Europe TIC Market for Sports and Entertainment Industry Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Service Type (Testing Services, Inspection Services, Certification Services, Auditing Services), by Sourcing Type (In-house, Outsourced), by Industry Vertical (Sports Industry, Entertainment Industry), by End User (Sports Venues & Stadium Operators, Entertainment Organizers, Broadcasters & Media Production Entities)

| Status : Published | Published On : Mar, 2026 | Report Code : VRSME9201 | Industry : Semiconductor & Electronics | Available Format :

|

Page : 158 |

Europe TIC Market for Sports and Entertainment Industry Overview

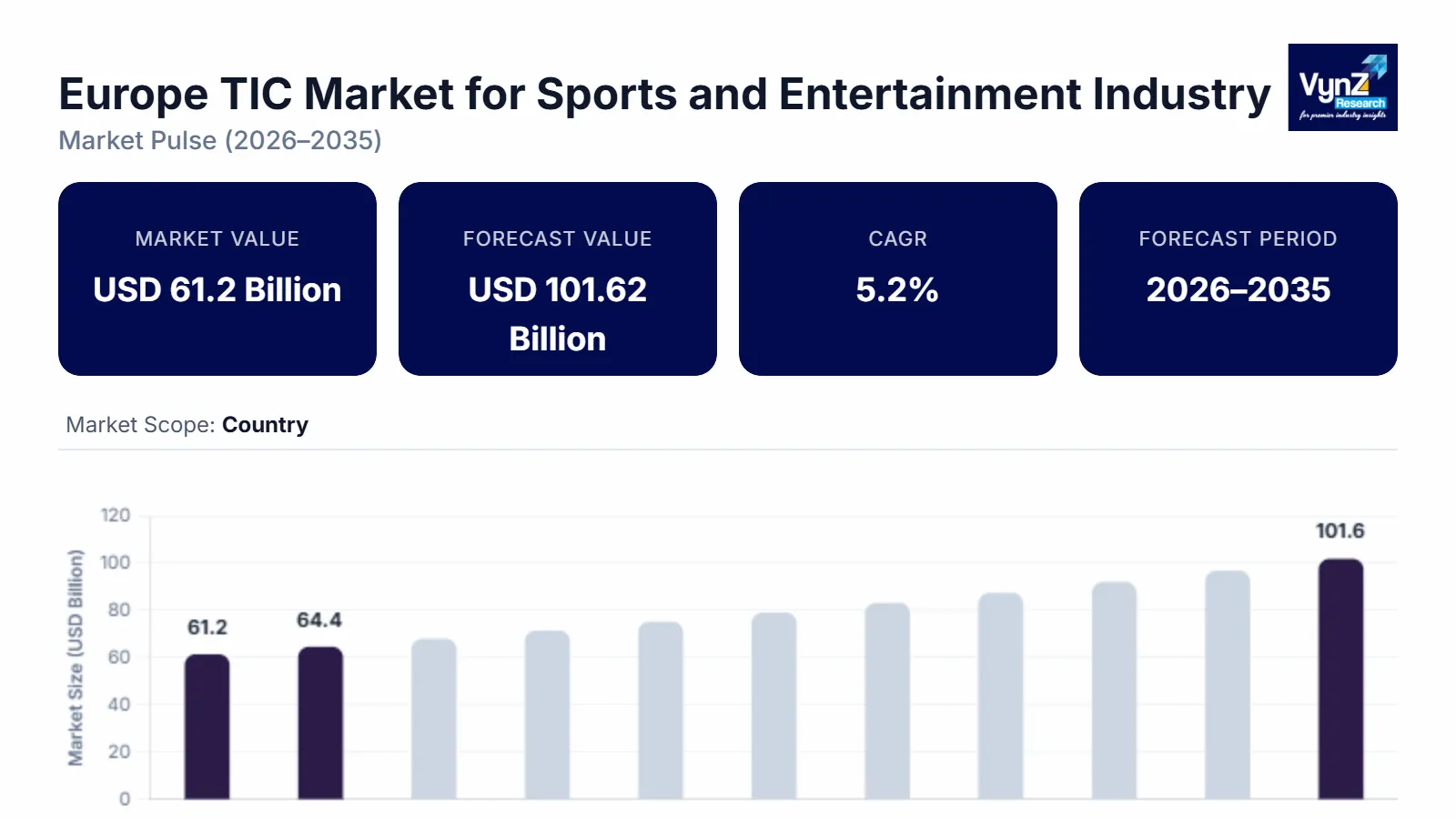

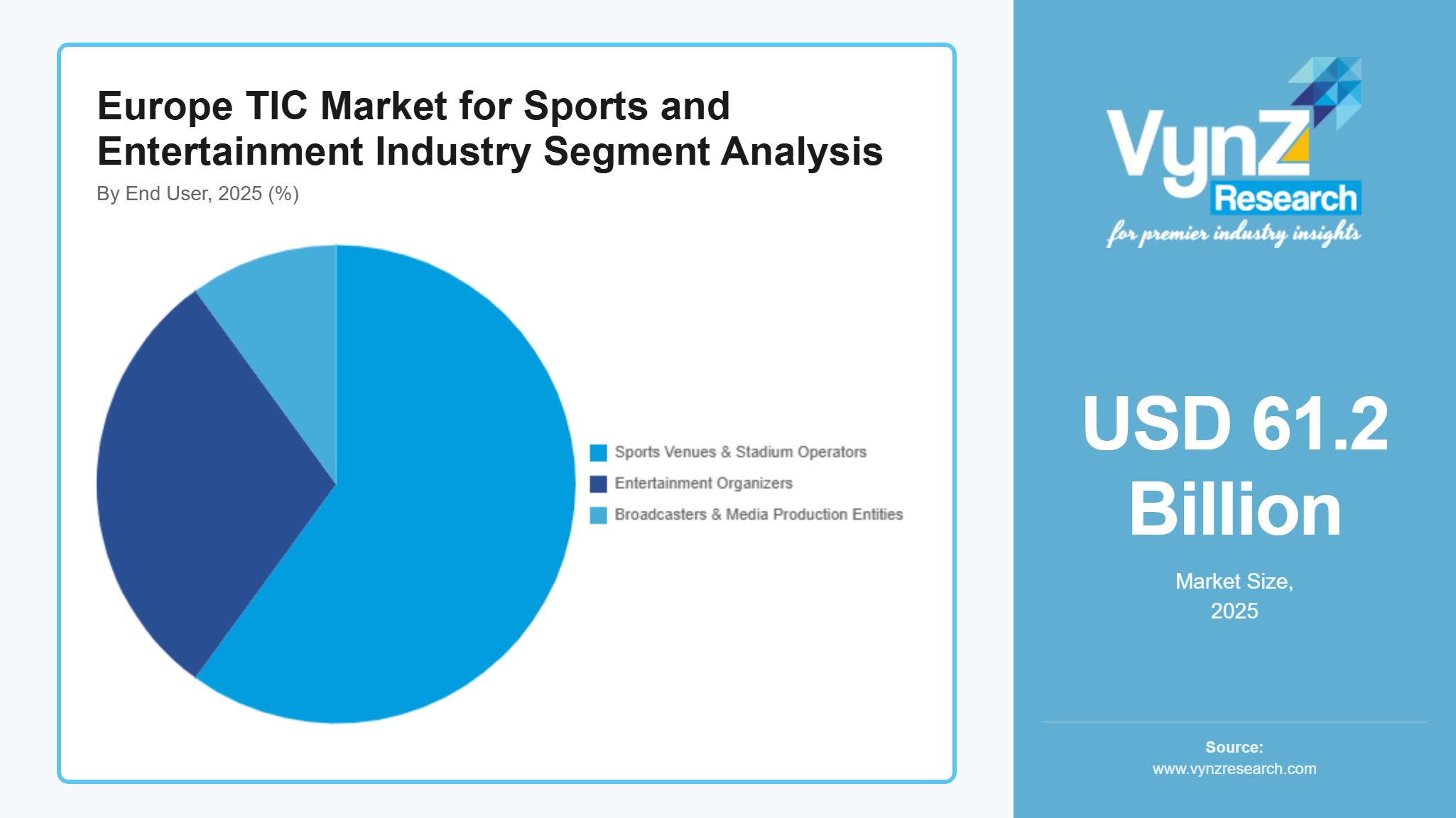

The Europe TIC market for sports and entertainment industry which was valued at approximately USD 61.2 billion in 2025 and is estimated to rise further up to almost USD 64.38 billion by 2026, is projected to reach around USD 101.62 billion in 2035, expanding at a CAGR of about 5.2% during the forecast period 2026 to 2035.

Market growth is driven by increasing regulatory compliance requirements, rising safety and quality standards in sports and entertainment venues, growing adoption of digital and IoT-based testing solutions, along with increasing use of automated inspection technologies. The increasing need for certified and secure sports equipment and entertainment stage infrastructure and event facilities together with ongoing European Union safety directive investments and national quality assurance activities, drive market growth across major regions which include Germany, France, and the United Kingdom.

Europe TIC Market for Sports and Entertainment Industry Dynamics

Market Trends

The market shows changing technology patterns and compliance methods through its rising use of digital conformity assessment frameworks and data‑driven inspection workflows. The market expands through remote auditing and digital inspection platform adoption because organizations now need operational efficiency and real‑time verification according to the European Commission’s Digital Europe Program which enables regulatory digitization. EU member states now adopt unified safety and quality standards which emerged as a new trend because regulations and industry compliance programs create common standards that force companies to use advanced reporting tools and standardized certification practices.

Growth Drivers

The market experiences growth because safety and compliance regulations in sports and entertainment venues create ongoing demand for regulatory requirements. The EU cohesion and regional development funds support market growth by funding infrastructure modernization projects that include stadium and entertainment complex renovations. The market expansion process depends on digital inspection and testing solution adoption, which enterprises use to achieve performance goals while maintaining operational transparency and public safety. This results in sustained demand for TIC services throughout the entire forecast period.

Market Restraints / Challenges

The market shows positive growth potential; however, its expansion faces multiple obstacles that lead to reduced market growth. The complex regulatory requirements which businesses must follow to evaluate compliance across multiple jurisdictions create a critical problem that reduces profitability while extending service delivery times. The testing equipment suppliers face operational difficulties because testing equipment needs to be imported, which adds cost and delivery delays. This situation hurts the market performance during economic downturns. The European Commission and industry oversight bodies publish reports that show smaller TIC service companies suffer from compliance cost burdens and technology access gaps.

Market Opportunities

The market shows strong opportunities through digital conformity assessment service expansion which public and private customers drive through their smart stadium and entertainment facility investments that use IoT sensors and performance monitoring systems. Integrated digital testing and certification solution providers stand to benefit from growing demand from large venue operators who need scalable automated assurance services. EU regulatory support creates an opportunity that enables cross‑border certification framework development which leads to long‑term client relationships through mutual safety and quality assurance investments. The competitive position of organizations will improve when they implement data analytics solutions because these solutions lead to better service delivery results.

Europe TIC Market for Sports and Entertainment Industry Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 61.2 Billion |

|

Revenue Forecast in 2035 |

USD 101.62 Billion |

|

Growth Rate |

5.2% |

|

Segments Covered in the Report |

By Service Type, By Sourcing Type, By Industry Vertical, By End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

Germany, The United Kingdom, France, Rest of Europe |

|

Key Companies |

Applus+, ALS Limited, Bureau Veritas, Dekra, Intertek Group PLC, Kiwa NV, SGS, TUV Nord Group, TUV Rheinland, TUV SUD |

|

Customization |

Available upon request |

Europe TIC Market for Sports and Entertainment Industry Segmentation

By Service Type

Testing services represented the major proportion of the European TIC market in 2025 since they generated about 48% of total segment revenues. The need for safety checks at sports venues and entertainment facilities together with EU inspection protocols and mandatory safety operations led to their market success. The EU public safety directives together with government programs for event management testing services enhance market demand. The inspection and certification sector will experience the most rapid expansion because digital inspection tools and IoT-based monitoring and automated reporting systems will become more widely adopted between 2026 and 2035.

By Sourcing Type

Outsourced services held a majority share in 2025, accounting for roughly 55% of segment revenue, as sports and entertainment operators continue to rely on specialized third-party TIC providers for expertise, scalability, and adherence to European safety standards. The in-house sourcing method will expand most rapidly because its projected growth rate from 2026 to 2035 will reach 6.1% through rising expenditures for internal quality control systems and digital inspection platforms and compliance frameworks which EU infrastructure modernization and safety programs promote. The combination of outsourced services together with in-house capabilities will create better operational results and expanded service delivery possibilities.

By Industry Vertical

The sports industry accounted for the largest segment of the Europe TIC market in 2025, contributing approximately 57% of revenue, supported by ongoing investments in stadium modernization, facility upgrades, and EU safety compliance mandates. The entertainment industry is expected to grow at the fastest rate, with an estimated CAGR of 6.0% during 2026 to 2035, driven by the expansion of live event productions, broadcast facilities, adoption of advanced digital inspection and certification processes. The European Commission and national safety authorities create regulatory systems which maintain quality standards across key European markets including Germany, France, and the UK.

By End User

Sports venues and stadium operators accounted for the largest end-user segment in 2025, representing approximately 60% of total market revenue, driven by large-scale urban investments, operational safety compliance, and EU-backed infrastructure programs. Entertainment organizers will achieve the fastest growth rate between 2026 to 2035 because their requirements include certified event infrastructure, digital monitoring tools and standardized compliance with European safety regulations. The media production entities and broadcasters drive revenue growth through TIC adoption which results from regulatory oversight for live broadcasting standards and high-volume production requirements.

Regional Insights

Germany

Germany held 28% of the market in 2025 because its industrial infrastructure and sports facility upgrades and EU safety regulation compliance for stadiums and entertainment venues brought about substantial market growth. The metropolitan areas of Berlin, Munich and Frankfurt display ongoing requirements for testing and inspection and certification services. The government backs infrastructure safety compliance programs and public funding for event upgrades and European Commission safety rules which boost investments into TIC services for sports and entertainment sectors. The region's market performance improves because consumers now expect safer experiences which include digital monitoring systems.

United Kingdom

The United Kingdom contributed roughly 22% of the market in 2025. The market develops through urbanization which creates more events and through the UK Health and Safety Executive (HSE) rules that offer regulatory guidance. The major stadiums, concert venues and media production facilities have developed a consistent demand for TIC services because they have started to adopt the system. The combination of government programs which promote public safety, certification of events and risk management together with private funding for stadium upgrades and new monitoring systems is boosting the regional market. The implementation of digital inspection systems together with automated testing solutions boosts both operational efficiency and confidence among stakeholders.

France

France represented approximately 18% of the Europe TIC market in 2025 through its development of entertainment centers, sports venues and broadcasting facilities. Government programs which promote safety compliance, event licensing and operational audits based on national and EU regulations support market growth. The major cities of Paris, Lyon and Marseille function as main centers for the adoption of TIC systems within the sports and entertainment sectors. The market now provides permanent business chances for companies which offer certified venue infrastructure and digital monitoring systems and risk mitigation services.

Rest of Europe

The markets from Italy, Spain and Netherlands and upcoming EU countries together contributed about 15% of the overall market in 2025. The stadium upgrades, digital safety monitoring systems and entertainment infrastructure upgrades which continue to happen lead to increased TIC service usage. Public safety regulations together with government compliance programs and consumer awareness about safety and quality standards drive market expansion. All other European nations show developing sports and entertainment systems while they have potential for extended market development contributing to the rest of it.

Competitive Landscape / Company Insights

The market is moderately competitive because regional and global companies compete through their service innovation and compliance expertise and geographic expansion efforts. Companies are increasingly investing in digital inspection tools and IoT-enabled monitoring and certification capabilities to achieve operational efficiency while meeting EU regulatory standards. Advanced TIC solutions enable firms to establish client trust while improving their market position in major European hubs which include Germany, the UK and France.

Mini Profiles

Applus+ focuses on inspection, testing, and certification services, supported by strong European presence, regulatory compliance expertise, and an extensive network of laboratories and service centers across multiple industries.

Bureau Veritas operates in premium TIC segments, emphasizing high-quality inspection, certification, and auditing services, leveraging technological innovation and global standards to ensure safety, reliability, and regulatory compliance for clients.

Dekra leverages local manufacturing and strategic partnerships to expand market presence, offering vehicle inspections, industrial testing, and certification solutions across Europe, supported by recognized brand reputation and comprehensive service portfolio.

Intertek Group PLC focuses on assurance, testing, and certification services, supported by a global laboratory network, digital reporting tools, and expertise in regulatory compliance for multiple industrial and commercial sectors.

Kiwa NV operates in specialized TIC services, emphasizing performance, sustainability, and customized solutions, leveraging strong European network, strategic partnerships, and digital monitoring technologies to enhance client trust and operational efficiency.

Key Players

- Applus+

- ALS Limited

- Bureau Veritas

- Dekra

- Intertek Group PLC

- Kiwa NV

- SGS

- TUV Nord Group

- TUV

- Rheinland

- TUV SUD

Recent Developments

In September 2025, Applus+ announced the acquisition of APEM Group to launch a new global Environmental Services business, expanding its TIC and sustainability consulting footprint. In December 2025, the company accelerated digital transformation initiatives, reinforcing its strategic focus on digital inspection and monitoring solutions across energy and industrial sectors.

In November 2025, ALS reported strong first‑half FY26 results with 14.7% underlying EBIT growth, supported by robust performance in commodities and life sciences testing services. Continued expansion of its laboratory services and digital testing capabilities strengthened ALS’s position in global compliance and assurance markets.

In early 2026, TÜV Nord expanded its technical service offerings in industrial and mobility testing amid rising demand for European conformity assessments, with workforce figures exceeding 15,000 employees. The company’s broad global network continued to support compliance and safety verification across key sectors including manufacturing and infrastructure.

Throughout 2025, TÜV Rheinland reported consistent expansion in digital inspection and certification services, responding to increased industry demand for quality and compliance verification across Europe. Investments in advanced testing technologies strengthened its role in supporting automotive, electronic, and industrial sector certifications.

In March 2025, TÜV SÜD was appointed as a Conformity Assessment Body for the Catena‑X Automotive Network, enhancing data verification and sustainability assurance standards across the automotive value chain. In November 2025, TÜV SÜD introduced an expanded IECEE Component Certification Programme, enabling faster global market access for electrotechnical products.

Europe TIC Market for Sports and Entertainment Industry Coverage

Service Type Insight and Forecast 2026 - 2035

- Testing Services

- Inspection Services

- Certification Services

- Auditing Services

Sourcing Type Insight and Forecast 2026 - 2035

- In-house

- Outsourced

Industry Vertical Insight and Forecast 2026 - 2035

- Sports Industry

- Entertainment Industry

End User Insight and Forecast 2026 - 2035

- Sports Venues & Stadium Operators

- Entertainment Organizers

- Broadcasters & Media Production Entities

Europe TIC Market for Sports and Entertainment Industry by Region

- Germany

- By Service Type

- By Sourcing Type

- By Industry Vertical

- By End User

- U.K.

- By Service Type

- By Sourcing Type

- By Industry Vertical

- By End User

- France

- By Service Type

- By Sourcing Type

- By Industry Vertical

- By End User

- Italy

- By Service Type

- By Sourcing Type

- By Industry Vertical

- By End User

- Spain

- By Service Type

- By Sourcing Type

- By Industry Vertical

- By End User

- Russia

- By Service Type

- By Sourcing Type

- By Industry Vertical

- By End User

- Rest of Europe

- By Service Type

- By Sourcing Type

- By Industry Vertical

- By End User

Table of Contents for Europe TIC Market for Sports and Entertainment Industry Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Service Type

1.2.2. By

Sourcing Type

1.2.3. By

Industry Vertical

1.2.4. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Europe Market Estimate and Forecast

4.1. Europe Market Overview

4.2. Europe Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Service Type

5.1.1. Testing Services

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Inspection Services

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Certification Services

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Auditing Services

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.2. By Sourcing Type

5.2.1. In-house

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Outsourced

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Industry Vertical

5.3.1. Sports Industry

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Entertainment Industry

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By End User

5.4.1. Sports Venues & Stadium Operators

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Entertainment Organizers

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Broadcasters & Media Production Entities

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

6. Germany Market Estimate and Forecast

6.1. By

Service Type

6.2. By

Sourcing Type

6.3. By

Industry Vertical

6.4. By

End User

7. U.K. Market Estimate and Forecast

7.1. By

Service Type

7.2. By

Sourcing Type

7.3. By

Industry Vertical

7.4. By

End User

8. France Market Estimate and Forecast

8.1. By

Service Type

8.2. By

Sourcing Type

8.3. By

Industry Vertical

8.4. By

End User

9. Italy Market Estimate and Forecast

9.1. By

Service Type

9.2. By

Sourcing Type

9.3. By

Industry Vertical

9.4. By

End User

10. Spain Market Estimate and Forecast

10.1. By

Service Type

10.2. By

Sourcing Type

10.3. By

Industry Vertical

10.4. By

End User

11. Russia Market Estimate and Forecast

11.1. By

Service Type

11.2. By

Sourcing Type

11.3. By

Industry Vertical

11.4. By

End User

12. Rest of Europe Market Estimate and Forecast

12.1. By

Service Type

12.2. By

Sourcing Type

12.3. By

Industry Vertical

12.4. By

End User

13. Company Profiles

13.1.

Applus+

13.1.1.

Snapshot

13.1.2.

Overview

13.1.3.

Offerings

13.1.4.

Financial

Insight

13.1.5.

Recent

Developments

13.2.

ALS Limited

13.2.1.

Snapshot

13.2.2.

Overview

13.2.3.

Offerings

13.2.4.

Financial

Insight

13.2.5.

Recent

Developments

13.3.

Bureau Veritas

13.3.1.

Snapshot

13.3.2.

Overview

13.3.3.

Offerings

13.3.4.

Financial

Insight

13.3.5.

Recent

Developments

13.4.

Dekra

13.4.1.

Snapshot

13.4.2.

Overview

13.4.3.

Offerings

13.4.4.

Financial

Insight

13.4.5.

Recent

Developments

13.5.

Intertek Group PLC

13.5.1.

Snapshot

13.5.2.

Overview

13.5.3.

Offerings

13.5.4.

Financial

Insight

13.5.5.

Recent

Developments

13.6.

Kiwa NV

13.6.1.

Snapshot

13.6.2.

Overview

13.6.3.

Offerings

13.6.4.

Financial

Insight

13.6.5.

Recent

Developments

13.7.

SGS

13.7.1.

Snapshot

13.7.2.

Overview

13.7.3.

Offerings

13.7.4.

Financial

Insight

13.7.5.

Recent

Developments

13.8.

TUV Nord Group

13.8.1.

Snapshot

13.8.2.

Overview

13.8.3.

Offerings

13.8.4.

Financial

Insight

13.8.5.

Recent

Developments

13.9.

TUV Rheinland

13.9.1.

Snapshot

13.9.2.

Overview

13.9.3.

Offerings

13.9.4.

Financial

Insight

13.9.5.

Recent

Developments

13.10.

TUV SUD

13.10.1.

Snapshot

13.10.2.

Overview

13.10.3.

Offerings

13.10.4.

Financial

Insight

13.10.5.

Recent

Developments

14. Appendix

14.1. Exchange Rates

14.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Europe TIC Market for Sports and Entertainment Industry