TIC Market for Government & Public Sector Size & Share | Growth Forecast Report (2026-2035)

Industry Insight by Service Type (Testing, Inspection, Certification), by Sourcing Type (In-House, Outsourced), by End Use Application (Infrastructure and Construction, Energy and Utilities, Transportation-related applications), by Asset Lifecycle Stage (Before the Commissioning Stage, Lifecycle-based)

| Status : Published | Published On : Apr, 2026 | Report Code : VRSME9204 | Industry : Semiconductor & Electronics | Available Format :

|

Page : 179 |

TIC Market for Government & Public Sector Overview

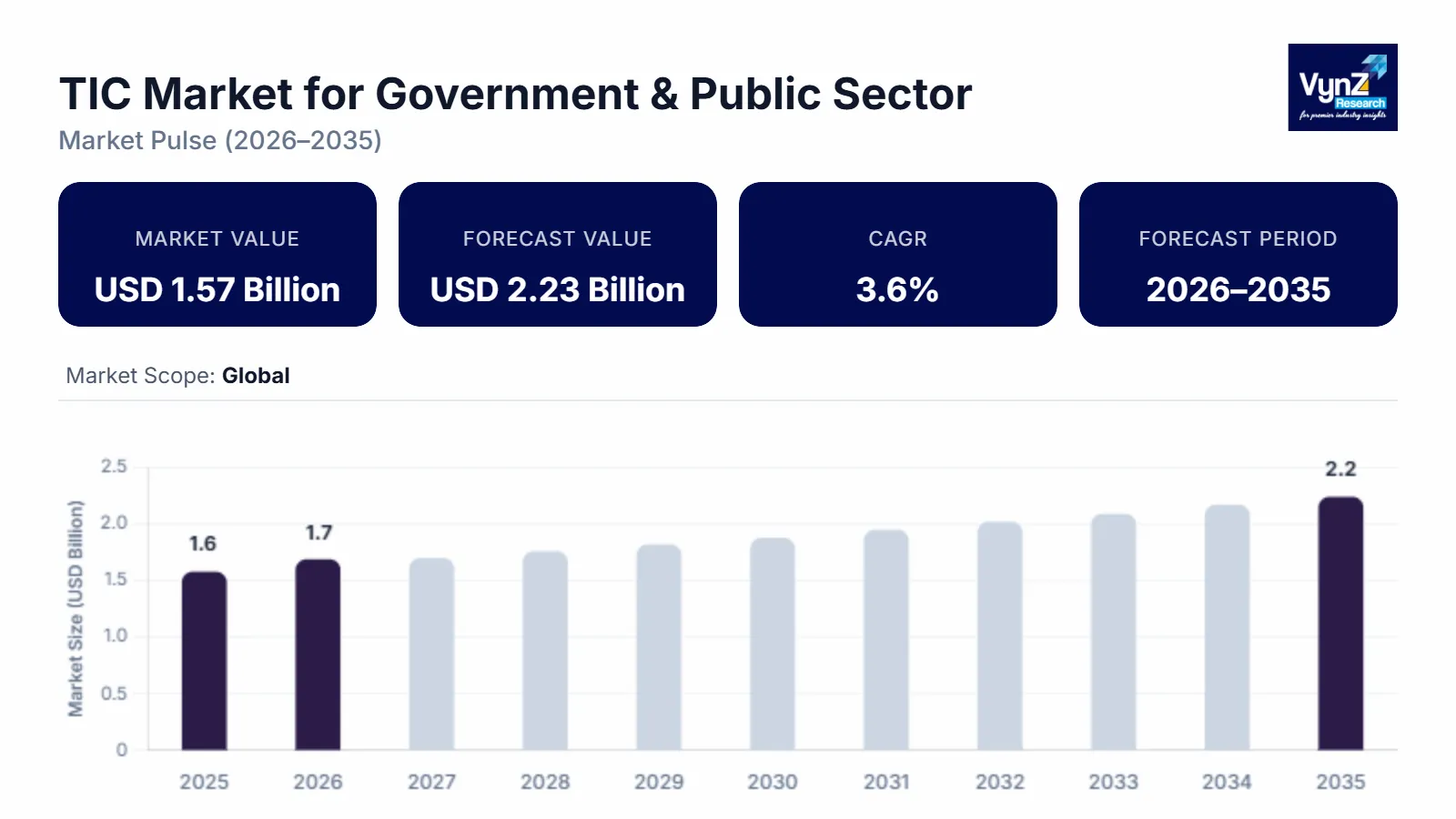

The global TIC Market for Government & Public Sector, which was valued at approximately USD 1.57 billion in 2025 and is estimated to reach around USD 1.6 billion in 2026, is projected to reach approximately USD 2.23 billion by 2035, expanding at a CAGR of about 3.6% during the forecast period from 2026 to 2035.

For the government and public sector, the Testing, Inspection, and Certification (TIC) industry is essential to maintaining infrastructure dependability, public safety, and regulatory compliance. In order to enforce standards in industries including building, transportation, healthcare, energy, and environmental management, governments are depending more and more on TIC services. Independent verification and quality assurance are becoming more and more necessary as public infrastructure projects become larger and more complicated.

Government across the world are facing various complex issues and are constantly challenged to deliver public services in an effective way with limited and constrained resources. The delivery of public sector services requires a careful and comprehensive approach, adhering to strict regulations, ensuring public safety, and providing services according to stringent standards and schedules. Moreover, the increasing middle-class populace, urbanization, stringent safety regulations, increasing trade of pirated products, development in networking and communication technology and creating brand image has propelled the growth of the TIC market in the government & public sector Thus, TIC services will help the public sector to find and mitigate the intrinsic risk of operations, supply chain, and business processes so as to provide safety, quality, and cost-effectiveness of public sector services and infrastructure.

TIC Market for Government & Public Sector Dynamics

Market Trends

The government and public sector's Testing, Inspection, and Certification (TIC) industry is driven by strict laws, infrastructure upgrading, and sustainability mandates. Digital inspection technology, ESG compliance, and asset integrity monitoring drive growth. TIC is moving toward proactive, tech-enabled risk management due to its growing reliance on lifecycle compliance services and public-private collaborations.

Growth Drivers

Across both categories of nations, public authorities are progressively extending the scope and intensity of their regulatory supervision in various fields such as transport infrastructure, utilities, defense acquisitions, healthcare assets, and public safety systems. Consequently, independent testing, inspection, and certification have become a structural necessity rather than a discretionary activity. It is estimated that compliance with government-linked regulations accounts for nearly one-third of the total global TIC demand. The volume of conformity assessment is expected to increase by roughly 6.5–7% annually between 2024 and 2030 due to the formalization of audit traceability, operational risk control, and safety governance.

Another major source of sustained government capital expenditure is a significant contributor to market growth. Public investments in roads, rail networks, ports, airports, electricity grids, water treatment plants, and urban infrastructure exceeded USD 4 trillion worldwide in 2023 and are still growing under long-term national development programs. Inspection and testing at each step, from design validation to commissioning and maintenance, are thus facilitated, resulting in a gradual increase of TIC revenues by about 7% per year driven by infrastructure demand only.

Meanwhile, digitization efforts in the public sector are redefining the needs of the TIC market. Governments are implementing e-governance platforms, smart infrastructure systems, public data centers, and cloud-based service architectures, which require cybersecurity testing, software validation, and operational audits. ESG compliance for publicly funded projects is also becoming mandatory in several regions. Therefore, TIC services associated with digital compliance and sustainability verification are growing at a much faster rate than traditional segments, reaching nearly 8–8.5% growth rates.

Market Restraints / Challenges

Financial limitations and drawn-out procurement procedures are just two of the difficulties facing the government and public sector's Testing, Inspection, and Certification (TIC) market. High operating and regulatory costs further strain this industry along with shortage of skilled labor. Ensuring data security, integrating digital technology, and preserving uniformity across agencies further complicate effective deployment.

Market Opportunities

The Testing, Inspection, and Certification (TIC) business has enormous potential for the public sector and government, driven by infrastructure expansion, public safety requirements, and regulatory compliance. Important subjects include infrastructure development, renewable energy, healthcare, food safety, transportation, and environmental monitoring. The demand for TIC services is increased in India by programs like Make in India and more stringent certification requirements. Through partnerships and public bids, governments serve as both large clientele and regulators. ESG compliance and digital inspection technologies also drive growth. For licensed TIC providers, the industry offers steady, long-term revenue prospects despite significant entry obstacles and costs.

Global TIC Market for Government & Public Sector Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 1.57 Billion |

|

Revenue Forecast in 2035 |

USD 2.23 Billion |

|

Growth Rate |

3.6% |

|

Segments Covered in the Report |

Service Type, Sourcing Type, End Use Application, Asset Lifecycle Stage |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific |

|

Key Companies |

ABB Ltd., BYD Company Limited, Contemporary Amperex Technology Co., Limited (CATL), Fluence Energy, Inc., Form Energy, Inc., LG Energy Solution Ltd., Panasonic Holdings Corporation, Samsung SDI Co., Ltd., Siemens Energy AG, Tesla, Inc |

|

Customization |

Available upon request |

TIC Market for Government & Public Sector Segmentation

By Service Type

Testing continues to be the major service category, contributing approximately 41–43% of market revenue in 2024, and is well supported by the ongoing needs for material testing, laboratory-based analysis, and performance verification of public assets. The inspection segment is gaining the strongest traction and is increasing by almost 8% yearly as a result of the safety recurring checks and asset condition monitoring, while the certification demand remains stable and is maintained by regulatory approvals and statutory documentation requirements.

By Sourcing Type

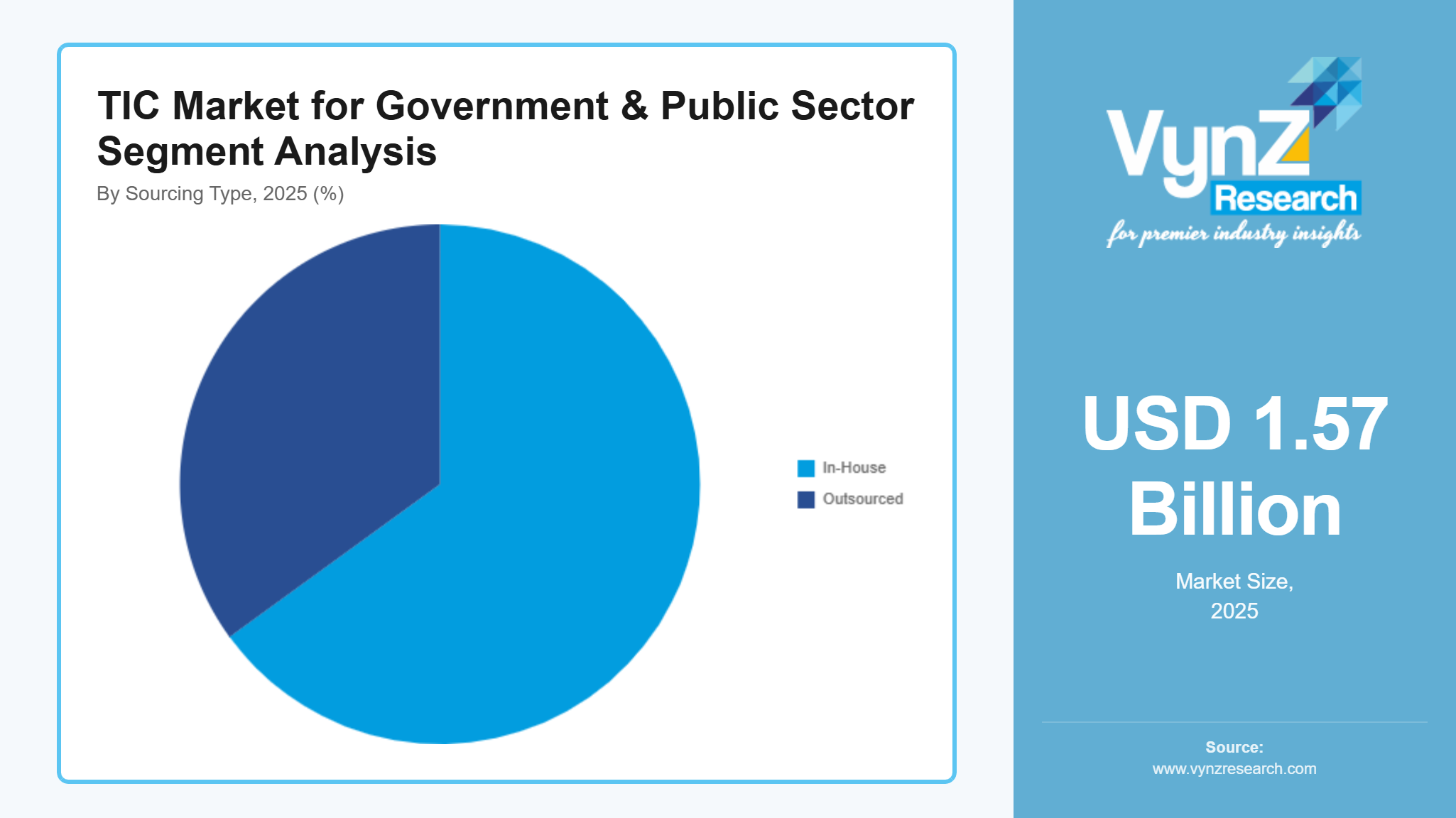

Third-party outsourced TIC services are the main source of government and public-sector demand and account for almost 65% of the total market value. Public agencies increasingly invite independent providers to help them keep neutrality, credibility, and regulatory consistency, especially in areas where technical specialization is needed. The volume of outsourced services is growing at a rate of about 7.4% per year, whereas the in-house inspection and testing departments, which are mostly limited to defense and critical agencies, are still increasing but at a much slower rate (just over 4%).

By End-Use Application

The primary area of application is represented by infrastructure and construction, which are responsible for almost 40% of the overall demand and are fueled by ongoing public works, urban development, and asset renewal programs. Energy and utilities follow the trend of the infrastructure sector. The next most significant industry for the use of transportation-related applications, which include railways, metros, airports, and ports, is growing the quickest, and it has a growth rate of over 8% as governments prioritize mobility infrastructure.

By Asset Lifecycle Stage

The majority (around 55%) of TIC demand comes from new project development caused by the necessity of testing and certification before the commissioning stage. Meanwhile, the importance of inspection and maintenance of already existing assets keeps growing as public infrastructure is getting older. Lifecycle-based inspection services are increasing by almost 7% per year, and this trend reflects government attention to prolonging asset life, lowering operational risks, and managing long-term maintenance costs.

Regional Insights

North America

North America continues to be a highly mature and value-rich market for government and public-sector TIC services, with contributions of approximately 31–33% to the worldwide revenue in 2024. The demand is mainly limited to the United States, where regulatory enforcement, public accountability, and audit transparency are tightly integrated into governance frameworks.

Long-term federal investment programs in areas such as transportation corridors, broadband infrastructure, clean energy, and public utilities keep the inspection and certification activities at a steady pace. The region’s TIC services directly connected to public infrastructure projects are on the rise at a rate of almost 6.8% CAGR, as they are supported by regular audits, renewals, and compliance reporting cycles.

Moreover, the heightened focus on cybersecurity standards and ESG disclosures across government departments is leading to an increase in demand for digital system validation and sustainability-focused certification services.

Asia Pacific

Asia Pacific is the fastest expanding regional market with growth rates of around 8.2% to 8.5% over the forecast period. The major factors behind such a strong upward trend are rapid urbanization, population increase and aggressive public infrastructure rollout programs in China, India, Japan, and Southeast Asia.

Investments driven by the government in areas such as transport networks, smart city projects, water management, and power infrastructure continue to create a high volume of testing and inspection work. The public-sector TIC spending in the region was more than USD 1.1 billion in 2024 and is forecasted to increase gradually as the infrastructure pipeline stays robust.

On the other hand, the regulatory frameworks in several emerging economies are becoming more formal and internationally aligned, thereby increasing the dependence on third-party certification to comply with global safety, quality, and sustainability standards.

Europe

Europe is responsible for about one-quarter of the global TIC demand originating from government and public-sector applications and has features such as mature regulatory systems and consistent enforcement. The region's growth is still stable and is being supported by harmonized EU standards and cross-border compliance requirements.

Sustainability and environment regulation take the central role in determining the TIC needs, especially for publicly financed infrastructure projects. The services concerned with energy efficiency validation, emissions monitoring, and environmental compliance are growing at almost 7% per year in large European economies.

Modernizing rail and electrifying public services through digital technologies funded by the local and national governments are the main reasons for the steady stream of inspection, testing, and certification requirements in the region.

Competitive Landscape / Company Insights

The TIC Market for Government & Public Sector is moderately to highly competitive, with global and regional companies focusing on technology innovation, strategic partnerships, and geographic expansion to strengthen their industry position. The TIC market is led by global players like SGS SA, Bureau Veritas, and Intertek Group plc, leveraging scale and global reach. Eurofins Scientific specializes in lab testing, while TUV SUD and DEKRA SE focus on safety and engineering, creating a mix of diversified leaders and niche specialists.

Mini Profiles

MISTRAS Group is an US-based provider specializing in asset integrity, non-destructive testing (NDT), and industrial inspection. Strong presence in oil & gas, aerospace, and energy sectors.

Eurofins Scientific is a global leader in laboratory testing services, especially in food, environment, and pharmaceuticals. Strong R&D focus and rapid expansion through acquisitions.

Intertek provides a diverse range of both military and civil Aerospace and Defence Services of all aspects of production and performance.

Bureau Veritas provides electrical safety testing and certification services that help gain access to global markets. This certification program test products against recognized safety standards relating to criteria such as electric shock, excessive temperature, radiation, implosion, and mechanical hazards and fire.

SGS SA is headquartered in Switzerland, SGS is one of the world’s largest TIC companies with extensive global presence. Known for inspection, verification, and environmental testing across industries.

Key Players

- Intertek Group Plc

- Bureau Veritas

- MISTRAS Group

- SGS SA

- Eurofins Scientific

- TUV Rheinland

- TUV SUD

- DEKRA SE

- Applus+

- DNV GL

Recent Developments

In March 2026, Panasonic has launched a liquid cooling systems business for AI data centers. This business focus on cooling systems for high-performance computing & generative AI servers and development of high-capacity cooling units (1,200 kW+) which aligns with rising demand from data centers and cloud computing.

In March 2026, ABB Robotics Partners with NVIDIA to Deliver Industrial-Grade Physical AI at Scale. The collaboration focuses on combining ABB Robotics’ software programming, design and simulation suite, RobotStudio, with the physically accurate simulation power of NVIDIA Omniverse libraries to close technology's long-standing 'sim-to-real’ gap. Developers can simulate robots in digital twins and generate synthetic data to train their physical AI models, enabling businesses of all types and sizes to deploy AI-driven robotics for various industrial workflows.

In February 2026, Google has awarded Form Energy, Inc. a USD billion contract to provide its cutting-edge iron-air batteries for a Minnesota data center project. One of the biggest and longest-lasting battery installations in the world, this project entails the deployment of a massive energy storage system that can provide electricity constantly for up to 100 hours. Iron-air batteries are less expensive for widespread use since they are made of inexpensive materials like iron.

Global TIC Market for Government & Public Sector Coverage

Service Type Insight and Forecast 2026 - 2035

- Testing

- Inspection

- Certification

Sourcing Type Insight and Forecast 2026 - 2035

- In-House

- Outsourced

End Use Application Insight and Forecast 2026 - 2035

- Infrastructure and Construction

- Energy and Utilities

- Transportation-related applications

Asset Lifecycle Stage Insight and Forecast 2026 - 2035

- Before the Commissioning Stage

- Lifecycle-based

Global TIC Market for Government & Public Sector by Region

- North America

- By Service Type

- By Sourcing Type

- By End Use Application

- By Asset Lifecycle Stage

- By Country - U.S., Canada, Mexico

- Europe

- By Service Type

- By Sourcing Type

- By End Use Application

- By Asset Lifecycle Stage

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Service Type

- By Sourcing Type

- By End Use Application

- By Asset Lifecycle Stage

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Service Type

- By Sourcing Type

- By End Use Application

- By Asset Lifecycle Stage

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for TIC Market for Government & Public Sector Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Service Type

1.2.2. By

Sourcing Type

1.2.3. By

End Use Application

1.2.4. By

Asset Lifecycle Stage

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Service Type

5.1.1. Testing

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Inspection

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Certification

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Sourcing Type

5.2.1. In-House

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Outsourced

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By End Use Application

5.3.1. Infrastructure and Construction

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Energy and Utilities

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Transportation-related applications

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.4. By Asset Lifecycle Stage

5.4.1. Before the Commissioning Stage

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Lifecycle-based

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Service Type

6.2. By

Sourcing Type

6.3. By

End Use Application

6.4. By

Asset Lifecycle Stage

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Service Type

7.2. By

Sourcing Type

7.3. By

End Use Application

7.4. By

Asset Lifecycle Stage

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Service Type

8.2. By

Sourcing Type

8.3. By

End Use Application

8.4. By

Asset Lifecycle Stage

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Service Type

9.2. By

Sourcing Type

9.3. By

End Use Application

9.4. By

Asset Lifecycle Stage

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Intertek Group Plc

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Bureau Veritas

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

MISTRAS Group

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

SGS SA

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Eurofins Scientific

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

TUV Rheinland

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

TUV SUD

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

DEKRA SE

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Applus+

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

DNV GL

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

TIC Market for Government & Public Sector