Europe TIC Market for IT & Telecom Industry Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Service Type (Testing, Inspection, Certification), by Sourcing Type (In house, Outsourced), by Application (Network infrastructure, Cloud and data centers, IoT systems, Software platforms), by End User (Telecom operators, IT service providers, Data centers, Managed service providers)

| Status : Published | Published On : Mar, 2026 | Report Code : VRSME9202 | Industry : Semiconductor & Electronics | Available Format :

|

Page : 161 |

Europe TIC Market for IT & Telecom Industry Overview

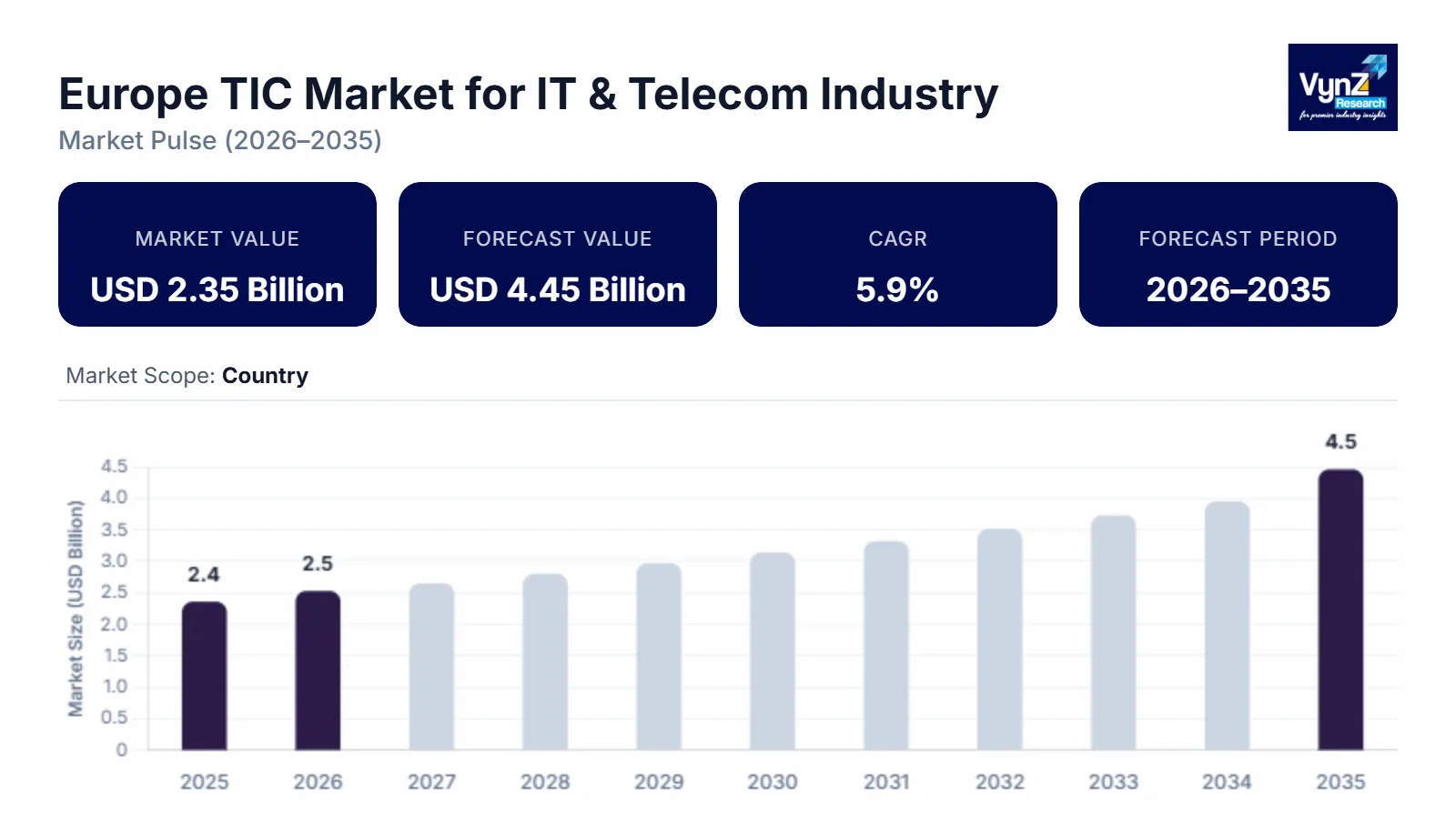

The Europe TIC Market for IT & Telecom Industry which was valued at approximately USD 2.35 billion in 2025 and is estimated to reach around USD 2.52 billion in 2026, is projected to reach approximately USD 4.45 billion by 2035, expanding at a CAGR of about 5.9% during the forecast period from 2026 to 2035.

Market expansion receives backing from multiple factors which include increased 5G network deployment, more challenging telecom infrastructure requirements, mandatory data security and network performance regulations and the rising use of digital testing and cybersecurity certification solutions. TIC services see rising demand from European Commission and European Union Agency for Cybersecurity (ENISA) frameworks which establish requirements for network resilience, cybersecurity compliance and data protection measures in the entire IT and telecom industry. Digital infrastructure programs and cybersecurity programs which the government implements to protect national security strengthen digital infrastructure and cybersecurity resilience for all major economies.

The European Commission Digital Decade strategy and ENISA cybersecurity guidelines drive businesses to seek compliance verification and certification services at higher rates. The market experiences expansion because public funds support the deployment of 5G networks and cloud computing infrastructure and secure communication systems. The European market experiences growing demand for TIC services because cities like Berlin, Paris and Amsterdam increasingly depend on IoT systems and data governance frameworks and telecom modernization projects.

Europe TIC Market for IT & Telecom Industry Dynamics

Market Trends

The market experiences a fundamental transformation which creates a need for digital compliance solutions and cybersecurity validation tools together with automated testing frameworks to support extensive digital transformation projects that major European companies execute. The European Commission Digital Decade framework together with European Union Agency for Cybersecurity (ENISA) guidelines establishes security standards which help network systems achieve greater reliability through unified security methods, better data protection and efficient network operation. The testing platforms which operate through cloud technology and the tools for remote inspection and the AI-based compliance solutions have witnessed higher adoption rates because they boost operational efficiency while enabling constant monitoring. Telecom operators and IT service providers are using automated validation systems together with cybersecurity certification processes to achieve better performance outcomes and meet regulatory requirements according to the new digital infrastructure guidelines that European authorities have developed.

Growth Drivers

The market experiences growth because European countries implement expanding 5G network systems and their digital communication networks become more intricate. The implementation of advanced telecom technologies together with cloud computing and Internet of Things ecosystems drives increased demand for testing, inspection and certification services which guarantee network performance and data protection. Industries are adopting secure digital platforms because enterprises need secure digital platforms and government-supported cybersecurity programs enable businesses to protect their digital operations. The European Commission and ENISA initiatives which promote secure communication systems, data governance and interoperability standards help organizations comply with regulations while building dependable infrastructure and expanding their use of TIC services in the telecom and IT fields.

Market Restraints / Challenges

Organizations need to invest in specialized infrastructure and automated systems and hire skilled workers to meet the requirements for advanced digital testing and cybersecurity certification. Government bodies conduct assessments according to European cybersecurity and digital policy frameworks which reveal that budget restrictions together with insufficient testing facility access present obstacles to smaller enterprises trying to adopt advanced testing equipment. The combination of multiple jurisdictions which have complex regulatory requirements together with data protection laws which are now undergoing changes creates additional compliance challenges and higher operational expenses. The requirement for high-skilled workers and advanced technology results in cost challenges for service providers who face both technological transitions and economic downturns.

Market Opportunities

The market provides growth opportunities for companies which develop cybersecurity testing services together with cloud certification and digital compliance services to meet the growing regulatory requirements for data privacy and network security and digital sovereignty. The European Commission Digital Decade program and ENISA cybersecurity strategies receive government backing which creates a path for organizations to adopt secure digital infrastructure and particular compliance guidelines. The combination of artificial intelligence, automation and remote auditing technology will create operational improvements which result in lower costs and greater service capacity development for organizations. Advanced TIC solutions which companies provide through their digital platforms create personalized solutions which organizations from telecom operators to cloud service providers and enterprise IT networks will choose to sustain their future market expansion.

Europe TIC Market for IT & Telecom Industry Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 2.35 Billion |

|

Revenue Forecast in 2035 |

USD 4.45 Billion |

|

Growth Rate |

5.9% |

|

Segments Covered in the Report |

By Service Type, By Sourcing Type, By Application, By End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

Germany, France, Italy, Rest of the Europe |

|

Key Companies |

Applus+, Bureau Veritas, DEKRA SE, DNV Group, Element Materials Technology, Eurofins Scientific, Intertek Group plc, MISTRAS Group, SGS SA, TUV SUD AG |

|

Customization |

Available upon request |

Europe TIC Market for IT & Telecom Industry Segmentation

By Service Type

Testing services constituted the largest portion of the market in 2025 because they generated 46% of total market revenue. The telecom sector and IT systems now require more network validation tests and performance evaluations and cybersecurity checks which created their current market dominance. European Commission regulatory frameworks together with European Union Agency for Cybersecurity ENISA cybersecurity standards create a requirement for communication networks and digital platforms to undergo permanent testing practices. This segment experiences continuous growth of 5.1% because 5G network expansion and cloud system development maintain demand for high frequency validation and continuous development of compliance requirements.

Certification services will achieve the highest growth rate during the timeframe from 2026 to 2035 through an approximate CAGR of 6.4%. The telecom sector and IT companies expand their operations because they require data security certification services and interoperability validation services and regulatory compliance services. The sector for inspection services maintains its growth rate of 5.6% because infrastructure audit requirements and network quality verification needs continue to increase. The digital policies that government agencies support together with cybersecurity frameworks create a positive environment for integrated TIC solution implementation which drives segment development.

By Sourcing Type

Internal services generated the biggest market share in 2025 through their 55% market contribution because telecom operators and IT enterprises preferred to maintain their testing functions and speed up their compliance processes. The organization achieves operational efficiency through its advanced in-house laboratories and digital testing infrastructure which provides real time monitoring capabilities. The European regulatory authorities require organizations to implement internal compliance mechanisms and continuous monitoring systems which results in improved security adoption rates among established companies that handle sensitive data in telecom and cloud service environments.

Outsourced services will achieve stronger market expansion through their projected CAGR of 6.6% during the upcoming forecast period. Enterprises develop their operations because telecom standards systems become more intricate while technological advancements accelerate and they seek to reduce costs. Small and mid-sized companies depend on third party TIC providers to obtain specialized knowledge and cutting-edge testing capabilities. The European Union digital infrastructure programs together with unified regulatory systems enable organizations to outsource TIC services which enhances their accessibility and service capacity.

.webp)

By Application

The network infrastructure segment generated the greatest revenue in 2025 because it represented 42% of total segment earnings. The continuous expansion of telecom networks through 5G deployment and fiber optic infrastructure upgrades across Europe sustains this dominant market position. The segment requires TIC services because current regulatory requirements establish network performance standards together with interoperability standards and cybersecurity compliance requirements. The economy maintains a stable growth rate at 5.3% because digital infrastructure investments grow and industrial sectors use high speed communication networks more.

The market for cloud and data center services will become the fastest growing segment through its CAGR which reaches 6.7% until 2035. The market grows because companies increasingly use cloud computing solutions and data storage products and enterprise digital transformation methods. Other applications including IoT systems and software platforms are also witnessing consistent growth at approximately 5.8%, supported by increasing demand for secure data transmission and real time system validation. Government data protection regulations and cybersecurity frameworks drive application domain adoption across multiple domains.

By End User

Telecom operators generated the largest market share in 2025 through their 58% revenue contribution which resulted from their extensive network systems and strict compliance obligations and ongoing investment in communication technology. The European Commission and ENISA established regulatory frameworks which require telecom operators to protect network security and conduct performance validation and compliance monitoring which creates demand for TIC services. The segment grows at a steady rate of 5.4% because 5G deployment and infrastructure modernization projects continue to progress.

IT service providers and enterprises will experience stronger growth through their projected CAGR of 6.5% during the upcoming forecast period. The industrial sector grows because organizations increasingly adopt cloud solutions, cybersecurity systems and digital transformation methods. The data centers together with managed service providers contribute to market growth through their 5.9% market share which results from increased demand for secure data management and compliance with regulations. Government initiatives that support digitalization and data governance and cybersecurity standards development act to improve adoption among all end user segments.

Regional Insights

Germany

Germany accounted for approximately 29% of the market in 2025 because its telecom infrastructure advanced military digitization and cybersecurity compliance frameworks became widely adopted. Berlin, Munich and Frankfurt serve as main centers for telecom testing activities which include network verification and certification processes. TIC services become necessary because the European Commission provides regulatory oversight and the European Union Agency for Cybersecurity (ENISA) creates cybersecurity standards. The government-backed initiatives which promote 5G deployment and data protection together with digital infrastructure modernization projects create more investment opportunities for testing and certification capabilities that boost regional market development.

France

France contributes approximately 23% of the market in 2025 because companies in the telecom and enterprise IT sectors undergo digital transformation. The market grows steadily because policies support cybersecurity measures, cloud computing and data governance frameworks become widely accepted. Paris and Lyon have developed into important locations which provide compliance validation services and telecom certification services. Organizations show needs for digital compliance based on European Commission digital strategies and national cybersecurity programs which create market demand. Telecom operators and cloud service providers and enterprise IT networks increase their usage of TIC services which results in continuous market expansion.

Italy

Italy represents around 20% of the market in 2025 because ongoing telecom modernization and fiber optic and 5G infrastructure expansion drive market growth. Infrastructure development and digital communication technology adoption across industries are driving the region's growth. The cities of Milan and Rome are now experiencing higher demand for testing and inspection and certification services which include network performance testing and cybersecurity validation. The combination of government support for digital transformation programs and regulatory compliance obligations creates market opportunities which help TIC providers maintain their market presence.

Rest of Europe

The Rest of Europe accounts for approximately 28% of the market in 2025 with countries like the Netherlands, Spain and Belgium showing growth because their digital ecosystems expand and their cross-border data exchange improves. The cities of Amsterdam, Madrid and Brussels are showing increased use of TIC services which support telecom and IT infrastructure development. Government policies which back data security and interoperability and digital compliance frameworks lead to wider adoption. The combined share of Germany, France, and Italy accounts for approximately 72% of the market because other European countries in this segment supply the remaining market demand which establishes total market distribution for the region at 100%.

Competitive Landscape / Company Insights

The market operates between a moderate and high level of competitiveness because both international and local companies concentrate their efforts on developing new services and implementing pricing strategies and expanding their market presence. The main service providers direct their funding toward digital testing platforms and cybersecurity validation tools and automated compliance systems to improve their operational efficiency and service delivery reliability. The European Commission's regulatory frameworks and the European Union Agency for Cybersecurity (ENISA) cybersecurity guidelines and the government digital infrastructure programs create a framework that enables adoption. The frameworks create a pathway for companies to enhance their market position while they extend their operations throughout telecom and IT service ecosystems.

Mini Profiles

Applus+ focuses on testing, inspection, and certification services across IT and telecom systems, supported by strong international presence, technical expertise, and cost efficient service delivery across regulated European markets.

Bureau Veritas operates in premium and compliance driven segments, emphasizing quality assurance, cybersecurity certification, and performance validation across telecom and digital infrastructure environments.

DEKRA SE leverages digital compliance solutions and strategic partnerships to expand market presence, supported by strong expertise in safety testing and certification across telecom networks and IT systems.

DNV Group focuses on assurance and certification services for digital infrastructure, supported by strong brand recognition, technical advisory capabilities, and expertise in cybersecurity and risk management across telecom ecosystems.

Eurofins Scientific leverages advanced laboratory networks and digital capabilities to expand market presence, supported by strong analytical expertise and growing focus on data validation and compliance testing services.

Key Players

- Applus+

- Bureau Veritas

- DEKRA SE

- DNV Group

- Element Materials Technology

- Eurofins Scientific

- Intertek Group plc

- MISTRAS Group

- SGS SA

- TUV SUD AG

Recent Developments

In March 2026, Intertek launched Digital Product Passport services in March 2026 to support regulatory compliance and traceability across digital and telecom supply chains. This initiative strengthens data transparency and aligns with evolving European digital compliance frameworks.

In February 2026, SGS contributed to the TIC Council digital strategy paper released in February 2026, focusing on digital transformation and conformity assessment modernization. The development highlights the company’s role in advancing digital compliance and certification frameworks globally.

In January 2026, Element Materials Technology expanded its advanced testing capabilities in early 2026 to address growing demand for telecom equipment validation and digital infrastructure compliance. The move supports increasing requirements for performance and safety testing in connected systems.

In January 2026, MISTRAS Group enhanced its digital inspection and monitoring solutions in January 2026, integrating advanced analytics for real time asset integrity and compliance. This development supports telecom infrastructure reliability and predictive maintenance applications.

In February 2026, Eurofins Scientific expanded its digital and analytical testing services in February 2026, focusing on data validation and cybersecurity compliance across IT systems. The initiative supports growing regulatory requirements for secure and high-performance digital infrastructure.

Europe TIC Market for IT & Telecom Industry Coverage

Service Type Insight and Forecast 2026 - 2035

- Testing

- Inspection

- Certification

Sourcing Type Insight and Forecast 2026 - 2035

- In house

- Outsourced

Application Insight and Forecast 2026 - 2035

- Network infrastructure

- Cloud and data centers

- IoT systems

- Software platforms

End User Insight and Forecast 2026 - 2035

- Telecom operators

- IT service providers

- Data centers

- Managed service providers

Europe TIC Market for IT & Telecom Industry by Region

- Germany

- By Service Type

- By Sourcing Type

- By Application

- By End User

- U.K.

- By Service Type

- By Sourcing Type

- By Application

- By End User

- France

- By Service Type

- By Sourcing Type

- By Application

- By End User

- Italy

- By Service Type

- By Sourcing Type

- By Application

- By End User

- Spain

- By Service Type

- By Sourcing Type

- By Application

- By End User

- Russia

- By Service Type

- By Sourcing Type

- By Application

- By End User

- Rest of Europe

- By Service Type

- By Sourcing Type

- By Application

- By End User

Table of Contents for Europe TIC Market for IT & Telecom Industry Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Service Type

1.2.2. By

Sourcing Type

1.2.3. By

Application

1.2.4. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Europe Market Estimate and Forecast

4.1. Europe Market Overview

4.2. Europe Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Service Type

5.1.1. Testing

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Inspection

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Certification

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Sourcing Type

5.2.1. In house

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Outsourced

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Application

5.3.1. Network infrastructure

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Cloud and data centers

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. IoT systems

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Software platforms

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.4. By End User

5.4.1. Telecom operators

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. IT service providers

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Data centers

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Managed service providers

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

6. Germany Market Estimate and Forecast

6.1. By

Service Type

6.2. By

Sourcing Type

6.3. By

Application

6.4. By

End User

7. U.K. Market Estimate and Forecast

7.1. By

Service Type

7.2. By

Sourcing Type

7.3. By

Application

7.4. By

End User

8. France Market Estimate and Forecast

8.1. By

Service Type

8.2. By

Sourcing Type

8.3. By

Application

8.4. By

End User

9. Italy Market Estimate and Forecast

9.1. By

Service Type

9.2. By

Sourcing Type

9.3. By

Application

9.4. By

End User

10. Spain Market Estimate and Forecast

10.1. By

Service Type

10.2. By

Sourcing Type

10.3. By

Application

10.4. By

End User

11. Russia Market Estimate and Forecast

11.1. By

Service Type

11.2. By

Sourcing Type

11.3. By

Application

11.4. By

End User

12. Rest of Europe Market Estimate and Forecast

12.1. By

Service Type

12.2. By

Sourcing Type

12.3. By

Application

12.4. By

End User

13. Company Profiles

13.1.

Applus+

13.1.1.

Snapshot

13.1.2.

Overview

13.1.3.

Offerings

13.1.4.

Financial

Insight

13.1.5.

Recent

Developments

13.2.

Bureau Veritas

13.2.1.

Snapshot

13.2.2.

Overview

13.2.3.

Offerings

13.2.4.

Financial

Insight

13.2.5.

Recent

Developments

13.3.

DEKRA SE

13.3.1.

Snapshot

13.3.2.

Overview

13.3.3.

Offerings

13.3.4.

Financial

Insight

13.3.5.

Recent

Developments

13.4.

DNV Group

13.4.1.

Snapshot

13.4.2.

Overview

13.4.3.

Offerings

13.4.4.

Financial

Insight

13.4.5.

Recent

Developments

13.5.

Element Materials Technology

13.5.1.

Snapshot

13.5.2.

Overview

13.5.3.

Offerings

13.5.4.

Financial

Insight

13.5.5.

Recent

Developments

13.6.

Eurofins Scientific

13.6.1.

Snapshot

13.6.2.

Overview

13.6.3.

Offerings

13.6.4.

Financial

Insight

13.6.5.

Recent

Developments

13.7.

Intertek Group plc

13.7.1.

Snapshot

13.7.2.

Overview

13.7.3.

Offerings

13.7.4.

Financial

Insight

13.7.5.

Recent

Developments

13.8.

MISTRAS Group

13.8.1.

Snapshot

13.8.2.

Overview

13.8.3.

Offerings

13.8.4.

Financial

Insight

13.8.5.

Recent

Developments

13.9.

SGS SA

13.9.1.

Snapshot

13.9.2.

Overview

13.9.3.

Offerings

13.9.4.

Financial

Insight

13.9.5.

Recent

Developments

13.10.

TUV SUD AG

13.10.1.

Snapshot

13.10.2.

Overview

13.10.3.

Offerings

13.10.4.

Financial

Insight

13.10.5.

Recent

Developments

14. Appendix

14.1. Exchange Rates

14.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Europe TIC Market for IT & Telecom Industry