapshot

13.3.2.

Overview

13.3.3.

Offerings

13.3.4.

Financial

Insight

13.3.5.

Recent

Developments

13.4.

ChargePoint Inc.

13.4.1.

Snapshot

13.4.2.

Overview

13.4.3.

Offerings

13.4.4.

Financial

Insight

13.4.5.

Recent

Developments

13.5.

Efacec Power Solutions SGPS S.A.

13.5.1.

Snapshot

13.5.2.

Overview

13.5.3.

Offerings

13.5.4.

Financial

Insight

13.5.5.

Recent

Developments

13.6.

Ekoenergetyka-Polska Sp. z o.o.

13.6.1.

Snapshot

13.6.2.

Overview

13.6.3.

Offerings

13.6.4.

Financial

Insight

13.6.5.

Recent

Developments

13.7.

JEMA Energy S.A.

13.7.1.

Snapshot

13.7.2.

Overview

13.7.3.

Offerings

13.7.4.

Financial

Insight

13.7.5.

Recent

Developments

13.8.

Kempower Oyj

13.8.1.

Snapshot

13.8.2.

Overview

13.8.3.

Offerings

13.8.4.

Financial

Insight

13.8.5.

Recent

Developments

13.9.

Siemens AG

13.9.1.

Snapshot

13.9.2.

Overview

13.9.3.

Offerings

13.9.4.

Financial

Insight

13.9.5.

Recent

Developments

13.10.

Solaris Bus & Coach sp. z o.o.

13.10.1.

Snapshot

13.10.2.

Overview

13.10.3.

Offerings

13.10.4.

Financial

Insight

13.10.5.

Recent

Developments

14. Appendix

14.1. Exchange Rates

14.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Europe Electric Bus Charging Station Market