Automotive Radar Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Range (Short and Medium Range Radar, Long Range Radar), by Frequency Band (77 GHz, 79 GHz), by Vehicle Type (Passenger Vehicles, Commercial Vehicles), by Application (Adaptive Cruise Control, Forward Collision Warning, Autonomous Emergency Braking, Parking Assistance Systems), by End User (Original Equipment Manufacturers, Aftermarket)

| Status : Published | Published On : Apr, 2026 | Report Code : VRAT9673 | Industry : Automotive & Transportation | Available Format :

|

Page : 195 |

Automotive Radar Market Overview

The global automotive radar market which was valued at approximately USD 6.10 billion in 2025 and is estimated to rise further up to almost USD 7.95 billion by 2026, is projected to reach around USD 62.40 billion in 2035, expanding at a CAGR of about 25% during the forecast period from 2026 to 2035.

The market expansion occurs because advanced driver assistance system implementation increases, vehicle safety regulation requirements become more demanding, and connected vehicle production rises, along with growing autonomous driving technology adoption. The market expansion across major regions including the United States, Germany, and China, receives additional support from the increasing need for better collision avoidance systems, and ongoing development of smart transportation systems.

The growth trajectory receives additional support from government-backed organizations which establish regulatory requirements and road safety programs. The United States National Highway Traffic Safety Administration and the European Commission established safety frameworks which promote the use of radar-based driver assistance systems in both passenger and commercial vehicles. International road safety organizations have published data which demonstrates that advanced sensing technologies have become essential for reducing traffic fatalities, leading to increased technology usage. The ongoing demand from crucial worldwide markets receives support from public investments in smart mobility ecosystems, which remain essential because automotive manufacturers focus on safety compliance and electric vehicle development.

Automotive Radar Market Dynamics

Market Trends

The industry is experiencing significant changes because companies are starting to use new technologies while they buy products according to their needs for intelligent mobility and safety-focused vehicle development. The market is experiencing its most important development through high-resolution radar system integration, which shows market demand for improved detection performance, immediate data processing, and all-weather operational capability. The government-backed road safety framework, which includes National Highway Traffic Safety Administration and European Commission support, establishes advanced sensing technologies as essential tools to decrease collision hazards while enhancing vehicle safety results. These initiatives are increasing the number of multi-mode radar systems that passenger vehicles and commercial vehicles use in their operations.

The automotive electronics field and digital infrastructure development drive the market for radar systems to combine with artificial intelligence and sensor fusion technologies. The market forces companies to create all-in-one sensing technologies that use radar together with cameras and lidar systems for complete environmental awareness. Chinese Ministry of Industry and Information Technology authorities support public mobility programs and smart transportation initiatives, which help cities implement autonomous systems and their semi-autonomous counterparts while making mobility systems more efficient and dependable.

Growth Drivers

The market experiences its main growth from advanced driver assistance systems, which require this technology in all vehicle types. The market for automotive radar systems experiences rapid growth because vehicle manufacturers are making more investments into manufacturing facilities and electrification infrastructure and smart transportation systems. The regulatory sector drives vehicle manufacturers to include safety systems, which include automatic emergency braking and blind spot detection, resulting in increased radar system use across all vehicle types. International transport and safety organizations established global road safety targets, which the regulatory measures follow to create ongoing market demand.

The development of connected and autonomous vehicle ecosystems drives market growth because it results in increased demand for these technologies. The automotive industry will maintain strong demand for radar-based sensing solutions because safety compliance and operational efficiency drive their use in real-time data systems throughout the entire forecasting period. Public investment programs in the United States, Germany, and China, which fund vehicle electrification and intelligent transport systems, are advancing infrastructure development while making it easier to use advanced sensing technologies in urban spaces and on highways.

Market Restraints / Challenges

The market has strong growth potential, but it encounters multiple obstacles that will restrict its market development. High system costs and complex designs make it difficult for emerging markets to adopt products, which affects all vehicle segments except for higher-end models. The production of advanced radar modules requires costly semiconductor components, which limits their use in entry-level vehicle segments because of its expensive manufacturing process. Government-backed industry assessments show that smaller manufacturers require substantial financial and technical resources to implement high-performance sensing technologies.

The semiconductor supply chain requires specialized electronic components, which make it hard for manufacturers and suppliers to operate when their business depends on those components. Trade and industry monitoring agencies have reported that global supply network interruptions create production delays and cost increases. The development of automotive safety certifications and electromagnetic compatibility standards leads to additional regulatory requirements, which extend development times and make operational procedures more difficult. The combination of these factors affects market growth because they decrease business adaptability during economic and industrial downturns.

Market Opportunities

The market provides major opportunities through the development of autonomous and semi-autonomous vehicle technologies, which receive increasing support from investment in smart mobility and digital infrastructure. Companies with high-performance scalable radar solutions will capture new business opportunities from automotive manufacturers and mobility service providers who require advanced safety and navigation systems. Government-supported programs that promote intelligent transport systems and vehicle automation create favorable conditions for technology adoption in rapidly urbanizing regions.

The development of cost-optimized and miniaturized radar systems exists as a major market opportunity, which semiconductor technologies and system integration progress will enable to expand into mid-range and entry-level vehicle markets. The increase in electric vehicle investment will lead to more radar-based solutions used in connected mobility platforms, which will create business opportunities that support sustainable growth. Public sector programs that support sustainable transportation and digital connectivity together with infrastructure funding and regulatory incentives will drive up adoption rates while enabling companies to build extended global partnerships and research networks in automotive ecosystems.

Global Automotive Radar Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 6.10 Billion |

|

Revenue Forecast in 2035 |

USD 62.40 Billion |

|

Growth Rate |

25% |

|

Segments Covered in the Report |

Range, Frequency Band, Vehicle Type, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Aptiv, Autoliv Inc., Continental AG, Denso Corporation, HELLA GmbH & Co. KGaA, Infineon Technologies AG, NXP Semiconductors, Robert Bosch GmbH, Texas Instruments Incorporated, Valeo |

|

Customization |

Available upon request |

Automotive Radar Market Segmentation

By Range

The market in 2025 received its greatest revenue share from short and medium range radar systems, which generated approximately 58% of total market revenue. The system remains dominant because it operates in vital safety features, which include blind spot detection and parking assistance and collision warning systems. The design provides cost effective solutions in a compact package, which results in high volume adoption by both developed markets and emerging automotive markets.

The market for long range radar systems will experience the highest growth rate, which shows an estimated compound annual growth rate of 26.8% from 2026 to 2035. The market for cruise control systems and highway autopilot functions grows because autonomous driving technologies and highway safety regulatory framework become more widely used. The rising investments in connected vehicle ecosystems and intelligent transportation infrastructure propel deployment across premium vehicle and electric vehicle segments.

By Frequency Band

The 77 GHz frequency band held the largest market share in 2025, which generated about 61% of the total revenue for that market segment. The market leader position of the product continues because it provides users with better resolution and better object detection and meets all worldwide automotive safety regulations. The standardization of radar systems in this frequency range occurred because manufacturers wanted to comply with regulatory requirements which applied to major markets such as Europe and Asia Pacific. The advanced driver assistance systems market continues to grow because the industry needs precise sensing technologies for its operations.

The 79 GHz band will achieve the highest growth rate between 2026 and 2035, which will produce a compound annual growth rate of 27.4%. The system achieves growth because its better bandwidth capacity enables users to produce higher resolution images, which improves detection performance in challenging driving conditions. The testing expansion of autonomous vehicles and government-supported initiatives which promote intelligent mobility research have both increased the adoption of advanced high-frequency radar systems in next-generation vehicles.

By Vehicle Type

The market for passenger vehicles generated the largest revenue in 2025, which represented 64% of the total market revenue. The market leader position occurs because high production rates enable automotive manufacturers to meet increasing customer demand for safety features, which automotive regulators require all new vehicles to have advanced driver assistance systems. The public safety programs which governments fund and the increased public knowledge about collision avoidance technologies support their widespread usage in cities and suburban residential areas.

The commercial vehicle market will achieve the highest growth rate, which will produce a compound annual growth rate of 25.9% from 2026 to 2035. The market growth occurs because companies modernize their fleets while they need better logistics operations and they must follow rules which protect driver safety in heavy-duty transportation. The public sector uses digital fleet management systems and road safety enforcement solutions to guide businesses towards adopting radar technology for their operations.

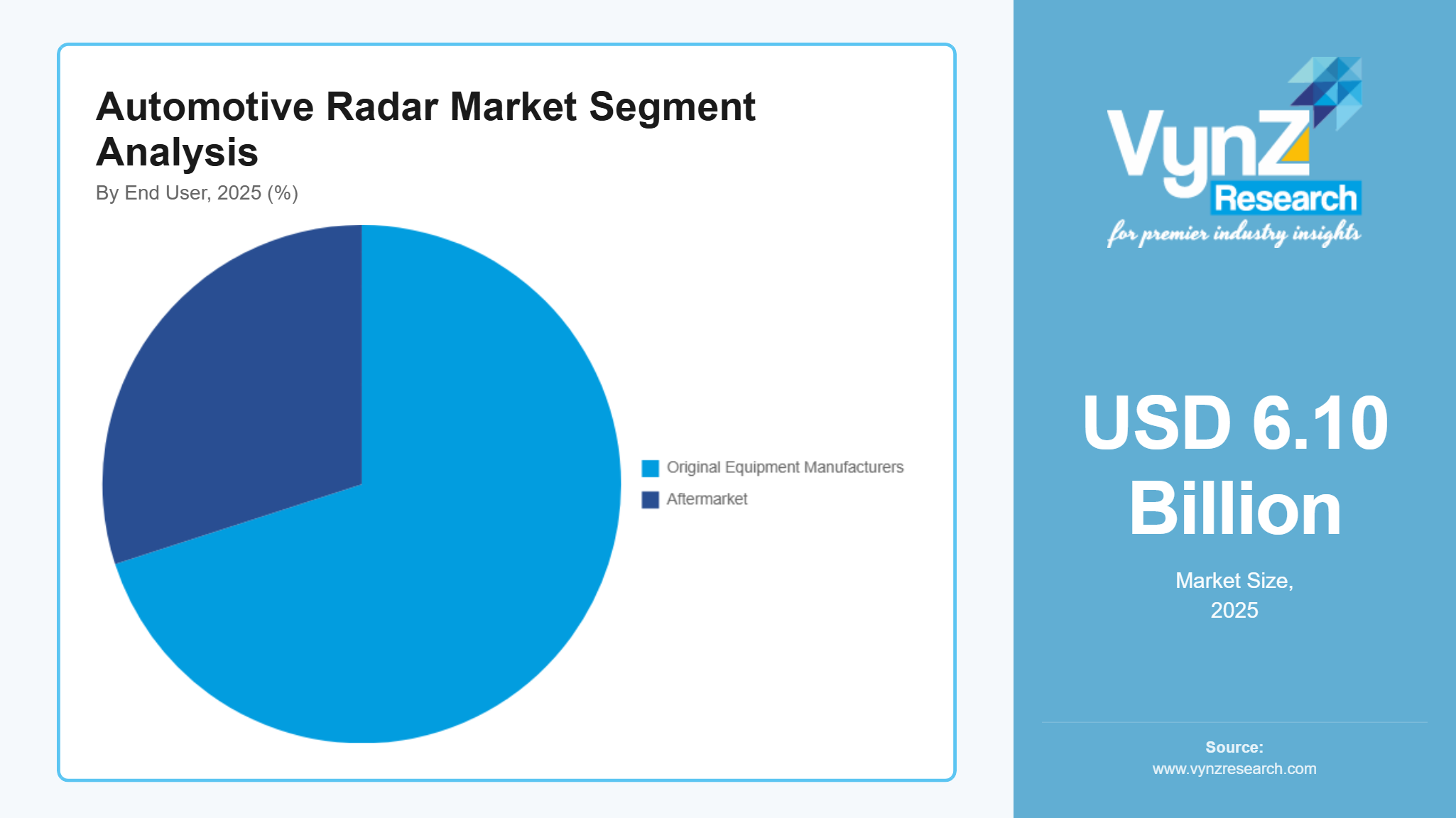

By End User

The largest market segment in 2025 belonged to original equipment manufacturers, who generated 72% of total market revenue. The company maintains its market share because it connects radar systems to vehicle production, which helps businesses meet safety standards while they invest in advanced automotive solutions. The security mandates which governments implement for automotive safety and business standards drive original equipment manufacturers to use radar systems across different vehicle types while maintaining their market leadership position.

The aftermarket segment will show growth with a compound annual growth rate of 24.6% between 2026 and 2035. The market growth occurs because vehicle owners need safety systems for existing vehicles and people want to know more about advanced driver assistance technologies and service networks are becoming more widespread. Government programs which support vehicle safety improvements and safety inspection procedures have both fueled the ongoing growth of this market segment.

Regional Insights

North America

The market in 2025 saw North America generate about 30% of its total market value through regulatory enforcement and advanced automotive manufacturing capabilities and vehicle safety technology implementation. The market shows ongoing growth because people in Detroit, California and Texas keep buying more passenger vehicles and premium cars. The National Highway Traffic Safety Administration together with other regulatory agencies has established safety requirements which need automatic emergency braking systems to be included in all new vehicle designs thus boosting the need for radar systems in those vehicles.

Europe

Europe provided approximately 28% of the market value in 2025 because European countries maintain strict vehicle safety standards and their automotive engineering expertise extends from Germany to France and the United Kingdom. The need for radar systems remains strong because both passenger and commercial vehicle markets experience increasing demand as safety requirements become stricter under local regulations. The European Commission has introduced mandatory safety features for new vehicles, which has resulted in faster radar deployment across both mid-range and premium vehicle categories.

Asia Pacific

The market in Asia Pacific reached about 22% of its total size by 2025 because China, India and Japan experience fast automobile manufacturing and urban development together with increased safety technology usage. The primary vehicle and technology centers in Beijing, Shanghai and Tokyo serve as essential locations for radar system implementation which covers multiple vehicle types. The Chinese government through its Ministry of Industry and Information Technology is promoting the establishment of intelligent vehicle systems and smart mobility solutions.

Rest of the World

The market for 2025 shows that Latin America with the Middle East plus Africa control 20% of the total market share. The regions experience expansion because more people acquire vehicles while new infrastructure projects start and people use safety technologies in their urban environments. Premium vehicle segments in Brazil, United Arab Emirates and South Africa are starting to adopt radar systems at their initial stages of development. The adoption of government-sponsored transport modernization initiatives and road safety programs is advancing at a slower rate compared to established markets.

Competitive Landscape / Company Insights

The market has intense competition because established global manufacturers and new regional businesses compete through technological innovations, lower costs and increased market reach. Companies enhance their market power through research and development and semiconductor technology and sensor integration development. The National Highway Traffic Safety Administration and European Commission establish regulatory frameworks and safety standards which drive companies to upgrade their products continuously while they develop high-frequency radar systems and driver assistance technology.

Mini Profiles

Aptiv focuses on advanced mobility solutions and vehicle safety technologies, supported by strong global automotive integration capabilities and innovation in autonomous driving systems enhancing connected vehicle performance and sensing efficiency.

Robert Bosch GmbH operates in premium automotive technology segments, emphasizing radar systems, driver assistance solutions, and engineering excellence supported by strong global manufacturing networks and established automotive supplier relationships.

Continental AG leverages strategic partnerships and advanced automotive electronics capabilities to expand market presence, focusing on radar integration, safety systems, and mobility technologies across passenger and commercial vehicle applications.

Denso Corporation focuses on automotive sensing and electronic systems, supported by strong Japanese manufacturing excellence, high reliability engineering, and deep integration with global automotive OEM supply chains.

Valeo operates in advanced automotive technology segments, emphasizing innovation in radar sensors and driver assistance systems supported by strong R&D capabilities and global automotive collaboration networks.

Key Players

- Aptiv

- Autoliv Inc.

- Continental AG

- Denso Corporation

- HELLA GmbH & Co. KGaA

- Infineon Technologies AG

- NXP Semiconductors

- Robert Bosch GmbH

- Texas Instruments Incorporated

- Valeo

Recent Developments

In February 2025, ZF Friedrichshafen AG expanded its radar-based ADAS portfolio by enhancing long-range sensing modules for Level 2+ and Level 3 autonomous driving applications. The company highlighted improved integration of radar with vehicle motion control systems to strengthen safety performance and regulatory compliance across European and global markets.

In March 2025, Infineon Technologies AG announced advancements in automotive radar semiconductor solutions designed for high-frequency 77 GHz and 79 GHz applications. The development focused on improving energy efficiency and processing speed, supporting next-generation driver assistance systems aligned with global vehicle safety standards.

In April 2025, Texas Instruments Incorporated introduced upgraded radar signal processing chipsets aimed at improving object detection accuracy and real-time responsiveness in automotive applications. The company emphasized enhanced scalability for mass-market ADAS deployment across passenger and commercial vehicle platforms.

In June 2025, Hella GmbH & Co. KGaA strengthened its automotive radar component manufacturing capabilities with a focus on compact sensor modules for urban mobility applications. The company highlighted increased collaboration with OEMs to support cost-efficient integration of radar systems in mid-range vehicle segments.

In July 2025, Autoliv Inc. expanded its active safety technology offerings by integrating radar-enabled collision mitigation systems into its next-generation safety platforms. The company emphasized improved sensor fusion capabilities supporting enhanced occupant protection and compliance with evolving global automotive safety regulations.

Global Automotive Radar Market Coverage

Range Insight and Forecast 2026 - 2035

- Short and Medium Range Radar

- Long Range Radar

Frequency Band Insight and Forecast 2026 - 2035

- 77 GHz

- 79 GHz

Vehicle Type Insight and Forecast 2026 - 2035

- Passenger Vehicles

- Commercial Vehicles

Application Insight and Forecast 2026 - 2035

- Adaptive Cruise Control

- Forward Collision Warning

- Autonomous Emergency Braking

- Parking Assistance Systems

End User Insight and Forecast 2026 - 2035

- Original Equipment Manufacturers

- Aftermarket

Global Automotive Radar Market by Region

- North America

- By Range

- By Frequency Band

- By Vehicle Type

- By Application

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Range

- By Frequency Band

- By Vehicle Type

- By Application

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Range

- By Frequency Band

- By Vehicle Type

- By Application

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Range

- By Frequency Band

- By Vehicle Type

- By Application

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Automotive Radar Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Range

1.2.2. By

Frequency Band

1.2.3. By

Vehicle Type

1.2.4. By

Application

1.2.5. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Range

5.1.1. Short and Medium Range Radar

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Long Range Radar

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.2. By Frequency Band

5.2.1. 77 GHz

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. 79 GHz

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Vehicle Type

5.3.1. Passenger Vehicles

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Commercial Vehicles

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By Application

5.4.1. Adaptive Cruise Control

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Forward Collision Warning

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Autonomous Emergency Braking

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Parking Assistance Systems

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.5. By End User

5.5.1. Original Equipment Manufacturers

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Aftermarket

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Range

6.2. By

Frequency Band

6.3. By

Vehicle Type

6.4. By

Application

6.5. By

End User

6.5.1.

U.S. Market Estimate and Forecast

6.5.2.

Canada Market Estimate and Forecast

6.5.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Range

7.2. By

Frequency Band

7.3. By

Vehicle Type

7.4. By

Application

7.5. By

End User

7.5.1.

Germany Market Estimate and Forecast

7.5.2.

France Market Estimate and Forecast

7.5.3.

U.K. Market Estimate and Forecast

7.5.4.

Italy Market Estimate and Forecast

7.5.5.

Spain Market Estimate and Forecast

7.5.6.

Russia Market Estimate and Forecast

7.5.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Range

8.2. By

Frequency Band

8.3. By

Vehicle Type

8.4. By

Application

8.5. By

End User

8.5.1.

China Market Estimate and Forecast

8.5.2.

Japan Market Estimate and Forecast

8.5.3.

India Market Estimate and Forecast

8.5.4.

South Korea Market Estimate and Forecast

8.5.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Range

9.2. By

Frequency Band

9.3. By

Vehicle Type

9.4. By

Application

9.5. By

End User

9.5.1.

Brazil Market Estimate and Forecast

9.5.2.

Saudi Arabia Market Estimate and Forecast

9.5.3.

South Africa Market Estimate and Forecast

9.5.4.

U.A.E. Market Estimate and Forecast

9.5.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Aptiv

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Autoliv Inc.

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Continental AG

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Denso Corporation

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

HELLA GmbH & Co. KGaA

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Infineon Technologies AG

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

NXP Semiconductors

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Robert Bosch GmbH

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Texas Instruments Incorporated

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Valeo

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Automotive Radar Market