Australia Data Center Cooling Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Cooling Solution (Air Conditioning, Precision Air Conditioning, Chillers, Cooling Towers, Economizers, Liquid Cooling Systems, Immersion Cooling, Free Cooling Systems), by Cooling Technique (Room Based Cooling, Row Based Cooling, Rack Based Cooling), by Data Center Type (Hyperscale Data Center, Colocation Data Center, Enterprise Data Center, Edge Data Center, Mid Size Data Center, Large Data Center), by End User (IT and Telecommunication, BFSI, Government, Healthcare, Manufacturing, Media and Entertainment, Energy, Retail and E Commerce), by Region (New South Wales and ACT, Victoria and Tasmania, Queensland, Rest of Australia)

| Status : Published | Published On : May, 2026 | Report Code : VRSME9220 | Industry : Semiconductor & Electronics | Available Format :

|

Page : 123 |

Australia Data Center Cooling Market Overview

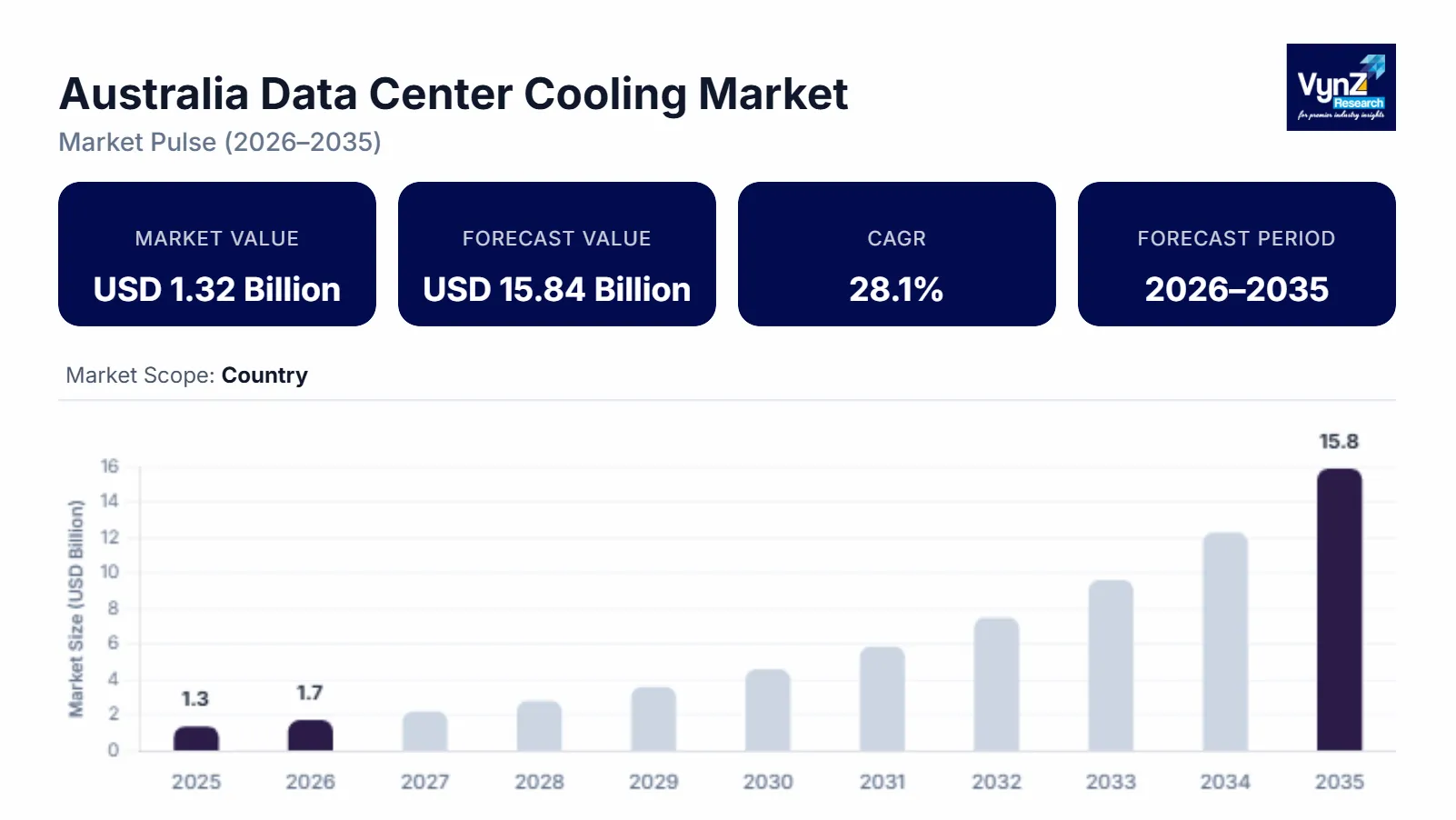

The Australia data center cooling market size stood at roughly USD 1.32 billion in 2025 and is anticipated to reach approximately USD 15.84 billion by 2035 from around USD 1.68 billion in 2026, registering a CAGR of about 28.1% during the forecast period 2026–2035.

Research Highlights

- Precision air conditioning held around 31.4% share in 2025 due to rising deployments.

- Hyperscale data centers accounted for nearly 39.2% revenue share in 2025 driven by AI infrastructure expansion.

- New South Wales and ACT dominated with almost 39% share in 2025 owing to strong hyperscale growth.

- Liquid cooling systems will grow at about 30.2% CAGR due to increasing demand for AI computing.

- IT and telecom held nearly 42.6% market share in 2025 due to rising cloud traffic.

Market growth is driven by increasing hyperscale data center construction with rising AI, high performance computing workloads, and a growing need for energy efficient thermal management infrastructure. The adoption of liquid cooling and immersion cooling technologies, demand for cloud computing, colocation services keep climbing, and ongoing investments in renewable energy integration together with national digital infrastructure development are backing market expansion across major regions like New South Wales, Victoria, and Queensland. Reports released by Australian government backed energy and sustainability authorities, also point to an increasing emphasis on low emission digital infrastructure and more efficient energy utilization inside large scale data center facilities.

Australia Data Center Cooling Market Dynamics

Market Trends

The industry is seeing some notable shifts toward liquid cooling adoption, high density thermal management being rolled out in more places, and energy efficient heat rejection system usage that feels more common lately. One of the big things pushing the market is how fast companies are moving to liquid and immersion cooling solutions showing a preference for higher efficiency and reduced energy consumption and better support for AI driven workloads. Another emerging trend is AI enabled thermal monitoring along with smart cooling automation systems mostly because digital transformation is happening and because the energy efficiency expectations are getting stricter due to stricter national sustainability and emissions reduction frameworks.

Growth Drivers

Market growth is subject to rise in construction of hyperscale and colocation data centers as it promotes demand for advanced heat control solutions to facilitate cloud computing and AI computing environments. Increasing investments in digital infrastructure, renewable powered facilities and high-performance computing setups are further pushing expansion. Also, there’s rising demand for uninterrupted digital services and more enterprise emphasis on operational efficiency, which is driving adoption of precision cooling systems, chillers, and liquid cooling technologies. Since operators are trying to improve energy efficiency, keep performance stable, and stay in line with regulatory compliance tied to national sustainability goals, demand for advanced cooling infrastructure should keep holding up through the forecast period. Government supported energy transition programs and digital economy initiatives are additionally helping with large scale infrastructure modernization in major Australian regions.

Market Restraints / Challenges

Even with good growth prospects, the market faces issues due to high capital expenditure requirements, electricity costs that keep climbing, and installation processes that can get complicated for advanced cooling technologies. These issues can affect profitability and adoption rates, especially for smaller operators and newer facilities that are still ramping up. There’s also dependence on imported cooling equipment, specialized parts, and advanced thermal systems, so supply chain vulnerabilities show up, which can mean cost swings, procurement delays and some limitations on scalability. Regulatory compliance around energy efficiency standards and environmental sustainability adds another layer of operational complexity and that tends to weigh on overall market performance during periods of infrastructure expansion.

Market Opportunities

The market also has opportunities, especially in liquid cooling and immersion cooling systems, largely because AI workloads are rising, high density computing needs keep expanding, and demand for energy efficient infrastructure is increasing. Businesses that provide modular, scalable, high performance cooling solutions are in a strong spot to capture that demand from hyperscale, colocation and enterprise data center operators. Another clear opportunity is smart and automated cooling optimization systems, where investments in AI enabled monitoring platforms and predictive thermal management are opening pathways for higher efficiency and practical operational savings. Progress in sustainable cooling technologies and better integration with renewable energy systems is expected to lift system performance and improve overall energy utilization.

Australia Data Center Cooling Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 1.32 Billion |

|

Revenue Forecast in 2035 |

USD 15.84 Billion |

|

Growth Rate |

28.1% |

|

Segments Covered in the Report |

Cooling Solution, Cooling Technique, Data Center Type, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

New South Wales and ACT, Victoria and Tasmania, Queensland, Rest of Australia |

|

Key Companies |

ALFA LAVAL Corporate AB, Daikin Industries Limited, Johnson Controls Inc., Mitsubishi Electric Corporation, Munters Group, Rittal GmbH & Co. KG, Schneider Electric SE, SRA Solutions, Stulz GmbH, Trane Technologies Company LLC |

|

Customization |

Available upon request |

Australia Data Center Cooling Market Segmentation

By Cooling Solution

In 2025, precision air conditioning took the biggest share, around 31.4% of total revenue, mainly because it’s been widely rolled out across hyperscale and colocation facilities where thermal stability matters a lot and uptime is nonnegotiable. Liquid cooling systems are projected to move the quickest, with growth of about 30.2% through the forecast period, helped by AI workloads picking up steam, high density computing setups, and the general push for energy efficient thermal management. More and more adoption is showing up across cloud infrastructure and enterprise data centers and that’s supported by the growing focus on cutting power usage effectiveness and improving operational efficiency across Australia’s digital infrastructure sites.

By Cooling Technique

Room based cooling held the largest share in 2025 at roughly 46.8%, since many operators keep leaning on centralized cooling infrastructure because it tends to be cost friendly and easier to maintain across older facilities. Rack-based cooling is expected to be the fastest mover, at around 29.6%, due to higher density server configurations and AI tuned computing workloads. Localized thermal control is expanding along with better heat dissipation efficiency and therefore advanced cooling architectures are being deployed more often. Row based cooling remains steady, supported by hybrid infrastructure upgrades and that gradual shift toward modular cooling designs in both enterprise and colocation environments.

By Data Center Type

In 2025, hyperscale data centers contributed 39.2% of the total market revenue due to higher investment by cloud providers in high-performance computing setup and rising AI. Edge data centers are estimated to grow at a 31.5% CAGR mainly due to the growing need for low latency computing, wider connectivity networks and distributed digital infrastructure. Colocation keeps getting strong adoption as enterprises increasingly outsource, while enterprise data centers show steadier demand from digital transformation efforts happening across BFSI, healthcare, and government sectors in Australia.

By End User

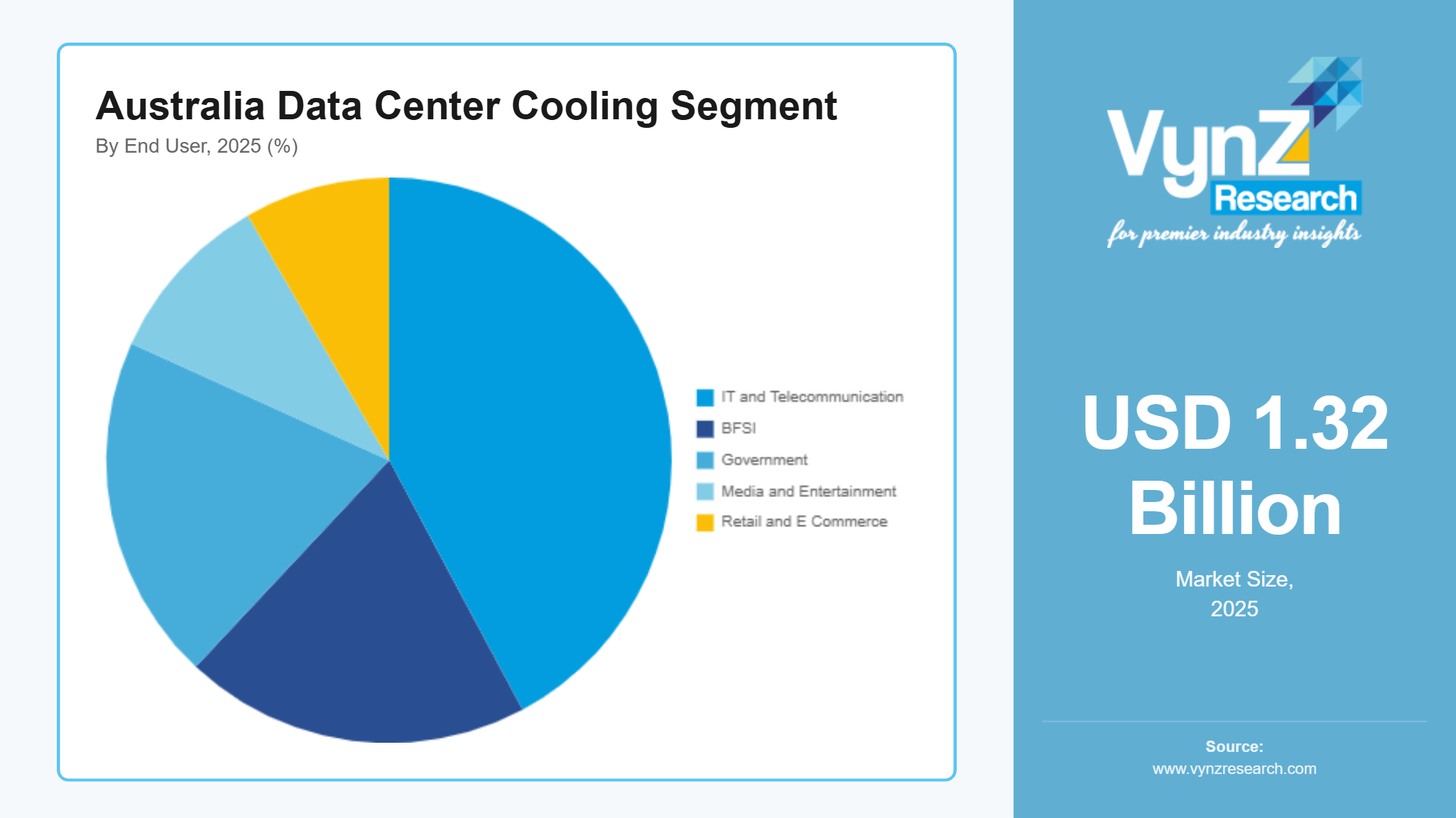

In 2025, IT and telecommunication held the largest market share of about 42.6% due to higher data traffic, cloud adoption, and continued 5G infrastructure development in Australia. Healthcare is estimated to expand roughly at 28.9% with higher use of digital health records and telemedicine and a more reliable and accessible data storage system.

BFSI and government segments will also grow at a rapid pace due to greater emphasis on data privacy, protection, and compliance requirements. It will also grow due to rapid modernization of digital frameworks, rising adoption and growing need for advanced and efficient cooling solutions.

Regional Insights

New South Wales and ACT

New South Wales and ACT accounted for nearly 39% of the entire market in 2025 due to better cloud infrastructure and large number of hyperscale data centers. This increases the demand for advanced, high-density thermal management systems in regions like Sydney and Canberra. Steady growth is also facilitated by the growing demand form financial services, cloud operators and government digital platforms. Government rules for energy efficiency and emission reduction initiatives also force companies to adopt liquid and precision cooling systems.

Victoria and Tasmania

Victoria and Tasmania held 25% of the market in 2025 mainly due to rapid digitalization across enterprises, higher investments in colocation, and growing data infrastructure in Melbourne and other metropolitan areas. BFSI, IT and healthcare adopt advanced liquid and hybrid cooling systems to ensure sustainability and match the requirements of the government policies regarding renewable energy integration. It also helps to promote operational efficiency and meet the rising demand with better and more stable digital connectivity networks.

Queensland

Queensland held about 18% of the market in 2025 due to wider deployment of edge data centers, continued digital transformation and growing need for enterprise connectivity across industrial hubs in Brisbane and other regions. Growth is also driven by higher scalability needs in distributed and cloud computing, further pushed by the government initiatives to develop smart cities and digital infrastructure. Rising demand from telecom and other small and large digital service providers is also pushing the market forward, resulting in growing investments to build more flexible and modular data centers.

Rest of Australia

The rest of Australia held 18% of the market in 2025 due to rising demand for remote connectivity, steady upgrading of digital infrastructure, and higher adoption of cloud-based services by enterprises. Smaller and regional data processing centers also push the demand higher for more efficient cooling systems which is backed by regional development programs and energy efficiency initiatives of the government across all emerging facilities.

Competitive Landscape / Company Insights

The market is moderately to highly competitive since all market players look for more efficient and advanced thermal management systems. Geographic expansion and innovations in liquid cooling urge companies to invest in research and development, building energy-efficient technologies with better digital monitoring capabilities. Colocation providers and hyperscale operators are collaborating with each other more to use low-emission cooling solutions, as required by the government sustainability frameworks thereby promoting infrastructure modernization in the long term across the entire sector.

Mini Profiles

ALFA LAVAL Corporate AB focuses on advanced heat transfer and cooling optimization solutions, supported by strong global brand recognition and established industrial engineering expertise across large scale data center thermal management applications.

Daikin Industries Limited operates in premium cooling and HVAC segments, emphasizing high-performance air-conditioning technologies, energy efficiency innovation, and customized thermal solutions for mission critical infrastructure environments.

Johnson Controls Inc. focuses on integrated building efficiency and cooling systems, supported by strong digital capabilities and smart infrastructure solutions that enhance energy management across modern data center facilities.

Mitsubishi Electric Corporation leverages advanced manufacturing expertise and strategic technological partnerships to expand market presence, delivering high efficiency cooling systems and intelligent thermal control solutions for critical environments.

Munters Group focuses on industrial air treatment and precision cooling solutions, supported by strong engineering specialization and cost-efficient climate control technologies tailored for high density data center operations.

Key Players

- ALFA LAVAL Corporate AB

- Daikin Industries Limited

- Johnson Controls Inc.

- Mitsubishi Electric Corporation

- Munters Group

- Rittal GmbH & Co. KG

- Schneider Electric SE

- SRA Solutions

- Stulz GmbH

- Trane Technologies Company LLC

Recent Developments

In March 2026, Schneider Electric SE expanded its liquid cooling and high-density data center thermal management portfolio to support AI driven infrastructure demands. The company focused on improving energy efficiency and operational resilience across hyperscale facilities.

In May 2025, Trane Technologies Company LLC introduced next generation precision cooling systems designed for high performance data centers. The launch emphasized reduced energy consumption and improved heat rejection efficiency for large scale digital infrastructure.

In July 2025, Rittal GmbH & Co. KG enhanced its modular data center cooling and rack based thermal management solutions portfolio. The company strengthened its focus on scalable infrastructure designs for rapidly expanding cloud and edge computing environments.

In September 2025, Stulz GmbH launched upgraded precision cooling systems optimized for high density server environments. The development focused on improving thermal stability and supporting continuous uptime requirements in mission critical facilities.

In January 2026, SRA Solutions expanded its integrated data center infrastructure and cooling optimization offerings across the Asia Pacific region. The company emphasized modular design efficiency and improved energy management for modern digital facilities.

Australia Data Center Cooling Market Coverage

Cooling Solution Insight and Forecast 2026 - 2035

- Air Conditioning

- Precision Air Conditioning

- Chillers

- Cooling Towers

- Economizers

- Liquid Cooling Systems

- Immersion Cooling

- Free Cooling Systems

Cooling Technique Insight and Forecast 2026 - 2035

- Room Based Cooling

- Row Based Cooling

- Rack Based Cooling

Data Center Type Insight and Forecast 2026 - 2035

- Hyperscale Data Center

- Colocation Data Center

- Enterprise Data Center

- Edge Data Center

- Mid Size Data Center

- Large Data Center

End User Insight and Forecast 2026 - 2035

- IT and Telecommunication

- BFSI

- Government

- Healthcare

- Manufacturing

- Media and Entertainment

- Energy

- Retail and E Commerce

Region Insight and Forecast 2026 - 2035

- New South Wales and ACT

- Victoria and Tasmania

- Queensland

- Rest of Australia

Australia Data Center Cooling Market by Region

- New South Wales and ACT

- By Cooling Solution

- By Cooling Technique

- By Data Center Type

- By End User

- By Region

- Victoria and Tasmania

- By Cooling Solution

- By Cooling Technique

- By Data Center Type

- By End User

- By Region

- Queensland

- By Cooling Solution

- By Cooling Technique

- By Data Center Type

- By End User

- By Region

- Rest of Australia

- By Cooling Solution

- By Cooling Technique

- By Data Center Type

- By End User

- By Region

Table of Contents for Australia Data Center Cooling Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Cooling Solution

1.2.2. By

Cooling Technique

1.2.3. By

Data Center Type

1.2.4. By

End User

1.2.5. By

Region

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Australia Market Estimate and Forecast

4.1. Australia Market Overview

4.2. Australia Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Cooling Solution

5.1.1. Air Conditioning

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Precision Air Conditioning

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Chillers

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Cooling Towers

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Economizers

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.1.6. Liquid Cooling Systems

5.1.6.1. Market Definition

5.1.6.2. Market Estimation and Forecast to 2035

5.1.7. Immersion Cooling

5.1.7.1. Market Definition

5.1.7.2. Market Estimation and Forecast to 2035

5.1.8. Free Cooling Systems

5.1.8.1. Market Definition

5.1.8.2. Market Estimation and Forecast to 2035

5.2. By Cooling Technique

5.2.1. Room Based Cooling

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Row Based Cooling

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Rack Based Cooling

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By Data Center Type

5.3.1. Hyperscale Data Center

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Colocation Data Center

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Enterprise Data Center

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Edge Data Center

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Mid Size Data Center

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.3.6. Large Data Center

5.3.6.1. Market Definition

5.3.6.2. Market Estimation and Forecast to 2035

5.4. By End User

5.4.1. IT and Telecommunication

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. BFSI

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Government

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Healthcare

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Manufacturing

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

5.4.6. Media and Entertainment

5.4.6.1. Market Definition

5.4.6.2. Market Estimation and Forecast to 2035

5.4.7. Energy

5.4.7.1. Market Definition

5.4.7.2. Market Estimation and Forecast to 2035

5.4.8. Retail and E Commerce

5.4.8.1. Market Definition

5.4.8.2. Market Estimation and Forecast to 2035

5.5. By Region

5.5.1. New South Wales and ACT

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Victoria and Tasmania

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Queensland

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Rest of Australia

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

6. New South Wales and ACT Market Estimate and Forecast

6.1. By

Cooling Solution

6.2. By

Cooling Technique

6.3. By

Data Center Type

6.4. By

End User

6.5. By

Region

7. Victoria and Tasmania Market Estimate and Forecast

7.1. By

Cooling Solution

7.2. By

Cooling Technique

7.3. By

Data Center Type

7.4. By

End User

7.5. By

Region

8. Queensland Market Estimate and Forecast

8.1. By

Cooling Solution

8.2. By

Cooling Technique

8.3. By

Data Center Type

8.4. By

End User

8.5. By

Region

9. Rest of Australia Market Estimate and Forecast

9.1. By

Cooling Solution

9.2. By

Cooling Technique

9.3. By

Data Center Type

9.4. By

End User

9.5. By

Region

10. Company Profiles

10.1.

ALFA LAVAL Corporate AB

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Daikin Industries Limited

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Johnson Controls Inc.

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Mitsubishi Electric Corporation

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Munters Group

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Rittal GmbH & Co. KG

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Schneider Electric SE

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

SRA Solutions

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Stulz GmbH

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Trane Technologies Company LLC

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Australia Data Center Cooling Market