Physical Security TIC Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Service Type (Testing, Inspection, Certification), by Security System Type (Video surveillance, Access Control, Intrusion Detection), by End User (Government and Public Sector, Commercial Facilities, Industrial Sites, Residential End Users), by Compliance Commercial Buildings (Legal Requirements, Insurance Checks, Safety oversight)

| Status : Published | Published On : Apr, 2026 | Report Code : VRSME9206 | Industry : Semiconductor & Electronics | Available Format :

|

Page : 175 |

Physical Security TIC Market Overview

The global TIC Market for Physical Security, which was valued at approximately USD 760 billion in 2025 and is estimated to reach around USD 800 billion in 2026, is projected to reach approximately USD 1400 billion by 2035, expanding at a CAGR of about 6.36% during the forecast period from 2026 to 2035.

There is an increase in demand for physical security owing to rising incidences of terror attacks, technological development and deployment of wireless technology in security systems, growing use of IP-based cameras for video surveillance, and increasing use of IoT-based security systems with cloud computing platforms which will propel the growth of TIC market for physical security.

TIC companies are catering to different industrial sectors such as agriculture, automotive, IT and electronics, physical security, building & construction, environmental protection, food testing, and oil and gas, maritime, medicine, education, tourism, logistics, consumer products, etc. and provide various standards and legislation.

Complex, integrated security systems that require rigorous testing and certification is driven by the growing urbanization. The aim of the Testing, Inspection, and Certification (TIC) industry for physical security is ensured by the dependability and security of security systems. The market is further supported by strict legislative frameworks and standards related to data security, safety, and system compatibility. While North America and Europe lead the region due to stringent restrictions and extensive usage of state-of-the-art security systems, Asia-Pacific is rapidly growing as a result of smart city projects and infrastructure development.

In general, the TIC market for physical security is vital to improving public safety, regulatory compliance, and system dependability in a variety of businesses. The usage of digital compliance solutions and remote inspections is also improving service delivery efficiency. Market expansion is being driven by growing concerns about terrorism, cyber-physical threats, and the security of critical infrastructure in sectors like government, banking, transportation, and commercial facilities.

Physical Security TIC Market Dynamics

Market Trends

The key concepts include the digitization of testing procedures, remote audits and the application of AI-driven analytics, along with the growing need for end-to-end compliance solutions.

Stricter global regulatory frameworks are too driving the need for third-party testing, inspection, and certification services to ensure compliance and patient safety.

Automation and artificial intelligence are transforming TIC services by improving testing accuracy, predictive analytics, and inspection efficiency. AI is being utilized more and more in drug development and quality control to improve compliance procedures while cutting costs and schedules.

Growth Drivers

More global dangers boost sales of safety checks for buildings and equipment. Attacks on vital sites, stolen goods, or people getting in without permission went up close to 18% during the last half decade - so cities, states, and firms now require audits, reviews, but also approvals for cameras, entry systems, warning setups. Needing these inspections just to follow rules adds about 7% more work each year.

More smart buildings plus essential facilities mean more demand for testing checks. Around six out of ten brand-new business structures worldwide already use combined security setups, needing outside verification to prove they work right and stay safe. Assessments on intelligent cameras, fingerprint entry tech, alongside boundary safeguards are climbing - about 8.2% yearly growth rate.

Tougher rules on safety push the market ahead. Because of standards like ISO 22301 or EN 50131, companies must pass checks and get certified now and then. In areas like transit spots, server rooms, or government buildings, almost four out of ten service needs come from these legal demands - thanks to codes from UL or local authorities.

Market Restraints / Challenges

The testing, inspection, and certification market in physical security may face certain challenges like trade wars and growth fluctuations, huge investment for automation and installation of industrial safety systems, integration issues among security solutions, device vulnerability and chances of system being hacked, and high cost of TIC owing to diverse standards and regulations globally. Moreover, a lack of testing facilities and skilled personnel may hamper the growth of the TIC market.

Market Opportunities

Testing, inspection, and certification is a massive market that provides lucrative opportunities in technologies such as AI, robotics, drones, big data analytics, next-generation automation, and cloud and cybersecurity. Moreover, the technological development and use of IP-based HD video in video surveillance, and the emergence of automated drones for security trolling will create promising opportunities for the growth of the TIC market in physical security.

Global Physical Security TIC Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 760 Billion |

|

Revenue Forecast in 2035 |

USD 1400 Billion |

|

Growth Rate |

6.36% |

|

Segments Covered in the Report |

Service Type, Security System Type, End User and Compliance Requirement |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific |

|

Key Companies |

Intertek Group plc, Bureau Veritas, UL LLC, SGS SA, Eurofins USA, TUV Rheinland, DEKRA SE, ALS Limited, Applus+, and DNV GL |

|

Customization |

Available upon request |

Physical Security TIC Market Segmentation

By Service Type

By kind of service, you’ve got testing, inspection, certification, or audits. Testing’s growing quickest - close to 8.9% each year - thanks to checking how well cameras, entry controls, alarms, also linked security setups work in offices and public buildings.

Testing takes nearly half the market - about 46% - since systems must work right before going live. On top of that, inspections are picking up pace because officials demand real-world validation and regular safety reviews.

Certification helps meet global and local safety rules. As companies use risk-focused security models, audits become more common.

By Security System Type

Video surveillance, access control, intrusion detection - these make up the main types of security setups found today. It’s video that's rising quickest, around 9.5% each year.

This jump comes from more IP cameras being used everywhere. Smart monitoring powered by AI adds fuel too. So do government-backed citywide watch programs spreading across countries.

Access control setups boost TIC needs because they use biometrics or connect with other tech. Burglar alarms need frequent checks since insurers or safety rules say so.

Perimeter security checks are growing at power plants, airports, also factories - spots where breakdowns can cause big trouble.

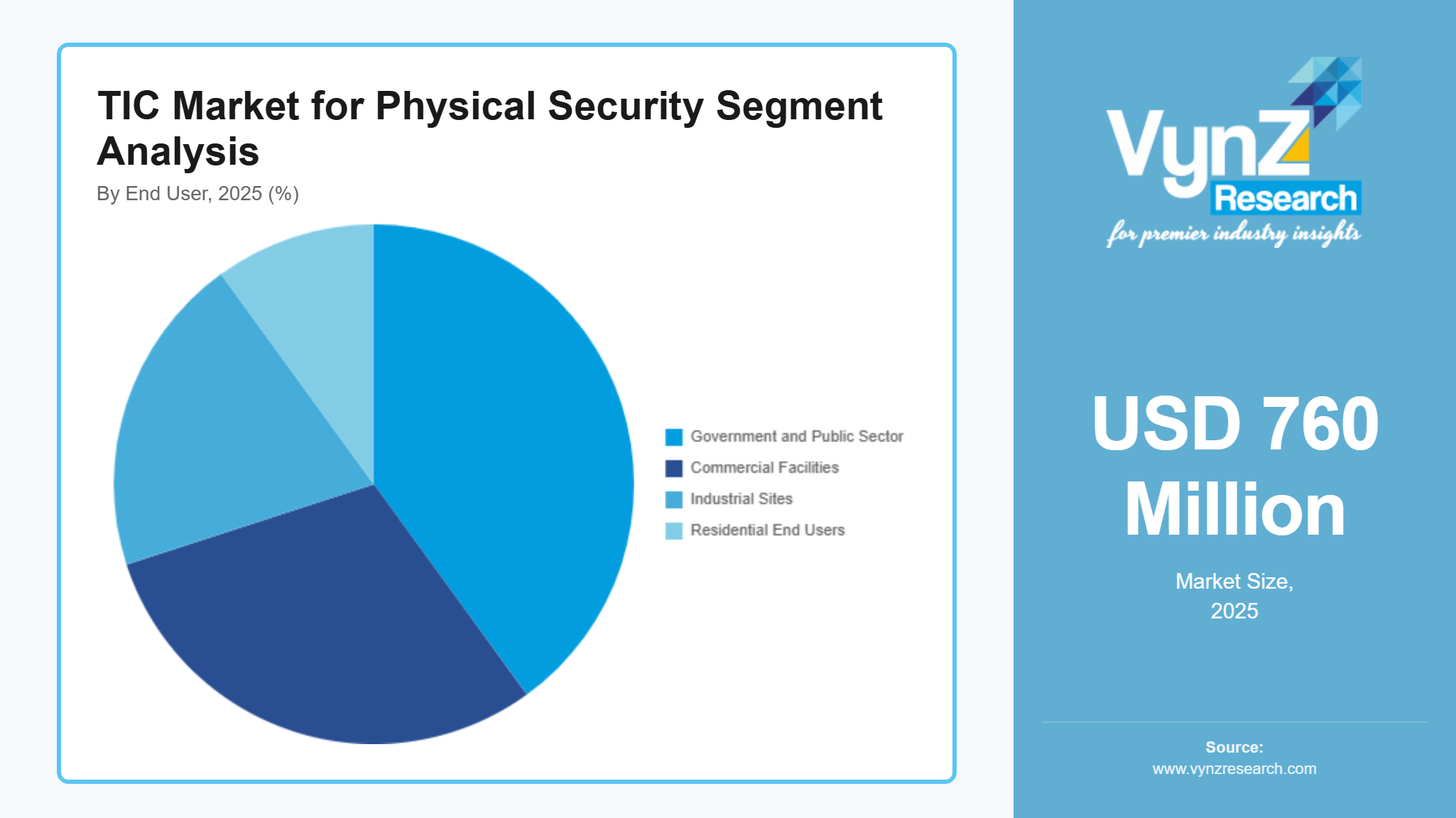

By End User

The market reaches offices, state-run sites, factories, also homes. State projects take up around 38–40% of testing checks because rules require inspections plus big safety setups are common there.

Commercial buildings are growing quickly - about 8% each year - as companies upgrade their security setups. Meanwhile, industrial sites need regular check-ups to keep equipment and workers safe.

Home safety checks are rising slowly - thanks to smarter homes plus secure neighbour -hoods popping up everywhere.

By Compliance Requirement

Because rules demand it, TIC services handle legal requirements, insurance checks, safety oversight, while also measuring how well things perform. The part about meeting laws grows quickest - around 9.1% each year - as safety rules change more often now, alongside stricter penalties.

Inspections tied to insurance are growing - firms now want verified setups that cut down on potential losses. These safety checks help boost readiness during crises while strengthening how well systems hold up under pressure.

As companies aim for better protection plus steady operations over time, testing performance starts catching on.

Regional Insights

North America

North America still leads as the top market, expanding by around 6.8% each year. Because government sites, airports, or data hubs widely use high-tech security setups, testing and inspection services stay in high need.

Frequent checks thrive under tight rules or insurer demands. Certification work thrives most in the U.S., thanks to demand or local standards.

Rising funds for vital infrastructure safeguards also boost the region’s TIC market outlook over time.

Asia Pacific

Asia Pacific’s growing quicker than anywhere else - close to 9.5% every year - thanks to cities spreading fast and new infrastructure popping up. Big smart city plans across China, India, or parts of Southeast Asia push demand for wide-reaching security setups.

Rules from officials to keep people safe boost checks by outside firms. At the same time, growing office spaces push up need for reviews and approvals.

Factories rising locally push global inspection companies to boost their nearby lab services.

Europe

Europe’s economy inches up yearly by roughly 6%, thanks to strict rules and solid safety norms. Bus stations, old landmarks, or official sites keep pushing need for testing services.

Across the EU, rules on safety demand approved setups plus routine checks. Using monitoring methods that fit GDPR brings extra challenges.

Europe's testing firms stick to premium certifications, while also offering guidance on rules to stay ahead.

Competitive Landscape / Company Insights

With a combination of international TIC providers and specialized security testing companies, the TIC market for physical security is quite consolidated. Acquisitions are looked for the expansion of their geographic reach and service offerings. Accreditation, technical know-how, and regulatory compliance are more important than price. AI-enabled testing, IoT validation, and cybersecurity integration for linked security systems are ways that players set themselves apart. While mid-sized businesses concentrate on specialized services and local markets, large enterprises predominate because of their high compliance credentials.

Mini Profiles

Intertek Group plc, is an UK-based multinational assurance and TIC provider with operations in over 100 countries. It offers quality assurance, product testing, and certification across industries including security systems. Intertek leverages a vast global laboratory network and focuses on digital testing and compliance solutions.

Bureau Veritas, that is founded in 1828, is a France-based global TIC leader operates in 140+ countries. It provides inspection, certification, and testing services across multiple sectors, including infrastructure and security. The company emphasizes innovation, sustainability, and digital transformation to strengthen compliance solutions.

MISTRAS Group, is an US-based provider specializing in asset protection, inspection, and advanced non-destructive testing (NDT). MISTRAS supports physical security and infrastructure integrity through real-time monitoring and analytics, particularly in industrial and critical infrastructure sectors.

SGS SA is the one of the world’s leading TIC companies, SGS offers comprehensive testing, inspection, and certification services. It is known for its strong global presence, digital compliance capabilities, and focus on sustainability and quality assurance across regulated industries.

Eurofins Scientific which is a global laboratory testing company with strong expertise in analytical testing. Eurofins supports security-related testing and certification through specialized labs and advanced technologies, particularly in regulated and high-precision environments.

Key Players

- Intertek Group Plc

- Bureau Veritas

- MISTRAS Group

- SGS SA

- Eurofins Scientific

- TUV Rheinland

- TUV SUD

- DEKRA SE

- Applus+

- DNV GL

Recent Developments

In March 2026, Panasonic has launched a liquid cooling systems business for AI data centers. This business focus on cooling systems for high-performance computing & generative AI servers and development of high-capacity cooling units (1,200 kW+) which aligns with rising demand from data centers and cloud computing.

In March 2026, ABB Robotics Partners with NVIDIA to Deliver Industrial-Grade Physical AI at Scale. The collaboration focuses on combining ABB Robotics’ software programming, design and simulation suite, RobotStudio, with the physically accurate simulation power of NVIDIA Omniverse libraries to close technology's long-standing 'sim-to-real’ gap. Developers can simulate robots in digital twins and generate synthetic data to train their physical AI models, enabling businesses of all types and sizes to deploy AI-driven robotics for various industrial workflows.

In February 2026, Google has awarded Form Energy, Inc. a USD billion contract to provide its cutting-edge iron-air batteries for a Minnesota data center project. One of the biggest and longest-lasting battery installations in the world, this project entails the deployment of a massive energy storage system that can provide electricity constantly for up to 100 hours. Iron-air batteries are less expensive for widespread use since they are made of inexpensive materials like iron.

Global Physical Security TIC Market Coverage

Service Type Insight and Forecast 2026 - 2035

- Testing

- Inspection

- Certification

Security System Type Insight and Forecast 2026 - 2035

- Video surveillance

- Access Control

- Intrusion Detection

End User Insight and Forecast 2026 - 2035

- Government and Public Sector

- Commercial Facilities

- Industrial Sites

- Residential End Users

Compliance Commercial Buildings Insight and Forecast 2026 - 2035

- Legal Requirements

- Insurance Checks

- Safety oversight

Global Physical Security TIC Market by Region

- North America

- By Service Type

- By Security System Type

- By End User

- By Compliance Commercial Buildings

- By Country - U.S., Canada, Mexico

- Europe

- By Service Type

- By Security System Type

- By End User

- By Compliance Commercial Buildings

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Service Type

- By Security System Type

- By End User

- By Compliance Commercial Buildings

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Service Type

- By Security System Type

- By End User

- By Compliance Commercial Buildings

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Physical Security TIC Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Service Type

1.2.2. By

Security System Type

1.2.3. By

End User

1.2.4. By

Compliance Commercial Buildings

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Service Type

5.1.1. Testing

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Inspection

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Certification

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Security System Type

5.2.1. Video surveillance

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Access Control

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Intrusion Detection

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By End User

5.3.1. Government and Public Sector

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Commercial Facilities

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Industrial Sites

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Residential End Users

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.4. By Compliance Commercial Buildings

5.4.1. Legal Requirements

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Insurance Checks

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Safety oversight

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Service Type

6.2. By

Security System Type

6.3. By

End User

6.4. By

Compliance Commercial Buildings

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Service Type

7.2. By

Security System Type

7.3. By

End User

7.4. By

Compliance Commercial Buildings

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Service Type

8.2. By

Security System Type

8.3. By

End User

8.4. By

Compliance Commercial Buildings

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Service Type

9.2. By

Security System Type

9.3. By

End User

9.4. By

Compliance Commercial Buildings

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Intertek Group Plc

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Bureau Veritas

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

MISTRAS Group

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

SGS SA

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Eurofins Scientific

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

TUV Rheinland

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

TUV SUD

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

DEKRA SE

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Applus+

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

DNV GL

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Physical Security TIC Market