Green AI Infrastructure Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Infrastructure Type (Green data centers, Edge AI infrastructure, Cloud AI infrastructure, Hybrid AI infrastructure, Energy efficient computing systems), by Component (AI servers and processors, Cooling and thermal management systems, Networking equipment, Infrastructure management software, Energy monitoring and optimization solutions), by Deployment Model (On premises, Cloud based, Hybrid infrastructure, Edge deployment environments), by AI Technology (Machine learning and deep learning, Natural language processing, Computer vision, Generative AI, Reinforcement learning), by End User (Cloud service providers, Enterprise IT organizations, Government and defense institutions, Healthcare organizations, Automotive and mobility companies, BFSI institutions, Retail and e commerce companies, Colocation data center operators), by Region (North America, Europe, Asia Pacific, Rest of the World)

| Status : Published | Published On : May, 2026 | Report Code : VRSME9214 | Industry : Semiconductor & Electronics | Available Format :

|

Page : 134 |

Green AI Infrastructure Market Overview

The global green AI infrastructure market, which was valued at approximately USD 15.2 billion in 2025 and is estimated to reach around USD 19.39 billion in 2026, is projected to reach approximately USD 173.92 billion by 2035, expanding at a CAGR of about 27.6% during the forecast period from 2026 to 2035.

Market expansion is driven by fast scaling of energy efficient artificial intelligence compute environments and the growing roll out of low carbon data center architectures. Global energy and digital infrastructure evaluations supported by international energy agencies along with sustainability aligned digital transformation blueprints indicate a rise in electricity use from hyperscale computing systems. This is increasing the demand for optimized and efficient AI workloads.

Government backed climate neutrality initiatives and digital infrastructure upgrades are making adoption easier across both enterprise and cloud ecosystems. Public sector actions aimed at carbon reduction inside digital operations and stronger regulatory standards for sustainable computing practices are pushing companies toward improved cooling systems, data centers powered by renewables, and more efficient AI hardware architectures.

Green AI Infrastructure Market Dynamics

Market Trends

The market is witnessing a shift toward data centers that are more energy efficient and a broader adoption of low carbon computing. There is an increased deployment of liquid cooling and more advanced thermal management systems for better efficiency and sustainability in high density AI workloads. Energy efficiency support from governments and the whole digital infrastructure sustainability framework is pushing adoption of optimized cooling and power management solutions across most major economies. Renewable powered data centers are getting paired with carbon aware computing models to ensure regulatory alignment and uphold national decarbonization policies.

Growth Drivers

The growth of the market is supported by demand that keeps climbing for energy efficient cloud computing and AI workload optimization across both enterprise and hyperscale settings. More investments in green data centers and renewable integration projects are helping the market expand. Public sector energy transition initiatives and digital sustainability programs are also reinforcing adoption during global infrastructure development. AI workloads are getting more intense and pushing demand among enterprises that prioritize cost efficiency, performance tuning and regulatory compliance.

Market Restraints / Challenges

The market players face high initial investment costs for sustainable infrastructure and advanced cooling systems which slow down adoption for smaller operators. Regulatory complexity across different regions raises compliance requirements to prolong deployment timelines. Supply chain dependency for semiconductors and high efficiency hardware components creates cost pressure and procurement delays which affect scalability and operational efficiency.

Market Opportunities

Strong opportunities lie in development of modular and energy optimized AI infrastructure solutions driven by demand for sustainable cloud and edge computing. Companies that focus on scalable green data center technologies can meet higher demand and with renewable integrated infrastructure and AI driven energy optimization systems along with increasing investment in digital sustainability and automation technologies, opportunities are wider. Government backed clean energy and digital transformation initiatives are also likely to speed up long term expansion.

Global Green AI Infrastructure Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 15.2 Billion |

|

Revenue Forecast in 2035 |

USD 173.92 Billion |

|

Growth Rate |

27.6% |

|

Segments Covered in the Report |

Infrastructure Type, Component, Deployment Model, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

AMD, Amazon Web Services, Cisco, Dell Technologies, Digital Realty, Equinix, Google (Alphabet), Hewlett Packard Enterprise, IBM, Microsoft |

|

Customization |

Available upon request |

Green AI Infrastructure Market Segmentation

By Infrastructure Type

Green data centers accounted for the largest share of the market in 2025, representing approximately 48% of total revenue. Their dominance is driven by increasing deployment of hyperscale AI workloads, renewable-powered facilities, and advanced cooling technologies designed to reduce energy consumption and carbon emissions. Rising investments by cloud providers and enterprise operators in sustainable computing infrastructure continue to strengthen segment growth globally.

Edge AI infrastructure is projected to witness the fastest growth during the forecast period from 2026 to 2035, with an estimated CAGR of 18.9%. Growth is supported by rising demand for low-latency AI processing across smart cities, industrial automation, autonomous vehicles, and IoT applications. Increasing adoption of decentralized and energy-efficient computing systems is further accelerating market expansion.

By Component

AI servers and processors accounted for the largest market share in 2025, contributing approximately 46% of segment revenue. Their dominance reflects growing demand for high-performance GPUs, TPUs, and AI accelerators capable of supporting large-scale machine learning and generative AI workloads. Technological advancements in energy-efficient semiconductor architectures are further driving adoption across enterprise and hyperscale environments.

Energy monitoring and optimization solutions are expected to register the fastest growth during 2026 to 2035, with an estimated CAGR of 19.4%. Increasing focus on carbon reduction, intelligent power management, and infrastructure efficiency optimization is encouraging organizations to deploy AI-powered energy analytics and workload management solutions.

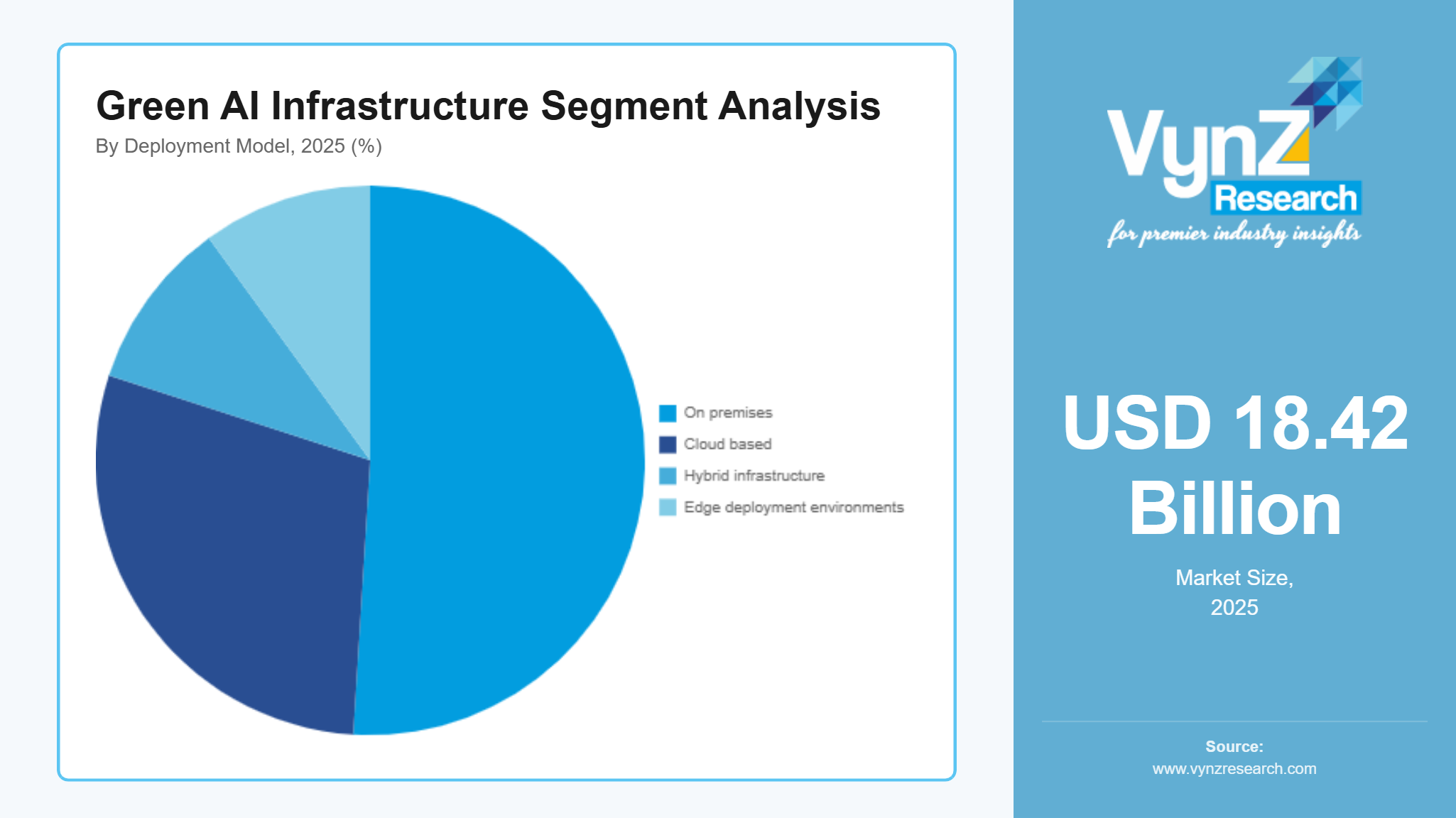

By Deployment Model

Cloud-based infrastructure held the largest market share in 2025, representing approximately 51% of total revenue. Growth is driven by increasing enterprise reliance on AI-as-a-service platforms, scalable computing resources, and renewable-powered hyperscale cloud facilities. Major cloud providers continue investing in sustainable operations and advanced cooling systems to support rising AI demand.

Hybrid infrastructure is anticipated to witness the fastest growth during the forecast period, expanding at a CAGR of approximately 18.6%. Organizations are increasingly adopting hybrid models that combine cloud scalability with the security and control of on-premises infrastructure. Rising regulatory requirements related to data privacy and energy efficiency are further supporting segment growth.

By End User

Cloud service providers accounted for the largest share of the market in 2025, contributing approximately 42% of total revenue. Their dominance is supported by extensive investments in hyperscale AI data centers, renewable energy integration, and sustainable cloud computing infrastructure. Expansion of enterprise AI adoption and increasing demand for AI cloud services continue to reinforce segment growth.

Government and defense institutions are projected to register the fastest growth from 2026 to 2035, with an estimated CAGR of 17.8%. Growth is driven by increasing investments in secure and energy-efficient AI infrastructure, digital transformation initiatives, and government sustainability mandates aimed at reducing emissions from public-sector computing operations.

Regional Insights

North America

North America accounted for approximately 33% of the market in 2025 driven by strong hyperscale data center concentration, rapid expansion of artificial intelligence workloads and advanced cloud ecosystem maturity. Major technology clusters across the United States and Canada continue to attract significant investments in energy efficient computing infrastructure. Government backed initiatives, including federal energy efficiency programs and digital sustainability frameworks supported by the U.S. Department of Energy, are accelerating deployment of low carbon data center systems. Increasing enterprise demand for renewable powered cloud services and high-performance computing optimization is further strengthening regional market expansion.

Europe

Europe accounted for approximately 28% of the market in 2025, supported by strict carbon neutrality regulations, strong industrial decarbonization mandates and widespread adoption of sustainable digital infrastructure standards. Key economies such as Germany, the United Kingdom, France and the Netherlands are leading investments in energy optimized data center ecosystems. Policy frameworks aligned with European Commission climate objectives and energy efficiency directives are encouraging large scale adoption of green computing technologies. Growing enterprise transition toward low emission cloud infrastructure and rising public sector digital transformation initiatives are reinforcing consistent regional demand.

Asia Pacific

Asia Pacific accounted for approximately 27% of the green AI infrastructure market in 2025, driven by rapid digitalization, expanding data center capacity and strong AI adoption across China, India, Japan and South Korea. Government led initiatives supporting smart cities, renewable integration, and ICT modernization, including programs supported by ministries of electronics and information technology in major economies, are significantly boosting infrastructure development. Increasing hyperscale cloud investments and rising manufacturing sector digitization are further accelerating adoption of energy efficient AI infrastructure solutions across the region.

Rest of the World

Rest of the world including the Middle East & Africa accounted for approximately 12% of the green AI infrastructure market in 2025, driven by increasing investments in smart city development, economic diversification strategies and expanding digital infrastructure projects in countries such as the United Arab Emirates, Saudi Arabia and South Africa. National transformation programs and energy efficiency initiatives supported by regional government authorities are encouraging deployment of advanced data center systems. Rising enterprise cloud adoption and growing demand for digital services are further contributing to steady market expansion across the region.

Competitive Landscape / Company Insights

The market is moderately to highly competitive with the presence of global and regional players focusing on energy efficient innovation, sustainable data center solutions and geographic expansion across high growth regions. Companies are increasingly investing in research and development, advanced cooling technologies and digital energy optimization capabilities to strengthen their market position. Government backed energy efficiency frameworks and international sustainability guidelines supported by agencies such as the International Energy Agency and national energy departments are encouraging compliance driven innovation. Strategic partnerships, renewable integration, and AI driven infrastructure management solutions are further shaping competitive intensity across the market.

Mini Profiles

AMD focuses on high performance computing processors and AI accelerators, supported by strong innovation capabilities and cost-efficient architecture design, enabling wide adoption across cloud, data center, and AI infrastructure environments globally.

Amazon Web Services operates in the premium cloud infrastructure segment, emphasizing scalable AI computing, advanced cloud services, and integrated data center solutions supported by strong global distribution and hyperscale infrastructure network capabilities.

Cisco leverages strategic partnerships and digital networking solutions to expand market presence, offering advanced networking hardware and software that support secure, scalable, and energy efficient AI infrastructure connectivity worldwide.

Dell Technologies focuses on enterprise IT infrastructure and server solutions, supported by strong brand recognition and global distribution strength, enabling efficient deployment of scalable computing systems for AI driven workloads.

Equinix operates in the premium colocation and data center interconnection segment, emphasizing high performance connectivity and global interconnection ecosystems supported by extensive multi region data center infrastructure presence.

Key Players

- AMD

- Amazon Web Services

- Cisco

- Dell Technologies

- Digital Realty

- Equinix

- Google (Alphabet)

- Hewlett Packard Enterprise

- IBM

- Microsoft

Recent Developments

In April 2025, AMD announced the expansion of its AI infrastructure ecosystem through its “Advancing AI 2025” initiative, focusing on next generation Instinct GPUs and rack scale data center solutions. The development strengthens AMD’s positioning in high performance AI computing and energy efficient infrastructure deployment across hyperscale environments.

In November 2025, Microsoft signed a $9.7 billion strategic contract with IREN to secure Nvidia powered AI computing capacity for its expanding data center requirements. The agreement supports large scale deployment of liquid cooled infrastructure and reflects rising demand for scalable AI compute resources across enterprise cloud systems.

In November 2025, Cisco entered a strategic joint venture with AMD and HUMAIN to develop up to 1 GW of advanced AI infrastructure capacity. The collaboration focuses on building energy efficient data center ecosystems integrated with next generation networking and compute technologies for large scale AI workloads.

In October 2025, NVIDIA expanded its AI infrastructure footprint by announcing a major AI Factory Research Center in partnership with Digital Realty in Virginia. The facility is designed to accelerate generative AI and large-scale computing research through advanced GPU driven data center architecture.

In October 2025, Digital Realty strengthened its AI infrastructure strategy by supporting NVIDIA powered AI factory deployments across hyperscale data center ecosystems. The initiative focuses on expanding colocation capacity for AI workloads and improving energy efficient infrastructure scalability across global markets.

Global Green AI Infrastructure Market Coverage

Infrastructure Type Insight and Forecast 2026 - 2035

- Green data centers

- Edge AI infrastructure

- Cloud AI infrastructure

- Hybrid AI infrastructure

- Energy efficient computing systems

Component Insight and Forecast 2026 - 2035

- AI servers and processors

- Cooling and thermal management systems

- Networking equipment

- Infrastructure management software

- Energy monitoring and optimization solutions

Deployment Model Insight and Forecast 2026 - 2035

- On premises

- Cloud based

- Hybrid infrastructure

- Edge deployment environments

AI Technology Insight and Forecast 2026 - 2035

- Machine learning and deep learning

- Natural language processing

- Computer vision

- Generative AI

- Reinforcement learning

End User Insight and Forecast 2026 - 2035

- Cloud service providers

- Enterprise IT organizations

- Government and defense institutions

- Healthcare organizations

- Automotive and mobility companies

- BFSI institutions

- Retail and e commerce companies

- Colocation data center operators

Region Insight and Forecast 2026 - 2035

- North America

- Europe

- Asia Pacific

- Rest of the World

Global Green AI Infrastructure Market by Region

- North America

- By Infrastructure Type

- By Component

- By Deployment Model

- By AI Technology

- By End User

- By Region

- By Country - U.S., Canada, Mexico

- Europe

- By Infrastructure Type

- By Component

- By Deployment Model

- By AI Technology

- By End User

- By Region

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Infrastructure Type

- By Component

- By Deployment Model

- By AI Technology

- By End User

- By Region

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Infrastructure Type

- By Component

- By Deployment Model

- By AI Technology

- By End User

- By Region

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Green AI Infrastructure Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Infrastructure Type

1.2.2. By

Component

1.2.3. By

Deployment Model

1.2.4. By

AI Technology

1.2.5. By

End User

1.2.6. By

Region

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Infrastructure Type

5.1.1. Green data centers

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Edge AI infrastructure

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Cloud AI infrastructure

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Hybrid AI infrastructure

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Energy efficient computing systems

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.2. By Component

5.2.1. AI servers and processors

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Cooling and thermal management systems

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Networking equipment

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Infrastructure management software

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. Energy monitoring and optimization solutions

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.3. By Deployment Model

5.3.1. On premises

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Cloud based

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Hybrid infrastructure

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Edge deployment environments

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.4. By AI Technology

5.4.1. Machine learning and deep learning

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Natural language processing

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Computer vision

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Generative AI

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Reinforcement learning

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

5.5. By End User

5.5.1. Cloud service providers

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Enterprise IT organizations

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Government and defense institutions

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Healthcare organizations

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

5.5.5. Automotive and mobility companies

5.5.5.1. Market Definition

5.5.5.2. Market Estimation and Forecast to 2035

5.5.6. BFSI institutions

5.5.6.1. Market Definition

5.5.6.2. Market Estimation and Forecast to 2035

5.5.7. Retail and e commerce companies

5.5.7.1. Market Definition

5.5.7.2. Market Estimation and Forecast to 2035

5.5.8. Colocation data center operators

5.5.8.1. Market Definition

5.5.8.2. Market Estimation and Forecast to 2035

5.6. By Region

5.6.1. North America

5.6.1.1. Market Definition

5.6.1.2. Market Estimation and Forecast to 2035

5.6.2. Europe

5.6.2.1. Market Definition

5.6.2.2. Market Estimation and Forecast to 2035

5.6.3. Asia Pacific

5.6.3.1. Market Definition

5.6.3.2. Market Estimation and Forecast to 2035

5.6.4. Rest of the World

5.6.4.1. Market Definition

5.6.4.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Infrastructure Type

6.2. By

Component

6.3. By

Deployment Model

6.4. By

AI Technology

6.5. By

End User

6.6. By

Region

6.6.1.

U.S. Market Estimate and Forecast

6.6.2.

Canada Market Estimate and Forecast

6.6.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Infrastructure Type

7.2. By

Component

7.3. By

Deployment Model

7.4. By

AI Technology

7.5. By

End User

7.6. By

Region

7.6.1.

Germany Market Estimate and Forecast

7.6.2.

France Market Estimate and Forecast

7.6.3.

U.K. Market Estimate and Forecast

7.6.4.

Italy Market Estimate and Forecast

7.6.5.

Spain Market Estimate and Forecast

7.6.6.

Russia Market Estimate and Forecast

7.6.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Infrastructure Type

8.2. By

Component

8.3. By

Deployment Model

8.4. By

AI Technology

8.5. By

End User

8.6. By

Region

8.6.1.

China Market Estimate and Forecast

8.6.2.

Japan Market Estimate and Forecast

8.6.3.

India Market Estimate and Forecast

8.6.4.

South Korea Market Estimate and Forecast

8.6.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Infrastructure Type

9.2. By

Component

9.3. By

Deployment Model

9.4. By

AI Technology

9.5. By

End User

9.6. By

Region

9.6.1.

Brazil Market Estimate and Forecast

9.6.2.

Saudi Arabia Market Estimate and Forecast

9.6.3.

South Africa Market Estimate and Forecast

9.6.4.

U.A.E. Market Estimate and Forecast

9.6.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

AMD

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Amazon Web Services

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Cisco

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Dell Technologies

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Digital Realty

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Equinix

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Google (Alphabet)

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Hewlett Packard Enterprise

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

IBM

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Microsoft

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Green AI Infrastructure Market