All-terrain Vehicle Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Type (Utility ATV, Sport ATV, Recreational ATV), by Engine Capacity (Below 400cc, 400cc to 800cc, Above 800cc), by Application (Agriculture, Sports, Recreational / leisure, Military and defense), by Fuel Type (Gasoline powered, Electric), by Drive Type (Two-wheel drive, Four-wheel drive, All wheel drive), by Number of Wheels (Three wheels, Four wheels, Six wheels), by Battery Type (Lithium ion, Lead acid), by Seating Capacity (Single rider, Two-seater)

| Status : Published | Published On : May, 2026 | Report Code : VRAT9675 | Industry : Automotive & Transportation | Available Format :

|

Page : 165 |

All-terrain Vehicle Market Overview

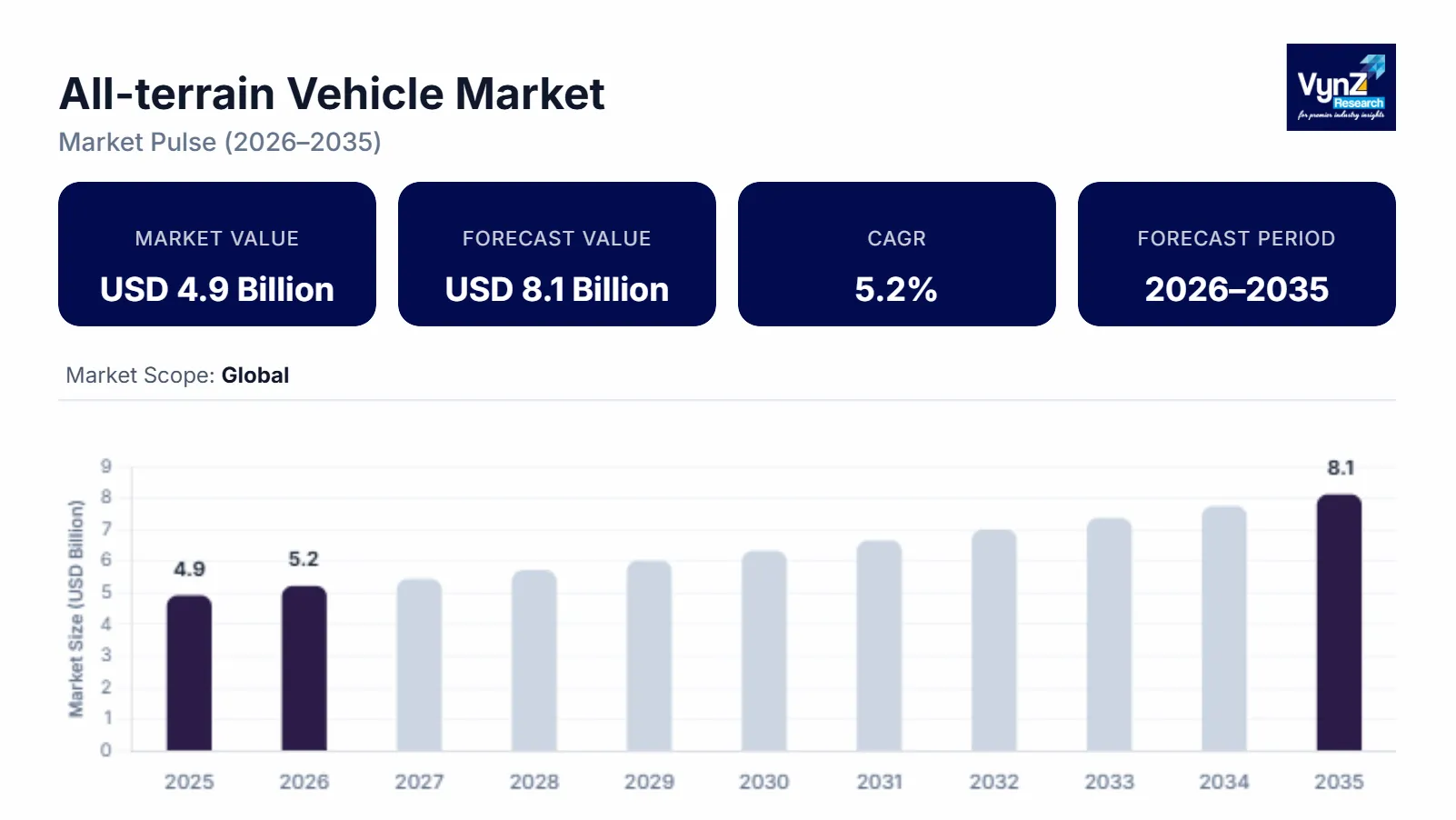

The global all-terrain vehicle market which was valued at approximately USD 4.9 billion in 2025 and is estimated to rise further up to almost USD 5.2 billion by 2026, is projected to reach around USD 8.1 billion in 2035, expanding at a CAGR of about 5.2% during the forecast period from 2026 to 2035.

Market expansion occurs because people want more recreational and outdoor utility vehicles. Also, agricultural activities now require these vehicles and defense operations need advanced mobility solutions which have become common in military and surveillance work. Major regions in Asia Pacific, North America and Europe see market growth because people want better off-road vehicles and they keep funding rural infrastructure projects and land management initiatives.

The market grows through government-backed programs and institutional research documents which provide evidence for market expansion. The Food and Agriculture Organization shows that farmers need compact utility vehicles which can operate in rough terrain because agricultural fields are becoming more mechanized according to their published data and which helps farmers to use ATVs in their work. The Stockholm International Peace Research Institute which tracks public defense spending shows that countries are increasing their acquisition of lightweight mobility platforms which will be used in tactical operations through their defense modernization initiatives. Market demand rises because agencies need effective terrain access to perform monitoring and conservation activities which they conduct through environmental and land-use management programs that support long-term market growth.

All-terrain Vehicle Market Dynamics

Market Trends

The industry is experiencing significant technological changes which impact how customers use vehicles for both work and leisure purposes. The market trend shows increasing demand for electric vehicles and low-emission vehicles which customers choose because they provide better fuel efficiency and lower environmental harm and comply with regulations. According to International Energy Agency reports off-road vehicles are becoming increasingly electrified because emission reduction goals and clean energy transition efforts are driving this change.

Growth Drivers

The market sector engineers control systems development and telematics development and durability development because these product advancements provide new competitive advantages. The all-terrain vehicle market experiences growth because agricultural and land management mechanization boosts rural demand. The market expansion receives additional support from agricultural productivity and rural infrastructure investments. The Food and Agriculture Organization reports that demand for compact farm equipment continues to grow especially in areas with land fragmentation and uneven terrain. The increase in defense and security requirements serves as a key factor driving greater adoption rates. The government agencies which need better mobility, better operational efficiency and better access to difficult terrains will drive continued demand for lightweight tactical vehicles.

Market Restraints / Challenges

The market cannot achieve its full potential because it faces multiple obstacles which prevent its expansion. High costs and regulatory requirements create challenges for users who consider price as their main purchasing factor. Environmental concerns about off-road vehicle operation have led to stricter regulations in multiple regions according to policy frameworks established by the United Nations Environment Program. The operation of manufacturing and supply chain operations faces challenges because manufacturers and suppliers rely on specific components. The market experiences disruptions when companies depend on imported parts and manufacturing inputs which increases their costs and delivery times.

Market Opportunities

The market provides substantial growth potential for electric and hybrid vehicle development because both regulatory changes and environmental awareness among consumers increase. The energy-efficient models which emit lower emissions enable companies to meet rising demand from both environmentally conscious consumers and institutional buyers. The International Energy Agency supports clean mobility initiatives which help advance sustainable vehicle technology development. The investment in premium and specialized experiences creates business opportunities in tourism, adventure sports and recreational services. The digital monitoring systems and the connected vehicle technologies will advance operational processes by improving user experiences which will increase market competition.

Global All-terrain Vehicle Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 4.9 Billion |

|

Revenue Forecast in 2035 |

USD 8.1 Billion |

|

Growth Rate |

5.2% |

|

Segments Covered in the Report |

Type, Engine Capacity, Fuel Type, Application |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Arctic Cat Inc., BRP Inc., CFMOTO, Hisun Motors Corp., Honda Motor Co., Ltd., Kawasaki Heavy Industries, Ltd., Kubota Corporation, Polaris Inc., Suzuki Motor Corporation, Yamaha Motor Co., Ltd. |

|

Customization |

Available upon request |

All-terrain Vehicle Market Segmentation

By Type

The market in 2025 reached its highest point through utility vehicles which generated about 48% of total revenue because they were used extensively in agriculture, forestry and industrial applications which required durable load-bearing vehicles. The Food and Agriculture Organization shows that farm mechanization increases which leads to higher demand for equipment that can function on small spaces and different ground types.

Sport vehicle growth rates will exceed all other vehicle categories because they will experience a 5.8% compound annual growth rate from 2026 to 2035 according to the increase in off-road recreational activities and motorsports participation. The recreational models show growth at a rate of 5.1% which tourism-related outdoor activities and consumer spending on leisure mobility solutions support.

By Engine Capacity

Mid-capacity vehicles achieved their highest market share in 2025 when they generated about 46% of total segment revenue through their value as both utility and recreational vehicles which delivered power and fuel efficiency. The segment maintains its leading position because of their widespread use in multiple types of applications.

High-capacity vehicles will achieve their fastest growth rate between 2026 and 2035 when their market will experience a 5.9% compound annual growth rate because defense operations and heavy-duty work require better torque and performance capabilities. The Stockholm International Peace Research Institute shows that mobility equipment investments are increasing which drives this business expansion. The low-capacity vehicle market grows at a steady rate of 4.8% because of its low price and demand from entry-level customers.

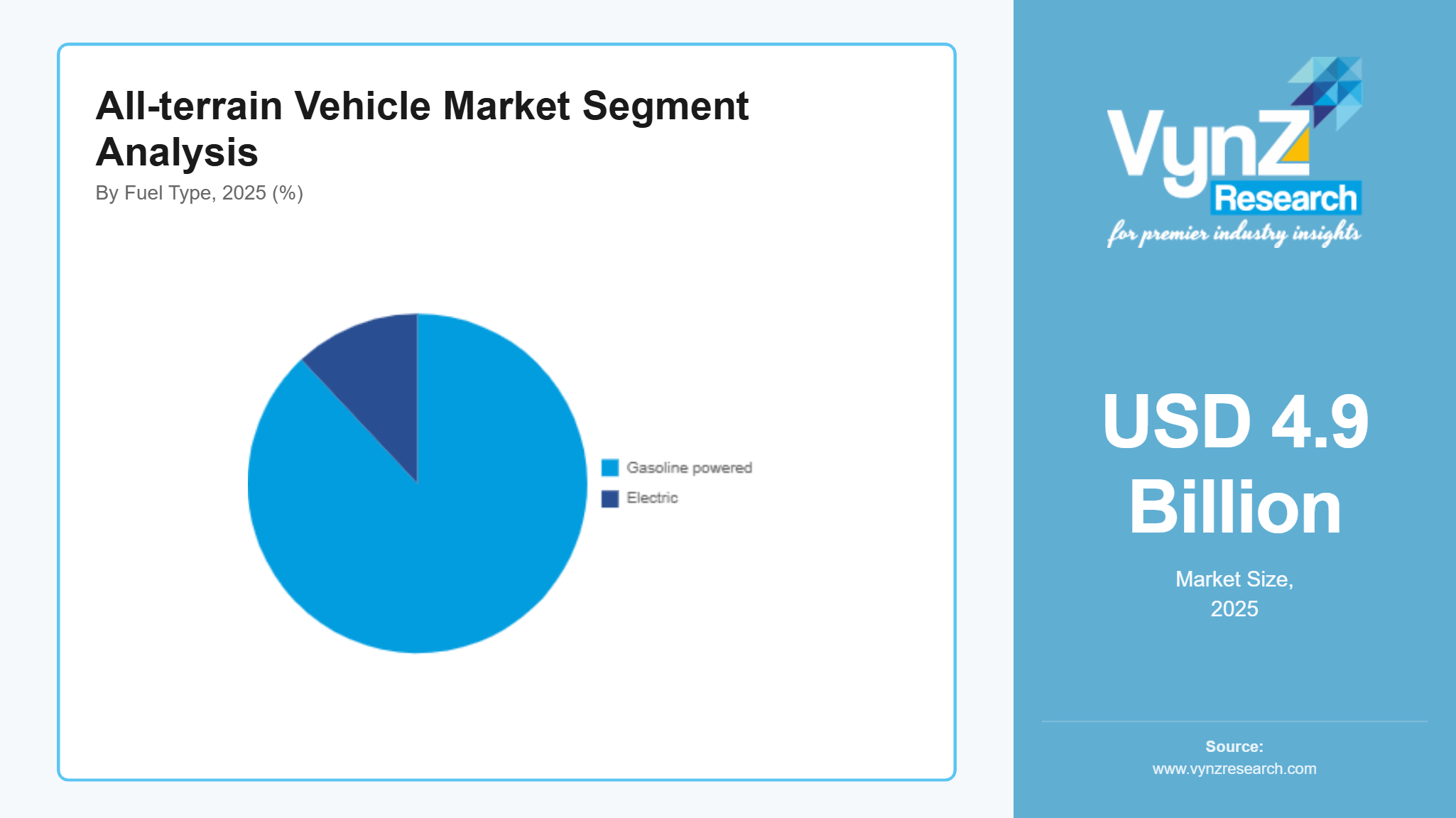

By Fuel Type

The market in 2025 was dominated by conventional fuel-powered vehicles which captured about 88% of total revenue because established infrastructure, higher power output and market availability in developed and emerging territories backed their market presence. The company maintains market control because its products provide operational reliability which functions best in heavy-duty situations.

The electric vehicle market will grow at the fastest pace when it achieves a 6.3% compound annual growth rate because regulatory bodies increasingly prioritize emissions reduction and clean energy adoption. The International Energy Agency reports that electrified mobility solutions grow in popularity for off-road segments. Government incentives and environmental policies are essential for adoption growth in environmentally sensitive regions.

By Application

Agriculture generated the highest revenue for 2025 because it represented about 42% of total market demand driven by increasing mechanization needs, land management requirements and the rising use of compact utility vehicles on uneven terrains. Government-backed agricultural productivity programs continue to drive adoption in rural areas because they support agricultural productivity in these areas.

Military applications grow the fastest because they will experience a 5.7% compound annual growth rate between 2026 and 2035 due to rising military investments in lightweight mobility platforms for tactical operations. The Stockholm International Peace Research Institute defense spending data shows that military procurement patterns remain consistent. The recreational and sports markets show growth at a rate of 5.0% because outdoor tourism and adventure activities become more popular.

Regional Insights

North America

The market reached 34% of its total value in 2025 because agriculture, defense and recreation increasingly require these vehicles. United States and Canada markets achieve high vehicle adoption because their regions have extensive off-road facilities and citizens practice outdoor activities. The United States Department of Agriculture reports that farming operations now use more mechanized equipment and utility vehicles which creates stable demand throughout rural regions.

Asia Pacific

The Asia Pacific market experienced continuous growth which results in 26% of total demand. This growth happens because agricultural activities increase and infrastructure development expands throughout China, India and Australia. The demand for products has grown because farmers, construction companies and rural workers need them. The Food and Agriculture Organization reports that emerging economies focus more on agricultural productivity through mechanization.

Europe

The European market reaches 20% of its value in 2025 because established regulations, growing agricultural and forestry use of vehicles drive market expansion. The demand for services in Germany, France and the United Kingdom grows because land management efficiency and environmental monitoring needs drive these requirements. Sustainable terrain access solutions for conservation areas and forestry operations need development according to the European Environment Agency.

Rest of the World

The rest of the world which includes Latin America, the Middle East and Africa will reach an 20% market share in 2025 because agricultural expansion increases and people start using mechanized equipment. Brazil, South Africa and the UAE experience growing demand because their infrastructure development and resource management activities drive these needs. The World Bank reports that these regions are experiencing a rise in funding for rural infrastructure and land utilization development projects.

Competitive Landscape / Company Insights

The market shows moderate competition because global and regional manufacturers compete through product development, research, price control techniques, and market expansion. Companies are increasing their research and development expenditures to strengthen their market position through advanced mobility technology investments. The International Energy Agency used industry data to show that electrification and efficiency improvements have become a major area of focus. Competitive dynamics and long-term strategic positioning of organizations in the market continue to change through strategic partnerships and portfolio diversification and emerging market entry.

Mini Profiles

Arctic Cat Inc. focuses on off-road vehicles and utility ATVs, supported by strong brand recognition, extensive dealer networks, and consistent product innovation tailored for recreational and utility users.

BRP Inc. operates in premium segments, emphasizing high-performance vehicles, advanced engineering, and strong design capabilities, supported by global distribution and a diversified powersports product portfolio.

CFMOTO leverages cost-efficient manufacturing and strategic partnerships to expand market presence, offering competitively priced ATVs and utility vehicles across emerging and developed markets.

Hisun Motors Corp. focuses on utility-focused all-terrain vehicles, supported by large-scale manufacturing capabilities, OEM partnerships, and cost-effective production strategies targeting value-driven customer segments.

Honda Motor Co., Ltd. operates across mass and premium segments, emphasizing reliability, performance, and technological innovation, supported by a strong global presence and well-established distribution infrastructure.

Key Players

- Arctic Cat Inc.

- BRP Inc.

- CFMOTO

- Hisun Motors Corp.

- Honda Motor Co., Ltd.

- Kawasaki Heavy Industries, Ltd.

- Kubota Corporation

- Polaris Inc.

- Suzuki Motor Corporation

- Yamaha Motor Co., Ltd.

Recent Developments

In February 2026, Polaris Inc. expanded its all-terrain vehicle portfolio with new models focused on improved durability and rider assistance features. The launch targets both utility and recreational users, strengthening its global product positioning.

In April 2025, Arctic Cat Inc. underwent a strategic ownership transition aimed at reviving production capabilities and strengthening its off-road vehicle lineup. The move is expected to enhance brand positioning and product innovation.

In March 2026, Honda Motor Co., Ltd. continued to enhance its ATV offerings with upgrades in engine efficiency and safety systems. The company is focusing on maintaining strong demand across utility and agricultural applications.

In October 2025, Yamaha Motor Co., Ltd. introduced updated ATV models designed for performance and off-road stability. The development aligns with increasing demand for recreational and adventure mobility solutions.

In January 2026, CFMOTO expanded its international distribution network and introduced competitively priced ATV models. The company is focusing on capturing demand across emerging markets through cost-efficient manufacturing strategies.

Global All-terrain Vehicle Market Coverage

Type Insight and Forecast 2026 - 2035

- Utility ATV

- Sport ATV

- Recreational ATV

Engine Capacity Insight and Forecast 2026 - 2035

- Below 400cc

- 400cc to 800cc

- Above 800cc

Application Insight and Forecast 2026 - 2035

- Agriculture

- Sports

- Recreational / leisure

- Military and defense

Fuel Type Insight and Forecast 2026 - 2035

- Gasoline powered

- Electric

Drive Type Insight and Forecast 2026 - 2035

- Two-wheel drive

- Four-wheel drive

- All wheel drive

Number of Wheels Insight and Forecast 2026 - 2035

- Three wheels

- Four wheels

- Six wheels

Battery Type Insight and Forecast 2026 - 2035

- Lithium ion

- Lead acid

Seating Capacity Insight and Forecast 2026 - 2035

- Single rider

- Two-seater

Global All-terrain Vehicle Market by Region

- North America

- By Type

- By Engine Capacity

- By Application

- By Fuel Type

- By Drive Type

- By Number of Wheels

- By Battery Type

- By Seating Capacity

- By Country - U.S., Canada, Mexico

- Europe

- By Type

- By Engine Capacity

- By Application

- By Fuel Type

- By Drive Type

- By Number of Wheels

- By Battery Type

- By Seating Capacity

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Type

- By Engine Capacity

- By Application

- By Fuel Type

- By Drive Type

- By Number of Wheels

- By Battery Type

- By Seating Capacity

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Type

- By Engine Capacity

- By Application

- By Fuel Type

- By Drive Type

- By Number of Wheels

- By Battery Type

- By Seating Capacity

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for All-terrain Vehicle Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Type

1.2.2. By

Engine Capacity

1.2.3. By

Application

1.2.4. By

Fuel Type

1.2.5. By

Drive Type

1.2.6. By

Number of Wheels

1.2.7. By

Battery Type

1.2.8. By

Seating Capacity

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Type

5.1.1. Utility ATV

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Sport ATV

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Recreational ATV

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Engine Capacity

5.2.1. Below 400cc

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. 400cc to 800cc

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Above 800cc

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By Application

5.3.1. Agriculture

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Sports

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Recreational / leisure

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Military and defense

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.4. By Fuel Type

5.4.1. Gasoline powered

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Electric

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.5. By Drive Type

5.5.1. Two-wheel drive

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Four-wheel drive

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. All wheel drive

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.6. By Number of Wheels

5.6.1. Three wheels

5.6.1.1. Market Definition

5.6.1.2. Market Estimation and Forecast to 2035

5.6.2. Four wheels

5.6.2.1. Market Definition

5.6.2.2. Market Estimation and Forecast to 2035

5.6.3. Six wheels

5.6.3.1. Market Definition

5.6.3.2. Market Estimation and Forecast to 2035

5.7. By Battery Type

5.7.1. Lithium ion

5.7.1.1. Market Definition

5.7.1.2. Market Estimation and Forecast to 2035

5.7.2. Lead acid

5.7.2.1. Market Definition

5.7.2.2. Market Estimation and Forecast to 2035

5.8. By Seating Capacity

5.8.1. Single rider

5.8.1.1. Market Definition

5.8.1.2. Market Estimation and Forecast to 2035

5.8.2. Two-seater

5.8.2.1. Market Definition

5.8.2.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Type

6.2. By

Engine Capacity

6.3. By

Application

6.4. By

Fuel Type

6.5. By

Drive Type

6.6. By

Number of Wheels

6.7. By

Battery Type

6.8. By

Seating Capacity

6.8.1.

U.S. Market Estimate and Forecast

6.8.2.

Canada Market Estimate and Forecast

6.8.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Type

7.2. By

Engine Capacity

7.3. By

Application

7.4. By

Fuel Type

7.5. By

Drive Type

7.6. By

Number of Wheels

7.7. By

Battery Type

7.8. By

Seating Capacity

7.8.1.

Germany Market Estimate and Forecast

7.8.2.

France Market Estimate and Forecast

7.8.3.

U.K. Market Estimate and Forecast

7.8.4.

Italy Market Estimate and Forecast

7.8.5.

Spain Market Estimate and Forecast

7.8.6.

Russia Market Estimate and Forecast

7.8.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Type

8.2. By

Engine Capacity

8.3. By

Application

8.4. By

Fuel Type

8.5. By

Drive Type

8.6. By

Number of Wheels

8.7. By

Battery Type

8.8. By

Seating Capacity

8.8.1.

China Market Estimate and Forecast

8.8.2.

Japan Market Estimate and Forecast

8.8.3.

India Market Estimate and Forecast

8.8.4.

South Korea Market Estimate and Forecast

8.8.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Type

9.2. By

Engine Capacity

9.3. By

Application

9.4. By

Fuel Type

9.5. By

Drive Type

9.6. By

Number of Wheels

9.7. By

Battery Type

9.8. By

Seating Capacity

9.8.1.

Brazil Market Estimate and Forecast

9.8.2.

Saudi Arabia Market Estimate and Forecast

9.8.3.

South Africa Market Estimate and Forecast

9.8.4.

U.A.E. Market Estimate and Forecast

9.8.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Arctic Cat Inc.

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

BRP Inc.

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

CFMOTO

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Hisun Motors Corp.

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Honda Motor Co., Ltd.

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Kawasaki Heavy Industries, Ltd.

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Kubota Corporation

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Polaris Inc.

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Suzuki Motor Corporation

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Yamaha Motor Co., Ltd.

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

All-terrain Vehicle Market