TIC Market for Food & Beverage Industry Size & Share | Growth Forecast Report (2026-2035)

Industry Insight by Service Type (Testing, Inspection, Certification), by Sourcing Type (In-House, Outsourced), by Product Category (Processed Foods, Packaged Foods), by Supply Chain Stage (Processing and Manufacturing, Post Production)

| Status : Published | Published On : Apr, 2026 | Report Code : VRSME9203 | Industry : Semiconductor & Electronics | Available Format :

|

Page : 178 |

TIC Market for Food & Beverage Industry Overview

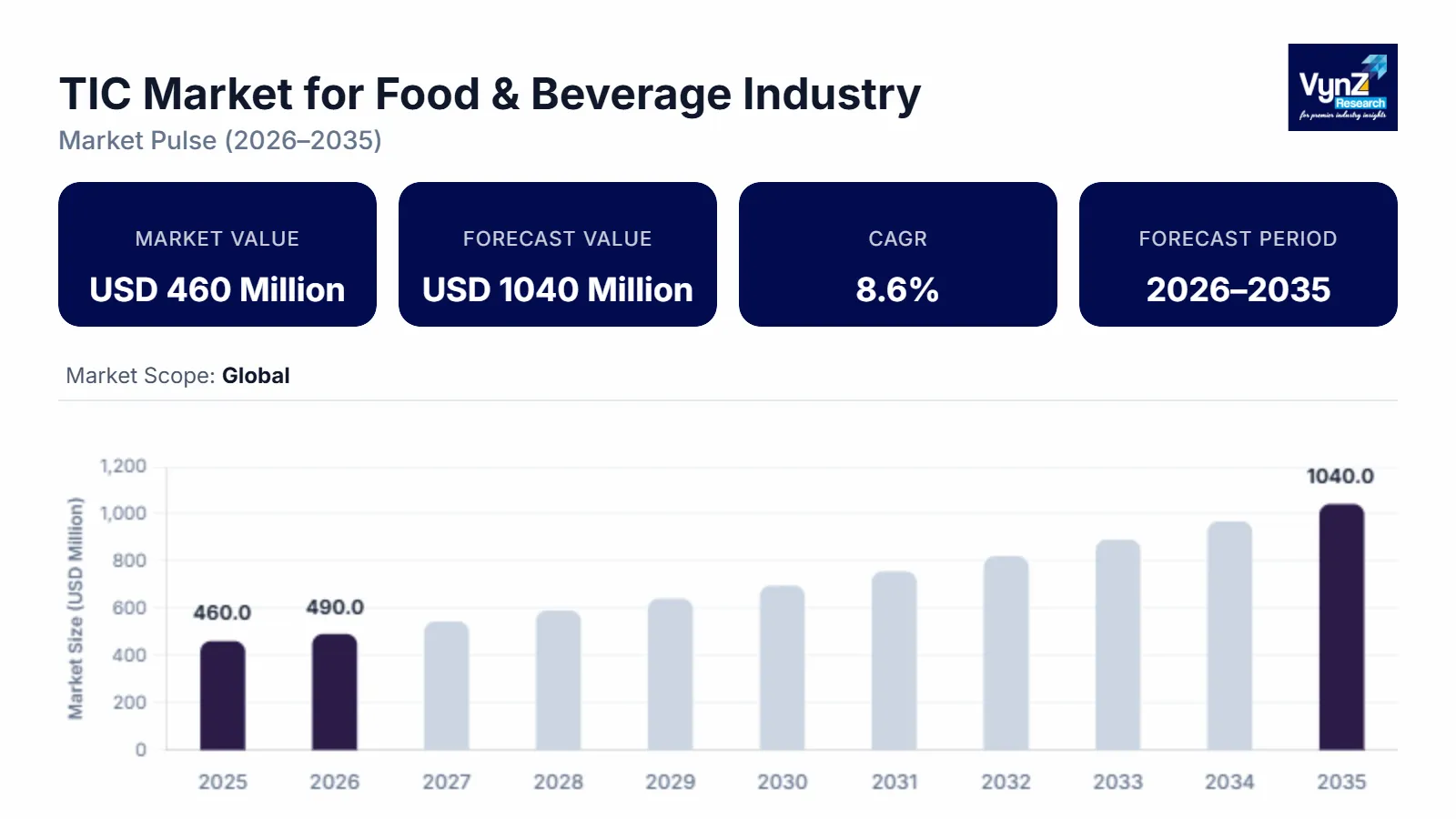

The global TIC Market for Food & Beverage Industry, which was valued at approximately USD 460 million in 2025 and is estimated to reach around USD 490 million in 2026, is projected to reach approximately USD 1040 million by 2035, expanding at a CAGR of about 8.6% during the forecast period from 2026 to 2035.

The food and beverage industry's Testing, Inspection, and Certification (TIC) sector guarantees product quality, safety, and regulatory compliance across supply chains. The need for trustworthy certification and testing has grown as consumer knowledge of food safety and health has grown. Food items' compliance with national and international standards for ingredient labeling, composition, packaging, and hygiene is confirmed by TIC services.

Strict laws enforced by organizations like the Food Safety and Standards Authority of India and international frameworks like ISO standards are what propel the market. The necessity for uniform inspection and certification procedures to guarantee cross-border conformity is further increased by the expanding global trade in food goods.

The TIC landscape is changing due to technological developments including digital inspection tools, blockchain for traceability, and quick testing techniques. Additionally, new testing requirements are being created by trends like sustainability, clean-label products, and organic foods.

TIC Market for Food & Beverage Industry Dynamics

Market Trends

Governments around the world are imposing stricter rules and specifications for food safety. In order to avoid fines and guarantee customer safety, voluntary procedures are being replaced by mandatory testing and certification, increasing demand for TIC services. Food supply chains have become lengthy and intricate as a result of globalization, necessitating many rounds of inspection and certification. As consumers' awareness of food safety, hygiene, and ingredient transparency has grown along with the demand for certified, organic, high-quality, and non-GMO products. TIC services support seamless cross-border trade and assist guarantee adherence to international norms. To cut costs and concentrate on core business activities, food manufacturers are increasingly contracting with specialized third-party providers to handle testing and certification, which is expanding the market for TIC services.

Growth Drivers

Food & beverage manufacturing companies have always been under the radar of regulatory authorities, and this pressure has not decreased but increased during the last ten years. In response to contamination and consumer health, safety concerns, governments keep on changing food safety laws, import-export controls, hygiene protocols, and labeling standards. Consequently, food safety testing and inspection have become mandatory third-party activities of the routine operational procedures. Food safety-related TIC services are forecasted to make up almost thirty percent of the total sector demand, with the volume of compliance-led services steadily increasing by about 6–7% per year during the present decade.

Worldwide food supply chains have become more complex, thus creating an additional layer of long-term demand. The raw materials are sourced from various countries, processed in multiple places, and sold through intricate cold-chain networks, which makes the quality failures and the traceability gaps more likely. To control this risk, producers and retailers depend to a great extent on the services of independent laboratories for microbiological testing, residue analysis, and shelf-life validation. The TIC spending related to international food trade has increased at a higher speed than the demand for domestic food trade, which is supported by the growth of export volumes and the tightening of the requirements in the destination countries.

The consumer behavior changes are also influencing the inspection and certification priorities. The demand for organic products, clean-label foods, plant-based alternatives, and allergen-free offerings has resulted in verification requirements that go beyond the simplest safety testing. The certification related to sustainability, non-GMO, and ethical sourcing is becoming a must-have rather than an option. These value-added certification services are growing at a rate of almost 8% per year, thus leaving behind the traditional inspection activities that are only focusing on regulatory compliance.

Market Restraints / Challenges

The testing, inspection, and certification market face certain challenges like trade wars and growth fluctuations, huge investment for automation and installation of industrial safety systems, high cost of TIC owing to diverse standards and regulations globally. The concern regarding adulterated food and food ingredients and lack of harmonization in food safety standards are acting as a restraint in the TIC market. Moreover, a lack of testing facilities and skilled personnel may hamper the growth of the TIC market.

Market Opportunities

Rapid urbanization, increasing exports, and evolving food regulations are driving the need for TIC services in these high-growth markets as this is specifically evident for organic, non-GMO, halal, and “free-from” food certifications shall open new revenue streams for TIC providers. Increasing focus on sustainability and environmentally responsible production is driving demand for green certifications, carbon footprint assessments, and ethical sourcing verification, creating new niches for TIC companies. As cutting-edge technology are adopted, TIC services are evolving. Real-time monitoring, predictive analysis, and enhanced traceability are all made possible by these technologies, opening doors for creative and valuable service offerings. Testing and certification services are in great demand since consumers are become more aware of food quality, hygiene, and transparency. There is a great deal of unrealized potential in Asia-Pacific, Africa, and Latin America.

Global TIC Market for Food & Beverage Industry Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 460 Million |

|

Revenue Forecast in 2035 |

USD 1040 Million |

|

Growth Rate |

8.6% |

|

Segments Covered in the Report |

Service Type, Sourcing Type, Product category and Supply Chain Stage |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific |

|

Key Companies |

ABB Ltd., BYD Company Limited, Contemporary Amperex Technology Co., Limited (CATL), Fluence Energy, Inc., Form Energy, Inc., LG Energy Solution Ltd., Panasonic Holdings Corporation, Samsung SDI Co., Ltd., Siemens Energy AG, Tesla, Inc |

|

Customization |

Available upon request |

TIC Market for Food & Beverage Industry Segmentation

By Service Type

Testing accounts for the biggest part of the food and beverage industry demand for TIC and brings approximately 45% of the total market revenue which is mainly driven by the execution of routine chemical, microbiological, and nutritional analyses. Next in line are the inspection activities, mainly performed in processing plants and cold storage facilities, whereas certification services are progressively becoming more relevant as branded manufacturers put more trust in third-party validation to help them with labeling, export approvals, and consumer trust.

By Sourcing Type

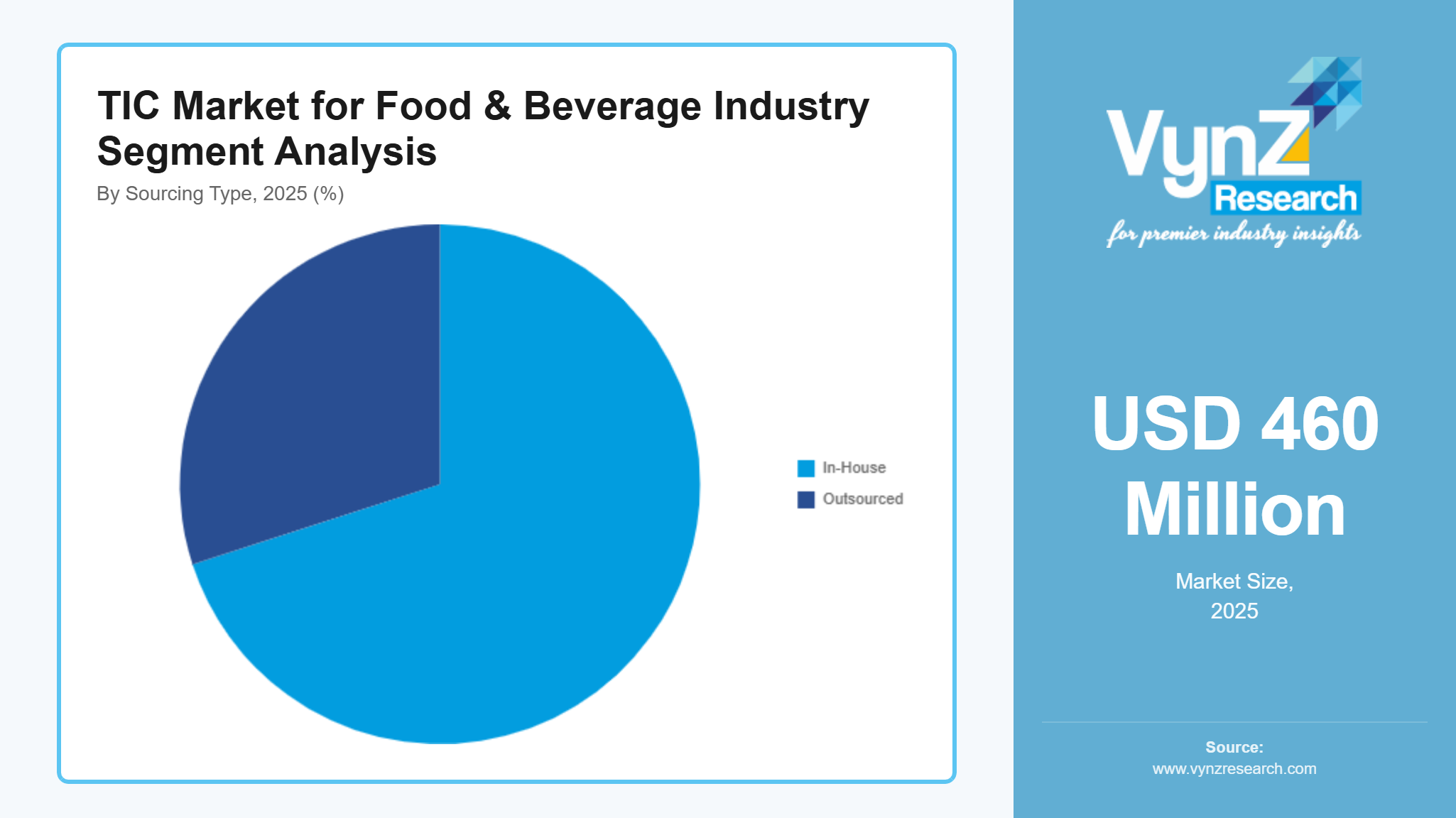

Outsourced TIC services are the major force of the market that accounts for nearly 70% of total demand, as most food-producing enterprises are not equipped with the necessary infrastructure or lack the accreditation for performing advanced testing. Independent laboratories and certification bodies are chosen by users because of their neutrality and worldwide acceptance. The conducted testing by the in-house method is limited to large multinational processors and slowly growing, mostly for the preliminary quality checks rather than for the regulatory submissions.

By Product Category

Processed and packaged foods are the major application segments that have resulted from frequent testing cycles and strict requirements for labeling. Following are dairy, meat, and seafood, which are supported by a high risk of contamination and are temperature-sensitive. Beverage testing, especially for functional drinks and alcoholic products, is experiencing a rapid increase in growth as the formulation complexity and regulatory oversight become stricter in the major markets.

By Stage of Supply Chain

The highest demand for TIC services comes from the processing and manufacturing stages that use more than half of the total service volume because safety validation is mandatory before market entry. A large portion of post-production inspection and distribution-stage testing is there, and they are steadily growing as measures for traceability and recall-prevention become more important. The lifecycle testing that covers sourcing, production, and distribution is becoming more popular among export-oriented producers.

Regional Insights

North America

North America stands for a mature market that is still consistently active in the field of food and beverage TIC services and accounts for a bit more than 30% of the worldwide demand. The United States is the main driver of the regional activities that are backed up by rigorous FDA and USDA regulations and frequent changes in the food safety modernization frameworks.

The demand is also facilitated by the high consumption of processed and packaged foods that prompt continuous testing across production batches. The TIC services that are associated with allergen testing, nutritional labeling, and recall prevention are warmly welcomed and supported by the enforcement that is strong and the risk of litigation in case of non-compliance that is high.

Moreover, the ever-growing focus on sustainability claims as well as the clean-label certification is causing the need for the non-regulatory testing and verification services to go up in the case of the premium food segments.

Asia Pacific

Asia Pacific is the most rapidly developing regional market that is estimated to grow at a CAGR of 8–9%. The main factors behind this substantial growth are a rise in food production volumes, export-oriented processing hubs, and implementation of tough domestic food safety laws. The new demand is mainly from China, India, and Southeast Asian economies.

The fast growth of packaged food consumption along with mounting government oversight has resulted in a significant increase in third-party testing laboratories' services. Manufacturers who are export-driven rely heavily on certification bodies that are recognized internationally to comply with the standards of the destination market.

As the regulatory enforcement becomes more reliable in the whole region, TIC services are shifting from the convention of being called a reactive Inspection toward a structured, recurring compliance program.

Europe

Europe is responsible for approximately 25% of the total worldwide demand for food and beverage TIC services. It is characterized by well-regulated and harmonized regulatory systems compliant with the EU framework for food safety regulation. The uniformity of the requirements results in a strict compliance with regulations, and this is the reason for a stable and regular need for testing and certification services.

Environmental and sustainability issues are gaining more and more influence over TIC activities, in particular, for organic food, animal welfare compliance, and carbon footprint disclosures. A faster expansion of sustainability-related certification compared to safety testing is evident.

The ongoing reformulation trends, taking the reduction of sugar and the nutritional labeling regulations as the main drivers, are additionally contributing to a steady demand for laboratory testing all over the region.

Competitive Landscape / Company Insights

The TIC Market for Food & Beverage Industry is moderately to highly competitive, with global and regional companies focusing on technology innovation, strategic partnerships, and geographic expansion to strengthen their industry position. Key players are investing in advanced battery chemistries, grid scale storage solutions, and digital energy management platforms to enhance system efficiency and reliability. Adoption is supported by clean energy transition initiatives promoted by the International Energy Agency and grid modernization programs implemented by the U.S. Department of Energy, encouraging companies to expand deployment capabilities and technological expertise.

Mini Profiles

ABB Ltd. focuses on advanced grid infrastructure and energy storage integration technologies, supported by strong global distribution networks, power automation expertise, and established partnerships with utilities implementing large scale renewable energy projects.

BYD Company Limited operates in mass and large-scale battery storage segments, emphasizing performance driven lithium battery technologies, supported by vertically integrated manufacturing capabilities and extensive deployment across renewable and utility storage applications.

Contemporary Amperex Technology Co., Limited (CATL) leverages large scale manufacturing and strategic partnerships with utilities and renewable developers to expand market presence, delivering advanced battery storage technologies with high efficiency and long operational lifecycle.

Fluence Energy, Inc. focuses on integrated grid scale battery storage platforms, supported by digital energy management software, strong project deployment capabilities, and partnerships with utilities seeking scalable renewable energy storage solutions.

Form Energy, Inc. operates in next generation long duration storage solutions, emphasizing innovative iron air battery technologies designed to support multi day energy storage requirements for renewable integration and resilient power systems.

Key Players

- ABB Ltd.

- BYD Company Limited

- Contemporary Amperex Technology Co., Limited (CATL)

- Fluence Energy, Inc.

- Form Energy, Inc.

- LG Energy Solution Ltd.

- Panasonic Holdings Corporation

- Samsung SDI Co., Ltd.

- Siemens Energy AG

- Tesla, Inc.

Recent Developments

In March 2026, Panasonic has launched a liquid cooling systems business for AI data centers. This business focus on cooling systems for high-performance computing & generative AI servers and development of high-capacity cooling units (1,200 kW+) which aligns with rising demand from data centers and cloud computing.

In March 2026, ABB Robotics Partners with NVIDIA to Deliver Industrial-Grade Physical AI at Scale. The collaboration focuses on combining ABB Robotics’ software programming, design and simulation suite, RobotStudio, with the physically accurate simulation power of NVIDIA Omniverse libraries to close technology's long-standing 'sim-to-real’ gap. Developers can simulate robots in digital twins and generate synthetic data to train their physical AI models, enabling businesses of all types and sizes to deploy AI-driven robotics for various industrial workflows.

In February 2026, Google has awarded Form Energy, Inc. a USD billion contract to provide its cutting-edge iron-air batteries for a Minnesota data center project. One of the biggest and longest-lasting battery installations in the world, this project entails the deployment of a massive energy storage system that can provide electricity constantly for up to 100 hours. Iron-air batteries are less expensive for widespread use since they are made of inexpensive materials like iron.

Global TIC Market for Food & Beverage Industry Coverage

Service Type Insight and Forecast 2026 - 2035

- Testing

- Inspection

- Certification

Sourcing Type Insight and Forecast 2026 - 2035

- In-House

- Outsourced

Product Category Insight and Forecast 2026 - 2035

- Processed Foods

- Packaged Foods

Supply Chain Stage Insight and Forecast 2026 - 2035

- Processing and Manufacturing

- Post Production

Global TIC Market for Food & Beverage Industry by Region

- North America

- By Service Type

- By Sourcing Type

- By Product Category

- By Supply Chain Stage

- By Country - U.S., Canada, Mexico

- Europe

- By Service Type

- By Sourcing Type

- By Product Category

- By Supply Chain Stage

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Service Type

- By Sourcing Type

- By Product Category

- By Supply Chain Stage

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Service Type

- By Sourcing Type

- By Product Category

- By Supply Chain Stage

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for TIC Market for Food & Beverage Industry Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Service Type

1.2.2. By

Sourcing Type

1.2.3. By

Product Category

1.2.4. By

Supply Chain Stage

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Service Type

5.1.1. Testing

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Inspection

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Certification

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Sourcing Type

5.2.1. In-House

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Outsourced

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Product Category

5.3.1. Processed Foods

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Packaged Foods

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By Supply Chain Stage

5.4.1. Processing and Manufacturing

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Post Production

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Service Type

6.2. By

Sourcing Type

6.3. By

Product Category

6.4. By

Supply Chain Stage

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Service Type

7.2. By

Sourcing Type

7.3. By

Product Category

7.4. By

Supply Chain Stage

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Service Type

8.2. By

Sourcing Type

8.3. By

Product Category

8.4. By

Supply Chain Stage

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Service Type

9.2. By

Sourcing Type

9.3. By

Product Category

9.4. By

Supply Chain Stage

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

ABB Ltd.

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

BYD Company Limited

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Contemporary Amperex Technology Co., Limited (CATL)

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Fluence Energy, Inc.

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Form Energy, Inc.

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

LG Energy Solution Ltd.

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Panasonic Holdings Corporation

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Samsung SDI Co., Ltd.

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Siemens Energy AG

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Tesla, Inc.

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

TIC Market for Food & Beverage Industry