GPU as a Service Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Component (Solution, Services), by Pricing Model (Pay per use, Subscription based plans), by Organization Size (Small and medium enterprises, Large enterprises), by Vertical (IT and telecom, BFSI, Media and entertainment, Gaming, Automotive, Healthcare)

| Status : Published | Published On : May, 2026 | Report Code : VRSME9210 | Industry : Semiconductor & Electronics | Available Format :

|

Page : 135 |

GPU as a Service Market Overview

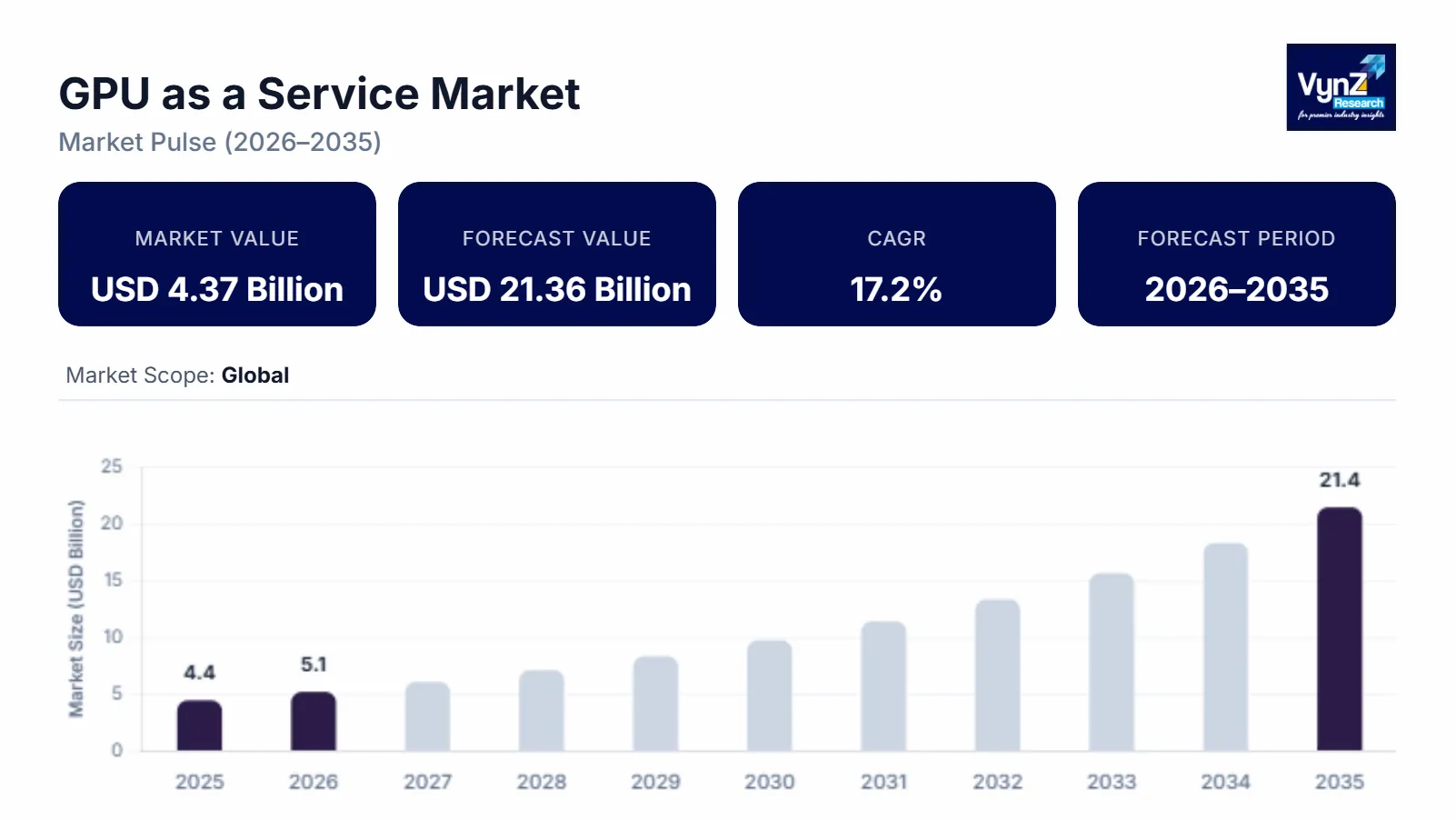

The GPU as a Service market which was valued at approximately USD 4.37 billion in 2025 and is estimated to rise further up to almost USD 5.12 billion by 2026, is projected to reach around USD 21.36 billion in 2035, expanding at a CAGR of about 17.2% during the forecast period from 2026 to 2035.

Market growth is driven by rising demand for AI and machine learning workloads, increasing adoption of cloud-based GPU virtualization and rapid expansion of high-performance computing infrastructure, along with increasing adoption of scalable compute on demand solutions. Rising demand for AI model training, real time analytics and graphics intensive computing workloads and ongoing investments in digital infrastructure development and national level AI computing initiatives are further supporting market expansion across major regions including North America, Europe, and Asia Pacific.

GPU as a Service Market Dynamics

Market Trends

The industry is seeing some real shifts in how cloud-based compute is adopted and how enterprise level AI infrastructure is actually being used. A standout trend is the quick move toward on demand GPU virtualization for cost efficiency and scalability and flexibility for high performance computing tasks. Another trend is the integration of AI optimized cloud architectures together with edge-based GPU deployment models, pushed by rapid changes in artificial intelligence frameworks and distributed computing systems that are evolving fast. Product lineups are getting reshaped and companies are leaning harder into integrated AI cloud ecosystems, multi-tenant GPU platforms and workload optimized infrastructure solutions.

Growth Drivers

The market is mostly powered by growing demand for artificial intelligence and machine learning workloads, which keeps creating steady needs across enterprise computing and research heavy application environments. More investments in hyperscale data centers and cloud infrastructure expansion are giving the market additional momentum. Greater need from high performance computing and real time data processing requirements pushes enterprises to prioritize cost optimization, faster model training and flexible compute access, needing GPU based cloud services. Government backed digital infrastructure initiatives and national AI development programs are increasing large scale compute and expand cloud ecosystem reach.

Market Restraints / Challenges

Even with strong growth signals, the market still has challenges that can slow down expansion. High infrastructure costs and GPU hardware dependency like supply chain constraints and semiconductor availability fluctuations are continuing to limit profitability and deployment scalability, especially for small and medium enterprises. The issue of data security and compliance complexity becomes operational heavy for cloud service providers. Dependence on advanced semiconductor manufacturing ecosystems and specialized GPU architecture supply chains create cost pressure, procurement delays, and scalability limits.

Market Opportunities

The market shows opportunities in AI driven cloud computing expansion due to demand for scalable machine learning infrastructure and ongoing enterprise digital transformation. Providers that offer flexible, pay per use GPU cloud solutions will get more business from startups, research groups and enterprise AI developers. Another opportunity is edge AI integration and hybrid cloud deployment models with more investment in distributed computing and real time analytics for better efficiency and improved performance delivery.

Global GPU as a Service Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 4.37 Billion |

|

Revenue Forecast in 2035 |

USD 21.36 Billion |

|

Growth Rate |

17.2% |

|

Segments Covered in the Report |

Component, Pricing Model, Organization Size, Vertical |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Arm Limited, Amazon Web Services Inc., Fujitsu, HCL Technologies Limited, IBM Corporation, Intel Corporation, Microsoft, NVIDIA Corporation, Oracle, Qualcomm Technologies, Inc. |

|

Customization |

Available upon request |

GPU as a Service Market Segmentation

By Component

In 2025, solution made up the biggest portion of the market, roughly 61% of total revenue due to high performance cloud computing and the integrated AI jobs deployed. The segment gets momentum from adoption across data intensive industries, especially where flexible compute provisioning matters and where cutting capital expenditure is crucial. As hyperscale cloud providers get used more along with AI driven digital transformation programs, demand is reinforced across global organizations.

Services are projected to grow the quickest, with an estimated CAGR of 18.4% from 2026 to 2035 due to the rising interest in managed GPU offerings, cloud orchestration support and consulting style optimization solutions. AI model training ecosystems are expanding and more startups and SMEs are turning to outsourced infrastructure management, which is pushing the segment higher.

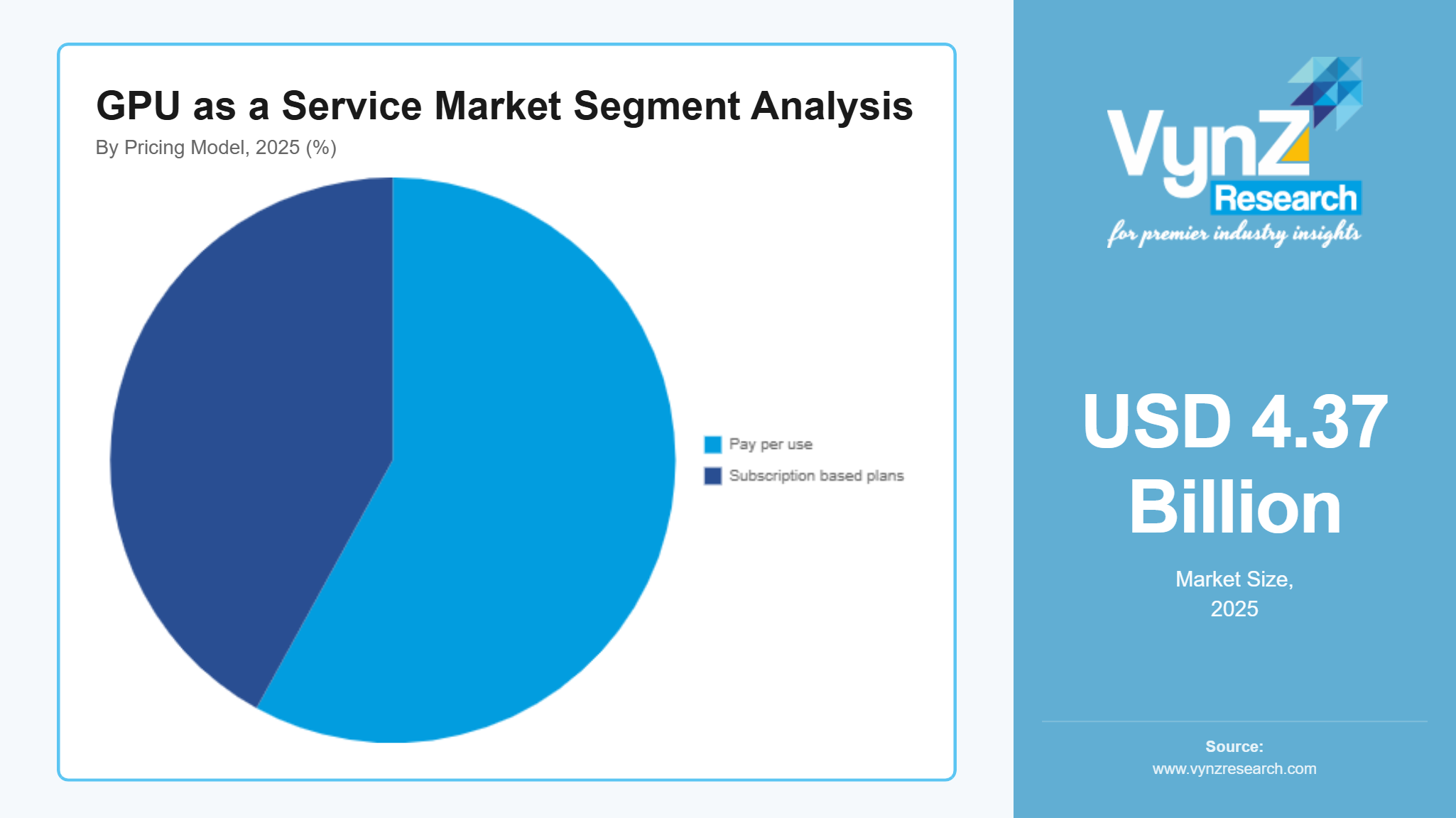

By Pricing Model

Pay per use made up the largest share of the market in 2025 with about 58% of total revenue due to flexible billing structures, workload-based cost efficiency and strong uptake for AI development, simulation, and cloud gaming. Many enterprises keep choosing it because scaling is easier and upfront infrastructure investment can stay lower.

Subscription based plans are expected to see the fastest growth, with an estimated CAGR of 17.9% during 2026 to 2035 supported by cost predictability, stronger enterprise budgeting discipline and growing demand for longer term GPU resource allocation. When tiered subscription approaches connect with performance optimized cloud GPU offerings it tends to boost adoption, especially in big organizations and research institutions.

By Organization Size

Large enterprises accounted for the largest share in 2025, about 64% of total revenue due to extensive AI workload deployment, massive data processing needs and their ability to fund advanced cloud computing infrastructure. They keep leading adoption across analytics, automation and high-performance simulation workloads.

Small and medium enterprises are expected to register the fastest growth, estimated CAGR of 19.2% from 2026 to 2035. As they are becoming more accessible, infrastructure barriers are being lowered, and AI enabled business models are spreading. Cost effective pay per use access lets SMEs scale computing power without needing heavy capital spending.

By Vertical

IT and telecom held the largest share of the market in 2025, representing around 27% of total revenue. This dominance seems driven by strong cloud adoption, network virtualization and the increasing integration of AI powered data processing systems. Ongoing expansion of digital infrastructure and enterprise level cloud migration is also continuously strengthening demand inside this vertical.

Gaming is expected to grow fastest, with an estimated CAGR of 20.1% during 2026 to 2035 due to rising demand for cloud gaming platforms, real time rendering technologies and more immersive user experiences. Healthcare is also showing notable expansion, supported by AI based diagnostics, medical imaging workloads and advanced computational research applications.

Regional Insights

North America

North America accounted for approximately 38% of the market in 2025, driven by strong hyperscale cloud infrastructure, early AI adoption and high concentration of technology enterprises across the United States and Canada. Major innovation hubs such as Silicon Valley, Seattle, and Toronto continue to support large scale deployment of GPU intensive workloads. Government backed initiatives focused on artificial intelligence development, semiconductor advancement, and digital infrastructure expansion are further strengthening regional competitiveness. Increasing enterprise demand for high performance computing, combined with rapid expansion of cloud service providers, is accelerating adoption of GPU based services across industries including IT, BFSI, and healthcare.

Asia Pacific

The Asia Pacific market is witnessing steady and rapid growth due to strong industrial digitization, expanding cloud ecosystems, and large-scale AI adoption across China, India, Japan, and South Korea. The region accounted for approximately 29% of the market in 2025, supported by increasing investments in data center infrastructure and rising demand for cost efficient computing solutions. Government initiatives such as national AI strategies, digital economy programs and semiconductor manufacturing support are accelerating adoption across enterprises. Growing usage in gaming, automotive, and e commerce sectors is further driving consistent demand across both developed and emerging economies.

Europe

Growth in Europe is supported by strong regulatory alignment around data security, increasing investments in AI research, and modernization of enterprise IT infrastructure across Germany, the United Kingdom, France and the Nordic countries. The region accounted for approximately 18% of the market in 2025, driven by rising adoption of cloud based HPC systems and sustainability focused data center initiatives. Government backed digital transformation programs and AI innovation funding frameworks are encouraging enterprises to adopt advanced GPU computing solutions. Expanding use across automotive engineering, healthcare analytics, and financial services is further strengthening regional market penetration.

Rest of the World

Latin America, Middle East and Africa collectively accounted for approximately 15% of the market in 2025, driven by gradual cloud adoption, expanding telecom infrastructure and increasing digital transformation initiatives. Growth in countries such as Brazil, Mexico, South Africa and the Gulf economies is supported by rising investments in data centers and enterprise modernization programs. Government led initiatives focusing on digital economy expansion, smart city development, and ICT infrastructure improvement are further supporting market entry for global cloud providers.

Competitive Landscape / Company Insights

The market is moderately to highly competitive, with the presence of global cloud providers and specialized GPU infrastructure companies focusing on service innovation, pricing optimization and expansion of high-performance computing capacity. Companies are increasingly investing in advanced AI infrastructure development, cloud orchestration capabilities and scalable data center ecosystems to strengthen their market position. Government supported digital transformation programs, national AI strategies, and semiconductor ecosystem initiatives are further influencing competitive dynamics and encouraging capacity expansion across major regions.

Mini Profiles

Amazon Web Services Inc. focuses on cloud computing infrastructure and GPU as a Service solution, supported by strong global distribution strength and extensive hyperscale data center network enabling scalable enterprise level AI workloads across industries.

Arm Limited operates in premium semiconductor architecture segments, emphasizing energy efficient chip design and advanced processing frameworks that support high performance computing ecosystems and enable next generation AI and cloud computing capabilities globally.

Fujitsu leverages strategic partnerships and enterprise digital solutions to expand market presence, focusing on integrated IT services, cloud infrastructure, and high-performance computing systems tailored for industrial and government applications.

HCL Technologies Limited focuses on IT services and cloud engineering solutions, supported by strong cost efficiency and global delivery model enabling scalable digital transformation and enterprise grade GPU computing adoption across multiple sectors.

IBM Corporation operates in premium enterprise technology segments, emphasizing hybrid cloud architecture, AI driven computing solutions, and advanced analytics platforms designed for large scale enterprise modernization and digital transformation initiatives.

Key Players

- Arm Limited

- Amazon Web Services, Inc.

- Fujitsu

- HCL Technologies Limited

- IBM Corporation

- Intel Corporation

- Microsoft

- NVIDIA Corporation

- Oracle

- Qualcomm Technologies, Inc.

Recent Developments

In August 2025, Intel Corporation announced expansion of its AI focused data center GPU and accelerator portfolio to strengthen high performance computing capabilities. The initiative is aimed at improving cloud workload efficiency and enterprise AI adoption, supported by increasing demand from hyperscale cloud providers and government backed digital infrastructure programs.

In January 2026, Microsoft enhanced its Azure cloud platform with upgraded GPU enabled AI infrastructure designed for large scale model training and deployment. The development strengthens hybrid cloud adoption and enterprise level AI integration, driven by rising demand for scalable computing solutions across global industries.

In December 2025, NVIDIA Corporation expanded its next generation AI GPU architecture to support advanced generative AI and high-performance computing workloads. The development focuses on improving processing efficiency for data centers and cloud service providers, supported by strong demand from enterprise AI ecosystems and research institutions.

In November 2025, Oracle upgraded its cloud infrastructure services by integrating enhanced GPU based computing capabilities for enterprise AI workloads. The improvement supports growing demand for real time analytics and scalable AI model deployment, driven by increasing digital transformation across finance, healthcare, and public sector organizations.

In September 2025, Qualcomm Technologies Inc. strengthened its AI and edge computing portfolio through advanced GPU enabled chip solutions for automotive and mobile applications. The development focuses on energy efficient high-performance processing, supported by rising adoption of connected devices and intelligent mobility ecosystems.

Global GPU as a Service Market Coverage

Component Insight and Forecast 2026 - 2035

- Solution

- Services

Pricing Model Insight and Forecast 2026 - 2035

- Pay per use

- Subscription based plans

Organization Size Insight and Forecast 2026 - 2035

- Small and medium enterprises

- Large enterprises

Vertical Insight and Forecast 2026 - 2035

- IT and telecom

- BFSI

- Media and entertainment

- Gaming

- Automotive

- Healthcare

Global GPU as a Service Market by Region

- North America

- By Component

- By Pricing Model

- By Organization Size

- By Vertical

- By Country - U.S., Canada, Mexico

- Europe

- By Component

- By Pricing Model

- By Organization Size

- By Vertical

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Component

- By Pricing Model

- By Organization Size

- By Vertical

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Component

- By Pricing Model

- By Organization Size

- By Vertical

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for GPU as a Service Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Component

1.2.2. By

Pricing Model

1.2.3. By

Organization Size

1.2.4. By

Vertical

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Component

5.1.1. Solution

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Services

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.2. By Pricing Model

5.2.1. Pay per use

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Subscription based plans

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Organization Size

5.3.1. Small and medium enterprises

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Large enterprises

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By Vertical

5.4.1. IT and telecom

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. BFSI

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Media and entertainment

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Gaming

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Automotive

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

5.4.6. Healthcare

5.4.6.1. Market Definition

5.4.6.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Component

6.2. By

Pricing Model

6.3. By

Organization Size

6.4. By

Vertical

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Component

7.2. By

Pricing Model

7.3. By

Organization Size

7.4. By

Vertical

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Component

8.2. By

Pricing Model

8.3. By

Organization Size

8.4. By

Vertical

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Component

9.2. By

Pricing Model

9.3. By

Organization Size

9.4. By

Vertical

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Arm Limited

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Amazon Web Services, Inc.

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Fujitsu

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

HCL Technologies Limited

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

IBM Corporation

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Intel Corporation

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Microsoft

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

NVIDIA Corporation

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Oracle

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Qualcomm Technologies, Inc.

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

GPU as a Service Market