Grid-Scale Battery Recycling Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Recycling Process (Pyrometallurgical, Hydrometallurgical, Direct recycling, Mechanical pre treatment systems), by Battery Chemistry (Lithium ion batteries, Lead acid batteries, Nickel based batteries, Solid state batteries), by Source (Electric vehicle batteries, Stationary energy storage systems, Industrial batteries, Consumer electronics derived batteries), by End User (Battery recyclers, Raw material manufacturers, Automotive OEMs, Energy utilities, Waste management companies)

| Status : Published | Published On : May, 2026 | Report Code : VRSME9215 | Industry : Semiconductor & Electronics | Available Format :

|

Page : 132 |

Grid-Scale Battery Recycling Market Overview

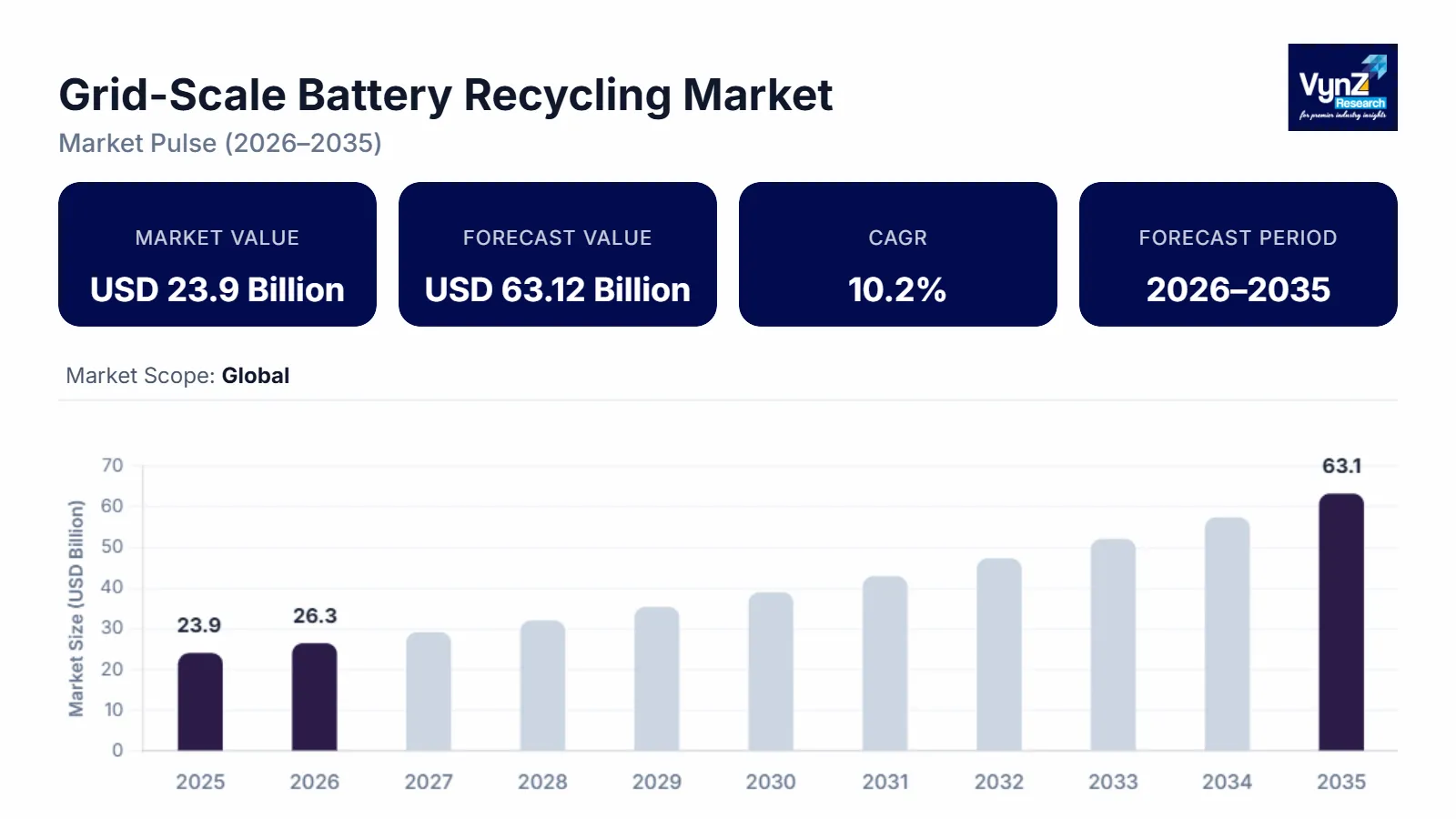

The global grid scale battery recycling market which was valued at approximately USD 23.9 billion in 2025 and is estimated to reach around USD 26.33 billion in 2026, is projected to reach approximately USD 63.12 billion by 2035, expanding at a CAGR of about 10.2% during the forecast period from 2026 to 2035.

Market expansion is driven mostly by a steadily rising deployment of utility scale battery energy storage systems and a growing amount of end-of-life lithium-ion battery volumes coming from electric vehicles and grid storage setups. The International Energy Agency reviews and national clean energy transition reports show rising demand mostly because renewable integration keeps getting stricter for more sustainable recycling infrastructure.

Government efforts promote circular economy practices and critical mineral security making adoption easier across big markets. National battery waste management regulations, extended producer responsibility frameworks, and clean energy transition policies are helping large-scale investments into recycling facilities. Public sector initiatives back domestic supply chain resilience for lithium, cobalt, and nickel recovery, reinforcing expansion across North America Europe and Asia Pacific.

Grid-Scale Battery Recycling Market Dynamics

Market Trends

The market is moving to technology, advanced hydrometallurgical approaches and automated recycling processes that are faster and more repeatable. A major trend is the growing adoption of closed loop battery recycling systems for resource efficiency, sustainability and better recovery of critical minerals. Reports from the International Energy Agency show battery demand climbing alongside renewable energy integration and electric mobility pushing the market toward more efficient recycling ecosystems. Digital tracking and battery lifecycle management systems are driven by regulatory alignment and the broader digitalization of waste management infrastructure.

Growth Drivers

Growth of the market is mainly due to the rising roll out of utility scale energy storage systems that help stabilizing demand for renewable balancing and grid stabilization use cases. More funding into battery manufacturing capacity and energy storage infrastructure is also pushing the market expansion. Government backed clean energy transition programs and critical mineral security strategies are reinforcing the shift toward large scale recycling. The increased use of end of life lithium ion batteries by utilities EV makers and energy operators prioritize cost efficiency, regulatory compliance, and responsible sourcing, increasing the need for battery recycling and material recovery solutions.

Market Restraints / Challenges

A big issue of the market is the high capital investment needed for advanced recycling facilities, hydrometallurgical processing plants and automated sorting systems. This hurts profitability and create entry barriers, especially for smaller companies who are trying to scale up. Regulatory complexity and hazardous waste handling and environmental compliance requirements vary making expansion harder and slower. Operational hurdles are caused due to dependency on imported raw materials and specialized recycling technologies. In addition, the availability of skilled talent in battery chemistry and recycling engineering isn’t always enough and it creates cost pressures, processing delays, and scalability problems.

Market Opportunities

Opportunities in the market lie around building large scale lithium-ion battery recycling infrastructure which is backed by rising electric vehicle penetration and expanding renewable energy storage. expanding. Companies providing high efficiency, modular, and automated recycling solutions are positioned to win incremental demand from utilities, EV manufacturers, and energy storage operators. Another opportunity is critical mineral recovery and the idea of circular battery supply chains. As investments increase in sustainable material sourcing and domestic manufacturing policies, there are openings for better margins and long-term strategic partnerships.

Global Grid-Scale Battery Recycling Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 23.9 Billion |

|

Revenue Forecast in 2035 |

USD 63.12 Billion |

|

Growth Rate |

10.2% |

|

Segments Covered in the Report |

Recycling Process, Battery Chemistry, Source, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

American Battery Technology Company, BASF SE, Contemporary Amperex Technology Co. Limited (CATL), Fortum Battery Recycling, Glencore plc, Li-Cycle Holdings Corp., Northvolt AB, Redwood Materials Inc., Retriev Technologies Inc., Umicore SA |

|

Customization |

Available upon request |

Grid-Scale Battery Recycling Market Segmentation

By Recycling Process

In 2025, pyrometallurgical processes held the largest share of the market, around 39%, driven by the high processing capacity and extensive use in big metal recovery facilities. It gets a boost in developed areas due to its ability to deal with mixed battery chemistries and high-volume waste streams.

Hydrometallurgical processes are forecast to grow the quickest, with an estimated CAGR of 23.4% from 2026 to 2035 due to better recovery efficiency and a comparatively lower environmental footprint.

By Battery Chemistry

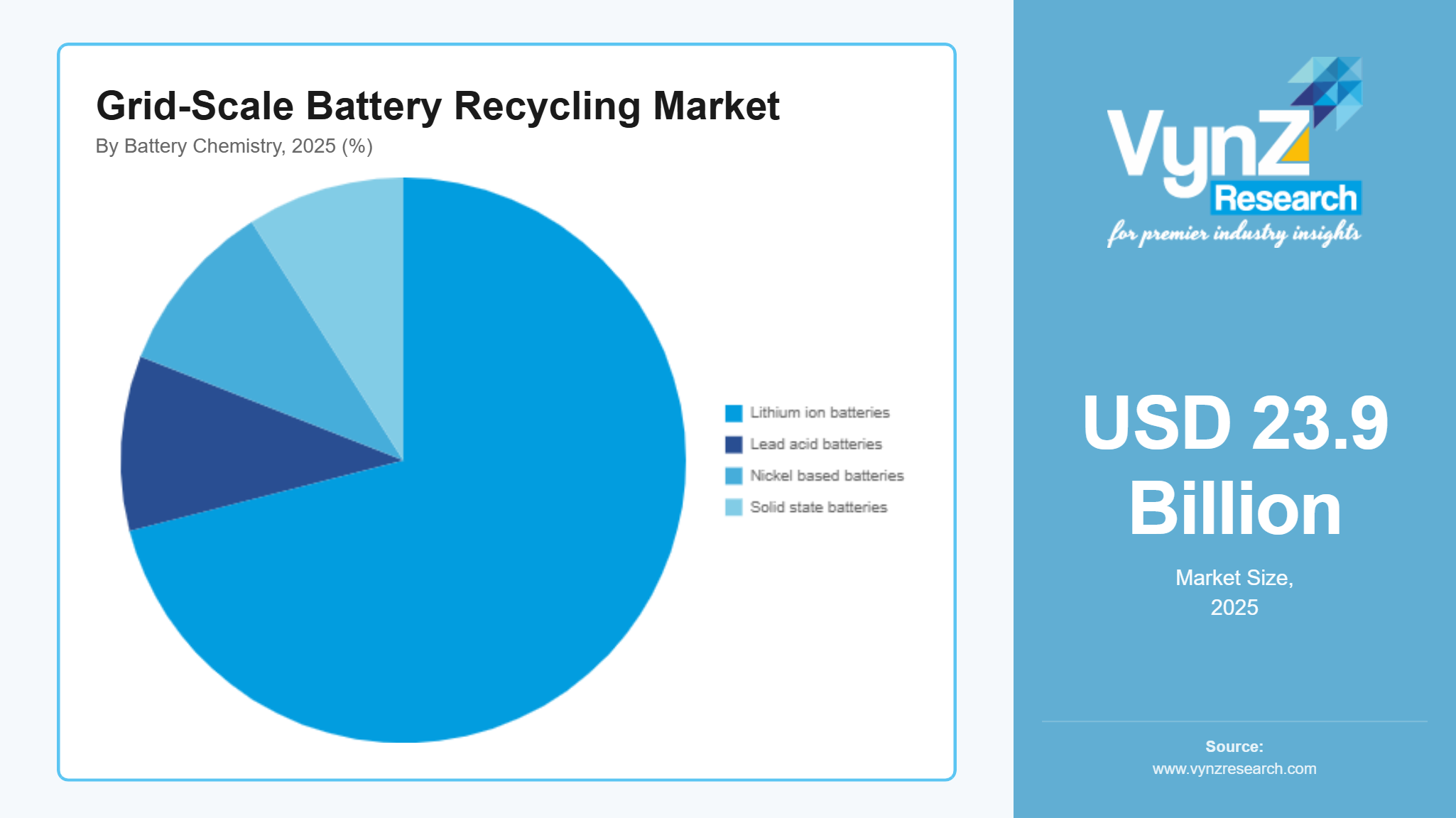

Lithium-ion batteries held the largest position in 2025, at roughly 71% share supported by heavy deployment across electric vehicles grid storage systems and renewable energy integration efforts. Policy backing for EV adoption and energy storage expansion keeps pushing huge amounts of recyclable lithium-ion waste into the system largely because more end-of-life batteries are reaching the point of disposal and the rising demand for critical minerals recover, including lithium, cobalt, and nickel. Government backed battery waste management rules are also helping build more organized recycling ecosystems worldwide.

By Source

Electric vehicle batteries accounted for the largest share in 2025, about 58%, driven by fast EV adoption and the large-scale installation of batteries in mobility uses. The growing retirement of early generation EV batteries is also pushing recycling volumes upward.

Electric vehicle battery recycling is also projected to be the fastest growing segment, with a CAGR of 24.1% between 2026 and 2035, driven by stronger EV penetration, tighter end of life management requirements, and government recycling obligations.

By End User

Battery recyclers made up the largest share in 2025, about 46%, mainly because of established infrastructure, solid technological know-how, and adherence to hazardous waste processing rules. The continued expansion of purpose-built recycling facilities and government supported circular economy programs is keeping their lead strong.

Energy utilities and automotive OEMs are expected to grow at the fastest pace, with an estimated CAGR of 22.9% from 2026 to 2035 due to a rising need for responsible battery lifecycle management along with higher investments in closed loop supply chains. Regulatory requirements that call for sustainable sourcing and recycling integration are further encouraging adoption across industrial ecosystems.

Regional Insights

North America

North America accounted for approximately 36% of the market in 2025, driven by rapid expansion of electric vehicle adoption, large scale deployment of utility energy storage systems and strong presence of advanced recycling infrastructure across the United States and Canada. Major industrial hubs such as California, Texas and Ontario continue to support high volumes of battery waste generation and recycling activity. Government initiatives led by environmental protection agencies and national energy departments, including extended producer responsibility frameworks and critical mineral recovery programs, are encouraging investments in recycling facilities, while expansion of circular economy policies and digital waste tracking systems is further strengthening regional market performance.

Europe

Europe accounted for approximately 32% of the market in 2025, supported by strict environmental regulations, aggressive decarbonization targets and strong implementation of battery waste management directives across Germany, France, the United Kingdom and Nordic countries. Increasing adoption of electric mobility and renewable energy storage systems is driving consistent demand for battery recycling infrastructure. Regulatory frameworks supported by European Union climate and sustainability policies, along with national level recycling mandates, are encouraging large scale investments in hydrometallurgical and advanced recovery facilities, while growing focus on domestic critical raw material security is further strengthening regional adoption.

Asia Pacific

Asia Pacific accounted for approximately 27% of the market in 2025, driven by rapid industrialization, expanding electric vehicle production and large-scale renewable energy installations across China, India, Japan and South Korea. Rising electricity demand and increasing battery manufacturing output are generating significant end of life battery volumes across the region. Government backed initiatives led by national energy ministries and environmental agencies, including battery recycling regulations and clean energy transition programs, are encouraging structured recycling infrastructure development, while growing investments in smart manufacturing and circular economy ecosystems are further accelerating regional growth.

Rest of the World

Rest of the world including Latin America, the Middle East, and Africa accounted for approximately 5% of the grid scale battery recycling market in 2025, driven by emerging investments in renewable energy storage projects, smart grid modernization, and early-stage electric mobility adoption. Countries such as Brazil, South Africa and the United Arab Emirates are gradually developing battery recycling frameworks supported by national sustainability and energy diversification programs. Government backed clean energy initiatives and international climate cooperation efforts are encouraging gradual infrastructure development, while increasing awareness of battery waste management is supporting long term market potential across the region.

Competitive Landscape / Company Insights

The market is moderately to highly competitive with the presence of global and regional players focusing on advanced recycling technologies, capacity expansion and geographic diversification across high growth regions. Companies are increasingly investing in research and development, automation and digital tracking systems to strengthen their market position. Government backed circular economy policies, extended producer responsibility frameworks, and critical mineral recovery initiatives supported by environmental protection agencies and energy ministries are encouraging large scale compliance driven investments. Strategic partnerships, vertical integration, and development of high efficiency hydrometallurgical and direct recycling solutions are further intensifying competition across the industry.

Mini Profiles

American Battery Technology Company focuses on lithium-ion battery recycling and critical mineral recovery, supported by advanced hydrometallurgical processes and strong innovation capabilities, enabling efficient domestic supply chain development in the United States.

BASF SE operates in premium chemical and materials recycling segments, emphasizing advanced battery material recovery and circular economy solutions, supported by strong global R&D capabilities and industrial partnerships across energy and automotive sectors.

Contemporary Amperex Technology Co. Limited leverages large scale battery manufacturing integration and strategic partnerships to expand market presence, strengthening closed loop recycling systems and enhancing lifecycle management across electric mobility and energy storage ecosystems.

Glencore plc focuses on large scale metal recovery and recycling operations, supported by strong global commodity trading networks and resource processing capabilities, enabling efficient recovery of cobalt, nickel, and lithium materials.

Li-Cycle Holdings Corp. operates in the niche battery recycling segment, emphasizing innovative spoke and hub processing technology, supported by strong North American expansion and partnerships with automotive and energy storage companies.

Key Players

- American Battery Technology Company

- BASF SE

- Contemporary Amperex Technology Co. Limited (CATL)

- Fortum Battery Recycling

- Glencore plc

- Li-Cycle Holdings Corp.

- Northvolt

- Redwood Materials Inc.

- Retriev

- Technologies Inc.

- Umicore SA

Recent Developments

In October 2025, Redwood Materials secured a $350 million funding round led by Eclipse Ventures with participation from Nvidia’s NVentures to expand its battery recycling and energy storage operations. The investment supports scaling of domestic critical mineral recovery and strengthening of grid energy storage systems linked to AI driven power demand.

In January 2026, Glencore expanded its battery recycling footprint through integration of Li-Cycle assets, strengthening its hydrometallurgical processing capabilities across North America and Europe. The move enhances its position in large scale recovery of lithium, nickel, and cobalt for circular supply chains.

In January 2026, CATL advanced its battery circular economy strategy by expanding recycling linked battery integration projects in Asia, focusing on large scale EV battery recovery systems. The initiative improves closed loop material recovery and strengthens domestic supply chain resilience for critical battery minerals.

In April 2026, Umicore expanded its battery materials recycling operations by increasing processing capacity for end-of-life lithium-ion batteries in Europe. The development supports rising demand for cobalt, nickel, and lithium recovery aligned with stricter EU circular economy regulations.

In February 2026, Fortum Battery Recycling strengthened its European operations by scaling advanced hydrometallurgical recycling capacity for EV batteries. The expansion focuses on improving metal recovery efficiency above 95% and supporting regional battery supply chain sustainability goals.

Global Grid-Scale Battery Recycling Market Coverage

Recycling Process Insight and Forecast 2026 - 2035

- Pyrometallurgical

- Hydrometallurgical

- Direct recycling

- Mechanical pre treatment systems

Battery Chemistry Insight and Forecast 2026 - 2035

- Lithium ion batteries

- Lead acid batteries

- Nickel based batteries

- Solid state batteries

Source Insight and Forecast 2026 - 2035

- Electric vehicle batteries

- Stationary energy storage systems

- Industrial batteries

- Consumer electronics derived batteries

End User Insight and Forecast 2026 - 2035

- Battery recyclers

- Raw material manufacturers

- Automotive OEMs

- Energy utilities

- Waste management companies

Global Grid-Scale Battery Recycling Market by Region

- North America

- By Recycling Process

- By Battery Chemistry

- By Source

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Recycling Process

- By Battery Chemistry

- By Source

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Recycling Process

- By Battery Chemistry

- By Source

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Recycling Process

- By Battery Chemistry

- By Source

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Grid-Scale Battery Recycling Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Recycling Process

1.2.2. By

Battery Chemistry

1.2.3. By

Source

1.2.4. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Recycling Process

5.1.1. Pyrometallurgical

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Hydrometallurgical

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Direct recycling

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Mechanical pre treatment systems

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.2. By Battery Chemistry

5.2.1. Lithium ion batteries

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Lead acid batteries

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Nickel based batteries

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Solid state batteries

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.3. By Source

5.3.1. Electric vehicle batteries

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Stationary energy storage systems

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Industrial batteries

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Consumer electronics derived batteries

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.4. By End User

5.4.1. Battery recyclers

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Raw material manufacturers

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Automotive OEMs

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Energy utilities

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Waste management companies

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Recycling Process

6.2. By

Battery Chemistry

6.3. By

Source

6.4. By

End User

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Recycling Process

7.2. By

Battery Chemistry

7.3. By

Source

7.4. By

End User

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Recycling Process

8.2. By

Battery Chemistry

8.3. By

Source

8.4. By

End User

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Recycling Process

9.2. By

Battery Chemistry

9.3. By

Source

9.4. By

End User

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

American Battery Technology Company

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

BASF SE

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Contemporary Amperex Technology Co. Limited (CATL)

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Fortum Battery Recycling

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Glencore plc

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Li-Cycle Holdings Corp.

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Northvolt AB

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Redwood Materials Inc.

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Retriev Technologies Inc.

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Umicore SA

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Grid-Scale Battery Recycling Market