Pneumatic Deluge Valve Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Type (Pneumatic deluge valves, Electro-pneumatic deluge valves), by System Type (Wet pilot systems, Dry pilot systems, Electric release, Pneumatic release), by Application (Fire protection systems, Foam fire suppression systems), by End-Use Industry (Oil & gas, Chemical & petrochemical, Power generation, Manufacturing, Warehousing & logistics, Infrastructure, Others)

| Status : Published | Published On : Apr, 2026 | Report Code : VRSME9205 | Industry : Semiconductor & Electronics | Available Format :

|

Page : 190 |

Pneumatic Deluge Valve Market Overview

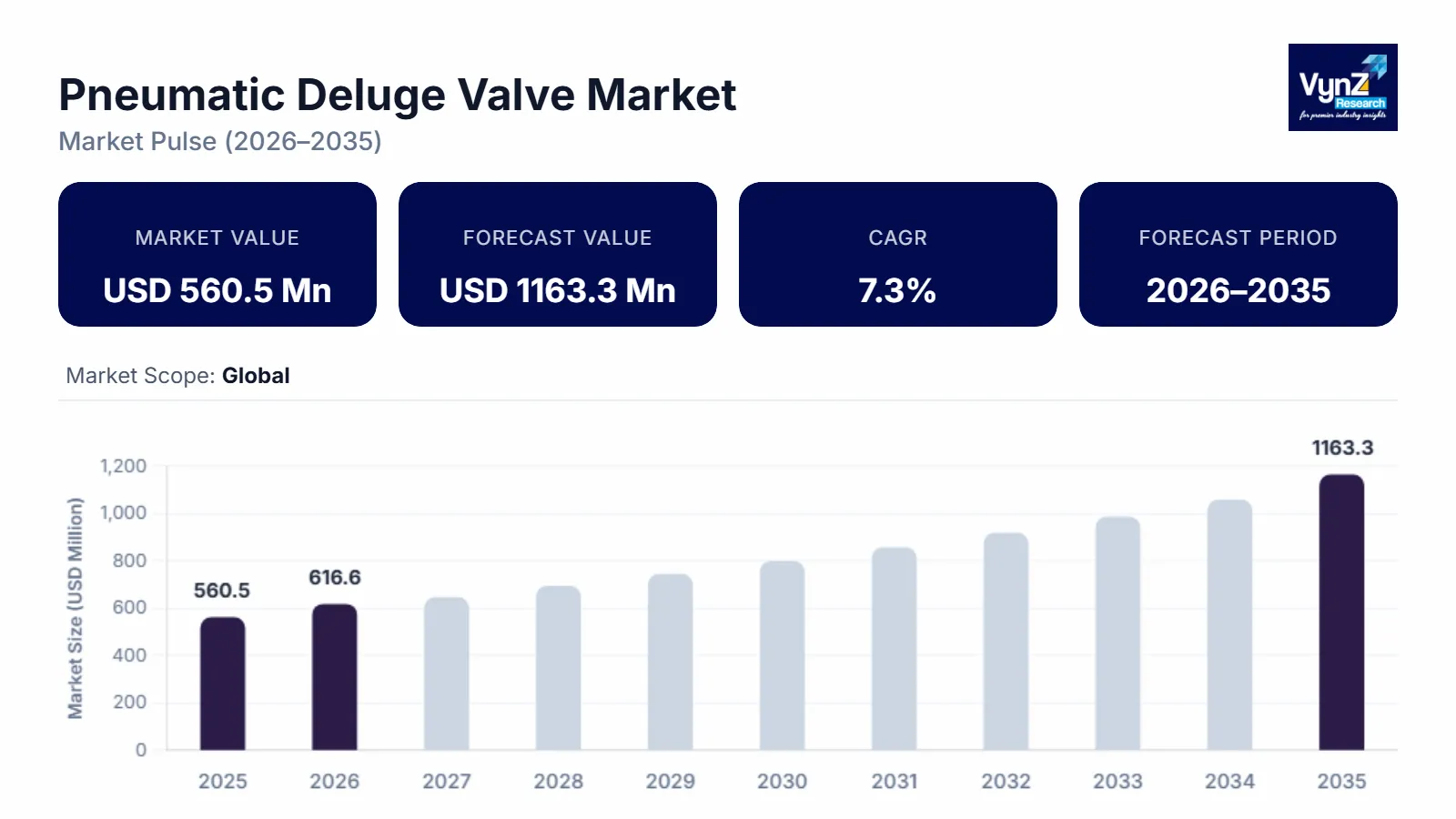

The pneumatic deluge valve market which was valued at approximately USD 560.5 million in 2025 and is estimated to reach around USD 616.6 million in 2026, is projected to reach close to USD 1163.3 million by 2035, expanding at a CAGR of about 7.3% during the forecast period from 2026 to 2035.

The pneumatic deluge valve market is driven by the growing importance of fire safety across industrial and commercial environments. Industries dealing with flammable materials, high temperatures, and hazardous operations require highly responsive fire suppression systems. Pneumatic deluge valves enable rapid release of water or foam over a wide area, which makes them a critical component in fire protection infrastructure. The rising awareness regarding workplace safety and asset protection continues to push organizations toward adopting such advanced systems. Stringent fire safety regulations and compliance requirements further accelerate market growth. Governments and regulatory authorities have implemented strict norms mandating the installation of reliable fire suppression systems in sectors such as oil & gas, power generation, transportation, and manufacturing. Companies are increasingly investing in pneumatic deluge valves to meet these standards and avoid penalties, operational risks, and safety violations.

Pneumatic Deluge Valve Market Dynamics

Market Trends

Integration with smart monitoring technologies is emerging as a significant trend in the pneumatic deluge valve market, driven by the need for enhanced safety, real-time visibility, and predictive maintenance. Modern fire protection systems are increasingly being equipped with sensors, IoT-enabled devices, and centralized control platforms that continuously monitor pressure levels, valve status, and system performance. This integration allows operators to detect faults early, receive instant alerts during abnormalities, and ensure quicker system activation during fire incidents. The Indian government has committed and deployed over ₹1.64 lakh crore (approximately USD 20+ billion) across more than 8,000 projects. This funding is distributed across multiple areas including smart mobility, water management, energy efficiency, surveillance systems, and digital governance. It also reduces manual inspection efforts and improves operational efficiency by enabling remote diagnostics and maintenance planning. Industries such as oil & gas, power generation, and large-scale infrastructure are actively adopting these smart solutions to strengthen risk management and minimize downtime.

Growth Drivers

Growing infrastructure development in emerging economies is a major growth driver for the pneumatic deluge valve market due to the rapid expansion of industrial facilities, urban projects, and critical infrastructure. Countries across Asia-Pacific, the Middle East, and Latin America are investing heavily in sectors such as oil & gas, power generation, transportation, and large-scale commercial construction. These projects require highly reliable fire protection systems to safeguard assets and ensure operational continuity. Pneumatic deluge valves are widely preferred in such environments because they provide rapid and effective fire suppression, especially in high-risk and hazardous conditions. The World Bank alone maintains an active portfolio of 192 urban development projects worth around $34.8 billion, with annual investments of about $5 billion in infrastructure, resilience, and land systems. The rise of smart cities, industrial corridors, airports, tunnels, and energy plants is further increasing the need for advanced safety systems that can handle large-area fire risks. In addition, stricter safety registration and growing awareness about risk management are encouraging developers and industries to integrate robust fire protection solutions from the initial stages of construction.

Market Restraints / Challenges

Dependence on reliable air supply systems is a key challenge in the pneumatic deluge valve market because the entire operation of these valves is based on maintaining consistent air pressure. Any fluctuation in pressure, leakage in air lines, or failure of compressors can prevent the valve from activating properly during a fire emergency. This creates a significant reliability concern, especially in critical environments where immediate response is essential. Maintaining a stable air supply requires continuous monitoring, backup systems, and regular maintenance, which increases operational complexity and cost. In remote or resource-limited locations, ensuring uninterrupted air pressure can be difficult, further limiting adoption. These factors make system performance highly dependent on supporting infrastructure rather than just the valve itself, which can act as a barrier for end users seeking simpler and more fail-safe fire protection solutions.

Market Opportunities

Increasing focus on safety compliance and risk management is creating strong opportunities in the pneumatic deluge valve market as industries prioritize adherence to stringent fire safety standards and the protection of critical assets. Regulatory authorities across the world are enforcing strict guidelines that require reliable and high-performance fire suppression systems in sectors such as oil & gas, power generation, manufacturing, and infrastructure. Organizations are responding by investing in advanced safety solutions that not only ensure compliance but also reduce operational risks and potential financial losses from fire incidents. Global initiatives like the Decade of Action for Fire Safety include proposed investments of around USD 500 million to strengthen fire safety systems worldwide. This investment is made to reduce fire-related deaths, improve safety infrastructure, and enhance compliance with fire protection standards, especially in developing regions. Pneumatic deluge valves play a crucial role in meeting these requirements due to their rapid response capability and reliability in hazardous environments. In addition, companies are increasingly adopting proactive risk management strategies, where preventing downtime and ensuring business continuity has become a key priority. This shift is encouraging the deployment of robust fire protection systems, thereby driving the demand for pneumatic deluge valves in both new and existing facilities.

Global Pneumatic Deluge Valve Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 560.5 Million |

|

Revenue Forecast in 2035 |

USD 1163.3 Million |

|

Growth Rate |

7.3% |

|

Segments Covered in the Report |

Type, System Type, Application, End-Use Industry |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia-Pacific, Rest of the World |

|

Key Companies |

Johnson Controls (Tyco), Viking Group, Minimax Viking, Reliable Automatic Sprinkler Co., Victaulic, Rapidrop Global, HD Fire Protect, Tyco Fire & Security (Johnson Controls), NAFFCO, SFFECO |

|

Customization |

Available upon request |

Pneumatic Deluge Valve Market Segmentation

By Type

The pneumatic deluge valves are the largest category with a market share of about 60% in 2025, due to their high reliability and independence from electrical systems. These valves are widely used in hazardous environments such as oil & gas, chemical plants, and power facilities where electrical failure can pose serious risks. Their simple mechanical design, durability, and ability to operate under extreme conditions make them the preferred choice for critical fire protection systems.

Electro-pneumatic deluge valves are the fastest-growing category with a CAGR of 7.7% during the forecast period, driven by increasing adoption of automation and smart fire safety systems. These valves offer enhanced control, remote operation, and seamless integration with IoT-based monitoring platforms. Growing demand for intelligent infrastructure, especially in commercial buildings and modern industrial setups, is accelerating their adoption. Their ability to combine pneumatic reliability with electrical control systems makes them suitable for advanced applications, leading to higher growth compared to conventional pneumatic valves.

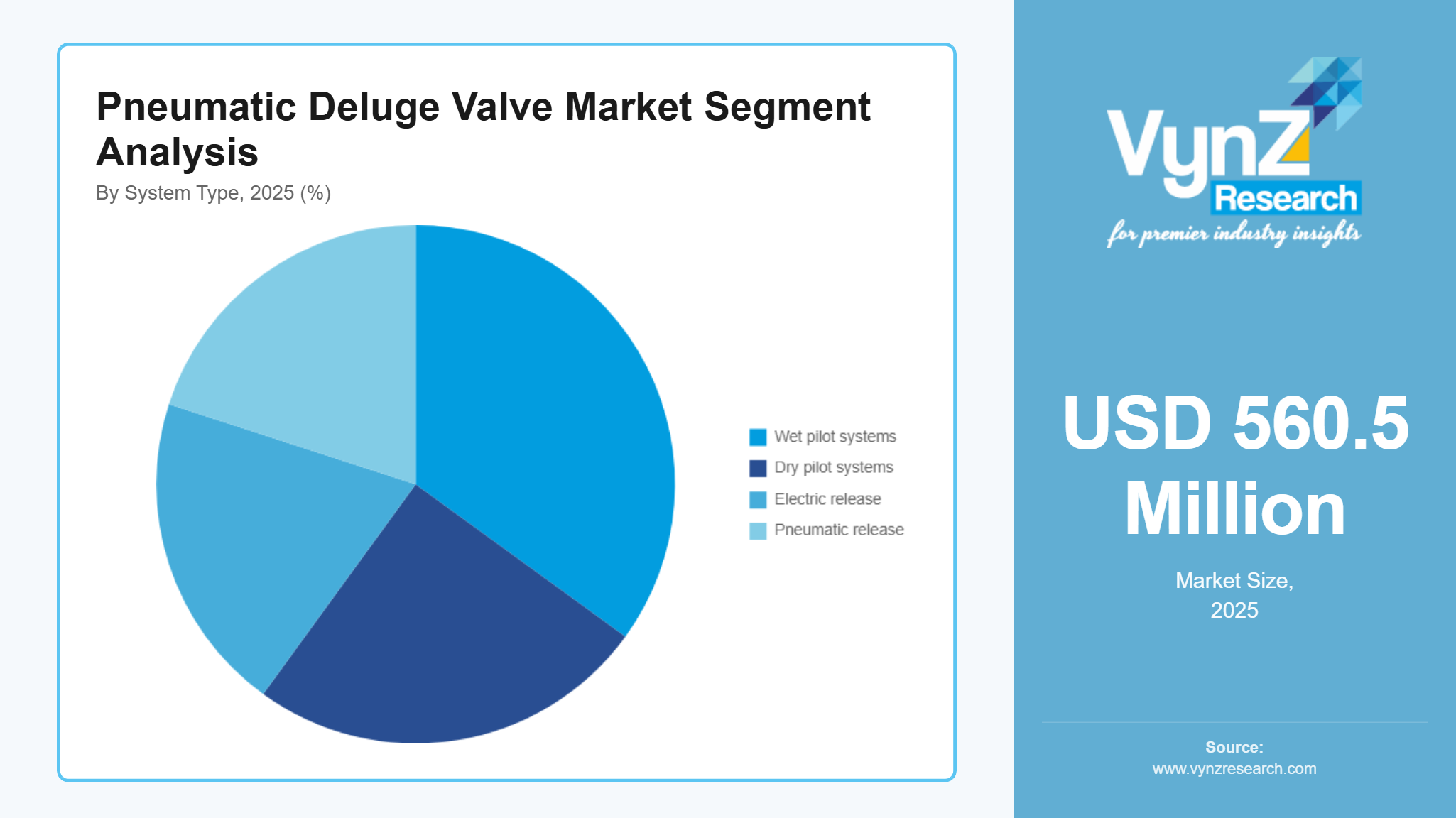

By System Type

Wet pilot systems are the largest category with a market share of about 35% in 2025, due to their fast response time and high reliability in controlled environments. These systems are commonly used in indoor industrial facilities and commercial buildings where temperature conditions remain stable. The presence of pressurized water in the pilot line allows immediate valve activation during fire incidents, improving suppression efficiency. Their relatively simple configuration and proven performance make them a preferred choice across a wide range of applications, supporting their leading market position.

Electric release is the fastest-growing category with a CAGR of 7.5% during the forecast period, due to the increasing shift toward automated and digitally controlled fire protection systems. These systems allow precise activation, remote monitoring, and integration with centralized control units. Rising adoption of smart buildings and industrial automation is driving demand for electrically controlled systems.

By Application

Fire protection systems are the largest category with a market share of about 65% in 2025, due to the core role of pneumatic deluge valves in fire suppression. These systems are extensively used across industries such as oil & gas, power generation, and infrastructure to protect assets and ensure safety compliance. The increasing focus on risk prevention and strict safety regulations further drive their widespread adoption. Their ability to deliver rapid and large-scale water discharge makes them essential in high-risk environments.

Foam fire suppression systems are the fastest-growing category during the forecast period, due to rising demand in environments involving flammable liquids and chemicals. These systems provide better fire containment and cooling compared to water-based systems, making them suitable for high-risk industrial applications. Growth in petrochemical and energy sectors is further boosting their adoption. Increasing awareness about advanced fire suppression techniques is also contributing to their rapid expansion.

By End-Use Industry

Oil & gas is the largest end-use industry category with a market share of about 25% in 2025, due to high fire risk across upstream, midstream, and downstream operations including processing units, tank farms, loading terminals, and offshore/onshore facilities. These environments often require fast, large-area fire suppression using deluge and foam systems, and pneumatic deluge valves are preferred in hazardous locations because they can operate reliably without depending on electrical power at the point of actuation. Ongoing investments in capacity, safety upgrades, and compliance further support demand from this segment.

Infrastructure is expected to be the fastest-growing end-use category with a CAGR of 7.9% during the forecast period, driven by new construction and modernization projects that require engineered fire protection for high-occupancy and high-value assets. The expansion of large warehousing and logistics hubs is also supporting growth, as these facilities increasingly deploy deluge-based solutions to protect wide areas and critical equipment. Greater adoption of centralized monitoring and automated control is further encouraging deployment of advanced electro-pneumatic deluge valve configurations.

Regional Insights

Asia-Pacific (APAC)

Asia Pacific accounted for approximately 34% of the market in 2025, driven by rapid industrialization, infrastructure expansion, and growing investments in oil & gas, chemical processing, power generation, and transportation projects across China, India, Southeast Asia, and Australia. Strong demand from industrial hubs and urban infrastructure projects continues to support market growth. According to the Government of India’s National Infrastructure Pipeline (NIP), planned investments of nearly USD 1.4 trillion are focused on roads, energy, industrial corridors, airports, and metro infrastructure, increasing demand for advanced fire suppression systems in high-risk facilities.

Government initiatives and stricter enforcement of industrial fire safety regulations are encouraging adoption of pneumatic and electro-pneumatic deluge valve systems across manufacturing plants, LNG terminals, refineries, and warehouses. In addition, India’s Fire Services Modernization Funding initiative with an allocation of nearly ₹5,000 crore is supporting upgrades in fire response infrastructure and safety equipment, further strengthening regional market growth.

North America

North America accounted for approximately 24% of the market in 2025, supported by strict fire safety regulations, advanced industrial infrastructure, and high adoption across oil & gas, power generation, chemical processing, and manufacturing industries. Strong demand from the United States and Canada continues to drive installation of reliable fire suppression systems in hazardous operating environments. According to Natural Resources Canada and federal wildfire resilience programs, Canada has committed more than CAD 120 million toward wildfire prevention and fire safety preparedness initiatives.

The region is witnessing steady growth due to ongoing modernization of industrial safety infrastructure and increasing compliance requirements. Growing investments in industrial automation and monitoring systems are also supporting adoption of electro-pneumatic deluge valve solutions integrated with centralized supervisory systems.

Europe

Europe accounted for approximately 18% of the market in 2025, driven by modernization of industrial facilities, stringent fire safety standards, and infrastructure upgrades across transportation, energy, and commercial sectors. Demand remains strong across Germany, France, the United Kingdom, and other industrial economies with high focus on operational safety and regulatory compliance. According to the European Commission, nearly €600 million was allocated in 2024 for strengthening firefighting and emergency response capabilities across Europe.

Growth in Europe is supported by retrofit projects, rising adoption of advanced fire monitoring systems, and investments in industrial safety modernization across chemical, pharmaceutical, and energy industries, creating long-term opportunities for market participants.

Rest of the World

The rest of the world, including the Middle East & Africa and Latin America, accounted for approximately 9% of the market in 2025, supported by investments in oil & gas production, petrochemicals, mining, and industrial infrastructure projects. Saudi Arabia’s Vision 2030 program, involving planned investments exceeding USD 1 trillion, continues to support development of industrial cities, energy infrastructure, and large-scale commercial projects requiring advanced fire protection systems. In Latin America, infrastructure modernization and industrial expansion in countries such as Mexico and Brazil are supporting steady demand growth. According to the Government of Mexico’s National Infrastructure Plan, investments exceeding USD 40 billion are focused on energy, transportation, and industrial development projects.

Across these regions, increasing focus on industrial safety compliance, insurer requirements, and protection of high-value assets is expected to support continued deployment of engineered deluge valve systems. Collectively, the above-mentioned regional markets account for nearly 83% of the global pneumatic deluge valve market, while the remaining share is distributed among smaller developing markets worldwide.

Competitive Landscape / Company Insights

The pneumatic deluge valve market is moderately competitive, with a mix of global fire protection system manufacturers, industrial automation providers, and specialized valve and suppression-system companies. Competition is shaped by product reliability, certifications and approvals, response performance, compatibility with deluge and foam systems, after-sales service networks, and the ability to integrate valves with detection and control panels. Leading players focus on expanding product portfolios (pneumatic and electro-pneumatic options), enhancing corrosion resistance and materials for harsh environments, and supporting end users with design, installation, and maintenance services across industrial and infrastructure applications.

Mini Profiles

Johnson Controls offers fire suppression and deluge system solutions through brands such as Tyco and Viking, supplying deluge valves and related components for industrial and commercial fire protection applications.

Viking Group, Inc. manufactures engineered fire protection products including deluge valves, detection and control solutions, and system components used in water and foam-based fire suppression systems.

Siemens AG provides fire detection and safety management platforms that can interface with deluge and suppression system actuation, supporting integrated fire protection architectures in complex facilities.

Honeywell International Inc. offers fire and life safety solutions, including control and monitoring systems that support activation and supervision of deluge-based fire suppression installations across industrial and commercial sites.

Victaulic Company supplies mechanical pipe-joining solutions and fire protection products, supporting deluge and sprinkler system installations in industrial, commercial, and infrastructure applications.

Key Players

- Johnson Controls

- Viking Group, Inc.

- Reliable Automatic Sprinkler Co., Inc.

- Victaulic Company

- Rapidrop Global Ltd.

- HD Fire Protect Pvt. Ltd.

- Siemens AG

- Honeywell International Inc.

- Eaton Corporation plc

- Emerson Electric Co.

Recent Developments

In April 2025, Johnson Controls expanded its fire suppression portfolio with updates across engineered systems supporting deluge-based applications in high-hazard industrial facilities.

In March 2025, Reliable Automatic Sprinkler Co. announced enhancements in deluge and sprinkler system offerings aimed at improving performance and maintenance efficiency for industrial fire protection deployments.

In February 2025, NAFFCO strengthened its industrial fire protection solutions portfolio to address rising demand for engineered deluge and foam system installations across energy and infrastructure projects.

In March 2026, HD Fire Protect Pvt. Ltd. received UL certification for its advanced deluge valve range with integrated pressure-reducing mechanisms designed for high-risk industrial and critical infrastructure applications.

In February 2026, Victaulic Company expanded manufacturing capacity for smart fire protection valve systems to support increasing demand from industrial facilities and data center infrastructure projects.

Global Pneumatic Deluge Valve Market Coverage

Type Insight and Forecast 2026 - 2035

- Pneumatic deluge valves

- Electro-pneumatic deluge valves

System Type Insight and Forecast 2026 - 2035

- Wet pilot systems

- Dry pilot systems

- Electric release

- Pneumatic release

Application Insight and Forecast 2026 - 2035

- Fire protection systems

- Foam fire suppression systems

End-Use Industry Insight and Forecast 2026 - 2035

- Oil & gas

- Chemical & petrochemical

- Power generation

- Manufacturing

- Warehousing & logistics

- Infrastructure

- Others

Global Pneumatic Deluge Valve Market by Region

- North America

- By Type

- By System Type

- By Application

- By End-Use Industry

- By Country - U.S., Canada, Mexico

- Europe

- By Type

- By System Type

- By Application

- By End-Use Industry

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Type

- By System Type

- By Application

- By End-Use Industry

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Type

- By System Type

- By Application

- By End-Use Industry

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Pneumatic Deluge Valve Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Type

1.2.2. By

System Type

1.2.3. By

Application

1.2.4. By

End-Use Industry

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Type

5.1.1. Pneumatic deluge valves

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Electro-pneumatic deluge valves

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.2. By System Type

5.2.1. Wet pilot systems

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Dry pilot systems

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Electric release

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Pneumatic release

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.3. By Application

5.3.1. Fire protection systems

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Foam fire suppression systems

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By End-Use Industry

5.4.1. Oil & gas

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Chemical & petrochemical

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Power generation

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Manufacturing

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Warehousing & logistics

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

5.4.6. Infrastructure

5.4.6.1. Market Definition

5.4.6.2. Market Estimation and Forecast to 2035

5.4.7. Others

5.4.7.1. Market Definition

5.4.7.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Type

6.2. By

System Type

6.3. By

Application

6.4. By

End-Use Industry

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Type

7.2. By

System Type

7.3. By

Application

7.4. By

End-Use Industry

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Type

8.2. By

System Type

8.3. By

Application

8.4. By

End-Use Industry

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Type

9.2. By

System Type

9.3. By

Application

9.4. By

End-Use Industry

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Johnson Controls

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Viking Group, Inc.

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Reliable Automatic Sprinkler Co., Inc.

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Victaulic Company

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Rapidrop Global Ltd.

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

HD Fire Protect Pvt. Ltd.

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Siemens AG

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Honeywell International Inc.

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Eaton Corporation plc

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Emerson Electric Co.

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Pneumatic Deluge Valve Market