India Semiconductor Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Component (Memory Devices, Logic Devices, Microprocessors & Microcontrollers, Analog ICs, Discrete Power Devices, Sensors, Optoelectronics), by Node Size (<10 nm, >10 to 28 nm, >28 to 65 nm, >65 nm), by Material Type (Silicon, Silicon Carbide, Gallium Nitride, Gallium Arsenide), by Manufacturing Type (Fabless, Foundry, Integrated Device Manufacturer, OSAT / ATMP), by Application (Consumer Electronics, Automotive, IT & Telecommunications, Industrial, Healthcare, Aerospace & Defense)

| Status : Published | Published On : Feb, 2026 | Report Code : VRSME9196 | Industry : Semiconductor & Electronics | Available Format :

|

Page : 135 |

India Semiconductor Market Overview

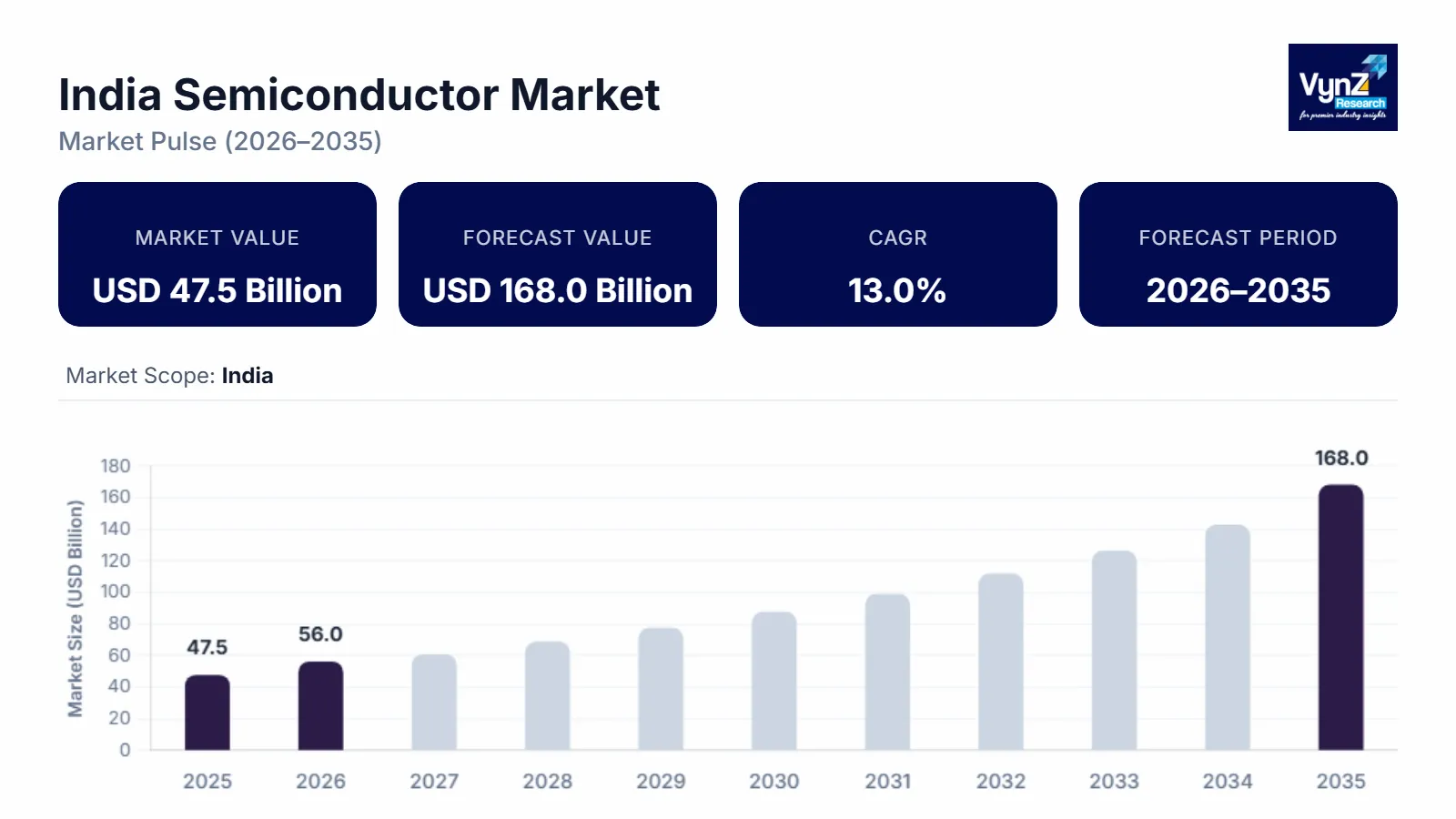

The India semiconductor market which was valued at approximately USD 47.5 billion in 2025 and is estimated to reach around USD 56.0 billion in 2026, is projected to reach close to USD 168.0 billion by 2035, expanding at a CAGR of about 13.0% during the forecast period from 2026 to 2035.

The India semiconductor market is primarily driven by rapid digital transformation across industries, supported by strong government initiatives and rising domestic demand for electronics. India Semiconductor Mission, a program of the Ministry of Electronics and Information Technology (MeitY), is hastening investments in chip production, packaging, and design systems. The rising demand of smartphone manufacture, consumer electronics, and automotive electronics, especially the rising demand of electric vehicles and hi-tech driver-assistance systems, has also contributed greatly to the use of semiconductors in the nation. The drive of India towards 5G implementation, data centers, and IoT enabled infrastructure is also increasing the pressure on high performance chips and connectivity solutions. Moreover, the high concentration of talent in the chip design and embedded system in the country has also made India a global location of semiconductor design services. The increasing global localization, diversification of supply chains through non-dependence on one country and production-linked incentive schemes (PLI) are also showing that global players are investing in fabrication and assembly plants. All these structural, policy driven and demand side factors are forming the foundation of an excellent growth path of the India semiconductor market.

Market Dynamics

Market Trends

Rising investments in chip fabrication and ATMP (Assembly, Testing, Marking, and Packaging) facilities are reshaping India’s semiconductor landscape by moving the country beyond its traditional role as a design hub toward becoming a manufacturing base. Under the India Semiconductor Mission, the government is providing substantial fiscal support to attract both domestic conglomerates and global semiconductor firms to set up fabs and advanced packaging units. Several large-scale proposals for wafer fabrication plants and outsourced semiconductor assembly and test (OSAT) facilities have been announced across states such as Gujarat and Assam, signaling regional industrial development. The government reported that 10 semiconductor projects across six states have been approved under ISM, with total committed investments of about ₹1.60 lakh crore (USD 18+ billion), reflecting large-scale private + public capital mobilisation for fabs, SiC/substrate projects and ATMP units. These investments are aimed at reducing India’s heavy reliance on imported chips, which currently account for a major share of electronics production costs. The focus on ATMP facilities is particularly strategic, as packaging and testing require relatively lower capital intensity compared to full-scale fabs while still strengthening supply chain resilience.

Growth Drivers

One of the biggest contributors to India semiconductor market is rapid development in electronics manufacturing since India is now one of the fastest developing centers of smartphone and consumer electronics manufacturing. The government has been promoting the development of large scale assembly and manufacturing plants in the country by creating schemes like the Make in India and the Production-Linked Incentive (PLI) scheme which has attracted both international manufacturers and internal manufacturers to establish large scale production and assembly facilities. India has undergone a major boom in production of mobile phones, IT hardware, television, and wearable devices and this has become a source of more processors, memory chips, display driver and power management semiconductors. The growth of electronic manufacturing hubs and better supply chain systems have also added to the strength of the domestic production. Tata Electronics Private Limited (India), in partnership with PSMC (Taiwan), is developing the Dholera semiconductor fab with a total project investment of approximately ₹91,000 crore (around USD 11 billion). The Government of India, under the India Semiconductor Mission (MeitY), is providing up to 50% fiscal support of the eligible project cost, which means central support could be around ₹45,000 crore (approx.), subject to approved cost components. With the current growth in exports of the electronic products, the consumption of the semiconductor is also growing in the same direction. The localization of the components is also being promoted, which is promoting the backward integration into the packaging and the manufacturing of semiconductor. Such a sustained growth in the electronics industry is generating a solid and stable base of demand of semiconductors in various segments of application.

Market Restraints / Challenges

The most critical threat to the India semiconductor market is high capital intensity of fabrication plant since establishing a semiconductor fab usually consumes between USD 5 billion and above USD 15 billion investment based on the technology node. This is augmented with a lithography machine, cleanroom infrastructure, ultra-pure water systems, power that is not interrupted, and extremely specialized manufacturing equipment. Moreover, semiconductor fabs must be upgraded continuously to be technologically competitive and incur even more costly long-term capital expenditure. In the case of a nascent semiconductor ecosystem such as India, to move such a scale of investments, there is the heavy government subsidization, policy predictability, and business trust in the system. The financial risk is also high as the semiconductor demand is cyclical and vulnerable to the international economic changes. The long gestation periods before commercial production are realised increases the concerns of investors in relation to their returns on investment. This has given rise to high enterability barriers and slows down the rate at which India can set up large-scale and sophisticated semiconductor production facilities.

Market Opportunities

The India semiconductor market is getting a good opportunity due to the growth of electric cars (EVs) and automotive electronics as the modern cars are highly dependent on the advanced semiconductor parts. EVs need considerably more chips than the conventional internal combustion engine cars, especially those related to battery management systems, power electronics, inverters, and onboard charging units. The Government of India, under the PM E-DRIVE Scheme, has allocated ₹2,000 crore specifically for public EV charging infrastructure to strengthen urban and highway charging networks. As of recent data, India has installed 39,485 public EV chargers, including 8,414 fast chargers, supporting large-scale EV adoption. Additionally, the PM e-Bus Sewa-PSM Scheme with a budget of ₹3,435 crore aims to deploy over 38,000 electric buses, further accelerating EV ecosystem growth. The demand of microcontrollers, sensors, and power semiconductors is also increasing owing to the growing use of advanced driver-assistance systems (ADAS), infotainment and connected car technologies. Government programs encouraging the use of EVs, including incentive programs and localization, are rapidly increasing vehicle production at home and increasing the use of semiconductors. Moreover, the transition into the electric mobility is raising the demand in silicon carbide (SiC) and other high-efficiency power semiconductor materials. The Government of India, through the Ministry of Heavy Industries, launched the National Programme on Advanced Chemistry Cell (ACC) with a PLI outlay of ₹18,100 crore. The scheme aims to establish around 50 GWh of domestic advanced battery manufacturing capacity in India. With the growth of local production by automotive manufacturers and investment in next-generation mobility solutions, semiconductor integration per vehicle is increasing. Such a lasting expansion of the ecosystem of automotive and EV offers a long-term demand prospect to the fledgling semiconductor production and packaging sector in India.

India Semiconductor Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 47.5 Billion |

|

Revenue Forecast in 2035 |

USD 168.0 Billion |

|

Growth Rate |

13.0% |

|

Segments Covered in the Report |

Component, Node Size, Material Type, Manufacturing Type, Application |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

South, West, North, East |

|

Key Companies |

Intel Corporation, Advanced Micro Devices, Inc., NVIDIA Corporation, Qualcomm Incorporated, Texas Instruments Incorporated, Micron Technology, Inc., Taiwan Semiconductor Manufacturing Company Limited, Samsung Electronics Co., Ltd., SK Hynix Inc., Tata Electronics Private Limited, Vedanta Limited, ASM Technologies Limited |

|

Customization |

Available upon request |

Market Segmentation

By Component

Memory Devices is the largest category with a market share of about 25% in 2025, because the manufacturing of smartphones, data center, and consumer electronics grows swiftly throughout India. DRAM and NAND are memory chips that are required by mobile devices, cloud storage and computing systems in enterprises. The growth of online service, on-the-top (OTT) application, and enterprise data storage needs are placing a strong demand on memory capacity solutions with high capacity. Also, expansion of local electronics assembly through incentive measures by the government is enhancing mass acquisition of memory parts. Memory devices are a stable and high-volume segment since they are utilized in virtually all electronic products. Thus, they are the most popular types of components in the Indian semiconductor market due to their wide application and demand in all industries.

Discrete Power Devices is the fastest-growing category with a CAGR of 13.2% during the forecast period, as the demand is increased by electric vehicles (EVs), renewable energy systems, and automation in industries. MOSFETs, IGBTs and silicon carbide power devices are essential in the realization of power management that could be energy efficient. As India is moving fast towards EV and has begun to install many solar power systems, the demand on power control components that are efficient is growing. Moreover, electrification of industries and creation of smart grids is favoring increased utilization of discrete components. These are the factors leading to investment in high-technology power semiconductor. This section will experience the highest growth momentum since the need to conserve energy is a national priority.

By Node Size

28–65 nm is the largest category with a market share of about 35% in 2025, as it serves a wide range of applications including automotive electronics, industrial systems, and consumer devices. Mature-node technologies are cost-effective and highly reliable, making them ideal for microcontrollers, power management ICs, and communication chips. Since India’s semiconductor demand is largely driven by automotive, telecom, and industrial segments, these nodes remain dominant. Additionally, most domestic manufacturing proposals initially focus on mature nodes due to lower complexity compared to advanced nodes. The broad industrial usability and affordability of this node range support its leadership position. Therefore, 28–65 nm technology remains the backbone of India’s semiconductor consumption profile.

<10 nm is the fastest-growing category with a CAGR of 13.6% during the forecast period, driven by increasing demand for high-performance computing, 5G infrastructure, and AI-enabled devices. Advanced node chips provide higher speed, lower power consumption, and improved processing capabilities. As India expands digital infrastructure and cloud computing capacity, demand for cutting-edge processors is accelerating. Multinational companies operating R&D centers in India are also contributing to advanced chip design demand. These performance advantages and digital transformation trends are fueling rapid growth in this node category.

By Material Type

Silicon (Si) is the largest category with a market share of about 80% in 2025, since it is used in most of the semiconductor equipment. The logic chip, memory devices, and analog IC are all made using silicon since it is economical and has been proven to be easy to fabricate. The silicon-based components are the main components in the electronics manufacturing ecosystem of India. Its dominance is also enhanced by the existence of mature technology in processing and global supply chains. This category of material faces a dominant market share in the market since the majority of consumer and industrial uses depend on silicon wafers.

Silicon Carbide (SiC) is the fastest-growing category during the forecast period, due to its high-voltage and high temperature efficiency. SiC finds application in electric cars, renewable energy converters, and power plants. With the adoption of the electric vehicles (EV) and the growth of clean energy in India, the demand of the high-performance power semiconductors is increasing. SiC devices are more energy efficient and compact to design system than silicon traditionally used. This material segment is rapidly investing in and adopting these technological benefits.

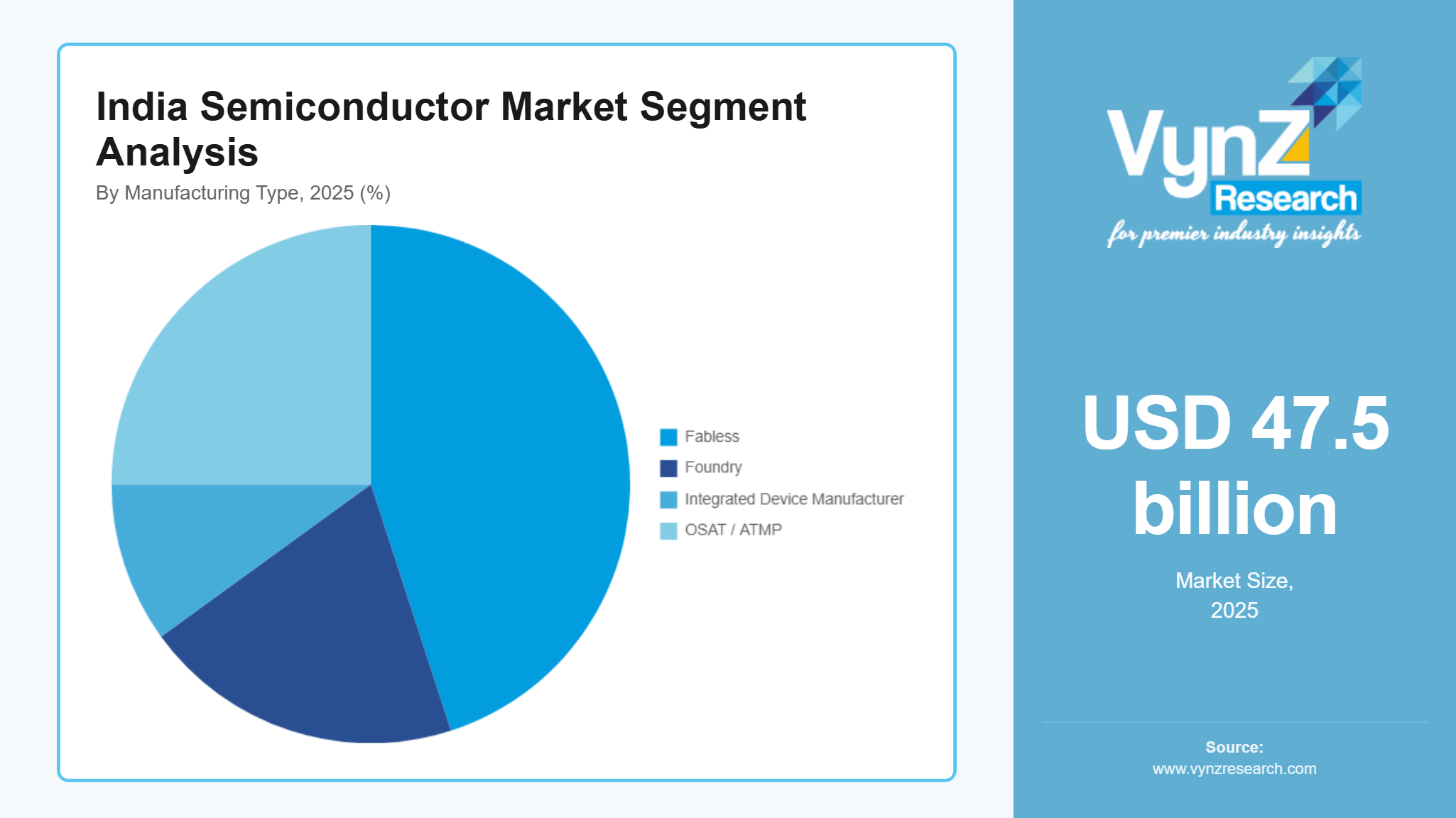

By Manufacturing Type

Fabless is the largest category with a market share of about 45% in 2025, as India has historically been a strong semiconductor design hub rather than a fabrication hub. Many domestic startups and global companies operate design and R&D centers in India without owning fabrication facilities. The country’s large pool of chip design engineers supports innovation in telecom, automotive, and consumer electronics chips. Since manufacturing is largely outsourced abroad, fabless companies dominate the ecosystem. Therefore, India’s semiconductor landscape is primarily design-driven, supporting the leadership of the fabless model.

OSAT / ATMP is the fastest-growing category during the forecast period, due to rising government incentives and comparatively lower capital requirements than full-scale fabs. Assembly, testing, marking, and packaging facilities are being prioritized to strengthen domestic value addition. These units help reduce import dependency and improve supply chain resilience. As India positions itself as an alternative global manufacturing destination, ATMP investments are accelerating. This makes OSAT/ATMP the fastest-growing manufacturing segment.

By Application

Consumer Electronics is the largest category with a market share of about 35% in 2025, due to the huge output of smartphone production in India and the increase in demand on televisions, laptops, and wearable gadgets. The production-based incentive programs have greatly spread consumer electronics production. These gadgets have processors, memory chips, display drivers, and connectivity ICs in huge quantities. This dominance of this segment is further enhanced by the magnitude of personal consumption and exports. Thus, consumer electronics is considered the main driver of demand of semiconductors in India.

Automotive is the fastest-growing category with a CAGR of 13.3% during the forecast period, because of the growing electric vehicle manufacture and the increasing integration of semiconductors per vehicle. The contemporary cars are equipped with chips to handle the battery, infotainment, safety and connectivity. The policies of government incentives on the adoption of EVs and localization are driving a rapid growth in the demand of automotive electronics. With the increased software-driven and electrified vehicles every day, the amount of semiconductor content in each vehicle is increasing. This is a structural change that is favourable to high growth in the automotive application segment.

Regional Insights

South

South is the largest regional market with a share of approximately 35% in 2025, driven by its strong concentration of semiconductor design centers, electronics manufacturing clusters, and established IT infrastructure. Karnataka and Tamil Nadu host major global semiconductor R&D facilities and chip design operations, particularly in Bengaluru and Chennai. The region benefits from a highly skilled engineering workforce, strong academic-industry collaboration, and a mature electronics ecosystem. The Indichip Semiconductors – Yitoa Micro Technology (Japan) partnership to establish a ₹14,000 crore silicon carbide (SiC) wafer fabrication plant in Kurnool, Andhra Pradesh directly strengthens India’s semiconductor manufacturing base. In addition, large-scale mobile phone and consumer electronics manufacturing units are concentrated in Tamil Nadu, increasing semiconductor demand. Telangana is also emerging as a semiconductor innovation hub through government-backed incentives and fabless startup promotion. The combination of design leadership, manufacturing activity, and policy support makes South India the dominant contributor to the domestic semiconductor ecosystem.

West

West is the fastest-growing region during the forecast period, primarily due to major semiconductor fabrication and ATMP investments. Gujarat has emerged as a key destination for large-scale semiconductor projects supported by state and central government incentives. The development of industrial corridors, port connectivity, and power infrastructure is strengthening the region’s attractiveness for capital-intensive semiconductor manufacturing. Maharashtra also contributes through electronics production and technology-driven industrial growth. The Electronics Component Manufacturing Scheme (₹22,919 crore, announced May 2025) directly supports semiconductor ecosystem development by promoting local manufacturing of components, specialty chemicals, gases, substrates, and other critical inputs required for fabs and ATMP units. As new fabrication and packaging facilities progress toward operational stages, West India’s semiconductor output is expected to expand significantly. The region’s policy-driven investment momentum and infrastructure readiness position it as the fastest-growing semiconductor hub in the country.

North

North is significant in the demand generation of semiconductor products, especially in consumer electronics production, deployment of telecommunication infrastructure and military applications. The state of Uttar Pradesh has formed significant mobile production belts, and semiconductor parts are used more. Government institutions, defense research bodies and the rolling out of 5G networks are also a plus to the region. The HCL–Foxconn joint venture fab near Jewar Airport, Uttar Pradesh, approved with ₹37.06 billion (₹3,706 crore) government support under the India Semiconductor Mission (ISM), is a semiconductor fabrication project focused on producing 36 million display driver chips per month, with commercial production. The regional supply chain is also being consolidated slowly due to policy programs to lure electronics manufacturing. Furthermore, the fabrication capacity is small, the increasing electronics manufacturing hub promotes the consistent growth in the demand of semiconductor in North India. targeted for 2027.

East

East is a new area in the field of semiconductor enabled by the rising industrial infrastructure and digital uptake. Odisha and West Bengal among other states are also experiencing slow rise of electronics assembly and IT based services. Despite the fact the region has a smaller market share in comparison to South and West India, the growth of semiconductor consumption is predicted due to the growth of investment in industrial automation and the rise of digital connectivity. The government's ambitious target of 30% EV penetration by 2030 necessitates substantial semiconductor content, as modern EVs require 20–30% more semiconductor components than conventional vehicles. The infrastructure development and skill improvement initiatives by the government are slowly establishing the base in the future participation in the semiconductor ecosystems. On the long-term, East India will increase its contribution by establishing downstream electronics production and industrial growth that is based on technology.

Competitive Landscape / Company Insights

The India semiconductor market is largely consolidated in nature, particularly in such fields as chip fabrication, advanced processors, and memory technologies, where only a small number of global players are highly dominant. A semiconductor fab is a high-capital equipment, high-technology, and highly technical business, which means that only a few companies can afford to venture into this area. The large multinational corporations or big domestic industrial groups are leading most of the major projects in India with the government support. The intensity of competition is still focused on a small group of established competitors with solid financial and technological resources. This framework enhances sustained concentration of the market and barriers to new entrants.

Mini Profiles

Intel Corporation is an international semiconductor giant in microprocessors, data center chips and advanced manufacturing technologies, and with robust design and research and development practices in India, it contributes to innovation and development of next-generation processors all over the world.

Advanced Micro Devices, Inc. develops high-performance CPUs, GPUs, and adaptive computing solutions for data centers, gaming, and embedded applications, leveraging India-based engineering talent to enhance chip design and software optimization.

NVIDIA Corporation specialises in graphics processing units (GPUs), AI accelerators, and high-performance computing platforms, and has a substantial presence in India in the area of R&D, which has been used to develop artificial intelligence, automotive computing, and data centres.

Qualcomm Incorporated designs advanced mobile chipsets, 5G modems, and wireless communication semiconductors, playing a key role in India’s smartphone ecosystem and next-generation connectivity infrastructure.

Texas Instruments Incorporated is the manufacturer of analog semiconductors and embedded processors, which are applied in the production of automotive, industrial, and consumer electronics and are serving the expanding electronics manufacturing and automation industry in India.

Key Players

- Intel Corporation

- Advanced Micro Devices, Inc.

- NVIDIA Corporation

- Qualcomm Incorporated

- Texas Instruments Incorporated

- Micron Technology, Inc.

- Taiwan Semiconductor Manufacturing Company Limited

- Samsung Electronics Co., Ltd.

- SK Hynix Inc.

- Tata Electronics Private Limited

- Vedanta Limited

- ASM Technologies Limited

Recent Developments

January 2026 – Tata Electronics Private Limited announced progress on its semiconductor fabrication facility in Gujarat, confirming the commencement of advanced site preparation and equipment procurement to support domestic chip manufacturing under the India Semiconductor Mission.

December 2025 – Micron Technology, Inc. expanded its assembly, testing, marking, and packaging (ATMP) operations in India, strengthening local memory packaging capabilities and accelerating workforce hiring for advanced semiconductor processing roles.

October 2025 – Vedanta Limited entered into a new technology collaboration agreement with an international semiconductor equipment provider to accelerate the development of its proposed fabrication facility and enhance process technology readiness.

August 2025 – Intel Corporation expanded its semiconductor design and validation operations in Bengaluru, focusing on next-generation AI processors and advanced node chip architecture development.

June 2025 – Qualcomm Incorporated announced increased investment in its India-based R&D centers to accelerate 5G chipset innovation and support the growing demand for locally manufactured smartphones and connected devices.

India Semiconductor Market Coverage

Component Insight and Forecast 2026 - 2035

- Memory Devices

- Logic Devices

- Microprocessors & Microcontrollers

- Analog ICs

- Discrete Power Devices

- Sensors

- Optoelectronics

Node Size Insight and Forecast 2026 - 2035

- <10 nm

- >10 to 28 nm

- >28 to 65 nm

- >65 nm

Material Type Insight and Forecast 2026 - 2035

- Silicon

- Silicon Carbide

- Gallium Nitride

- Gallium Arsenide

Manufacturing Type Insight and Forecast 2026 - 2035

- Fabless

- Foundry

- Integrated Device Manufacturer

- OSAT / ATMP

Application Insight and Forecast 2026 - 2035

- Consumer Electronics

- Automotive

- IT & Telecommunications

- Industrial

- Healthcare

- Aerospace & Defense

India Semiconductor Market by Region

- South

- By Component

- By Node Size

- By Material Type

- By Manufacturing Type

- By Application

- West

- By Component

- By Node Size

- By Material Type

- By Manufacturing Type

- By Application

- North

- By Component

- By Node Size

- By Material Type

- By Manufacturing Type

- By Application

- East

- By Component

- By Node Size

- By Material Type

- By Manufacturing Type

- By Application

Table of Contents for India Semiconductor Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Component

1.2.2. By

Node Size

1.2.3. By

Material Type

1.2.4. By

Manufacturing Type

1.2.5. By

Application

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. India Market Estimate and Forecast

4.1. India Market Overview

4.2. India Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Component

5.1.1. Memory Devices

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Logic Devices

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Microprocessors & Microcontrollers

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Analog ICs

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Discrete Power Devices

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.1.6. Sensors

5.1.6.1. Market Definition

5.1.6.2. Market Estimation and Forecast to 2035

5.1.7. Optoelectronics

5.1.7.1. Market Definition

5.1.7.2. Market Estimation and Forecast to 2035

5.2. By Node Size

5.2.1. <10 nm

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. >10 to 28 nm

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. >28 to 65 nm

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. >65 nm

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.3. By Material Type

5.3.1. Silicon

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Silicon Carbide

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Gallium Nitride

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Gallium Arsenide

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.4. By Manufacturing Type

5.4.1. Fabless

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Foundry

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Integrated Device Manufacturer

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. OSAT / ATMP

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.5. By Application

5.5.1. Consumer Electronics

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Automotive

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. IT & Telecommunications

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Industrial

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

5.5.5. Healthcare

5.5.5.1. Market Definition

5.5.5.2. Market Estimation and Forecast to 2035

5.5.6. Aerospace & Defense

5.5.6.1. Market Definition

5.5.6.2. Market Estimation and Forecast to 2035

6. South Market Estimate and Forecast

6.1. By

Component

6.2. By

Node Size

6.3. By

Material Type

6.4. By

Manufacturing Type

6.5. By

Application

7. West Market Estimate and Forecast

7.1. By

Component

7.2. By

Node Size

7.3. By

Material Type

7.4. By

Manufacturing Type

7.5. By

Application

8. North Market Estimate and Forecast

8.1. By

Component

8.2. By

Node Size

8.3. By

Material Type

8.4. By

Manufacturing Type

8.5. By

Application

9. East Market Estimate and Forecast

9.1. By

Component

9.2. By

Node Size

9.3. By

Material Type

9.4. By

Manufacturing Type

9.5. By

Application

10. Company Profiles

10.1.

Intel Corporation

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Advanced Micro Devices, Inc.

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

NVIDIA Corporation

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Qualcomm Incorporated

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Texas Instruments Incorporated

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Micron Technology, Inc.

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Taiwan Semiconductor Manufacturing Company Limited

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Samsung Electronics Co., Ltd.

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

SK Hynix Inc.

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Tata Electronics Private Limited

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

Vedanta Limited

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

10.12.

ASM Technologies Limited

10.12.1.

Snapshot

10.12.2.

Overview

10.12.3.

Offerings

10.12.4.

Financial

Insight

10.12.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

India Semiconductor Market